Management Accounting Report: Merlin Financial Consultancy Analysis

VerifiedAdded on 2020/10/22

|21

|6143

|235

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring its various systems, reporting methods, and practical applications within the context of Merlin Financial Consultancy. It delves into cost accounting, including actual, normal, standard, job, process, batch, and contract costing. The report examines inventory management and price optimization techniques. Furthermore, it analyzes different management accounting reporting methods, such as budget reports, performance reports, accounts receivable aging reports, and cost managerial accounting reports. The report also evaluates the benefits of each system and their integration within an organization's processes. The report also analyses the planning tools used for budgetary control, and their advantages and disadvantages. The report highlights how organizations use management accounting to address financial challenges, using Merlin Financial Consultancy and Equilibrium Assets Management as comparison cases, and provides a conclusion and references.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1. Management accounting and its different types of system....................................................1

P2 Explain different method of management accounting reporting...........................................3

M1. Evaluation of benefits of various management accounting systems....................................4

D1 Management accounting system and management accounting reporting are integrated with

organisation process.....................................................................................................................5

TASK 2............................................................................................................................................5

P3 .Appropriate techniques of cost analysis to prepare an income statement.............................5

M2 Management accounting techniques and financial reporting documents.............................8

D2 Financial reports which applies to interpret many business activities .................................9

TASK 3............................................................................................................................................9

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control..........................................................................................................................................9

M3. Usage of different planning tools for preparing and forecasting budgets..........................11

P5 Organisations are adapting management accounting systems to respond to financial

problems.....................................................................................................................................12

TASK 4..........................................................................................................................................14

P5 Comparison Between Merlin Financial Consultant and Equilibrium Assets Management. 14

M4 Management accounting in response to financial problem can lead organisations to

sustainable success ....................................................................................................................15

D3 Various Planning tool to resolve financial problems...........................................................15

CONCLUSION..............................................................................................................................15

REFRENCES.................................................................................................................................16

INTRODUCTION...........................................................................................................................1

P1. Management accounting and its different types of system....................................................1

P2 Explain different method of management accounting reporting...........................................3

M1. Evaluation of benefits of various management accounting systems....................................4

D1 Management accounting system and management accounting reporting are integrated with

organisation process.....................................................................................................................5

TASK 2............................................................................................................................................5

P3 .Appropriate techniques of cost analysis to prepare an income statement.............................5

M2 Management accounting techniques and financial reporting documents.............................8

D2 Financial reports which applies to interpret many business activities .................................9

TASK 3............................................................................................................................................9

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control..........................................................................................................................................9

M3. Usage of different planning tools for preparing and forecasting budgets..........................11

P5 Organisations are adapting management accounting systems to respond to financial

problems.....................................................................................................................................12

TASK 4..........................................................................................................................................14

P5 Comparison Between Merlin Financial Consultant and Equilibrium Assets Management. 14

M4 Management accounting in response to financial problem can lead organisations to

sustainable success ....................................................................................................................15

D3 Various Planning tool to resolve financial problems...........................................................15

CONCLUSION..............................................................................................................................15

REFRENCES.................................................................................................................................16

INTRODUCTION

Management accounting consists of two words “management” and “accounting”. It is the

study of managerial concepts (Bruynseels and Cardinaels, 2013). This is a kind of system which

is helpful providing monitory and non monitory informations to the companies to make future

decisions and policies for future. Generally these reports are prepared for the internal purpose

and for internal decision-making. Management accounting consists many reports which are

required by management for many purpose to the companies. There is no specific time period to

prepare management accounting reports, these can be prepare according to the organisation need.

To understand the concept and practice of management accounting Merlin Financial Consultancy

company is selected. It was founded in 1988. This company deals in various financial products

and services like fixed deposits, mortgage loan, financial advices etc.

In the project report detailed information about the management accounting, its types,

benefits are described. In addition this report highlight on various planning tools of budgetary

control and their advantage, disadvantage, different costing techniques. It describes the way in

which organisations manage with financial problems with the use of management accounting

techniques to achieve objectives and goals.

LO1

P1. Management accounting and its different types of system.

Accounting is a process of recording financial transactions in a systematic manner which

is helpful for the organisations (Chandar, Collier and Miranti, 2012). This is a systematic process

of recording, analysing and presenting statements of finance. Basically the main objective of

accounting is to provide data for preparation of various financial statements. This is done in a

particular time period which is known by accounting period. Accounting is of many types.

Management accounting is a part of accounting which is described below

Management accounting- Management accounting is a kind of system which is related to

providing important financial and financial information to the management for making future

policies and plans. This accounting system is useful for internal purpose and to make internal

decisions for the organisation. It is not done in a particular accounting period, it is done when it

is needed by the organisation. This accounting system is not compulsory for the companies, it is

1

Management accounting consists of two words “management” and “accounting”. It is the

study of managerial concepts (Bruynseels and Cardinaels, 2013). This is a kind of system which

is helpful providing monitory and non monitory informations to the companies to make future

decisions and policies for future. Generally these reports are prepared for the internal purpose

and for internal decision-making. Management accounting consists many reports which are

required by management for many purpose to the companies. There is no specific time period to

prepare management accounting reports, these can be prepare according to the organisation need.

To understand the concept and practice of management accounting Merlin Financial Consultancy

company is selected. It was founded in 1988. This company deals in various financial products

and services like fixed deposits, mortgage loan, financial advices etc.

In the project report detailed information about the management accounting, its types,

benefits are described. In addition this report highlight on various planning tools of budgetary

control and their advantage, disadvantage, different costing techniques. It describes the way in

which organisations manage with financial problems with the use of management accounting

techniques to achieve objectives and goals.

LO1

P1. Management accounting and its different types of system.

Accounting is a process of recording financial transactions in a systematic manner which

is helpful for the organisations (Chandar, Collier and Miranti, 2012). This is a systematic process

of recording, analysing and presenting statements of finance. Basically the main objective of

accounting is to provide data for preparation of various financial statements. This is done in a

particular time period which is known by accounting period. Accounting is of many types.

Management accounting is a part of accounting which is described below

Management accounting- Management accounting is a kind of system which is related to

providing important financial and financial information to the management for making future

policies and plans. This accounting system is useful for internal purpose and to make internal

decisions for the organisation. It is not done in a particular accounting period, it is done when it

is needed by the organisation. This accounting system is not compulsory for the companies, it is

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

depend on the companies whether they want to do or not. So management accounting system has

its own importance in internal management of organisation.

2

its own importance in internal management of organisation.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

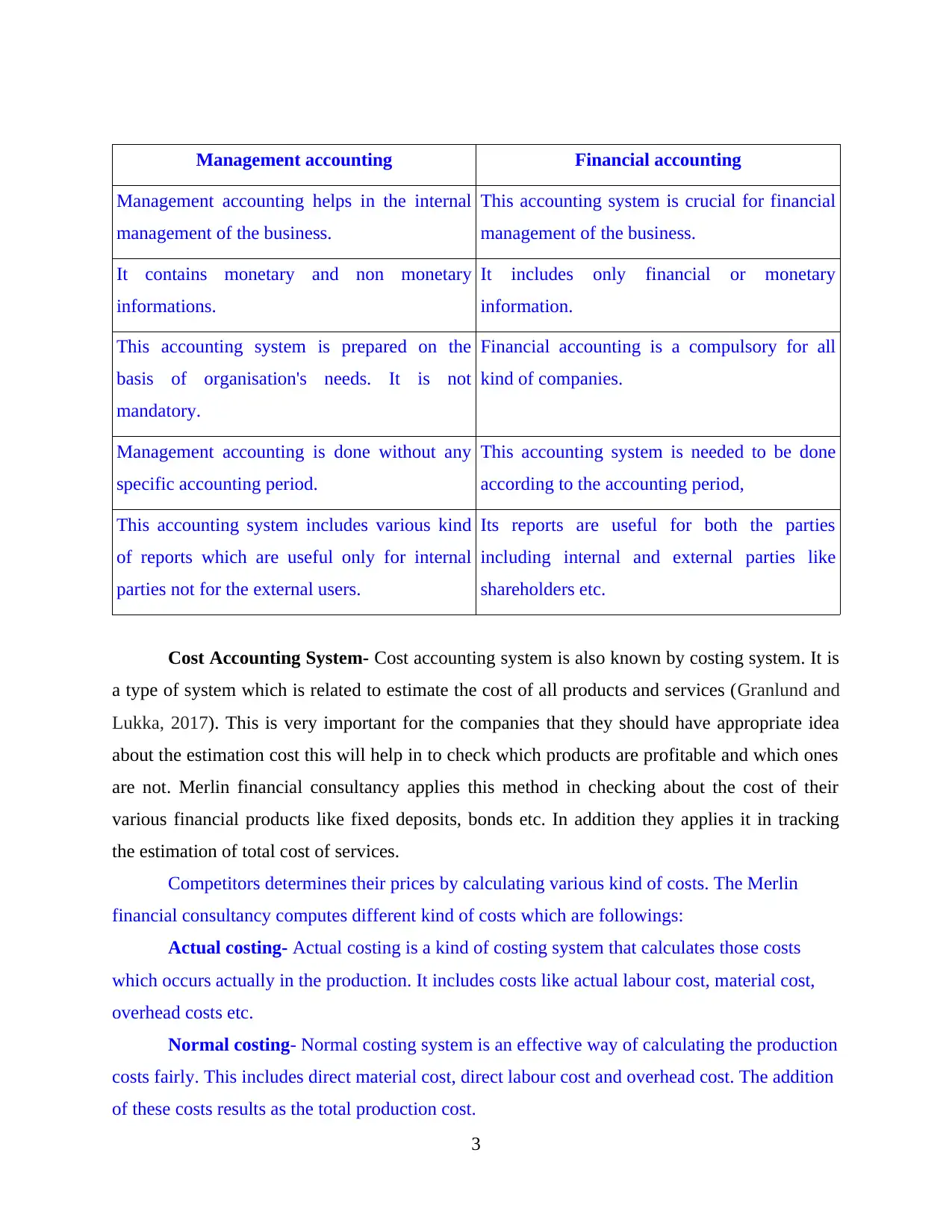

Management accounting Financial accounting

Management accounting helps in the internal

management of the business.

This accounting system is crucial for financial

management of the business.

It contains monetary and non monetary

informations.

It includes only financial or monetary

information.

This accounting system is prepared on the

basis of organisation's needs. It is not

mandatory.

Financial accounting is a compulsory for all

kind of companies.

Management accounting is done without any

specific accounting period.

This accounting system is needed to be done

according to the accounting period,

This accounting system includes various kind

of reports which are useful only for internal

parties not for the external users.

Its reports are useful for both the parties

including internal and external parties like

shareholders etc.

Cost Accounting System- Cost accounting system is also known by costing system. It is

a type of system which is related to estimate the cost of all products and services (Granlund and

Lukka, 2017). This is very important for the companies that they should have appropriate idea

about the estimation cost this will help in to check which products are profitable and which ones

are not. Merlin financial consultancy applies this method in checking about the cost of their

various financial products like fixed deposits, bonds etc. In addition they applies it in tracking

the estimation of total cost of services.

Competitors determines their prices by calculating various kind of costs. The Merlin

financial consultancy computes different kind of costs which are followings:

Actual costing- Actual costing is a kind of costing system that calculates those costs

which occurs actually in the production. It includes costs like actual labour cost, material cost,

overhead costs etc.

Normal costing- Normal costing system is an effective way of calculating the production

costs fairly. This includes direct material cost, direct labour cost and overhead cost. The addition

of these costs results as the total production cost.

3

Management accounting helps in the internal

management of the business.

This accounting system is crucial for financial

management of the business.

It contains monetary and non monetary

informations.

It includes only financial or monetary

information.

This accounting system is prepared on the

basis of organisation's needs. It is not

mandatory.

Financial accounting is a compulsory for all

kind of companies.

Management accounting is done without any

specific accounting period.

This accounting system is needed to be done

according to the accounting period,

This accounting system includes various kind

of reports which are useful only for internal

parties not for the external users.

Its reports are useful for both the parties

including internal and external parties like

shareholders etc.

Cost Accounting System- Cost accounting system is also known by costing system. It is

a type of system which is related to estimate the cost of all products and services (Granlund and

Lukka, 2017). This is very important for the companies that they should have appropriate idea

about the estimation cost this will help in to check which products are profitable and which ones

are not. Merlin financial consultancy applies this method in checking about the cost of their

various financial products like fixed deposits, bonds etc. In addition they applies it in tracking

the estimation of total cost of services.

Competitors determines their prices by calculating various kind of costs. The Merlin

financial consultancy computes different kind of costs which are followings:

Actual costing- Actual costing is a kind of costing system that calculates those costs

which occurs actually in the production. It includes costs like actual labour cost, material cost,

overhead costs etc.

Normal costing- Normal costing system is an effective way of calculating the production

costs fairly. This includes direct material cost, direct labour cost and overhead cost. The addition

of these costs results as the total production cost.

3

Standard costing- This costing system is also known by the target costing. It estimates

the future costs that can be occur in the production. The main aim of this costing system is to

keep control the cost of production.

Job costing- Job costing system is a method of calculating the each units cost. This

method computes the cost by calculating the each job's cost that assigned in the job. It helps in

analysing the each units cost individually.

Process costing- Process costing system is useful in calculating the cost of different

process of production. This costing system is suitable for those organisations which produce

products into different processes. Merlin financial limited use this tool for calculating the cost of

different financial products and services.3

Batch costing- Batch costing system works as the same framework of job costing

system. This costing system divides the products into different batches that helps in calculating

each units cost.

Contract costing- Contract costing system is applied in the large projects and contracts.

This is beneficial for controlling the different cost of projects. Basically it is used by the

companies when they deal a contract or project.

Inventory Management System- Inventory management system is a kind of system

which is related to tracks the movements of services and goods (Ismail and King, 2014). This is

very important tool of management accounting system. It is helpful for the Merlin financial

consultancy in managing their financial products and services. This helps them in tracking the

movement of financial services. Like if company wants to check about the process of a fixed

deposit service then they may apply to this system in checking the documentation, clarification

etc.

Price Optimisation- Price optimisation is method of analysing that how customers will

react on different pricing of products and services. It provides a framework to set the level of

price at which organisation may achieve their goals and objectives. In addition it sets the level of

price which is also suitable for customers. Merlin financial consultancy uses this method of

pricing. Under this method they determine the pricing level of their financial products and

services at which they can gain maximum profit. This pricing method increase the satisfaction

level of their customers.

4

the future costs that can be occur in the production. The main aim of this costing system is to

keep control the cost of production.

Job costing- Job costing system is a method of calculating the each units cost. This

method computes the cost by calculating the each job's cost that assigned in the job. It helps in

analysing the each units cost individually.

Process costing- Process costing system is useful in calculating the cost of different

process of production. This costing system is suitable for those organisations which produce

products into different processes. Merlin financial limited use this tool for calculating the cost of

different financial products and services.3

Batch costing- Batch costing system works as the same framework of job costing

system. This costing system divides the products into different batches that helps in calculating

each units cost.

Contract costing- Contract costing system is applied in the large projects and contracts.

This is beneficial for controlling the different cost of projects. Basically it is used by the

companies when they deal a contract or project.

Inventory Management System- Inventory management system is a kind of system

which is related to tracks the movements of services and goods (Ismail and King, 2014). This is

very important tool of management accounting system. It is helpful for the Merlin financial

consultancy in managing their financial products and services. This helps them in tracking the

movement of financial services. Like if company wants to check about the process of a fixed

deposit service then they may apply to this system in checking the documentation, clarification

etc.

Price Optimisation- Price optimisation is method of analysing that how customers will

react on different pricing of products and services. It provides a framework to set the level of

price at which organisation may achieve their goals and objectives. In addition it sets the level of

price which is also suitable for customers. Merlin financial consultancy uses this method of

pricing. Under this method they determine the pricing level of their financial products and

services at which they can gain maximum profit. This pricing method increase the satisfaction

level of their customers.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job Costing System- Job costing is a kind of system which calculate the total cost of

products or service then assign cost to the each unit of product. It is very helpful for the

organisations in analysing total cost and expenses and as well as assigning the cost individually.

Merlin financial consultancy uses this system in calculating the cost of their financial products

and services like cost of documentation in financial services, agent charges and many more. It

helps them in analysing the total cost.

P2 Explain different method of management accounting reporting.

Management accounting reports are those reports which are helpful in

measurement of performance. On the basis of these reports management plans their future

activities and strategies. So it is very necessary that these reports should be prepared without any

mistakes. Merlin financial consultancy makes various financial reports for their performance

analysis and to make effective strategies. They prepares following reports:.

Budget report- Budgets reports contains the estimation of income and expenses for a

particular time period. On the basis of these reports an organisation compares their actual

performance with budgeted targets. This helps companies in making future plans and policies.

These reports consists only financial data (Kastberg, and Siverbo, 2013). The basis of these

reports is the previous year's data. Merlin financial consultancy makes these reports in making

comparison between the actual income and budgeted income. This helps them in making

effective planning if their revenue is low. In addition, it is also important for them in analysing

financial position.

Performance report- Performance reports are helpful in analyse the performance of

organisation and as well as of employees. It review the performance. This is also important in

selecting the employees who are eligible for rewards. Merlin financial consultancy uses this

report in analysing the performance of the employees and organisations. This helps company in

improving the quality of service providing to the customers.

Account receivable ageing report- This type of report is helpful for those companies

which makes their transactions on credit. It consists many information within it like amount

which is due by customer, date on which transaction took place etc. This removes the headache

of financial manger to keep remember about the credit transaction. They can use this report in

checking about total debt collection from customers. Merlin financial consultancy uses this

report in checking that how much amount they needed to recover from customer. In addition it

5

products or service then assign cost to the each unit of product. It is very helpful for the

organisations in analysing total cost and expenses and as well as assigning the cost individually.

Merlin financial consultancy uses this system in calculating the cost of their financial products

and services like cost of documentation in financial services, agent charges and many more. It

helps them in analysing the total cost.

P2 Explain different method of management accounting reporting.

Management accounting reports are those reports which are helpful in

measurement of performance. On the basis of these reports management plans their future

activities and strategies. So it is very necessary that these reports should be prepared without any

mistakes. Merlin financial consultancy makes various financial reports for their performance

analysis and to make effective strategies. They prepares following reports:.

Budget report- Budgets reports contains the estimation of income and expenses for a

particular time period. On the basis of these reports an organisation compares their actual

performance with budgeted targets. This helps companies in making future plans and policies.

These reports consists only financial data (Kastberg, and Siverbo, 2013). The basis of these

reports is the previous year's data. Merlin financial consultancy makes these reports in making

comparison between the actual income and budgeted income. This helps them in making

effective planning if their revenue is low. In addition, it is also important for them in analysing

financial position.

Performance report- Performance reports are helpful in analyse the performance of

organisation and as well as of employees. It review the performance. This is also important in

selecting the employees who are eligible for rewards. Merlin financial consultancy uses this

report in analysing the performance of the employees and organisations. This helps company in

improving the quality of service providing to the customers.

Account receivable ageing report- This type of report is helpful for those companies

which makes their transactions on credit. It consists many information within it like amount

which is due by customer, date on which transaction took place etc. This removes the headache

of financial manger to keep remember about the credit transaction. They can use this report in

checking about total debt collection from customers. Merlin financial consultancy uses this

report in checking that how much amount they needed to recover from customer. In addition it

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

also help finance department to focus more on important activities because it makes the work

easy of financial manager.

Cost Managerial Accounting Report- Cost managerial accounting report is helpful in

making comparison between selling amount and expenses done by the company. It provides a

basis for analyse the profit and loss of the company. This report calculates the total expenses

which become a basis for comparison. Merlin financial consultant make this report to analyse

that how much profit or loss they are getting from their different financial products and services.

It also helps in making strong strategies for those services and products which are not beneficial.

M1. Evaluation of benefits of various management accounting systems.

Management accounting system Advantage

Cost accounting system Helps in measurement and

improvement of efficiency of services

and products or company.

Beneficial in recording of total cost of

various financial services.

Inventory management system Inventory management system is

helpful in saving time and money of the

company because it brings efficiency in

services

This system is helpful in tracking the

position of various financial services

Price optimisation system It is advantageous for company in

analysing the customers reaction on the

different pricing. It provides a

framework.

This system is easy to use for the

company. It consumes less time and

cost of the company.

Job costing system It helps in checking the profit earned

through an individual activity as well as

6

easy of financial manager.

Cost Managerial Accounting Report- Cost managerial accounting report is helpful in

making comparison between selling amount and expenses done by the company. It provides a

basis for analyse the profit and loss of the company. This report calculates the total expenses

which become a basis for comparison. Merlin financial consultant make this report to analyse

that how much profit or loss they are getting from their different financial products and services.

It also helps in making strong strategies for those services and products which are not beneficial.

M1. Evaluation of benefits of various management accounting systems.

Management accounting system Advantage

Cost accounting system Helps in measurement and

improvement of efficiency of services

and products or company.

Beneficial in recording of total cost of

various financial services.

Inventory management system Inventory management system is

helpful in saving time and money of the

company because it brings efficiency in

services

This system is helpful in tracking the

position of various financial services

Price optimisation system It is advantageous for company in

analysing the customers reaction on the

different pricing. It provides a

framework.

This system is easy to use for the

company. It consumes less time and

cost of the company.

Job costing system It helps in checking the profit earned

through an individual activity as well as

6

it also defines the cost of each

individual activity.

This is important in minimisation of

cost of different products and services.

D1 Management accounting system and management accounting reporting are integrated with

organisation process.

Management accounting system and management accounting reporting both have link

with each other (Kolk and Perego, 2015). The reason behind this link is that if a company wants

to make an accounting report then that company needed many kind of data from the management

accounting systems. Like while making cost managerial accounting report, company needs,

many information and data from the cost accounting system. Management of Merlin financial

consultant makes many kind of reports with the help of link between accounting reports and

accounting system. So this link is very important for companies in making reports and tools of

accounting.

TASK 2

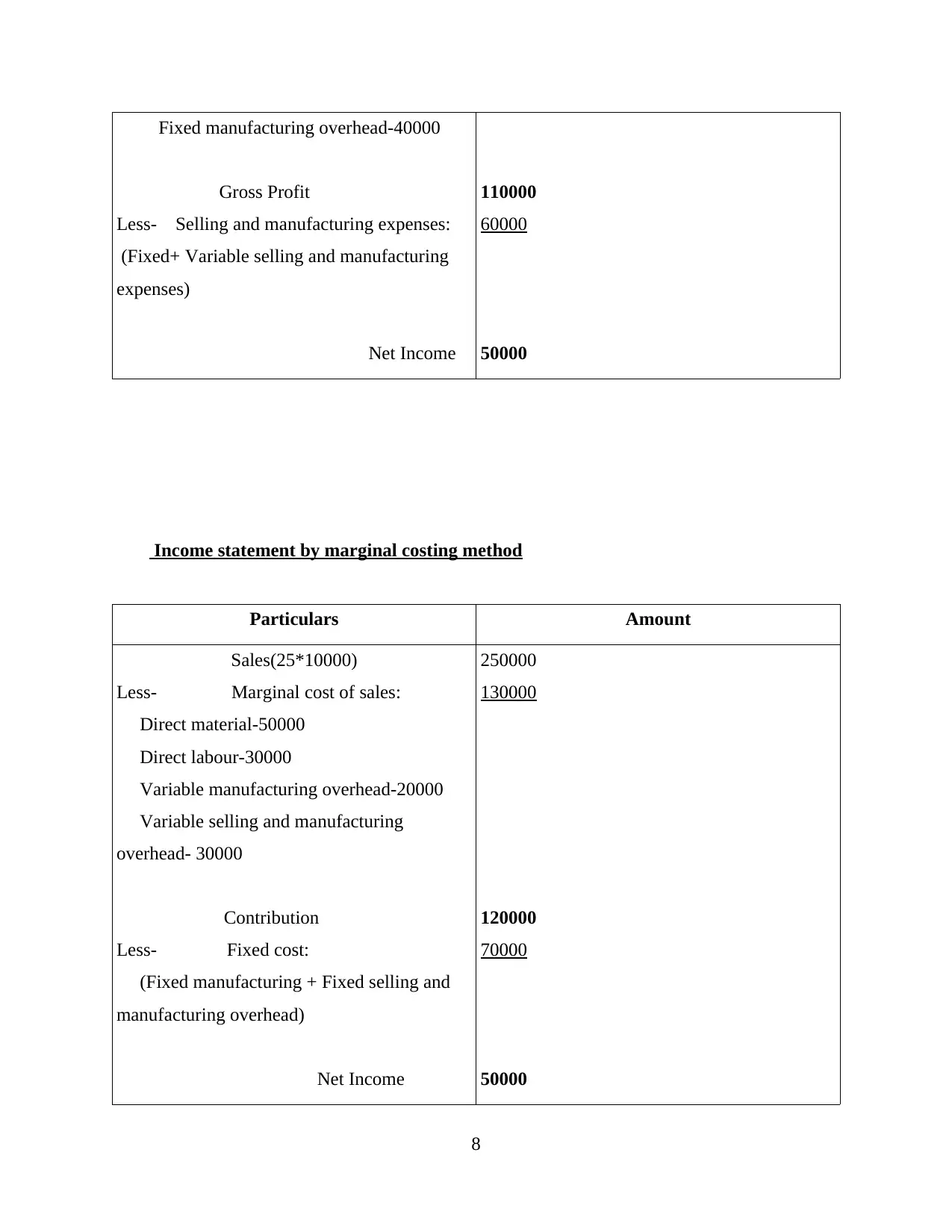

P3 .Appropriate techniques of cost analysis to prepare an income statement

Absorption costing- Absorption costing is also known by full costing method. This

method helps in calculating total cost of production and after that assign the cost in each

product's unit (Li, 2013).

Marginal costing- Marginal costing method is a kind of costing system which considers

the variable cost as the unit cost and fixed cost as the period cost.

Income statement by absorption costing method

Particulars Amount

Sales (25*10000)

Less- Cost of goods sold:

Direct labour-30000

Direct labour-50000

Variable manufacturing overhead-20000

250000

140000

7

individual activity.

This is important in minimisation of

cost of different products and services.

D1 Management accounting system and management accounting reporting are integrated with

organisation process.

Management accounting system and management accounting reporting both have link

with each other (Kolk and Perego, 2015). The reason behind this link is that if a company wants

to make an accounting report then that company needed many kind of data from the management

accounting systems. Like while making cost managerial accounting report, company needs,

many information and data from the cost accounting system. Management of Merlin financial

consultant makes many kind of reports with the help of link between accounting reports and

accounting system. So this link is very important for companies in making reports and tools of

accounting.

TASK 2

P3 .Appropriate techniques of cost analysis to prepare an income statement

Absorption costing- Absorption costing is also known by full costing method. This

method helps in calculating total cost of production and after that assign the cost in each

product's unit (Li, 2013).

Marginal costing- Marginal costing method is a kind of costing system which considers

the variable cost as the unit cost and fixed cost as the period cost.

Income statement by absorption costing method

Particulars Amount

Sales (25*10000)

Less- Cost of goods sold:

Direct labour-30000

Direct labour-50000

Variable manufacturing overhead-20000

250000

140000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed manufacturing overhead-40000

Gross Profit

Less- Selling and manufacturing expenses:

(Fixed+ Variable selling and manufacturing

expenses)

Net Income

110000

60000

50000

Income statement by marginal costing method

Particulars Amount

Sales(25*10000)

Less- Marginal cost of sales:

Direct material-50000

Direct labour-30000

Variable manufacturing overhead-20000

Variable selling and manufacturing

overhead- 30000

Contribution

Less- Fixed cost:

(Fixed manufacturing + Fixed selling and

manufacturing overhead)

Net Income

250000

130000

120000

70000

50000

8

Gross Profit

Less- Selling and manufacturing expenses:

(Fixed+ Variable selling and manufacturing

expenses)

Net Income

110000

60000

50000

Income statement by marginal costing method

Particulars Amount

Sales(25*10000)

Less- Marginal cost of sales:

Direct material-50000

Direct labour-30000

Variable manufacturing overhead-20000

Variable selling and manufacturing

overhead- 30000

Contribution

Less- Fixed cost:

(Fixed manufacturing + Fixed selling and

manufacturing overhead)

Net Income

250000

130000

120000

70000

50000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation- From above solved numerical, it has been recommend that in both

methods, net income is same. In absorption method net income is of 50000 and in marginal

method net income is of 50000.

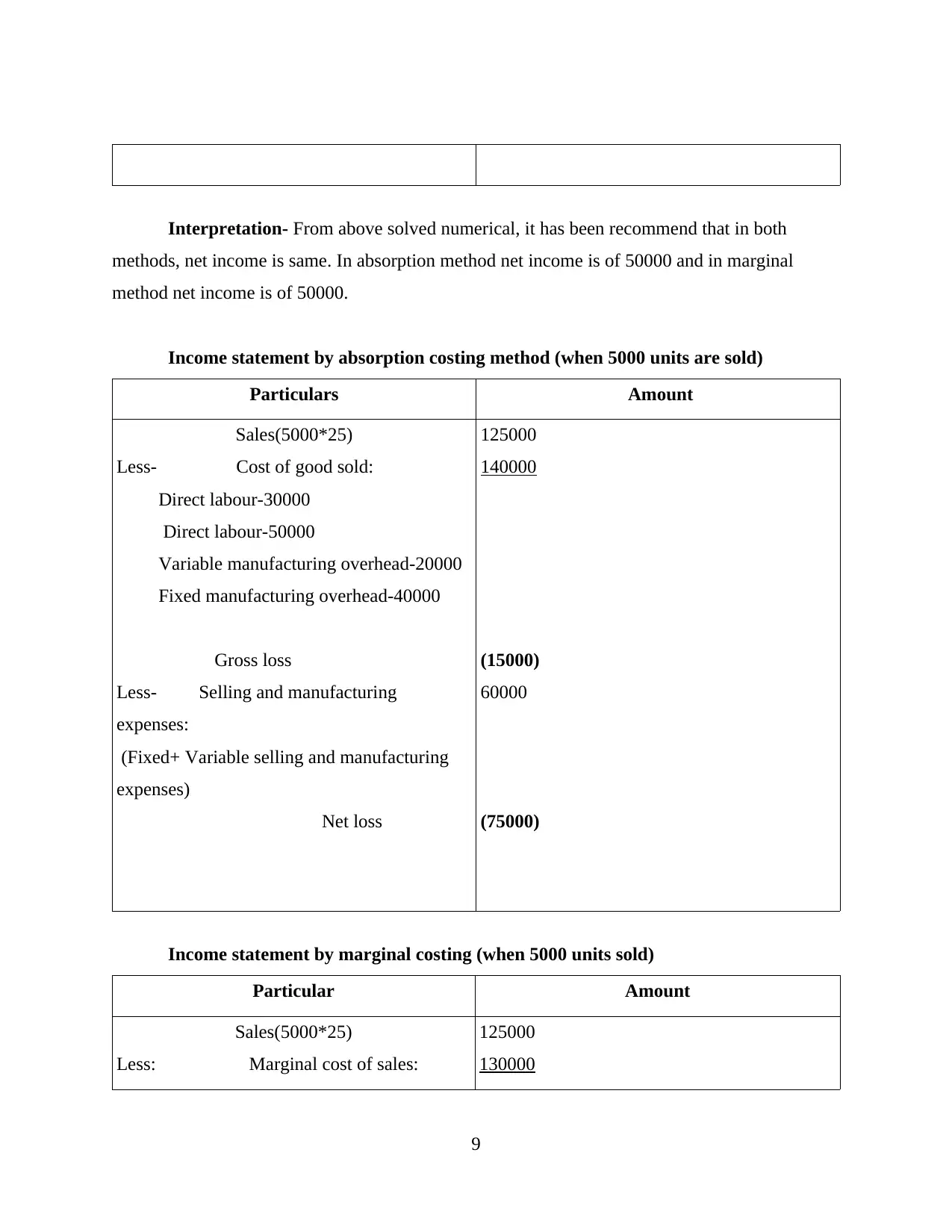

Income statement by absorption costing method (when 5000 units are sold)

Particulars Amount

Sales(5000*25)

Less- Cost of good sold:

Direct labour-30000

Direct labour-50000

Variable manufacturing overhead-20000

Fixed manufacturing overhead-40000

Gross loss

Less- Selling and manufacturing

expenses:

(Fixed+ Variable selling and manufacturing

expenses)

Net loss

125000

140000

(15000)

60000

(75000)

Income statement by marginal costing (when 5000 units sold)

Particular Amount

Sales(5000*25)

Less: Marginal cost of sales:

125000

130000

9

methods, net income is same. In absorption method net income is of 50000 and in marginal

method net income is of 50000.

Income statement by absorption costing method (when 5000 units are sold)

Particulars Amount

Sales(5000*25)

Less- Cost of good sold:

Direct labour-30000

Direct labour-50000

Variable manufacturing overhead-20000

Fixed manufacturing overhead-40000

Gross loss

Less- Selling and manufacturing

expenses:

(Fixed+ Variable selling and manufacturing

expenses)

Net loss

125000

140000

(15000)

60000

(75000)

Income statement by marginal costing (when 5000 units sold)

Particular Amount

Sales(5000*25)

Less: Marginal cost of sales:

125000

130000

9

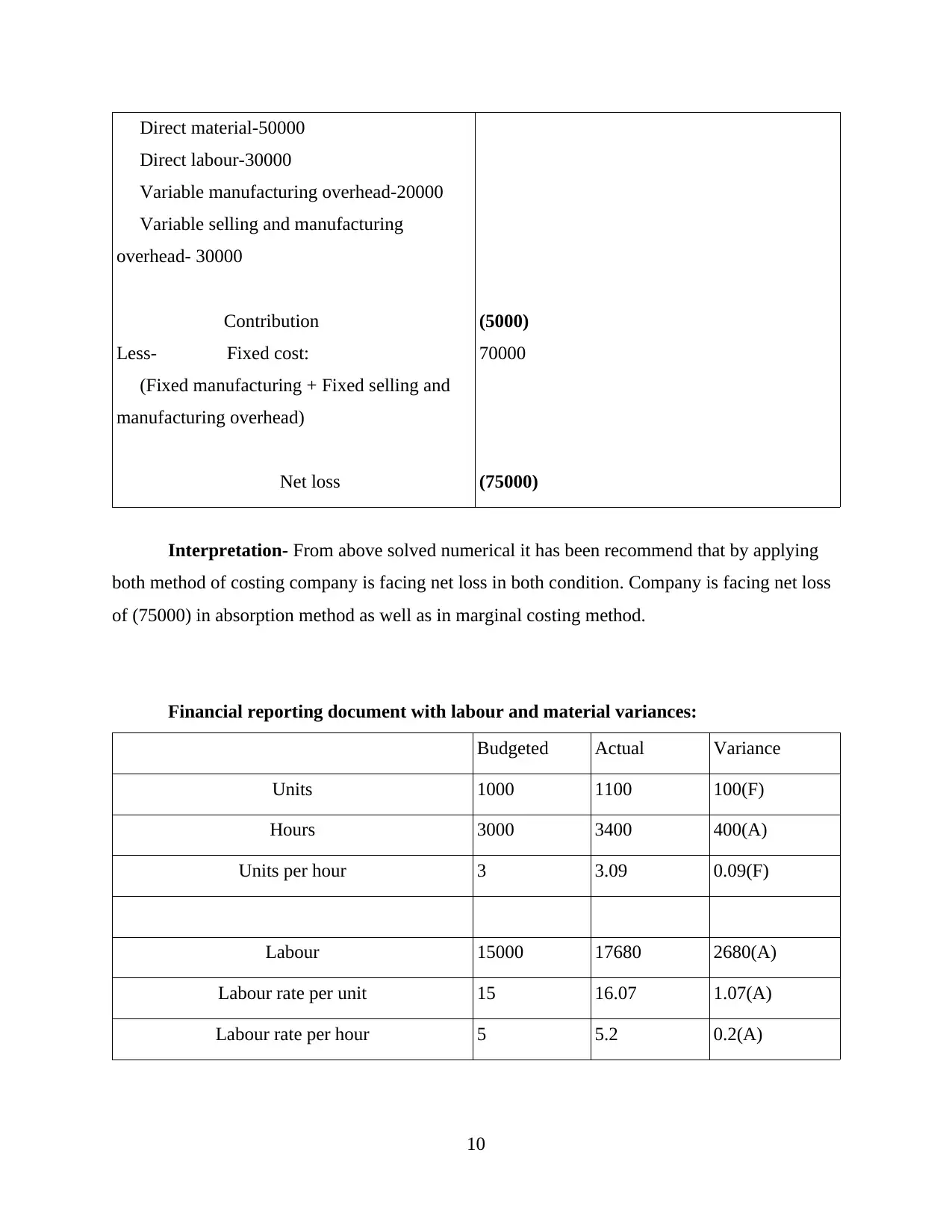

Direct material-50000

Direct labour-30000

Variable manufacturing overhead-20000

Variable selling and manufacturing

overhead- 30000

Contribution

Less- Fixed cost:

(Fixed manufacturing + Fixed selling and

manufacturing overhead)

Net loss

(5000)

70000

(75000)

Interpretation- From above solved numerical it has been recommend that by applying

both method of costing company is facing net loss in both condition. Company is facing net loss

of (75000) in absorption method as well as in marginal costing method.

Financial reporting document with labour and material variances:

Budgeted Actual Variance

Units 1000 1100 100(F)

Hours 3000 3400 400(A)

Units per hour 3 3.09 0.09(F)

Labour 15000 17680 2680(A)

Labour rate per unit 15 16.07 1.07(A)

Labour rate per hour 5 5.2 0.2(A)

10

Direct labour-30000

Variable manufacturing overhead-20000

Variable selling and manufacturing

overhead- 30000

Contribution

Less- Fixed cost:

(Fixed manufacturing + Fixed selling and

manufacturing overhead)

Net loss

(5000)

70000

(75000)

Interpretation- From above solved numerical it has been recommend that by applying

both method of costing company is facing net loss in both condition. Company is facing net loss

of (75000) in absorption method as well as in marginal costing method.

Financial reporting document with labour and material variances:

Budgeted Actual Variance

Units 1000 1100 100(F)

Hours 3000 3400 400(A)

Units per hour 3 3.09 0.09(F)

Labour 15000 17680 2680(A)

Labour rate per unit 15 16.07 1.07(A)

Labour rate per hour 5 5.2 0.2(A)

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.