Case Study: Business Merger Impact on Profitability & Income Taxes

VerifiedAdded on 2023/06/07

|9

|1815

|421

Case Study

AI Summary

This case study investigates the impact of business mergers on the profitability and income taxes of CPA firms, specifically examining the merger of Moore Stevens into BDO. The study uses financial ratio analysis to compare BDO's performance before (2018) and after (2019) the merger. The results indicate a significant impact on profitability metrics such as operating profit ratio and return on investment, alongside a decrease in income tax payments. The study concludes that mergers can be a beneficial strategy for growth, provided that fairness, negotiation, and the reputation of the merging parties are carefully considered. Desklib provides access to this case study and many other solved assignments and past papers.

The Impact of Business

Merger on the Profitability

and income Taxes : case study

of two CPA firms

Merger on the Profitability

and income Taxes : case study

of two CPA firms

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ABSTRACT

Merger & Acquisitions are two distinct terms in business that describes the consolidations

between companies through different ways. The study investigates the role impact of mergers

and acquisitions over the profitability of companies.

Merger & Acquisitions are two distinct terms in business that describes the consolidations

between companies through different ways. The study investigates the role impact of mergers

and acquisitions over the profitability of companies.

Table of Contents

Purpose............................................................................................................................................4

Introduction......................................................................................................................................4

Hypothesis.......................................................................................................................................4

Literature Review............................................................................................................................4

Methodology of the study................................................................................................................5

Conclusion.......................................................................................................................................8

Recommendations............................................................................................................................8

REFERENCES................................................................................................................................1

Purpose............................................................................................................................................4

Introduction......................................................................................................................................4

Hypothesis.......................................................................................................................................4

Literature Review............................................................................................................................4

Methodology of the study................................................................................................................5

Conclusion.......................................................................................................................................8

Recommendations............................................................................................................................8

REFERENCES................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purpose

The aim of the study is to examine the impact of Business Merger on the Profitability and

income taxes. The purpose of the study is to enhance the knowledge of merger and acquisition

and its effect over the profits and the income tax payments of the company.

Study Problem

The problem to which the current study deals with is whether the companies should use

merger and acquisition into its planning for the growth perspectives.

Significance of Study

The significance of the study’s topic is that it helps businesses majorly to explore wide

range of products and services that can satisfy consumer needs and increase the market share and

profits.

Introduction

There are a multiple number of reasons like increasing the profitability, growth of market

shares in numbers and price, to achieve the compatibility to pay dividends regularly, etc. that

indulges companies into mergers over the years. Reported that a merger can be looked upon as a

situation where two or more companies come together in order to combine, forming bigger

organization. According to Singh and Das (2018) a merger is a kind of business transaction that

is made with the purpose of making a new single entity from multiple business entities that are

already existing. Further Brooks, Chen and Zeng (2018) noted that the problem in efficiently

using limited resources can be countered along with hiking the competitiveness and performance

of a company. The method is considered as the best way for expanding the market share/

ownership according to Christofi and et.al (2019).

Financial theories are studied for analysing the positive as well as negative impacts that

mergers entail over corporative firms. A merger can on one hand help a company by enhancing

its liquidity and on the side can impact financial performance & profitability negatively. There

are three types of mergers namely, horizontal, vertical & conglomerate.

The aim of the study is to examine the impact of Business Merger on the Profitability and

income taxes. The purpose of the study is to enhance the knowledge of merger and acquisition

and its effect over the profits and the income tax payments of the company.

Study Problem

The problem to which the current study deals with is whether the companies should use

merger and acquisition into its planning for the growth perspectives.

Significance of Study

The significance of the study’s topic is that it helps businesses majorly to explore wide

range of products and services that can satisfy consumer needs and increase the market share and

profits.

Introduction

There are a multiple number of reasons like increasing the profitability, growth of market

shares in numbers and price, to achieve the compatibility to pay dividends regularly, etc. that

indulges companies into mergers over the years. Reported that a merger can be looked upon as a

situation where two or more companies come together in order to combine, forming bigger

organization. According to Singh and Das (2018) a merger is a kind of business transaction that

is made with the purpose of making a new single entity from multiple business entities that are

already existing. Further Brooks, Chen and Zeng (2018) noted that the problem in efficiently

using limited resources can be countered along with hiking the competitiveness and performance

of a company. The method is considered as the best way for expanding the market share/

ownership according to Christofi and et.al (2019).

Financial theories are studied for analysing the positive as well as negative impacts that

mergers entail over corporative firms. A merger can on one hand help a company by enhancing

its liquidity and on the side can impact financial performance & profitability negatively. There

are three types of mergers namely, horizontal, vertical & conglomerate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hypothesis

H01 = There is no major distinction in the profitability of chosen CPA businesses for the period

before & after merger.

H02 = There exists no significant change over the taxes of selected CPA companies pre & post-

merger.

Literature Review

The available literature highlighted many tools technique for analysing the effects of

merger, Analysis of financial ratios to find out the effects of mergers.

Positive impacts of merger on profitability

On systematic assessment and evaluation of researched 150 articles related to financial

mergers and acquisition it was found that efficiency level was affected positively by the mergers

of North American Bank. Literary works has also revealed a situation of creation of wealthy

which concerns the stakeholders shown by the mixed picture. Literature of European bank

related to the merger showed gains in the efficiency along with improvement in the value for

stockholders. Diversification with respect to the product and geography impacted in mixed sense

via merger whereas, adverse impacts were revealed on the types of borrowers, external

stakeholders and depositors shown by mergers of the financial institutions. Brueller, Carmeli and

Markman (2018).

It has been found that the efficiency related to the cost and profits affected the merger

events in the banking sector in the US sector of banking by utilization of the SFA (Stochastic

Frontier Approach) and DEA (Data Envelopment Analysis which includes studying the merged

and non-merged banks’ structure of production. An improved efficiency of cost and profit was

depicted post-merger. Additionally, higher costs were revealed for the non – merged banks as

compared to the merged banks reason being, the focus of such merged bank is on technical and

well located efficiency.

According to Welch and et.al (2020) a merger has its positive impact over the

organizations in the form of increase in revenue that is achieved as a result of deduction in the

costs. The market share potential of the company increases in both the domestic market and also

the foreign market where the new consumers seeks for such merger firm’s products and services.

Mergers leads to reduction in competition that significantly helps in increasing profitability.

H01 = There is no major distinction in the profitability of chosen CPA businesses for the period

before & after merger.

H02 = There exists no significant change over the taxes of selected CPA companies pre & post-

merger.

Literature Review

The available literature highlighted many tools technique for analysing the effects of

merger, Analysis of financial ratios to find out the effects of mergers.

Positive impacts of merger on profitability

On systematic assessment and evaluation of researched 150 articles related to financial

mergers and acquisition it was found that efficiency level was affected positively by the mergers

of North American Bank. Literary works has also revealed a situation of creation of wealthy

which concerns the stakeholders shown by the mixed picture. Literature of European bank

related to the merger showed gains in the efficiency along with improvement in the value for

stockholders. Diversification with respect to the product and geography impacted in mixed sense

via merger whereas, adverse impacts were revealed on the types of borrowers, external

stakeholders and depositors shown by mergers of the financial institutions. Brueller, Carmeli and

Markman (2018).

It has been found that the efficiency related to the cost and profits affected the merger

events in the banking sector in the US sector of banking by utilization of the SFA (Stochastic

Frontier Approach) and DEA (Data Envelopment Analysis which includes studying the merged

and non-merged banks’ structure of production. An improved efficiency of cost and profit was

depicted post-merger. Additionally, higher costs were revealed for the non – merged banks as

compared to the merged banks reason being, the focus of such merged bank is on technical and

well located efficiency.

According to Welch and et.al (2020) a merger has its positive impact over the

organizations in the form of increase in revenue that is achieved as a result of deduction in the

costs. The market share potential of the company increases in both the domestic market and also

the foreign market where the new consumers seeks for such merger firm’s products and services.

Mergers leads to reduction in competition that significantly helps in increasing profitability.

Further Argentesi and et.al (2021) highlights some of the elements that needs to be

considered for effective merger. To begin with the merger partner should be first ensured for the

suitability of coming together and merge. There should be trust between the parties for the

smooth negotiation. The valuation should be good considered with diligence. The experience

from the past mergers & acquisitions should always serve as a guide for efficacy in future

dealings.

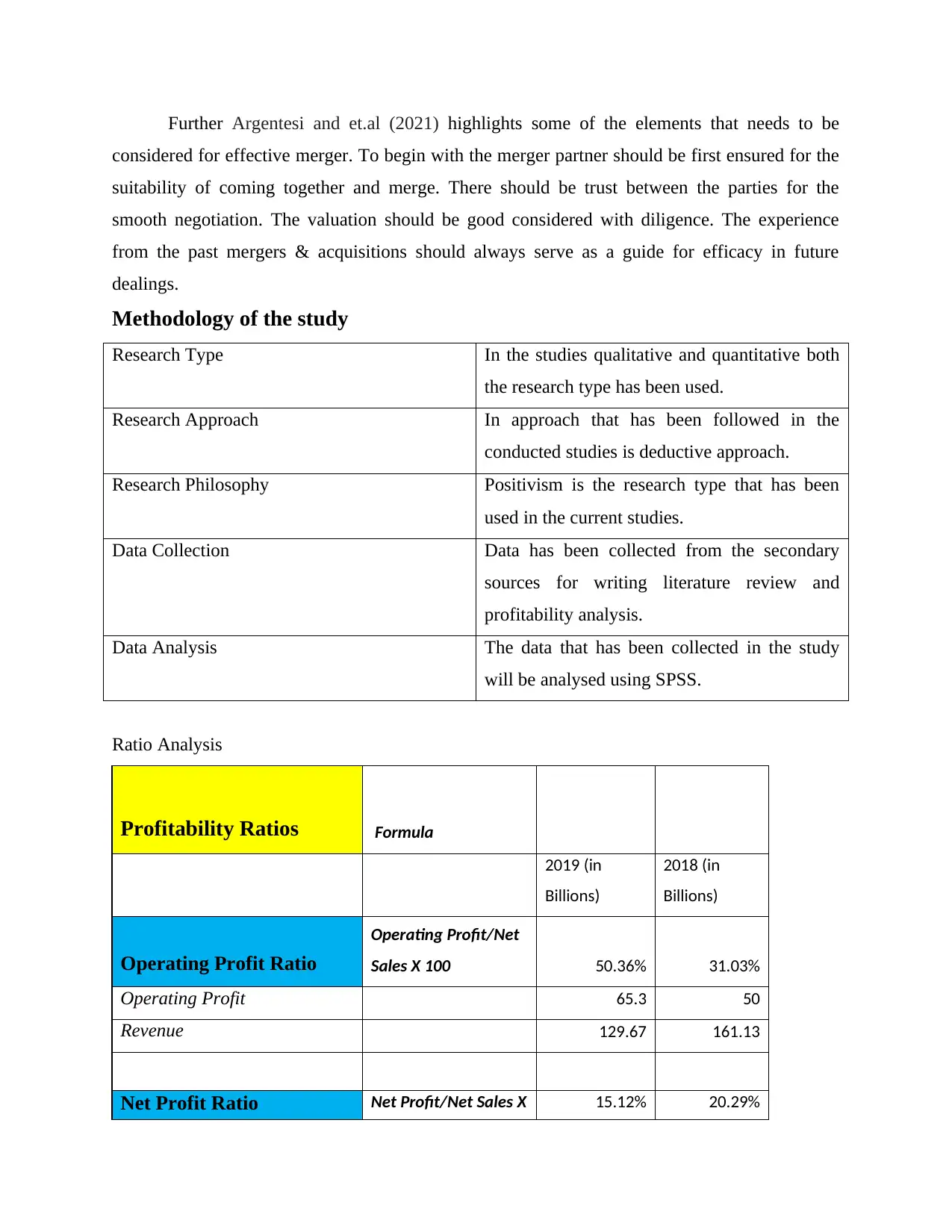

Methodology of the study

Research Type In the studies qualitative and quantitative both

the research type has been used.

Research Approach In approach that has been followed in the

conducted studies is deductive approach.

Research Philosophy Positivism is the research type that has been

used in the current studies.

Data Collection Data has been collected from the secondary

sources for writing literature review and

profitability analysis.

Data Analysis The data that has been collected in the study

will be analysed using SPSS.

Ratio Analysis

Profitability Ratios Formula

2019 (in

Billions)

2018 (in

Billions)

Operating Profit Ratio

Operating Profit/Net

Sales X 100 50.36% 31.03%

Operating Profit 65.3 50

Revenue 129.67 161.13

Net Profit Ratio Net Profit/Net Sales X 15.12% 20.29%

considered for effective merger. To begin with the merger partner should be first ensured for the

suitability of coming together and merge. There should be trust between the parties for the

smooth negotiation. The valuation should be good considered with diligence. The experience

from the past mergers & acquisitions should always serve as a guide for efficacy in future

dealings.

Methodology of the study

Research Type In the studies qualitative and quantitative both

the research type has been used.

Research Approach In approach that has been followed in the

conducted studies is deductive approach.

Research Philosophy Positivism is the research type that has been

used in the current studies.

Data Collection Data has been collected from the secondary

sources for writing literature review and

profitability analysis.

Data Analysis The data that has been collected in the study

will be analysed using SPSS.

Ratio Analysis

Profitability Ratios Formula

2019 (in

Billions)

2018 (in

Billions)

Operating Profit Ratio

Operating Profit/Net

Sales X 100 50.36% 31.03%

Operating Profit 65.3 50

Revenue 129.67 161.13

Net Profit Ratio Net Profit/Net Sales X 15.12% 20.29%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

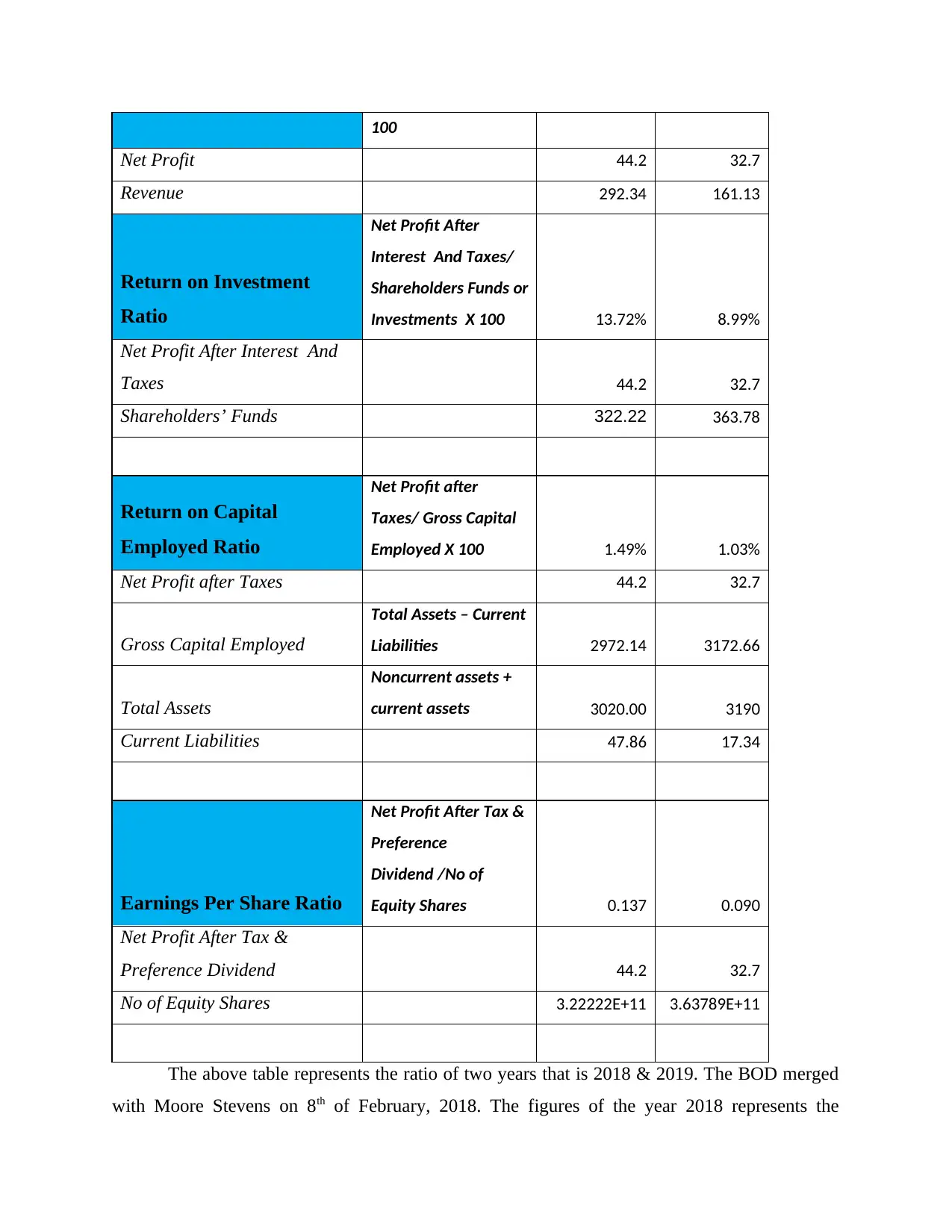

100

Net Profit 44.2 32.7

Revenue 292.34 161.13

Return on Investment

Ratio

Net Profit After

Interest And Taxes/

Shareholders Funds or

Investments X 100 13.72% 8.99%

Net Profit After Interest And

Taxes 44.2 32.7

Shareholders’ Funds 322.22 363.78

Return on Capital

Employed Ratio

Net Profit after

Taxes/ Gross Capital

Employed X 100 1.49% 1.03%

Net Profit after Taxes 44.2 32.7

Gross Capital Employed

Total Assets – Current

Liabilities 2972.14 3172.66

Total Assets

Noncurrent assets +

current assets 3020.00 3190

Current Liabilities 47.86 17.34

Earnings Per Share Ratio

Net Profit After Tax &

Preference

Dividend /No of

Equity Shares 0.137 0.090

Net Profit After Tax &

Preference Dividend 44.2 32.7

No of Equity Shares 3.22222E+11 3.63789E+11

The above table represents the ratio of two years that is 2018 & 2019. The BOD merged

with Moore Stevens on 8th of February, 2018. The figures of the year 2018 represents the

Net Profit 44.2 32.7

Revenue 292.34 161.13

Return on Investment

Ratio

Net Profit After

Interest And Taxes/

Shareholders Funds or

Investments X 100 13.72% 8.99%

Net Profit After Interest And

Taxes 44.2 32.7

Shareholders’ Funds 322.22 363.78

Return on Capital

Employed Ratio

Net Profit after

Taxes/ Gross Capital

Employed X 100 1.49% 1.03%

Net Profit after Taxes 44.2 32.7

Gross Capital Employed

Total Assets – Current

Liabilities 2972.14 3172.66

Total Assets

Noncurrent assets +

current assets 3020.00 3190

Current Liabilities 47.86 17.34

Earnings Per Share Ratio

Net Profit After Tax &

Preference

Dividend /No of

Equity Shares 0.137 0.090

Net Profit After Tax &

Preference Dividend 44.2 32.7

No of Equity Shares 3.22222E+11 3.63789E+11

The above table represents the ratio of two years that is 2018 & 2019. The BOD merged

with Moore Stevens on 8th of February, 2018. The figures of the year 2018 represents the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance of company for the pre- merger period and the values of 2019 taken represents the

post – merger profitability of the company. Operating profit ratio of the company hiked from

31.03 % in the previous year to 50.36 % in the current year. The net profit ratio shows a decrease

of five –percent approximately. Another major determinant of a company’s progress and

profitability is through its return on the money put in for carrying out the activities of the

business. The year 2018 BOD seen an investment return ratio as nearly 9% and in the year 2019

this jumped to 14% approximately. It can be said that the company’s potentiality of receive

investments increased. There is also an increase in the EPS of the company. 0.44% of increase is

seen in the return on capital employed making the shareholders’ investment more worthy.

Income tax for the year 2018 was 15.02 B and year 2019 income tax was 11.01 B. it shows a

decline of 4.01 B.

Conclusion

On the basis of the studies it can be concluded that there is a significant impact that an

organization experiences in its profitability and tax payments in situation of mergers. The study

has selected two CPA firms one is BDO and the other is Moore Stevens. The later merged into

the former in the year 2019. For analysing the impact of merger on BDO the financial statements

of the company have been analysed in the studies for the years 2018 & 2019.

Recommendations

On the basis of the studies it can be recommended to the company that mergers are one of

the best ways through which it can experience good growth by combating all the challenges. To

have successful mergers certain points are suggested to the company firstly it should ensure

fairness to all the parties in the process the negotiation must be completely justifiable. It should

be noted that the selected must be reputed in the market as reputation of the company plays a

major role behind the successful and effective merger.

post – merger profitability of the company. Operating profit ratio of the company hiked from

31.03 % in the previous year to 50.36 % in the current year. The net profit ratio shows a decrease

of five –percent approximately. Another major determinant of a company’s progress and

profitability is through its return on the money put in for carrying out the activities of the

business. The year 2018 BOD seen an investment return ratio as nearly 9% and in the year 2019

this jumped to 14% approximately. It can be said that the company’s potentiality of receive

investments increased. There is also an increase in the EPS of the company. 0.44% of increase is

seen in the return on capital employed making the shareholders’ investment more worthy.

Income tax for the year 2018 was 15.02 B and year 2019 income tax was 11.01 B. it shows a

decline of 4.01 B.

Conclusion

On the basis of the studies it can be concluded that there is a significant impact that an

organization experiences in its profitability and tax payments in situation of mergers. The study

has selected two CPA firms one is BDO and the other is Moore Stevens. The later merged into

the former in the year 2019. For analysing the impact of merger on BDO the financial statements

of the company have been analysed in the studies for the years 2018 & 2019.

Recommendations

On the basis of the studies it can be recommended to the company that mergers are one of

the best ways through which it can experience good growth by combating all the challenges. To

have successful mergers certain points are suggested to the company firstly it should ensure

fairness to all the parties in the process the negotiation must be completely justifiable. It should

be noted that the selected must be reputed in the market as reputation of the company plays a

major role behind the successful and effective merger.

Refrences

Books and Journals

Argentesi, E., Buccirossi, P., Calvano, E., Duso, T., Marrazzo, A., & Nava, S. (2021). Merger

policy in digital markets: an ex post assessment. Journal of Competition Law &

Economics. 17(1). 95-140.

Brooks, C., Chen, Z., & Zeng, Y. (2018). Institutional cross-ownership and corporate strategy:

The case of mergers and acquisitions. Journal of Corporate Finance. 48. 187-216.

Brueller, N. N., Carmeli, A., & Markman, G. D. (2018). Linking merger and acquisition

strategies to postmerger integration: A configurational perspective of human resource

management. Journal of Management. 44(5). 1793-1818.

Christofi, M., Vrontis, D., Thrassou, A., & Shams, S. R. (2019). Triggering technological

innovation through cross-border mergers and acquisitions: A micro-foundational

perspective. Technological Forecasting and Social Change. 146. 148-166.

Singh, S., & Das, S. (2018). Impact of post-merger and acquisition activities on the financial

performance of banks: A study of Indian private sector and public sector banks. Revista

Espacios Magazine. 39(26). 25.

Welch, X., Pavićević, S., Keil, T., & Laamanen, T. (2020). The pre-deal phase of mergers and

acquisitions: A review and research agenda. Journal of Management. 46(6). 843-878.

1

Books and Journals

Argentesi, E., Buccirossi, P., Calvano, E., Duso, T., Marrazzo, A., & Nava, S. (2021). Merger

policy in digital markets: an ex post assessment. Journal of Competition Law &

Economics. 17(1). 95-140.

Brooks, C., Chen, Z., & Zeng, Y. (2018). Institutional cross-ownership and corporate strategy:

The case of mergers and acquisitions. Journal of Corporate Finance. 48. 187-216.

Brueller, N. N., Carmeli, A., & Markman, G. D. (2018). Linking merger and acquisition

strategies to postmerger integration: A configurational perspective of human resource

management. Journal of Management. 44(5). 1793-1818.

Christofi, M., Vrontis, D., Thrassou, A., & Shams, S. R. (2019). Triggering technological

innovation through cross-border mergers and acquisitions: A micro-foundational

perspective. Technological Forecasting and Social Change. 146. 148-166.

Singh, S., & Das, S. (2018). Impact of post-merger and acquisition activities on the financial

performance of banks: A study of Indian private sector and public sector banks. Revista

Espacios Magazine. 39(26). 25.

Welch, X., Pavićević, S., Keil, T., & Laamanen, T. (2020). The pre-deal phase of mergers and

acquisitions: A review and research agenda. Journal of Management. 46(6). 843-878.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.