Derivatives and Fixed Income Securities: MG Case Study Analysis

VerifiedAdded on 2023/06/08

|9

|1776

|304

Report

AI Summary

This report analyzes the Metallgesellschaft (MG) case study, focusing on the use of futures and derivatives in hedging strategies. It examines whether MG was hedging or speculating, providing justification for the assessment. The report delves into the impact of underlying asset mismatch and maturity mismatch on hedge results, highlighting how these factors contributed to MG's financial difficulties. Specifically, the analysis discusses the critical role of maturity mismatch in the MG case, emphasizing the consequences of using short-term hedging instruments for long-term delivery obligations. The report references key figures illustrating cash flow structures and present value relationships, and it also includes an analysis of academic research and literature on the topic. The report concludes by underscoring the importance of aligning hedging strategies with the underlying assets and maturity dates to mitigate financial risks.

Running head: ACCOUNTING AND FINANCIAL REPORTING

Derivatives and Fixed Income Securities

Name of the Student:

Name of the University:

Authors Note:

Derivatives and Fixed Income Securities

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCIAL REPORTING

Table of Contents

Part B: Hedge use Futures and Derivatives Disaster.................................................................2

Question B2.1: Providing justification whether MG was hedging or speculating.....................2

Question B2.2: Indicating how underlining assets mismatch and maturity mismatch impact

hedge results...............................................................................................................................3

Question B2.3: Discussing how maturity mismatch is critical in the case of

Metallgescellschaft AG..............................................................................................................5

Reference:..................................................................................................................................8

1 | P a g e

Table of Contents

Part B: Hedge use Futures and Derivatives Disaster.................................................................2

Question B2.1: Providing justification whether MG was hedging or speculating.....................2

Question B2.2: Indicating how underlining assets mismatch and maturity mismatch impact

hedge results...............................................................................................................................3

Question B2.3: Discussing how maturity mismatch is critical in the case of

Metallgescellschaft AG..............................................................................................................5

Reference:..................................................................................................................................8

1 | P a g e

ACCOUNTING AND FINANCIAL REPORTING

Part B: Hedge use Futures and Derivatives Disaster

Question B2.1: Providing justification whether MG was hedging or speculating

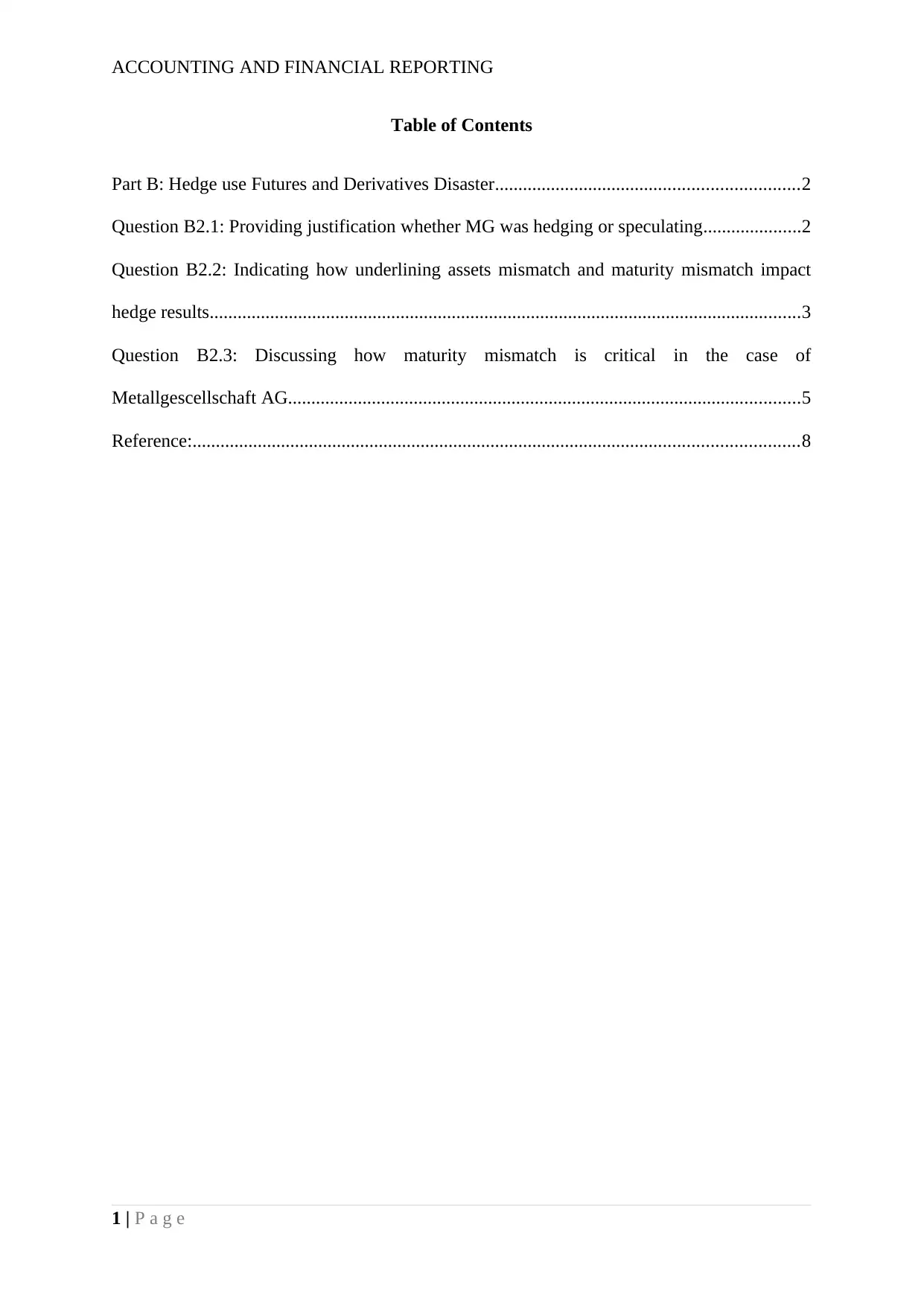

Figure 1: Indicating the cash flow structure of hedges for MGRM

(Source: Mello and Parsons 1995)

Journal of Applied Corporate finance highlights significant information regarding the

speculative measures, which was taken into consideration by the management of MG

Refining and Marketing (MGRM). The measure taken by the management of MGRM was

not accurate, as they were not hedging for the underlying assets that were being committed by

every month. Moreover, the company mainly focused on short term valuation of the oil prices

and opted to buy contract with short term duration, while the actual sales were conducted for

long term. This mainly increased the mismatch of maturity structure of the company, as

derivatives used for hedging purpuras did not match the delivery of the contracts. This

increased overall variance of the organisation, while dealing with the hedging instruments

and exposed the organisation to the excessive amount of basic risk. The accumulated risk

2 | P a g e

Part B: Hedge use Futures and Derivatives Disaster

Question B2.1: Providing justification whether MG was hedging or speculating

Figure 1: Indicating the cash flow structure of hedges for MGRM

(Source: Mello and Parsons 1995)

Journal of Applied Corporate finance highlights significant information regarding the

speculative measures, which was taken into consideration by the management of MG

Refining and Marketing (MGRM). The measure taken by the management of MGRM was

not accurate, as they were not hedging for the underlying assets that were being committed by

every month. Moreover, the company mainly focused on short term valuation of the oil prices

and opted to buy contract with short term duration, while the actual sales were conducted for

long term. This mainly increased the mismatch of maturity structure of the company, as

derivatives used for hedging purpuras did not match the delivery of the contracts. This

increased overall variance of the organisation, while dealing with the hedging instruments

and exposed the organisation to the excessive amount of basic risk. The accumulated risk

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCIAL REPORTING

structure of the organisation was shared when the prices were going down and increased the

cash flow deficit from the mismatched hedges (Neuberger 2015).

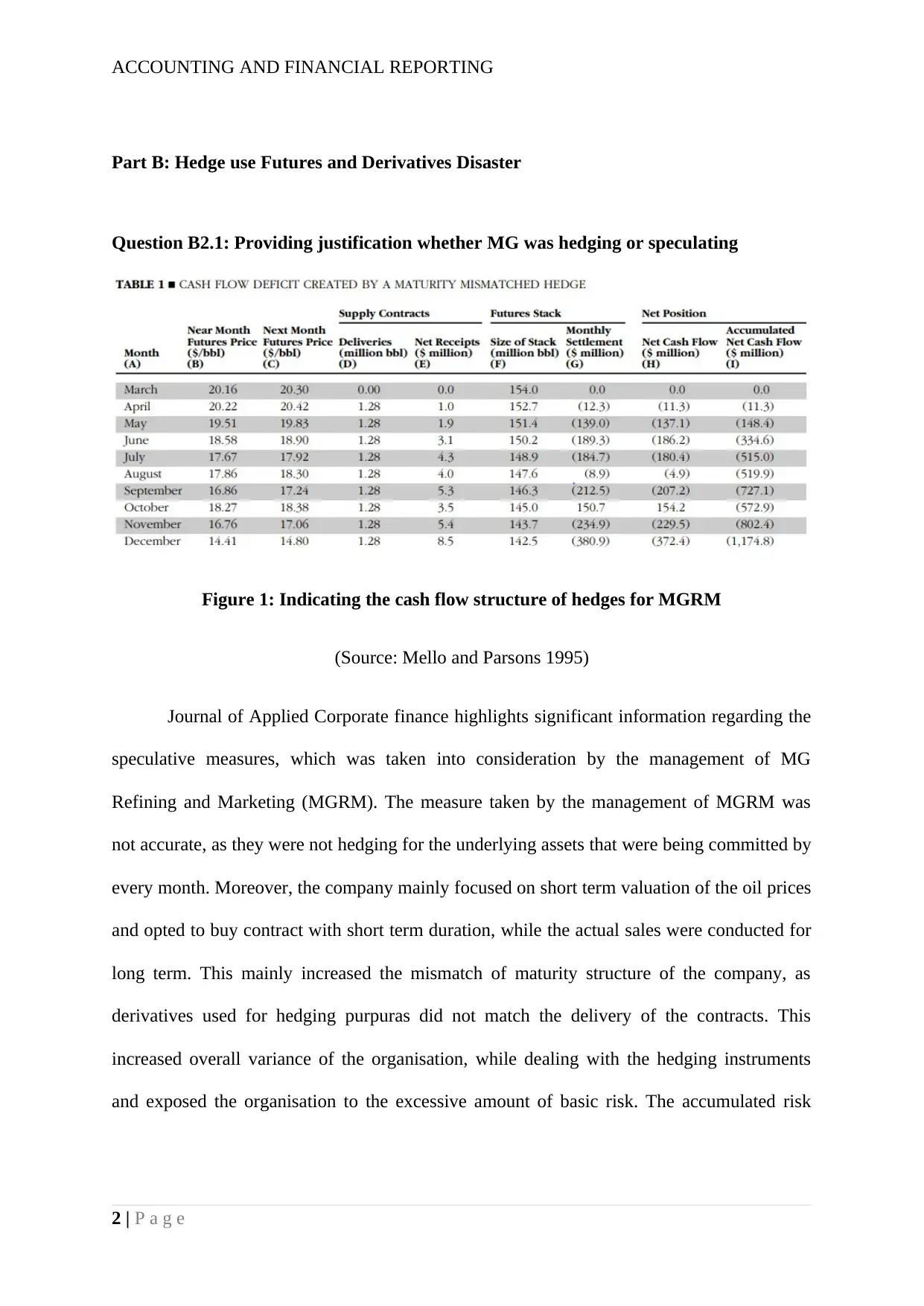

Figure 2: Present Value relationship

(Source: Mello and Parsons 1995)

The second major loophole in the decision of MGRM was the hedging measures used

for long term contracts. The organisation did not account on the present value of derivatives,

which was negatively affecting their hedge position. This can be considered that biggest

mistake, as the hedging period and delivery period of the context did not match and exposed

the organisation to high volatility. The organisation also used one to one hedge ratio, which is

not advisable for shorty term contract, which was being used by MGRM. This mainly

increased the negative hedge value for the rolling contracts of MGRM and exposed the

organisation to exponential losses (Abdel-Khalik 2014).

Question B2.2: Indicating how underlining assets mismatch and maturity mismatch

impact hedge results

The claims regarding the purpose of hedging futures are correct, as the organisation

needs to comply with the choice of asset underling the future contract and the delivery month.

The underlying asset mismatch directly affects the level of pricing, which can be conducted

3 | P a g e

structure of the organisation was shared when the prices were going down and increased the

cash flow deficit from the mismatched hedges (Neuberger 2015).

Figure 2: Present Value relationship

(Source: Mello and Parsons 1995)

The second major loophole in the decision of MGRM was the hedging measures used

for long term contracts. The organisation did not account on the present value of derivatives,

which was negatively affecting their hedge position. This can be considered that biggest

mistake, as the hedging period and delivery period of the context did not match and exposed

the organisation to high volatility. The organisation also used one to one hedge ratio, which is

not advisable for shorty term contract, which was being used by MGRM. This mainly

increased the negative hedge value for the rolling contracts of MGRM and exposed the

organisation to exponential losses (Abdel-Khalik 2014).

Question B2.2: Indicating how underlining assets mismatch and maturity mismatch

impact hedge results

The claims regarding the purpose of hedging futures are correct, as the organisation

needs to comply with the choice of asset underling the future contract and the delivery month.

The underlying asset mismatch directly affects the level of pricing, which can be conducted

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCIAL REPORTING

for the particular asset. Therefore, in context of hedging it can be detected that underlying

asset mismatch arises only when the underlying asset does match the hedging instrument.

This mainly creates an imperfect hedge, which increases the level of risk attributes for the

organisation conducting the hedge. Dickinson et al. (2017) indicates that investors and

organisation mainly use hedging process for reducing the risk attributes of their portfolio

exposure. On the other hand, Corbett and Smodis (2018) criticises that without adequate

research the hedging measure mainly increases the risk level and raises the chances of loss

from fluctuating prices.

Therefore, organisations dealing with jet oil cannot hedge their exposure in the

commodity by hedging an underlying asset of heating oil futures, as the price valuation and

output of the commodities are different. This measure will not allow the organisation to

adequately hedge their products and reduce the actual exposure. As an alternative, the

hedging measure will increase the level of risk for the organisation and exponentially

increase the chance of losses. In addition, this kind of measure mainly leads to speculation

and not hedge the underlying assets that needs to be hedged by the organisation is not being

targeted.

The maturity mismatch is also considered to one of the problematic conditions for

organisation, as it increases the risk attribute of the hedging measure. In addition, the

maturity mismatch arises, when the underlying asset maturity does not match the hedging

instrument maturity. This difference in contract maturity level mainly raises the basic risk of

the underlying asset, which is being used by the organisation for its hedging purpose.

Furthermore, the organisation needs to follow the roll over method for continuing the hedge,

as the maturity level of the product delivery is not being hedged by the organisation. Magnan,

Menini and Parbonetti (2015) mentioned that companies use the maturity mismatch to

improve the effectives of the hedge, which can only be possible with adequate research and

4 | P a g e

for the particular asset. Therefore, in context of hedging it can be detected that underlying

asset mismatch arises only when the underlying asset does match the hedging instrument.

This mainly creates an imperfect hedge, which increases the level of risk attributes for the

organisation conducting the hedge. Dickinson et al. (2017) indicates that investors and

organisation mainly use hedging process for reducing the risk attributes of their portfolio

exposure. On the other hand, Corbett and Smodis (2018) criticises that without adequate

research the hedging measure mainly increases the risk level and raises the chances of loss

from fluctuating prices.

Therefore, organisations dealing with jet oil cannot hedge their exposure in the

commodity by hedging an underlying asset of heating oil futures, as the price valuation and

output of the commodities are different. This measure will not allow the organisation to

adequately hedge their products and reduce the actual exposure. As an alternative, the

hedging measure will increase the level of risk for the organisation and exponentially

increase the chance of losses. In addition, this kind of measure mainly leads to speculation

and not hedge the underlying assets that needs to be hedged by the organisation is not being

targeted.

The maturity mismatch is also considered to one of the problematic conditions for

organisation, as it increases the risk attribute of the hedging measure. In addition, the

maturity mismatch arises, when the underlying asset maturity does not match the hedging

instrument maturity. This difference in contract maturity level mainly raises the basic risk of

the underlying asset, which is being used by the organisation for its hedging purpose.

Furthermore, the organisation needs to follow the roll over method for continuing the hedge,

as the maturity level of the product delivery is not being hedged by the organisation. Magnan,

Menini and Parbonetti (2015) mentioned that companies use the maturity mismatch to

improve the effectives of the hedge, which can only be possible with adequate research and

4 | P a g e

ACCOUNTING AND FINANCIAL REPORTING

detection of the fluctuating prices. Bessis (2015) further indicated that when the beta of the

stock is 1 and no maturity mismatch is present then risk from the underlying asset is nullified.

Therefore, it can be detected that organisations using the mismatch underlying asset

and mismatch maturity will eventually increase the level of basic risk from their hedging

instrument. In addition, from the evaluation it can be detected that the measure increases the

level of risk from investment and does accurately hedge the exposure of the organisation.

However, utilisation of the both the mismatch underlying asset and mismatch maturity can be

conducted by the organisation, when the actual commodity instrument cannot be found in the

market for hedging. The use of excessive research and correlation data can be used for

conducting the hedge and securing the exposure (Goodhart and Perotti 2015).

Question B2.3: Discussing how maturity mismatch is critical in the case of

Metallgescellschaft AG

The case study of MGRM directly sheds light on the criticality of the maturity

mismatch, which needs to be taken into consideration by the organisation. In addition, the

case study of MGRM also depicts that the hedging instruments maturity needs to be at the

same level with the underlying asset delivery maturity. The occurrence of mismatch maturity

will eventually raise the level of basic risk for the organisation, which led to the high losses

incurred by MGRM at the end of 1993. The implementation of the strategy raised two critical

consequences for MGRM, which led to the massive liquidity crisis for the company. This

increment in massive liquidity problem did not indicate the use of adequate hedging measure

imposed by the organisation.

5 | P a g e

detection of the fluctuating prices. Bessis (2015) further indicated that when the beta of the

stock is 1 and no maturity mismatch is present then risk from the underlying asset is nullified.

Therefore, it can be detected that organisations using the mismatch underlying asset

and mismatch maturity will eventually increase the level of basic risk from their hedging

instrument. In addition, from the evaluation it can be detected that the measure increases the

level of risk from investment and does accurately hedge the exposure of the organisation.

However, utilisation of the both the mismatch underlying asset and mismatch maturity can be

conducted by the organisation, when the actual commodity instrument cannot be found in the

market for hedging. The use of excessive research and correlation data can be used for

conducting the hedge and securing the exposure (Goodhart and Perotti 2015).

Question B2.3: Discussing how maturity mismatch is critical in the case of

Metallgescellschaft AG

The case study of MGRM directly sheds light on the criticality of the maturity

mismatch, which needs to be taken into consideration by the organisation. In addition, the

case study of MGRM also depicts that the hedging instruments maturity needs to be at the

same level with the underlying asset delivery maturity. The occurrence of mismatch maturity

will eventually raise the level of basic risk for the organisation, which led to the high losses

incurred by MGRM at the end of 1993. The implementation of the strategy raised two critical

consequences for MGRM, which led to the massive liquidity crisis for the company. This

increment in massive liquidity problem did not indicate the use of adequate hedging measure

imposed by the organisation.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCIAL REPORTING

.

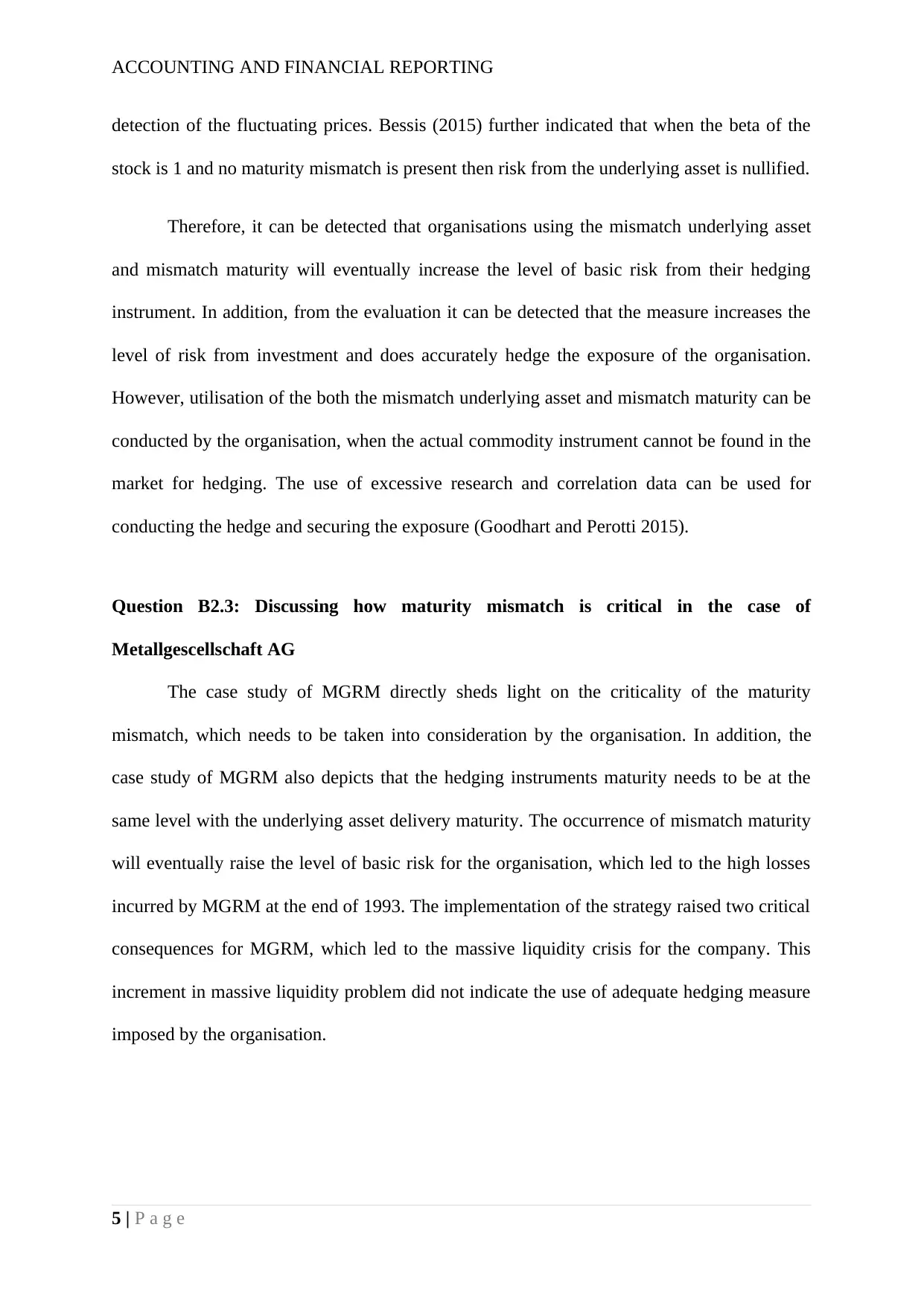

Figure 3: The income and losses from delivery contract and Hedged contract

(Source: Mello and Parsons 1995)

The above figure relates to the cash inflow and outflow of MGRM, where the

mismatch hedges were used by the organisation, which led to the accumulation of high cash

outflows. In addition, the use of mismatched hedges increased the level of variance for the

forms cash flow and exposed MGRM to excessive amount of basic risk, as the short dated

future contracts were not compensated by the long dated delivery obligations. Hence, the use

of short term hedge position for long term delivery obligations led to cash flow troubles for

the organisation, which can be seen in the above figure. The use of rolling method for

mismatched maturity is directly affecting the level of cash flows of MGRM and escalated the

losses from the hedging instrument, as the basic risk from investment rose exponentially

(Culp and Miller 1995).

6 | P a g e

.

Figure 3: The income and losses from delivery contract and Hedged contract

(Source: Mello and Parsons 1995)

The above figure relates to the cash inflow and outflow of MGRM, where the

mismatch hedges were used by the organisation, which led to the accumulation of high cash

outflows. In addition, the use of mismatched hedges increased the level of variance for the

forms cash flow and exposed MGRM to excessive amount of basic risk, as the short dated

future contracts were not compensated by the long dated delivery obligations. Hence, the use

of short term hedge position for long term delivery obligations led to cash flow troubles for

the organisation, which can be seen in the above figure. The use of rolling method for

mismatched maturity is directly affecting the level of cash flows of MGRM and escalated the

losses from the hedging instrument, as the basic risk from investment rose exponentially

(Culp and Miller 1995).

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCIAL REPORTING

The scenario of the cash flow problems is depicted in figure 1, where the continuous

decline in short term future prices was directly increasing the negative balance in

accumulated net cash flow. The rollover method also played a vital role in accumulating the

losses, where the actual deliver of the contract was not being hedged by the organisation,

which was being conducted in short term (Converse 2017). The delivery on monthly basis

was at 1.28 million bbl, while the monthly hedge position was 154.0 million bbl and

declining. This mismatch in maturity date raised the basic level of risk and projected a non-

functionally hedge position for MGRM.

7 | P a g e

The scenario of the cash flow problems is depicted in figure 1, where the continuous

decline in short term future prices was directly increasing the negative balance in

accumulated net cash flow. The rollover method also played a vital role in accumulating the

losses, where the actual deliver of the contract was not being hedged by the organisation,

which was being conducted in short term (Converse 2017). The delivery on monthly basis

was at 1.28 million bbl, while the monthly hedge position was 154.0 million bbl and

declining. This mismatch in maturity date raised the basic level of risk and projected a non-

functionally hedge position for MGRM.

7 | P a g e

ACCOUNTING AND FINANCIAL REPORTING

Reference:

Abdel-Khalik, A.R., 2014. Prospect Theory predictions in the field: Risk seekers in settings

of weak accounting controls. Journal of Accounting Literature, 33(1-2), pp.58-84.

Bessis, J., 2015. Risk management in banking. John Wiley & Sons.

Converse, N., 2017. Uncertainty, capital flows, and maturity mismatch. Journal of

International Money and Finance.

Corbett, T.P. and Smodis, S., 2018. Buy-side liquidity risk management best

practices. Journal of Risk Management in Financial Institutions, 11(3), pp.207-217.

Culp, Christopher L. and Miller, Merton H., 1995, Metallgesellschaft and the Economics of

Synthetic Storage, Journal of Applied Corporate Finance, Vol. 7.4, P62-76

Dickinson, D.L., Chaudhuri, A. and Greenaway-McGrevy, R., 2017. Trading while sleepy?

Circadian mismatch and excess volatility in a global experimental asset market.

Goodhart, C.A. and Perotti, E., 2015. Maturity mismatch stretching: banking has taken a

wrong turn. CEPR Policy Insight, 81.

Magnan, M., Menini, A. and Parbonetti, A., 2015. Fair value accounting: information or

confusion for financial markets?. Review of Accounting Studies, 20(1), pp.559-591.

Mello, A.S. and Parsons, J.E., 1995. Maturity structure of a hedge matters: Lessons from the

Metallgesellschaft debacle. Journal of Applied Corporate Finance, 8(1), pp.106-121.

Neuberger, A., 2015. Rollover Risk. Wiley Encyclopedia of Management, pp.1-2.

8 | P a g e

Reference:

Abdel-Khalik, A.R., 2014. Prospect Theory predictions in the field: Risk seekers in settings

of weak accounting controls. Journal of Accounting Literature, 33(1-2), pp.58-84.

Bessis, J., 2015. Risk management in banking. John Wiley & Sons.

Converse, N., 2017. Uncertainty, capital flows, and maturity mismatch. Journal of

International Money and Finance.

Corbett, T.P. and Smodis, S., 2018. Buy-side liquidity risk management best

practices. Journal of Risk Management in Financial Institutions, 11(3), pp.207-217.

Culp, Christopher L. and Miller, Merton H., 1995, Metallgesellschaft and the Economics of

Synthetic Storage, Journal of Applied Corporate Finance, Vol. 7.4, P62-76

Dickinson, D.L., Chaudhuri, A. and Greenaway-McGrevy, R., 2017. Trading while sleepy?

Circadian mismatch and excess volatility in a global experimental asset market.

Goodhart, C.A. and Perotti, E., 2015. Maturity mismatch stretching: banking has taken a

wrong turn. CEPR Policy Insight, 81.

Magnan, M., Menini, A. and Parbonetti, A., 2015. Fair value accounting: information or

confusion for financial markets?. Review of Accounting Studies, 20(1), pp.559-591.

Mello, A.S. and Parsons, J.E., 1995. Maturity structure of a hedge matters: Lessons from the

Metallgesellschaft debacle. Journal of Applied Corporate Finance, 8(1), pp.106-121.

Neuberger, A., 2015. Rollover Risk. Wiley Encyclopedia of Management, pp.1-2.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.