Detailed Financial Performance Analysis Report: Metro Bank PLC

VerifiedAdded on 2023/01/12

|16

|3922

|38

Report

AI Summary

This report provides a detailed financial analysis of Metro Bank PLC, examining its performance from 2015 to 2018. The analysis includes a general overview of the bank, a critical evaluation of its balance sheet and income statement, and a thorough examination of its performance using various financial ratios, including profitability, efficiency, asset quality, and capital adequacy ratios. The report also assesses the impact of changes in the banking sector on Metro Bank PLC's performance and provides an outlook on its expected future performance. The analysis highlights key trends in the bank's financial health, such as the growth in assets, changes in deposit and debt levels, and fluctuations in profitability ratios. The report utilizes financial data to provide a comprehensive assessment of Metro Bank PLC's financial position and operational efficiency, offering valuable insights into its strengths, weaknesses, and future prospects. The report concludes with an overview of the bank's current standing and potential future growth.

Modern Banking

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

1. General overview of bank..................................................................................................3

2. Critically analyse of bank with BS and IS..........................................................................3

3. Critically analyse of bank’s performance with different ratios..........................................6

4. Evaluation of changes in banking sectors........................................................................10

5. Expected future performance...........................................................................................12

CONCLUSION..............................................................................................................................12

REEFRENCES..............................................................................................................................13

APPENDIX....................................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

1. General overview of bank..................................................................................................3

2. Critically analyse of bank with BS and IS..........................................................................3

3. Critically analyse of bank’s performance with different ratios..........................................6

4. Evaluation of changes in banking sectors........................................................................10

5. Expected future performance...........................................................................................12

CONCLUSION..............................................................................................................................12

REEFRENCES..............................................................................................................................13

APPENDIX....................................................................................................................................14

INTRODUCTION

In the present world, each and every concept of business is chaining as well as different

advance techniques and technologies have been adapted by businesses in order to increase

profitability (Peters and Panayi, 2016). The modern banking is concepts related with introduction

of e banking with use of advance technology that makes easier banking services for customer. E

banking mainly includes Internet banking and banking through other electronic modes such as

ATM, M-banking etc. which save cost and time for both parties (customer as well as bank

members). In order to better understand the concept of modern banking Metro Bank PLC

MBNKF is selected.

In this report, analysis of bank on the basis of BS, IS and different ratios are discussed.

Impact of changes in banking industry which influence on bank performance is shown and

expected future performance in upcoming years are defined.

TASK

1. General overview of bank

Metro Bank plc is a UK-based commercial and investment bank, established by Vernon

Hill and Anthony Thomson in 2010. It became the first major high street financial institution to

be introduced in the UK in over 150 years which is mentioned on the LSX. Metro Bank offers

financial facilities to accounts holder to both individuals and companies. It is approved by the

Prudential Regulation Agency and governed from both the Authority for financial behaviour as

well as the Law for Prudential Compliance. During the first quarter of 2013, Metro Bank raised

its bank customers by 50 per cent for a sum of 200,000 deposit accounts, such as 15,000

company accounts. This planned to establish 200 UK outlets by 2020. In August 2013, Metro

Bank purchased SME Financial services and in May 2014 rebranded the company to Metro Bank

SME Fund (About Metro bank plc, 2020).

2. Critically analyse of bank with BS and IS

The balance sheet is often called the financial condition document that reflects the

financial circumstances of a business in the end of a defined accounting period. In general term it

is define as a "snapshot" of the financial condition of the company which can be used to

determine the total assets, liabilities and debts and equity hold for a year. In the context of Metro

In the present world, each and every concept of business is chaining as well as different

advance techniques and technologies have been adapted by businesses in order to increase

profitability (Peters and Panayi, 2016). The modern banking is concepts related with introduction

of e banking with use of advance technology that makes easier banking services for customer. E

banking mainly includes Internet banking and banking through other electronic modes such as

ATM, M-banking etc. which save cost and time for both parties (customer as well as bank

members). In order to better understand the concept of modern banking Metro Bank PLC

MBNKF is selected.

In this report, analysis of bank on the basis of BS, IS and different ratios are discussed.

Impact of changes in banking industry which influence on bank performance is shown and

expected future performance in upcoming years are defined.

TASK

1. General overview of bank

Metro Bank plc is a UK-based commercial and investment bank, established by Vernon

Hill and Anthony Thomson in 2010. It became the first major high street financial institution to

be introduced in the UK in over 150 years which is mentioned on the LSX. Metro Bank offers

financial facilities to accounts holder to both individuals and companies. It is approved by the

Prudential Regulation Agency and governed from both the Authority for financial behaviour as

well as the Law for Prudential Compliance. During the first quarter of 2013, Metro Bank raised

its bank customers by 50 per cent for a sum of 200,000 deposit accounts, such as 15,000

company accounts. This planned to establish 200 UK outlets by 2020. In August 2013, Metro

Bank purchased SME Financial services and in May 2014 rebranded the company to Metro Bank

SME Fund (About Metro bank plc, 2020).

2. Critically analyse of bank with BS and IS

The balance sheet is often called the financial condition document that reflects the

financial circumstances of a business in the end of a defined accounting period. In general term it

is define as a "snapshot" of the financial condition of the company which can be used to

determine the total assets, liabilities and debts and equity hold for a year. In the context of Metro

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

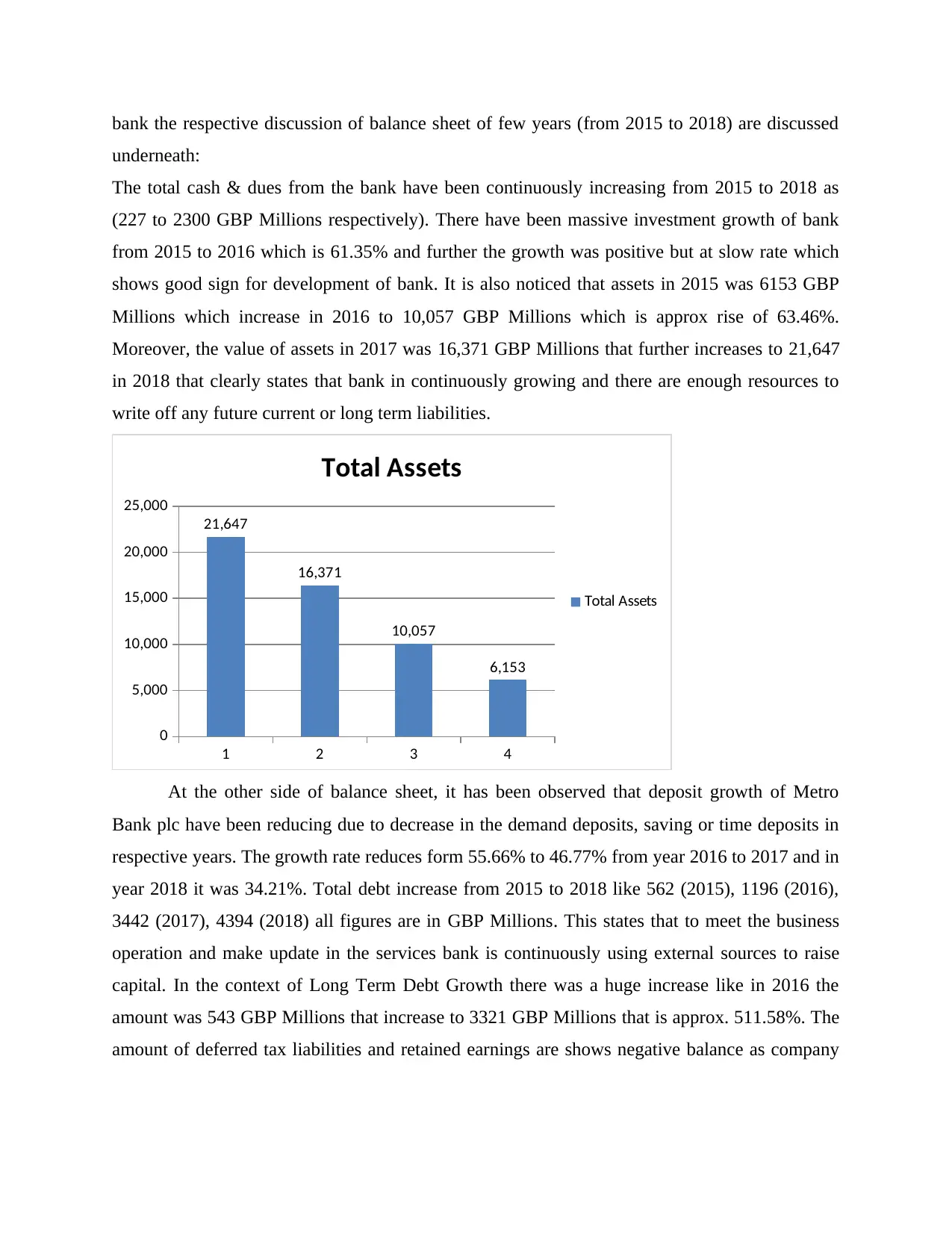

bank the respective discussion of balance sheet of few years (from 2015 to 2018) are discussed

underneath:

The total cash & dues from the bank have been continuously increasing from 2015 to 2018 as

(227 to 2300 GBP Millions respectively). There have been massive investment growth of bank

from 2015 to 2016 which is 61.35% and further the growth was positive but at slow rate which

shows good sign for development of bank. It is also noticed that assets in 2015 was 6153 GBP

Millions which increase in 2016 to 10,057 GBP Millions which is approx rise of 63.46%.

Moreover, the value of assets in 2017 was 16,371 GBP Millions that further increases to 21,647

in 2018 that clearly states that bank in continuously growing and there are enough resources to

write off any future current or long term liabilities.

1 2 3 4

0

5,000

10,000

15,000

20,000

25,000

21,647

16,371

10,057

6,153

Total Assets

Total Assets

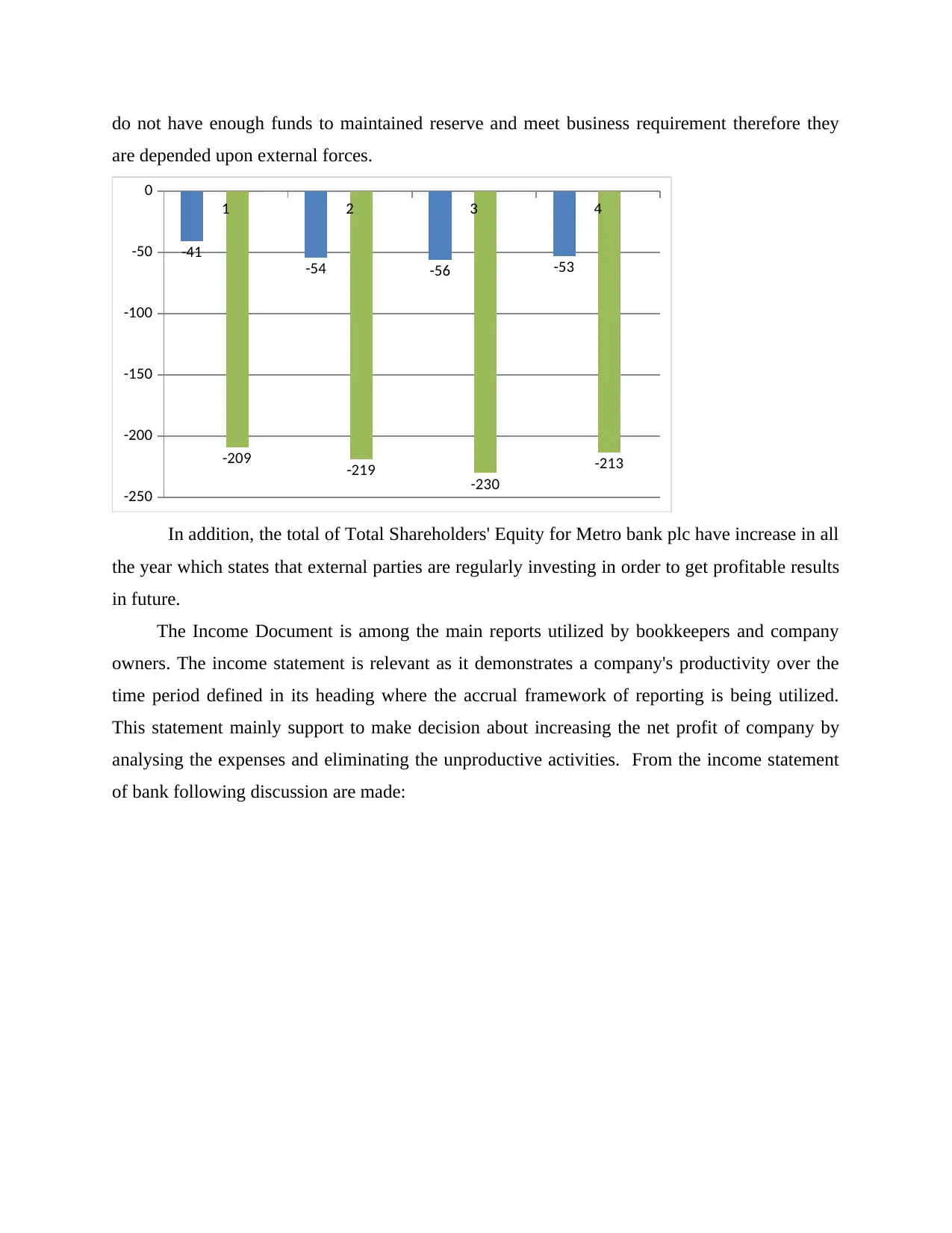

At the other side of balance sheet, it has been observed that deposit growth of Metro

Bank plc have been reducing due to decrease in the demand deposits, saving or time deposits in

respective years. The growth rate reduces form 55.66% to 46.77% from year 2016 to 2017 and in

year 2018 it was 34.21%. Total debt increase from 2015 to 2018 like 562 (2015), 1196 (2016),

3442 (2017), 4394 (2018) all figures are in GBP Millions. This states that to meet the business

operation and make update in the services bank is continuously using external sources to raise

capital. In the context of Long Term Debt Growth there was a huge increase like in 2016 the

amount was 543 GBP Millions that increase to 3321 GBP Millions that is approx. 511.58%. The

amount of deferred tax liabilities and retained earnings are shows negative balance as company

underneath:

The total cash & dues from the bank have been continuously increasing from 2015 to 2018 as

(227 to 2300 GBP Millions respectively). There have been massive investment growth of bank

from 2015 to 2016 which is 61.35% and further the growth was positive but at slow rate which

shows good sign for development of bank. It is also noticed that assets in 2015 was 6153 GBP

Millions which increase in 2016 to 10,057 GBP Millions which is approx rise of 63.46%.

Moreover, the value of assets in 2017 was 16,371 GBP Millions that further increases to 21,647

in 2018 that clearly states that bank in continuously growing and there are enough resources to

write off any future current or long term liabilities.

1 2 3 4

0

5,000

10,000

15,000

20,000

25,000

21,647

16,371

10,057

6,153

Total Assets

Total Assets

At the other side of balance sheet, it has been observed that deposit growth of Metro

Bank plc have been reducing due to decrease in the demand deposits, saving or time deposits in

respective years. The growth rate reduces form 55.66% to 46.77% from year 2016 to 2017 and in

year 2018 it was 34.21%. Total debt increase from 2015 to 2018 like 562 (2015), 1196 (2016),

3442 (2017), 4394 (2018) all figures are in GBP Millions. This states that to meet the business

operation and make update in the services bank is continuously using external sources to raise

capital. In the context of Long Term Debt Growth there was a huge increase like in 2016 the

amount was 543 GBP Millions that increase to 3321 GBP Millions that is approx. 511.58%. The

amount of deferred tax liabilities and retained earnings are shows negative balance as company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

do not have enough funds to maintained reserve and meet business requirement therefore they

are depended upon external forces.

1 2 3 4

-250

-200

-150

-100

-50

0

-41

-54 -56 -53

-209 -219 -230

-213

In addition, the total of Total Shareholders' Equity for Metro bank plc have increase in all

the year which states that external parties are regularly investing in order to get profitable results

in future.

The Income Document is among the main reports utilized by bookkeepers and company

owners. The income statement is relevant as it demonstrates a company's productivity over the

time period defined in its heading where the accrual framework of reporting is being utilized.

This statement mainly support to make decision about increasing the net profit of company by

analysing the expenses and eliminating the unproductive activities. From the income statement

of bank following discussion are made:

are depended upon external forces.

1 2 3 4

-250

-200

-150

-100

-50

0

-41

-54 -56 -53

-209 -219 -230

-213

In addition, the total of Total Shareholders' Equity for Metro bank plc have increase in all

the year which states that external parties are regularly investing in order to get profitable results

in future.

The Income Document is among the main reports utilized by bookkeepers and company

owners. The income statement is relevant as it demonstrates a company's productivity over the

time period defined in its heading where the accrual framework of reporting is being utilized.

This statement mainly support to make decision about increasing the net profit of company by

analysing the expenses and eliminating the unproductive activities. From the income statement

of bank following discussion are made:

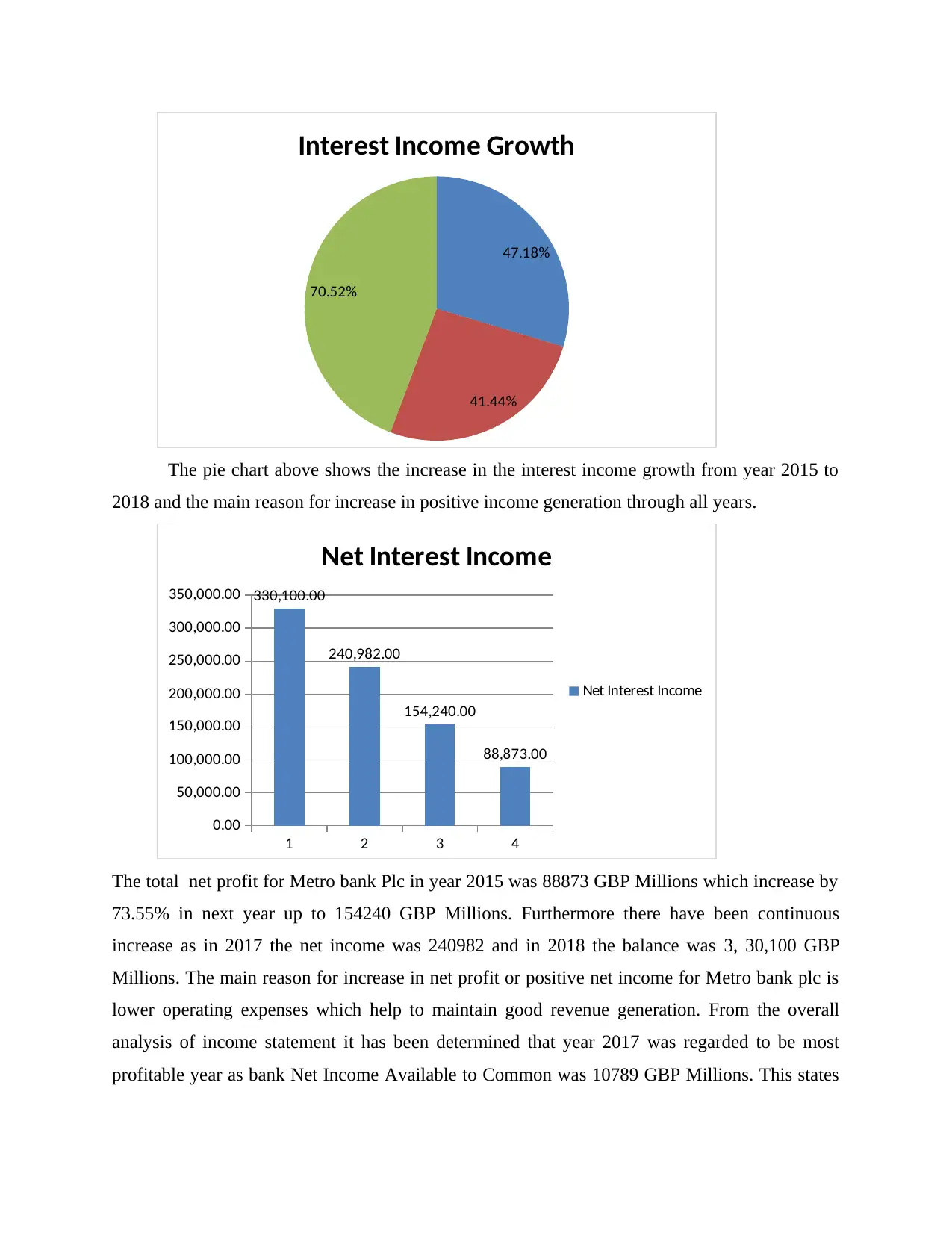

47.18%

41.44%

70.52%

Interest Income Growth

The pie chart above shows the increase in the interest income growth from year 2015 to

2018 and the main reason for increase in positive income generation through all years.

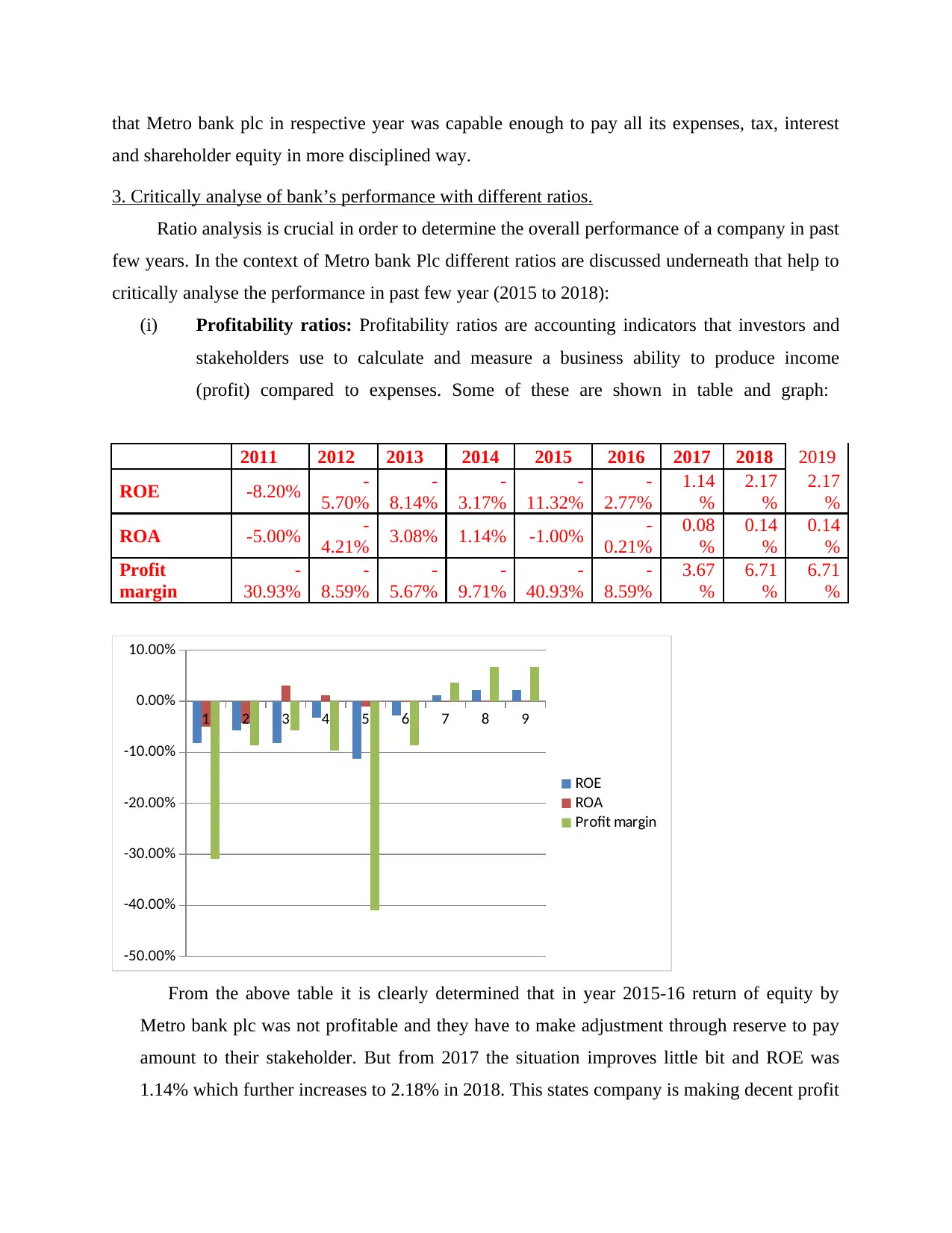

1 2 3 4

0.00

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

350,000.00 330,100.00

240,982.00

154,240.00

88,873.00

Net Interest Income

Net Interest Income

The total net profit for Metro bank Plc in year 2015 was 88873 GBP Millions which increase by

73.55% in next year up to 154240 GBP Millions. Furthermore there have been continuous

increase as in 2017 the net income was 240982 and in 2018 the balance was 3, 30,100 GBP

Millions. The main reason for increase in net profit or positive net income for Metro bank plc is

lower operating expenses which help to maintain good revenue generation. From the overall

analysis of income statement it has been determined that year 2017 was regarded to be most

profitable year as bank Net Income Available to Common was 10789 GBP Millions. This states

41.44%

70.52%

Interest Income Growth

The pie chart above shows the increase in the interest income growth from year 2015 to

2018 and the main reason for increase in positive income generation through all years.

1 2 3 4

0.00

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

350,000.00 330,100.00

240,982.00

154,240.00

88,873.00

Net Interest Income

Net Interest Income

The total net profit for Metro bank Plc in year 2015 was 88873 GBP Millions which increase by

73.55% in next year up to 154240 GBP Millions. Furthermore there have been continuous

increase as in 2017 the net income was 240982 and in 2018 the balance was 3, 30,100 GBP

Millions. The main reason for increase in net profit or positive net income for Metro bank plc is

lower operating expenses which help to maintain good revenue generation. From the overall

analysis of income statement it has been determined that year 2017 was regarded to be most

profitable year as bank Net Income Available to Common was 10789 GBP Millions. This states

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that Metro bank plc in respective year was capable enough to pay all its expenses, tax, interest

and shareholder equity in more disciplined way.

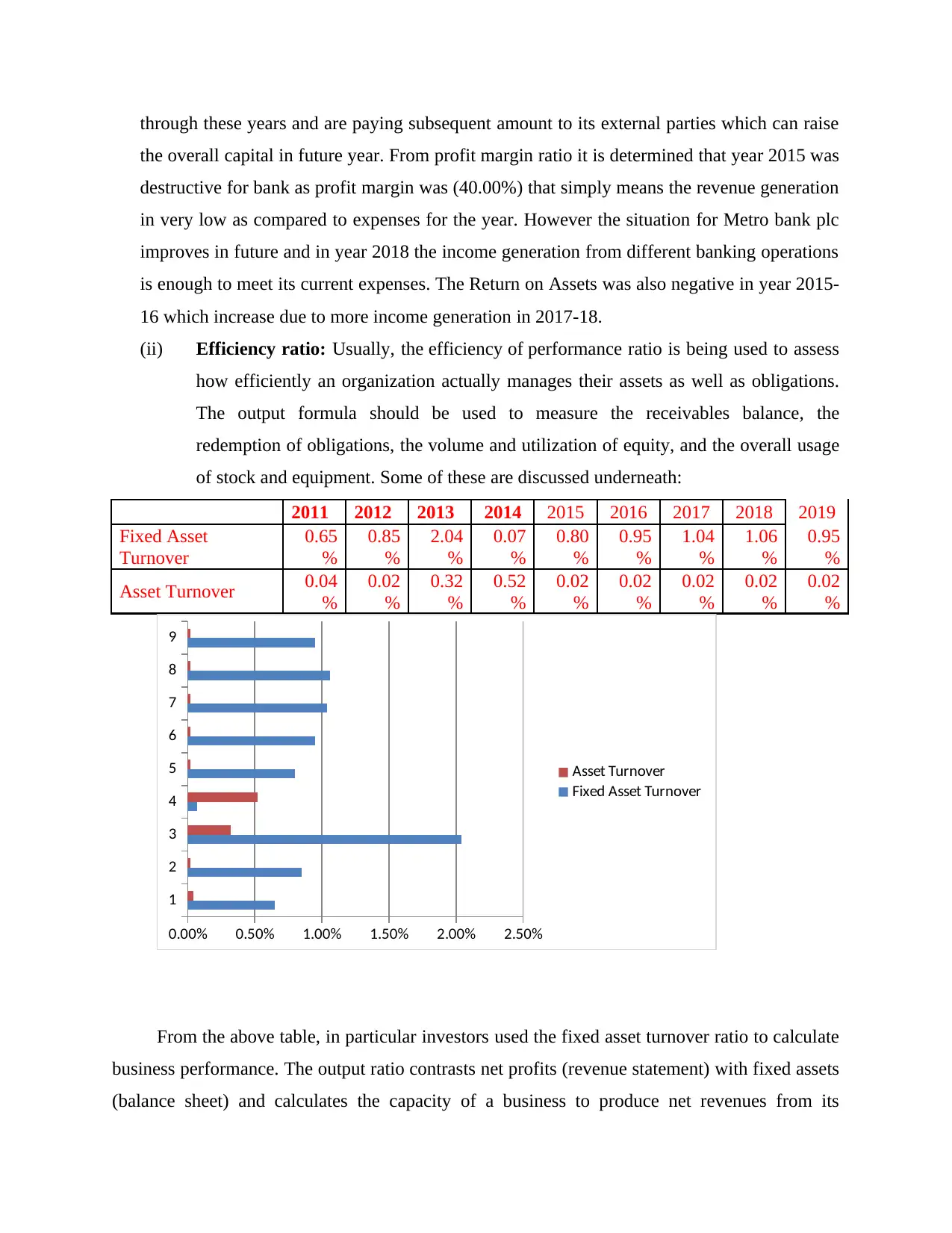

3. Critically analyse of bank’s performance with different ratios.

Ratio analysis is crucial in order to determine the overall performance of a company in past

few years. In the context of Metro bank Plc different ratios are discussed underneath that help to

critically analyse the performance in past few year (2015 to 2018):

(i) Profitability ratios: Profitability ratios are accounting indicators that investors and

stakeholders use to calculate and measure a business ability to produce income

(profit) compared to expenses. Some of these are shown in table and graph:

2011 2012 2013 2014 2015 2016 2017 2018 2019

ROE -8.20% -

5.70%

-

8.14%

-

3.17%

-

11.32%

-

2.77%

1.14

%

2.17

%

2.17

%

ROA -5.00% -

4.21% 3.08% 1.14% -1.00% -

0.21%

0.08

%

0.14

%

0.14

%

Profit

margin

-

30.93%

-

8.59%

-

5.67%

-

9.71%

-

40.93%

-

8.59%

3.67

%

6.71

%

6.71

%

1 2 3 4 5 6 7 8 9

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

ROE

ROA

Profit margin

From the above table it is clearly determined that in year 2015-16 return of equity by

Metro bank plc was not profitable and they have to make adjustment through reserve to pay

amount to their stakeholder. But from 2017 the situation improves little bit and ROE was

1.14% which further increases to 2.18% in 2018. This states company is making decent profit

and shareholder equity in more disciplined way.

3. Critically analyse of bank’s performance with different ratios.

Ratio analysis is crucial in order to determine the overall performance of a company in past

few years. In the context of Metro bank Plc different ratios are discussed underneath that help to

critically analyse the performance in past few year (2015 to 2018):

(i) Profitability ratios: Profitability ratios are accounting indicators that investors and

stakeholders use to calculate and measure a business ability to produce income

(profit) compared to expenses. Some of these are shown in table and graph:

2011 2012 2013 2014 2015 2016 2017 2018 2019

ROE -8.20% -

5.70%

-

8.14%

-

3.17%

-

11.32%

-

2.77%

1.14

%

2.17

%

2.17

%

ROA -5.00% -

4.21% 3.08% 1.14% -1.00% -

0.21%

0.08

%

0.14

%

0.14

%

Profit

margin

-

30.93%

-

8.59%

-

5.67%

-

9.71%

-

40.93%

-

8.59%

3.67

%

6.71

%

6.71

%

1 2 3 4 5 6 7 8 9

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

ROE

ROA

Profit margin

From the above table it is clearly determined that in year 2015-16 return of equity by

Metro bank plc was not profitable and they have to make adjustment through reserve to pay

amount to their stakeholder. But from 2017 the situation improves little bit and ROE was

1.14% which further increases to 2.18% in 2018. This states company is making decent profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

through these years and are paying subsequent amount to its external parties which can raise

the overall capital in future year. From profit margin ratio it is determined that year 2015 was

destructive for bank as profit margin was (40.00%) that simply means the revenue generation

in very low as compared to expenses for the year. However the situation for Metro bank plc

improves in future and in year 2018 the income generation from different banking operations

is enough to meet its current expenses. The Return on Assets was also negative in year 2015-

16 which increase due to more income generation in 2017-18.

(ii) Efficiency ratio: Usually, the efficiency of performance ratio is being used to assess

how efficiently an organization actually manages their assets as well as obligations.

The output formula should be used to measure the receivables balance, the

redemption of obligations, the volume and utilization of equity, and the overall usage

of stock and equipment. Some of these are discussed underneath:

2011 2012 2013 2014 2015 2016 2017 2018 2019

Fixed Asset

Turnover

0.65

%

0.85

%

2.04

%

0.07

%

0.80

%

0.95

%

1.04

%

1.06

%

0.95

%

Asset Turnover 0.04

%

0.02

%

0.32

%

0.52

%

0.02

%

0.02

%

0.02

%

0.02

%

0.02

%

1

2

3

4

5

6

7

8

9

0.00% 0.50% 1.00% 1.50% 2.00% 2.50%

Asset Turnover

Fixed Asset Turnover

From the above table, in particular investors used the fixed asset turnover ratio to calculate

business performance. The output ratio contrasts net profits (revenue statement) with fixed assets

(balance sheet) and calculates the capacity of a business to produce net revenues from its

the overall capital in future year. From profit margin ratio it is determined that year 2015 was

destructive for bank as profit margin was (40.00%) that simply means the revenue generation

in very low as compared to expenses for the year. However the situation for Metro bank plc

improves in future and in year 2018 the income generation from different banking operations

is enough to meet its current expenses. The Return on Assets was also negative in year 2015-

16 which increase due to more income generation in 2017-18.

(ii) Efficiency ratio: Usually, the efficiency of performance ratio is being used to assess

how efficiently an organization actually manages their assets as well as obligations.

The output formula should be used to measure the receivables balance, the

redemption of obligations, the volume and utilization of equity, and the overall usage

of stock and equipment. Some of these are discussed underneath:

2011 2012 2013 2014 2015 2016 2017 2018 2019

Fixed Asset

Turnover

0.65

%

0.85

%

2.04

%

0.07

%

0.80

%

0.95

%

1.04

%

1.06

%

0.95

%

Asset Turnover 0.04

%

0.02

%

0.32

%

0.52

%

0.02

%

0.02

%

0.02

%

0.02

%

0.02

%

1

2

3

4

5

6

7

8

9

0.00% 0.50% 1.00% 1.50% 2.00% 2.50%

Asset Turnover

Fixed Asset Turnover

From the above table, in particular investors used the fixed asset turnover ratio to calculate

business performance. The output ratio contrasts net profits (revenue statement) with fixed assets

(balance sheet) and calculates the capacity of a business to produce net revenues from its

expenditures in working capital, including land, plants and machinery. A higher ratio means that

management is allowing more efficient use of the financial assets. Therefore a large FAT ratio do

not informs about the capacity of a business to produce higher income or increase cash flows.

Thus in year 2015 the FAT for Metro bank plc was 0.8% which increases to 0.95% in year 2016

and keeps on increase year by year like 1.04% in 2017 and 1.06% in 2018. This simply means

the bank have been regularly making good use of their assets and other equivalent in producing

decent and faithful sales through all years. The increasing percentages also defines that sales is

rising at decent rate which can be effective in meeting any future expenses for bank.

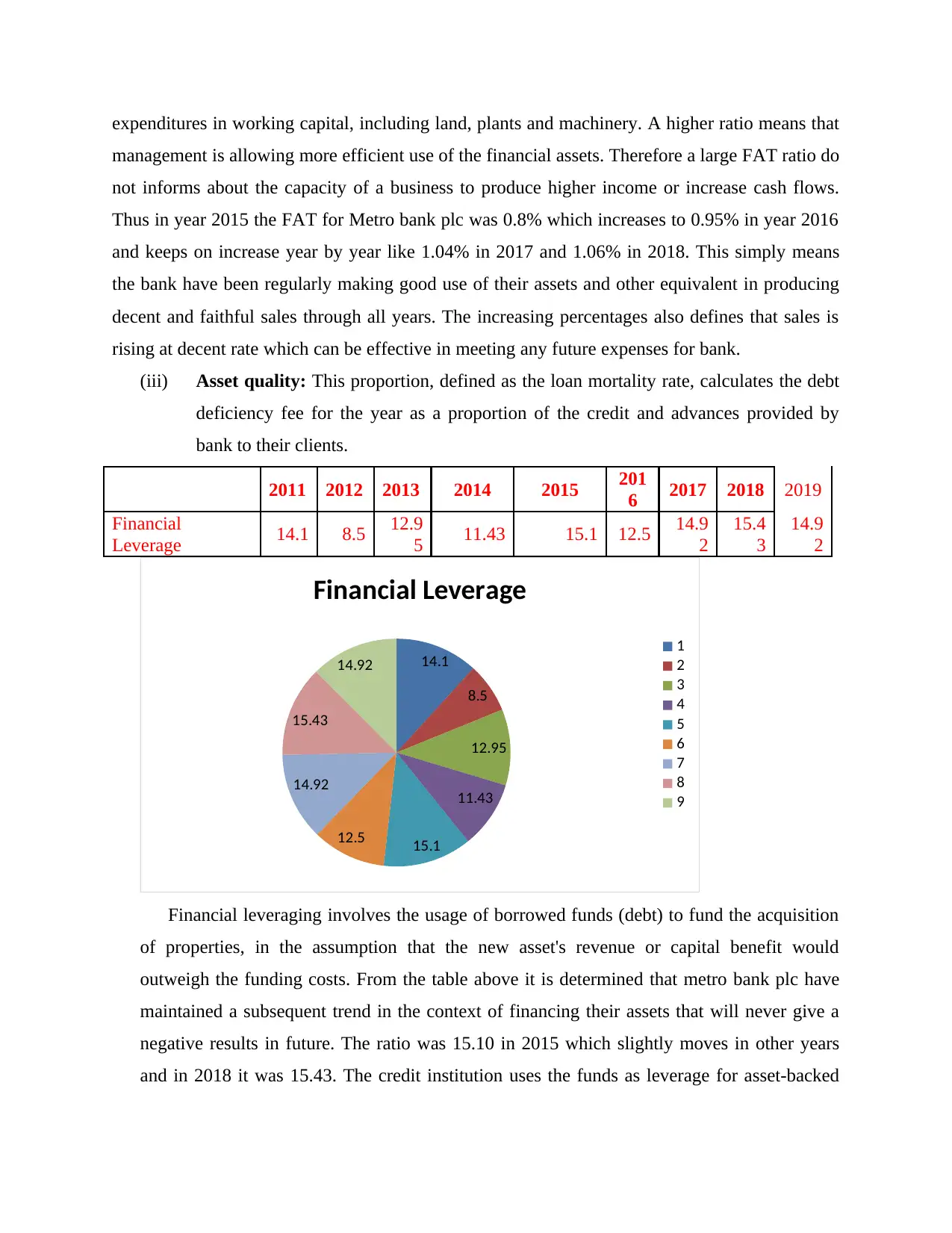

(iii) Asset quality: This proportion, defined as the loan mortality rate, calculates the debt

deficiency fee for the year as a proportion of the credit and advances provided by

bank to their clients.

2011 2012 2013 2014 2015 201

6 2017 2018 2019

Financial

Leverage 14.1 8.5 12.9

5 11.43 15.1 12.5 14.9

2

15.4

3

14.9

2

14.1

8.5

12.95

11.43

15.1

12.5

14.92

15.43

14.92

Financial Leverage

1

2

3

4

5

6

7

8

9

Financial leveraging involves the usage of borrowed funds (debt) to fund the acquisition

of properties, in the assumption that the new asset's revenue or capital benefit would

outweigh the funding costs. From the table above it is determined that metro bank plc have

maintained a subsequent trend in the context of financing their assets that will never give a

negative results in future. The ratio was 15.10 in 2015 which slightly moves in other years

and in 2018 it was 15.43. The credit institution uses the funds as leverage for asset-backed

management is allowing more efficient use of the financial assets. Therefore a large FAT ratio do

not informs about the capacity of a business to produce higher income or increase cash flows.

Thus in year 2015 the FAT for Metro bank plc was 0.8% which increases to 0.95% in year 2016

and keeps on increase year by year like 1.04% in 2017 and 1.06% in 2018. This simply means

the bank have been regularly making good use of their assets and other equivalent in producing

decent and faithful sales through all years. The increasing percentages also defines that sales is

rising at decent rate which can be effective in meeting any future expenses for bank.

(iii) Asset quality: This proportion, defined as the loan mortality rate, calculates the debt

deficiency fee for the year as a proportion of the credit and advances provided by

bank to their clients.

2011 2012 2013 2014 2015 201

6 2017 2018 2019

Financial

Leverage 14.1 8.5 12.9

5 11.43 15.1 12.5 14.9

2

15.4

3

14.9

2

14.1

8.5

12.95

11.43

15.1

12.5

14.92

15.43

14.92

Financial Leverage

1

2

3

4

5

6

7

8

9

Financial leveraging involves the usage of borrowed funds (debt) to fund the acquisition

of properties, in the assumption that the new asset's revenue or capital benefit would

outweigh the funding costs. From the table above it is determined that metro bank plc have

maintained a subsequent trend in the context of financing their assets that will never give a

negative results in future. The ratio was 15.10 in 2015 which slightly moves in other years

and in 2018 it was 15.43. The credit institution uses the funds as leverage for asset-backed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

loans before the investor pays back the mortgage. Throughout the context of a liquidity

lending, it requires the bank overall creditworthiness to finance the assets.

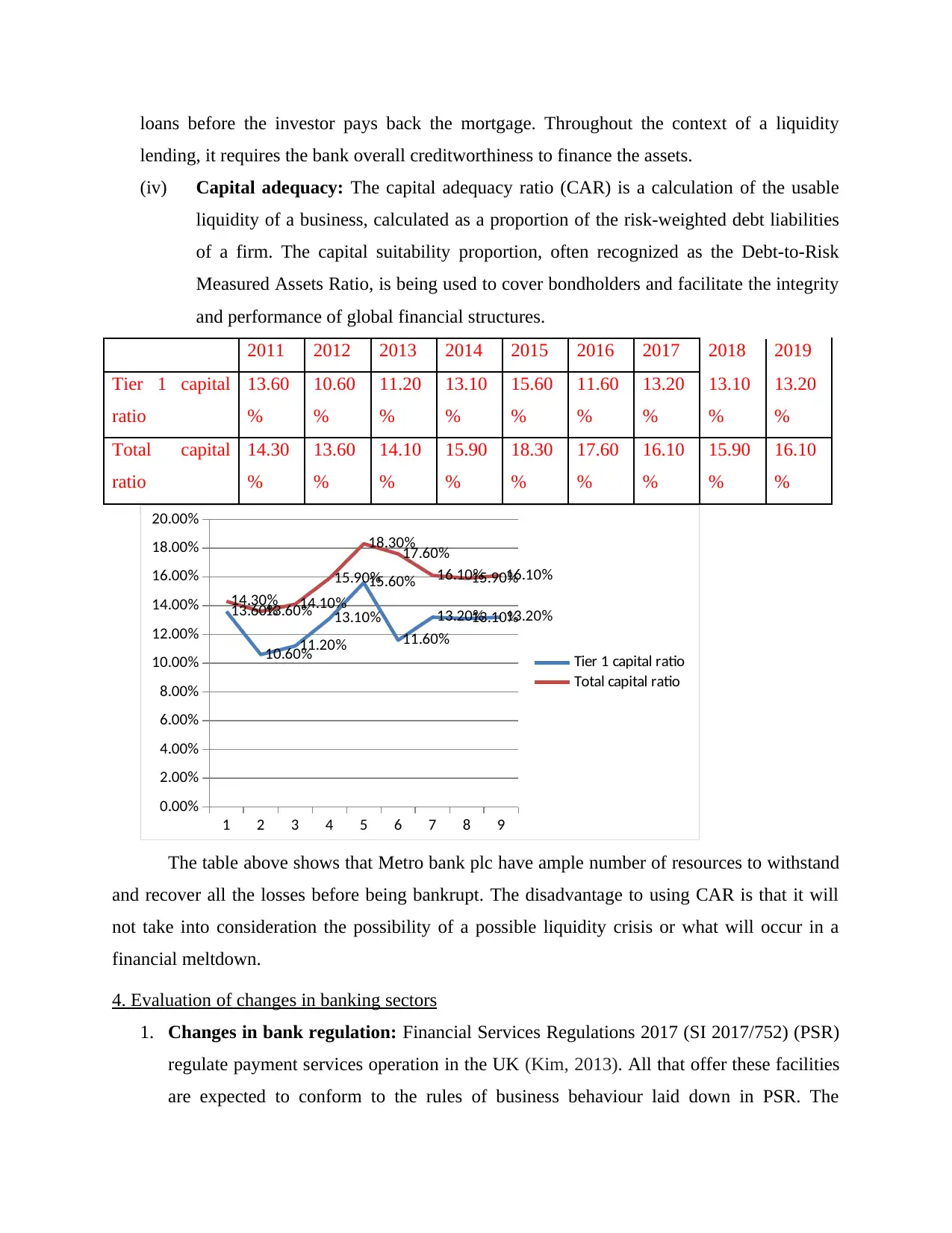

(iv) Capital adequacy: The capital adequacy ratio (CAR) is a calculation of the usable

liquidity of a business, calculated as a proportion of the risk-weighted debt liabilities

of a firm. The capital suitability proportion, often recognized as the Debt-to-Risk

Measured Assets Ratio, is being used to cover bondholders and facilitate the integrity

and performance of global financial structures.

2011 2012 2013 2014 2015 2016 2017 2018 2019

Tier 1 capital

ratio

13.60

%

10.60

%

11.20

%

13.10

%

15.60

%

11.60

%

13.20

%

13.10

%

13.20

%

Total capital

ratio

14.30

%

13.60

%

14.10

%

15.90

%

18.30

%

17.60

%

16.10

%

15.90

%

16.10

%

1 2 3 4 5 6 7 8 9

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

13.60%

10.60%

11.20%

13.10%

15.60%

11.60%

13.20%13.10%13.20%

14.30%

13.60%14.10%

15.90%

18.30%

17.60%

16.10%15.90%16.10%

Tier 1 capital ratio

Total capital ratio

The table above shows that Metro bank plc have ample number of resources to withstand

and recover all the losses before being bankrupt. The disadvantage to using CAR is that it will

not take into consideration the possibility of a possible liquidity crisis or what will occur in a

financial meltdown.

4. Evaluation of changes in banking sectors

1. Changes in bank regulation: Financial Services Regulations 2017 (SI 2017/752) (PSR)

regulate payment services operation in the UK (Kim, 2013). All that offer these facilities

are expected to conform to the rules of business behaviour laid down in PSR. The

lending, it requires the bank overall creditworthiness to finance the assets.

(iv) Capital adequacy: The capital adequacy ratio (CAR) is a calculation of the usable

liquidity of a business, calculated as a proportion of the risk-weighted debt liabilities

of a firm. The capital suitability proportion, often recognized as the Debt-to-Risk

Measured Assets Ratio, is being used to cover bondholders and facilitate the integrity

and performance of global financial structures.

2011 2012 2013 2014 2015 2016 2017 2018 2019

Tier 1 capital

ratio

13.60

%

10.60

%

11.20

%

13.10

%

15.60

%

11.60

%

13.20

%

13.10

%

13.20

%

Total capital

ratio

14.30

%

13.60

%

14.10

%

15.90

%

18.30

%

17.60

%

16.10

%

15.90

%

16.10

%

1 2 3 4 5 6 7 8 9

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

13.60%

10.60%

11.20%

13.10%

15.60%

11.60%

13.20%13.10%13.20%

14.30%

13.60%14.10%

15.90%

18.30%

17.60%

16.10%15.90%16.10%

Tier 1 capital ratio

Total capital ratio

The table above shows that Metro bank plc have ample number of resources to withstand

and recover all the losses before being bankrupt. The disadvantage to using CAR is that it will

not take into consideration the possibility of a possible liquidity crisis or what will occur in a

financial meltdown.

4. Evaluation of changes in banking sectors

1. Changes in bank regulation: Financial Services Regulations 2017 (SI 2017/752) (PSR)

regulate payment services operation in the UK (Kim, 2013). All that offer these facilities

are expected to conform to the rules of business behaviour laid down in PSR. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Banking Act 2009 created a Special Resolution Regime to promote bank settlement of

financial trouble in an organized manner. This provides strategies for stabilizing non-

insolvency, bank bankruptcy litigation, and bank management. The Benchmarks

Legislation (Legislation on indexes that are used as indicators in financial products and

investment transactions or to calculate the output of investment funds) came into effect

on 1 January 2018. The BMR's key goals are to regain investor and customer trust in the

precision, reliability and credibility of benchmarks used as measurements in financial

products and monetary agreements, or to assess investment company results, as well as

the benchmarks setting mechanism itself. The BMR aims to do so by guaranteeing that

metrics are not prone to potential conflicts, are properly used and represent the current

demand or economic environment to be calculated.

2. Increase impact of Fin Tech developments: Clear strategy and management

frameworks that enable banks to adjust their management plans to bring into account

possible revenue implications for emerging technologies as well as the entrants to the

banking sector. Workforce preparation processes to insure to bank personnel are

sufficiently informed and prepared to handle the challenges of Fin tech. Significant new

model licenses and mechanisms of change management to better handle technical

advances as well as company practices. Risk assessment processes in accordance with the

Basel Committee on Sonorous Operational Risk Management (PSMOR) Standards in Fin

tech. Evaluation and examination procedures for innovative goods, facilities or

distribution platforms for enforcement with applicable legislative criteria, including

customer safety, data security, the struggle against money laundering and terrorist

funding (Harmening, 2018).

3. Consolidation in the banking sector: UK banks are planning for a fresh restructuring

surge, as increasing prices, intensified demand and a weak economy pose new

opportunities for groups to counter the five major lenders. Cantered on the financial

crisis, regulations aimed at improving competitiveness in the banking industry have

allowed new institutions and specialized borrowers to thrive. In the context of Metro

banks plc the main challengers at the UK Finance industry advocacy organization, said

others would be merged "almost unavoidable. In a wide number of purposes, mergers and

acquisitions in the banking industry are carried out. In this event, the decision to combine

financial trouble in an organized manner. This provides strategies for stabilizing non-

insolvency, bank bankruptcy litigation, and bank management. The Benchmarks

Legislation (Legislation on indexes that are used as indicators in financial products and

investment transactions or to calculate the output of investment funds) came into effect

on 1 January 2018. The BMR's key goals are to regain investor and customer trust in the

precision, reliability and credibility of benchmarks used as measurements in financial

products and monetary agreements, or to assess investment company results, as well as

the benchmarks setting mechanism itself. The BMR aims to do so by guaranteeing that

metrics are not prone to potential conflicts, are properly used and represent the current

demand or economic environment to be calculated.

2. Increase impact of Fin Tech developments: Clear strategy and management

frameworks that enable banks to adjust their management plans to bring into account

possible revenue implications for emerging technologies as well as the entrants to the

banking sector. Workforce preparation processes to insure to bank personnel are

sufficiently informed and prepared to handle the challenges of Fin tech. Significant new

model licenses and mechanisms of change management to better handle technical

advances as well as company practices. Risk assessment processes in accordance with the

Basel Committee on Sonorous Operational Risk Management (PSMOR) Standards in Fin

tech. Evaluation and examination procedures for innovative goods, facilities or

distribution platforms for enforcement with applicable legislative criteria, including

customer safety, data security, the struggle against money laundering and terrorist

funding (Harmening, 2018).

3. Consolidation in the banking sector: UK banks are planning for a fresh restructuring

surge, as increasing prices, intensified demand and a weak economy pose new

opportunities for groups to counter the five major lenders. Cantered on the financial

crisis, regulations aimed at improving competitiveness in the banking industry have

allowed new institutions and specialized borrowers to thrive. In the context of Metro

banks plc the main challengers at the UK Finance industry advocacy organization, said

others would be merged "almost unavoidable. In a wide number of purposes, mergers and

acquisitions in the banking industry are carried out. In this event, the decision to combine

could be based on more than one reason. Motives that differ in scale or organizational

structure of corporate characteristics, over time, in nations, in market segments or

through business lines of one sector (Landvoigt and Begenau, 2016).

4. Other issues relevant to the changes: The main results about the effect on stability in

the banking sector with UK due to the post-crisis systemic transition concern:

Bank resilience and risk-taking: Globally, banks have improved their exposure to potential

threats by developing capital and liquidity reserves significantly (Weber, 2012). As the recession

often gives way to improved stability in the future, the usage of stress testing by banks and

regulators will help encourage credit in good or poor times. Therefore, developed economies

have switched to more secure sources of financing and invested in healthier, more complicated

investments.

Market sentiment and future bank profitability: Given a rebound in market- equity feelings

for larger companies in recent years, investors in equities have stayed cautious regarding certain

low- banks. A workgroup modelling review shows that more cost and institutional changes needs

to be carried out by certain organisations (Li, 2013).

5. Expected future performance

From the overall analysis it has been determined that in upcoming years the profitability

of Metro bank plc is going to be increase by good margin. The main reason for the same is

growing interest income and reducing operating expenses as well as ROA and ROE also increase

in last couple of years. Moreover, asset manager of Metro bank plc implement special

Administration Regulations 2011 put off a bankruptcy system that pertains to financial

institutions.

CONCLUSION

In the end of report, it is stated that modern banking in a far better way of doing banking

at fingers tips which reduces the burden of customer as more importantly increase the customer

base for banks. Different ratios are effective to define the overall performance of business during

a year and balance sheet and income statement define the actual financial condition of company

during a year.

structure of corporate characteristics, over time, in nations, in market segments or

through business lines of one sector (Landvoigt and Begenau, 2016).

4. Other issues relevant to the changes: The main results about the effect on stability in

the banking sector with UK due to the post-crisis systemic transition concern:

Bank resilience and risk-taking: Globally, banks have improved their exposure to potential

threats by developing capital and liquidity reserves significantly (Weber, 2012). As the recession

often gives way to improved stability in the future, the usage of stress testing by banks and

regulators will help encourage credit in good or poor times. Therefore, developed economies

have switched to more secure sources of financing and invested in healthier, more complicated

investments.

Market sentiment and future bank profitability: Given a rebound in market- equity feelings

for larger companies in recent years, investors in equities have stayed cautious regarding certain

low- banks. A workgroup modelling review shows that more cost and institutional changes needs

to be carried out by certain organisations (Li, 2013).

5. Expected future performance

From the overall analysis it has been determined that in upcoming years the profitability

of Metro bank plc is going to be increase by good margin. The main reason for the same is

growing interest income and reducing operating expenses as well as ROA and ROE also increase

in last couple of years. Moreover, asset manager of Metro bank plc implement special

Administration Regulations 2011 put off a bankruptcy system that pertains to financial

institutions.

CONCLUSION

In the end of report, it is stated that modern banking in a far better way of doing banking

at fingers tips which reduces the burden of customer as more importantly increase the customer

base for banks. Different ratios are effective to define the overall performance of business during

a year and balance sheet and income statement define the actual financial condition of company

during a year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.