ACCT20075: Detailed Audit Report on Magellan Financial Group (MFG)

VerifiedAdded on 2023/01/16

|12

|2850

|72

Report

AI Summary

This report presents an in-depth analysis of the audit of Magellan Financial Group (MFG). It begins with an introduction to audit concepts, particularly materiality, and its significance in financial statements. The report then examines MFG's audit, including the company's operations, the role of Ernst & Young, and the quantitative estimation of materiality. It delves into specific areas such as investment valuation, business combinations, and financial ratios, providing a detailed assessment of the company's financial stability and performance. The cash flow statement is also examined, along with non-cash financial activities and the assessment of going concern risk. Finally, the report considers the opinions expressed by the auditors, offering a comprehensive overview of the audit process and its key findings.

Running head: Report on the Audit of MFG

Report on the Audit of MFG

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Report on the Audit of MFG

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1REPORT ON THE AUDIT OF MFG

Table of Contents

Introduction:...............................................................................................................................2

Assertions relating to MFG:.......................................................................................................3

The company Magellan Financial Group Audit analysis:..........................................................3

The Quantitative estimate of materiality:...................................................................................4

Investment existence and valuation:..........................................................................................4

Section 2:....................................................................................................................................5

Section 3:....................................................................................................................................6

Non-cash financial and investing activities:..............................................................................7

Going concern Risk:...................................................................................................................8

Opinions expressed by the auditors:..........................................................................................9

References:...............................................................................................................................10

Table of Contents

Introduction:...............................................................................................................................2

Assertions relating to MFG:.......................................................................................................3

The company Magellan Financial Group Audit analysis:..........................................................3

The Quantitative estimate of materiality:...................................................................................4

Investment existence and valuation:..........................................................................................4

Section 2:....................................................................................................................................5

Section 3:....................................................................................................................................6

Non-cash financial and investing activities:..............................................................................7

Going concern Risk:...................................................................................................................8

Opinions expressed by the auditors:..........................................................................................9

References:...............................................................................................................................10

2REPORT ON THE AUDIT OF MFG

Introduction:

The material is a concept of Audit term it determines the level of misstatement of

information in a company’s financial statements. This happens when the information to be

represented in the financial statement is altered, omitted or misstated. If the users have not

altered the action, then the omission or misstatement is immaterial. Materiality hence is

related to significance of transactions, balances and errors contained in the financial

statement. I7t is a threshold after which the financial information becomes relevant to the

decision making for the users. The information present in the financial statement should be

complete in all respect of material in order to be true and fair. It is stated the level of

materiality is judgmental if the amount is above or between 5% and 10% is material.

For example: If an amount of 2 million dollar is defaulted and not stated in the

financial statement then it is material to the financial statement and leads to incorrect decision

making.

Nature of materiality:

The company may plan to curtail the operations in business segments which can be a

major source of revenue for the company. This information is very important for the

stakeholders. The information should be mentioned in the financial statement as it may be of

the material nature. It will help to understand the scope of operation in future. The nature of

materiality can be discussed as follows (DeAngelo, 1991):

Relevance: Information of materiality that will influence the economic decision making of

the users and is relevant to the need.

Reliability: Omission or misstatement of an important information can impair user’s

ability to in correct decision making. This may affect the reliable information.

Introduction:

The material is a concept of Audit term it determines the level of misstatement of

information in a company’s financial statements. This happens when the information to be

represented in the financial statement is altered, omitted or misstated. If the users have not

altered the action, then the omission or misstatement is immaterial. Materiality hence is

related to significance of transactions, balances and errors contained in the financial

statement. I7t is a threshold after which the financial information becomes relevant to the

decision making for the users. The information present in the financial statement should be

complete in all respect of material in order to be true and fair. It is stated the level of

materiality is judgmental if the amount is above or between 5% and 10% is material.

For example: If an amount of 2 million dollar is defaulted and not stated in the

financial statement then it is material to the financial statement and leads to incorrect decision

making.

Nature of materiality:

The company may plan to curtail the operations in business segments which can be a

major source of revenue for the company. This information is very important for the

stakeholders. The information should be mentioned in the financial statement as it may be of

the material nature. It will help to understand the scope of operation in future. The nature of

materiality can be discussed as follows (DeAngelo, 1991):

Relevance: Information of materiality that will influence the economic decision making of

the users and is relevant to the need.

Reliability: Omission or misstatement of an important information can impair user’s

ability to in correct decision making. This may affect the reliable information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3REPORT ON THE AUDIT OF MFG

Completeness: Information that is contained in the financial statement should be complete

in all material respect in order to be fair and true view of the affair of the company.

Different bases and consideration employed:

Inherent uncertainty about appropriateness of evidence.

Uncertainty about the effectiveness of a client’s internal controls.

Uncertainty as to whether the financial statements are fairly stated when the audit is

completed.

Assertions relating to MFG:

It is claims that the management represents regarding the preparation of the financial

statement. The assertions can be regarding the class of the transactions or Assertions

relating to assets, liabilities and equity balances at the period end or Assertions relating to

presentation and disclosures (Fukukawa & Mock, 2011).

The company Magellan Financial Group Audit analysis:

Magellan financial group of company is based in Sydney and it provides the service to

high net worth, retail and institutional investors. It offers high value market leading

strategies to its clients. The company started its operations from 2006 to engage clients

who can be given high returns while properly protecting their capital. The company is

managing the $79 billion in global equity and infrastructure strategies. The external audit

partner for Magellan is Ernst & Young. The Audit is prepared at the year end and notes

comprising a summary of significant accounting policies and other explanatories are

provided in the audit statement. The company is preparing the audit report based on

Corporations Act 2001. The ethical requirements of the accounting professionals and

Completeness: Information that is contained in the financial statement should be complete

in all material respect in order to be fair and true view of the affair of the company.

Different bases and consideration employed:

Inherent uncertainty about appropriateness of evidence.

Uncertainty about the effectiveness of a client’s internal controls.

Uncertainty as to whether the financial statements are fairly stated when the audit is

completed.

Assertions relating to MFG:

It is claims that the management represents regarding the preparation of the financial

statement. The assertions can be regarding the class of the transactions or Assertions

relating to assets, liabilities and equity balances at the period end or Assertions relating to

presentation and disclosures (Fukukawa & Mock, 2011).

The company Magellan Financial Group Audit analysis:

Magellan financial group of company is based in Sydney and it provides the service to

high net worth, retail and institutional investors. It offers high value market leading

strategies to its clients. The company started its operations from 2006 to engage clients

who can be given high returns while properly protecting their capital. The company is

managing the $79 billion in global equity and infrastructure strategies. The external audit

partner for Magellan is Ernst & Young. The Audit is prepared at the year end and notes

comprising a summary of significant accounting policies and other explanatories are

provided in the audit statement. The company is preparing the audit report based on

Corporations Act 2001. The ethical requirements of the accounting professionals and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4REPORT ON THE AUDIT OF MFG

Ethical Standards Board’s APES110 audit are conducted in accordance with Australian

Auditing Standards.

The Quantitative estimate of materiality:

The group revenue is earned by the management. Performance fees are earned by the

Magellan Asset Management Limited (MAM) which is a consolidated subsidiary,

although the investment management agreement is in place with the third party. For the

year ended 30 June, 2017 the management fee was $300,529,000 and performance fees

were $21,696,000 which equates to 88.8% and 6.4% of total revenue respectively. This

recognition criteria is in accordance with Australian Accounting Standard - AASB 118:

Revenue (AASB 118) (Schwartz, 2016). The company recognized the note from Note 6

which states the details of the revenue earned. The management fee earned and calculated

in accordance with the Investment Management Agreements, mandates and Constitutions

of the funds as set out in (Note 6).

Investment existence and valuation:

The audit was done to understand the effectiveness of the controls used by the

company. This was done to realize the sale and profit on the listed, unlisted equity and

own managed funds. The value of the financial assets, as per Note 12 of the financial

report was $274,567,000 that is 40.7% of the total assets. The importance of the financial

matter was important for the audit. The materiality was adequate to be analyzed. The

disclosure according to note 12 was correct and fair (Klein, 2002).

Business combination:

On March 1, 2018 the Company acquired 100% of the shares of Airlie Funds

Management Pty Limited for $97,112,915. The second acquisition was for Frontier

Ethical Standards Board’s APES110 audit are conducted in accordance with Australian

Auditing Standards.

The Quantitative estimate of materiality:

The group revenue is earned by the management. Performance fees are earned by the

Magellan Asset Management Limited (MAM) which is a consolidated subsidiary,

although the investment management agreement is in place with the third party. For the

year ended 30 June, 2017 the management fee was $300,529,000 and performance fees

were $21,696,000 which equates to 88.8% and 6.4% of total revenue respectively. This

recognition criteria is in accordance with Australian Accounting Standard - AASB 118:

Revenue (AASB 118) (Schwartz, 2016). The company recognized the note from Note 6

which states the details of the revenue earned. The management fee earned and calculated

in accordance with the Investment Management Agreements, mandates and Constitutions

of the funds as set out in (Note 6).

Investment existence and valuation:

The audit was done to understand the effectiveness of the controls used by the

company. This was done to realize the sale and profit on the listed, unlisted equity and

own managed funds. The value of the financial assets, as per Note 12 of the financial

report was $274,567,000 that is 40.7% of the total assets. The importance of the financial

matter was important for the audit. The materiality was adequate to be analyzed. The

disclosure according to note 12 was correct and fair (Klein, 2002).

Business combination:

On March 1, 2018 the Company acquired 100% of the shares of Airlie Funds

Management Pty Limited for $97,112,915. The second acquisition was for Frontier

5REPORT ON THE AUDIT OF MFG

Partners Inc on 5 February 2018 and Frontegra Strategies LLC on 2 April 2018 for total

cash of $14,623,000. The testing for the valuation model followed was found fair and true

and followed as per the standards and disclosure in Note 18. The tangible and intangible

asset was as per the Australian accounting standards, the acquisition was found to be an

important material to the group (Hao & Liu, 2017).

These are the transactions of quantitative aspects that could have affected the decision

making of the stakeholders if it went unnoticed, and unaccounted. The amount involved

had material importance. As per the audit Report, the Company was found to be using the

true and fair methods to realize it.

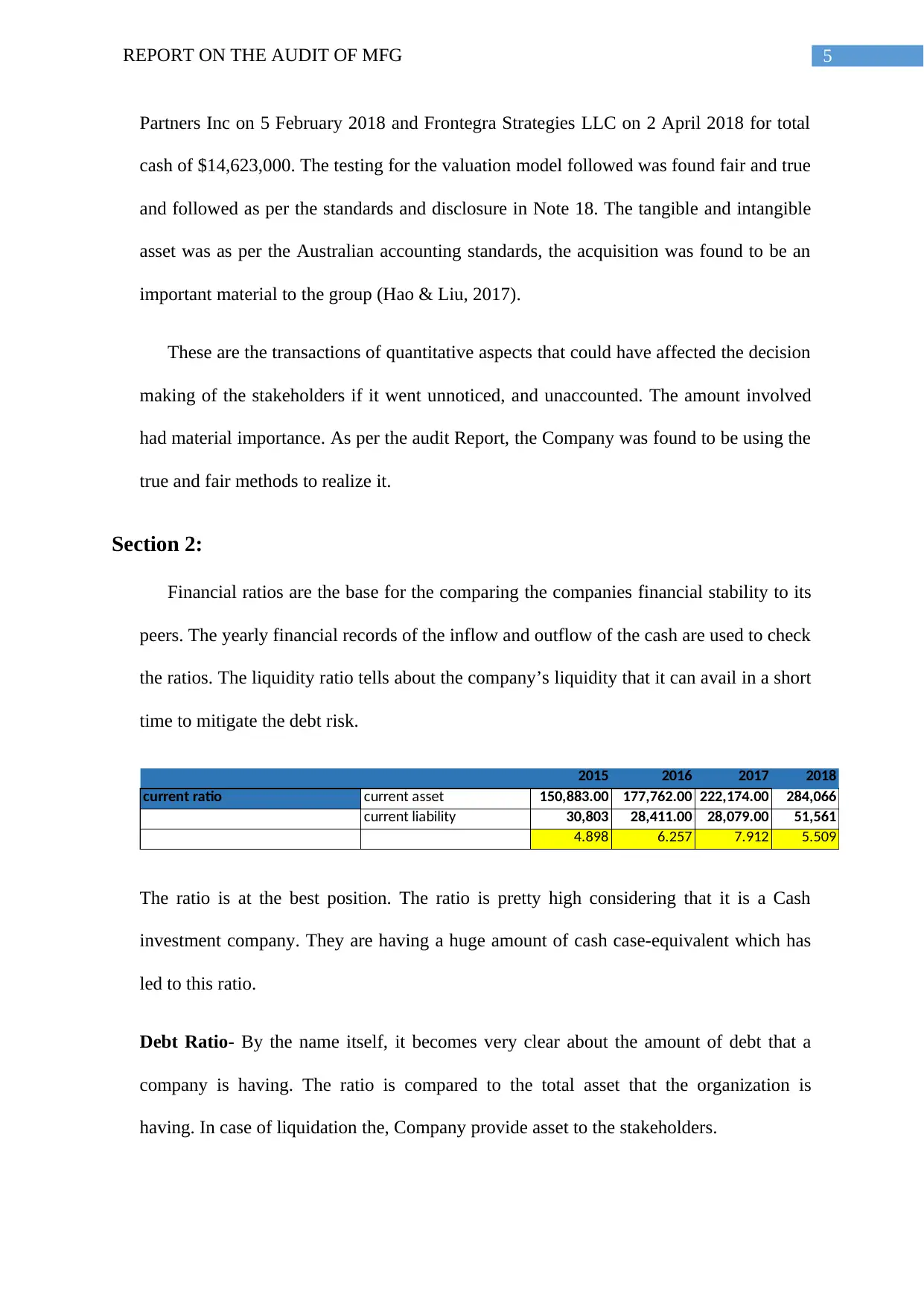

Section 2:

Financial ratios are the base for the comparing the companies financial stability to its

peers. The yearly financial records of the inflow and outflow of the cash are used to check

the ratios. The liquidity ratio tells about the company’s liquidity that it can avail in a short

time to mitigate the debt risk.

2015 2016 2017 2018

current ratio current asset 150,883.00 177,762.00 222,174.00 284,066

current liability 30,803 28,411.00 28,079.00 51,561

4.898 6.257 7.912 5.509

The ratio is at the best position. The ratio is pretty high considering that it is a Cash

investment company. They are having a huge amount of cash case-equivalent which has

led to this ratio.

Debt Ratio- By the name itself, it becomes very clear about the amount of debt that a

company is having. The ratio is compared to the total asset that the organization is

having. In case of liquidation the, Company provide asset to the stakeholders.

Partners Inc on 5 February 2018 and Frontegra Strategies LLC on 2 April 2018 for total

cash of $14,623,000. The testing for the valuation model followed was found fair and true

and followed as per the standards and disclosure in Note 18. The tangible and intangible

asset was as per the Australian accounting standards, the acquisition was found to be an

important material to the group (Hao & Liu, 2017).

These are the transactions of quantitative aspects that could have affected the decision

making of the stakeholders if it went unnoticed, and unaccounted. The amount involved

had material importance. As per the audit Report, the Company was found to be using the

true and fair methods to realize it.

Section 2:

Financial ratios are the base for the comparing the companies financial stability to its

peers. The yearly financial records of the inflow and outflow of the cash are used to check

the ratios. The liquidity ratio tells about the company’s liquidity that it can avail in a short

time to mitigate the debt risk.

2015 2016 2017 2018

current ratio current asset 150,883.00 177,762.00 222,174.00 284,066

current liability 30,803 28,411.00 28,079.00 51,561

4.898 6.257 7.912 5.509

The ratio is at the best position. The ratio is pretty high considering that it is a Cash

investment company. They are having a huge amount of cash case-equivalent which has

led to this ratio.

Debt Ratio- By the name itself, it becomes very clear about the amount of debt that a

company is having. The ratio is compared to the total asset that the organization is

having. In case of liquidation the, Company provide asset to the stakeholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6REPORT ON THE AUDIT OF MFG

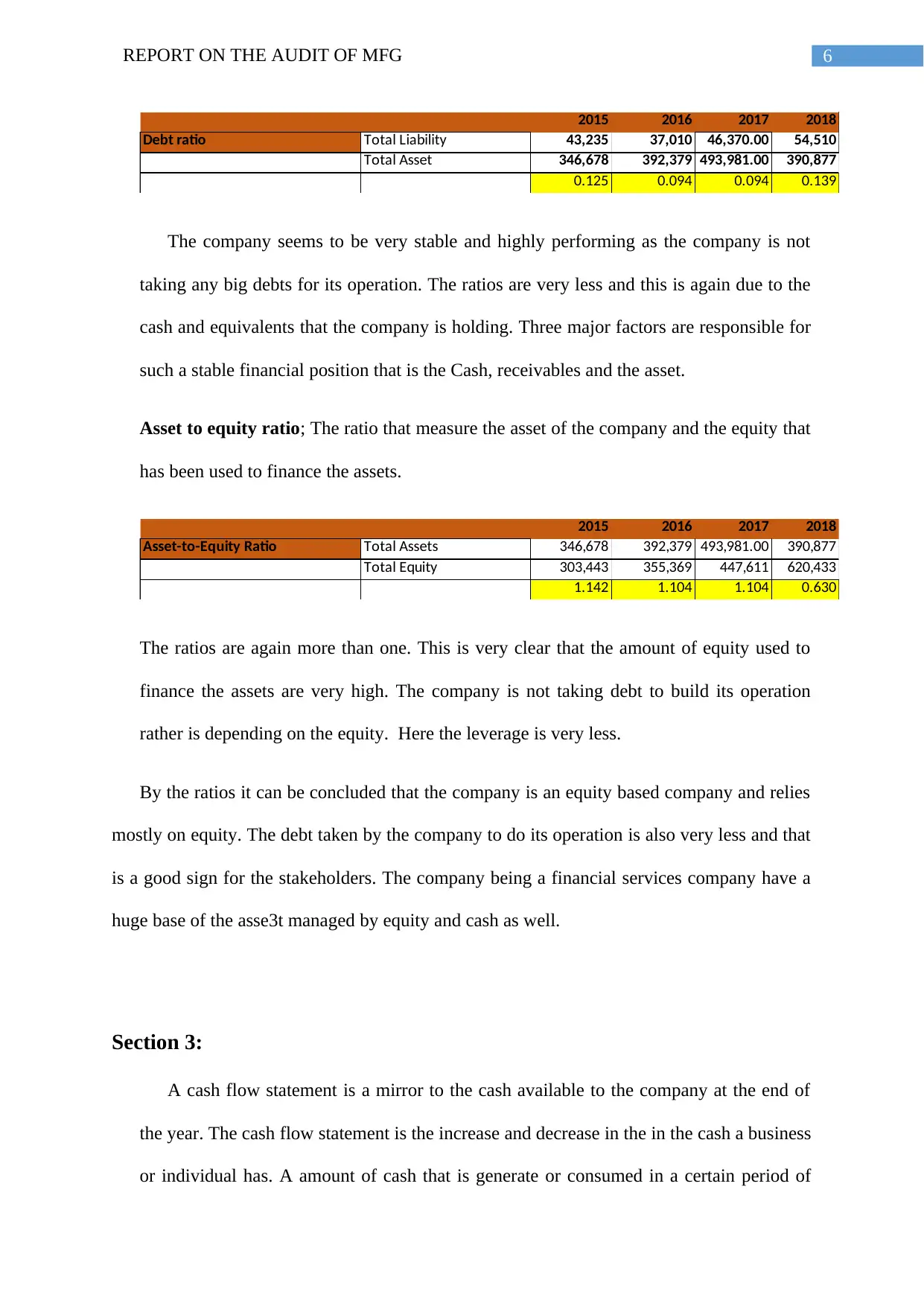

2015 2016 2017 2018

Debt ratio Total Liability 43,235 37,010 46,370.00 54,510

Total Asset 346,678 392,379 493,981.00 390,877

0.125 0.094 0.094 0.139

The company seems to be very stable and highly performing as the company is not

taking any big debts for its operation. The ratios are very less and this is again due to the

cash and equivalents that the company is holding. Three major factors are responsible for

such a stable financial position that is the Cash, receivables and the asset.

Asset to equity ratio; The ratio that measure the asset of the company and the equity that

has been used to finance the assets.

2015 2016 2017 2018

Asset-to-Equity Ratio Total Assets 346,678 392,379 493,981.00 390,877

Total Equity 303,443 355,369 447,611 620,433

1.142 1.104 1.104 0.630

The ratios are again more than one. This is very clear that the amount of equity used to

finance the assets are very high. The company is not taking debt to build its operation

rather is depending on the equity. Here the leverage is very less.

By the ratios it can be concluded that the company is an equity based company and relies

mostly on equity. The debt taken by the company to do its operation is also very less and that

is a good sign for the stakeholders. The company being a financial services company have a

huge base of the asse3t managed by equity and cash as well.

Section 3:

A cash flow statement is a mirror to the cash available to the company at the end of

the year. The cash flow statement is the increase and decrease in the in the cash a business

or individual has. A amount of cash that is generate or consumed in a certain period of

2015 2016 2017 2018

Debt ratio Total Liability 43,235 37,010 46,370.00 54,510

Total Asset 346,678 392,379 493,981.00 390,877

0.125 0.094 0.094 0.139

The company seems to be very stable and highly performing as the company is not

taking any big debts for its operation. The ratios are very less and this is again due to the

cash and equivalents that the company is holding. Three major factors are responsible for

such a stable financial position that is the Cash, receivables and the asset.

Asset to equity ratio; The ratio that measure the asset of the company and the equity that

has been used to finance the assets.

2015 2016 2017 2018

Asset-to-Equity Ratio Total Assets 346,678 392,379 493,981.00 390,877

Total Equity 303,443 355,369 447,611 620,433

1.142 1.104 1.104 0.630

The ratios are again more than one. This is very clear that the amount of equity used to

finance the assets are very high. The company is not taking debt to build its operation

rather is depending on the equity. Here the leverage is very less.

By the ratios it can be concluded that the company is an equity based company and relies

mostly on equity. The debt taken by the company to do its operation is also very less and that

is a good sign for the stakeholders. The company being a financial services company have a

huge base of the asse3t managed by equity and cash as well.

Section 3:

A cash flow statement is a mirror to the cash available to the company at the end of

the year. The cash flow statement is the increase and decrease in the in the cash a business

or individual has. A amount of cash that is generate or consumed in a certain period of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7REPORT ON THE AUDIT OF MFG

time. There are three major heads under the cash flow statement determining the cash

coming in or leaving the organization due to which activities. There are many types of

cash flow like Cash from Operating activities are the cash that is generated by companies

core business. Cash from flow of equity determine the cash available from the

reinvestment into the business and cash from to the company. It is the free cash that is

used in financial modeling and leveraging.

The cash flow statement for year 2018 has number of cash inflow and outflow. The

highest cash inflow and outflows are from the cash from Operating Activities. The major

cash receipts for the year are from Management and services fees received for the amount

of 399,854 dollars. This has a material impact and has been audited by the auditor to

check the procedures followed by the company as per the Australian accounting

standards. The major payment in the in the financing activities and operating activities

categories. Dividends paid for amount (156,948) dollars in the financing outflow of cash

and Payments to suppliers and employees (inclusive of Goods and Service Tax) for the

amount of GST (128,478) dollars.

Non-cash financial and investing activities:

Statement of cash flow from the operating, investing and financing activities affect

the cash and cash equivalents. There is segment of the non cash financial activities. These

activities are very important as it has huge impact on the current and future performance

in terms of revenue, profits and also the positive cash flow. That why it is very important

to disclose the non cash financial activities to the audit report and the annual report. Some

of the example of non-cash activities are:

Issuance of the stock retire a debt.

Purchase of an asset by issuing stock, bonds or a note payable.

time. There are three major heads under the cash flow statement determining the cash

coming in or leaving the organization due to which activities. There are many types of

cash flow like Cash from Operating activities are the cash that is generated by companies

core business. Cash from flow of equity determine the cash available from the

reinvestment into the business and cash from to the company. It is the free cash that is

used in financial modeling and leveraging.

The cash flow statement for year 2018 has number of cash inflow and outflow. The

highest cash inflow and outflows are from the cash from Operating Activities. The major

cash receipts for the year are from Management and services fees received for the amount

of 399,854 dollars. This has a material impact and has been audited by the auditor to

check the procedures followed by the company as per the Australian accounting

standards. The major payment in the in the financing activities and operating activities

categories. Dividends paid for amount (156,948) dollars in the financing outflow of cash

and Payments to suppliers and employees (inclusive of Goods and Service Tax) for the

amount of GST (128,478) dollars.

Non-cash financial and investing activities:

Statement of cash flow from the operating, investing and financing activities affect

the cash and cash equivalents. There is segment of the non cash financial activities. These

activities are very important as it has huge impact on the current and future performance

in terms of revenue, profits and also the positive cash flow. That why it is very important

to disclose the non cash financial activities to the audit report and the annual report. Some

of the example of non-cash activities are:

Issuance of the stock retire a debt.

Purchase of an asset by issuing stock, bonds or a note payable.

8REPORT ON THE AUDIT OF MFG

Exchange of non-cash assets.

Conversion of debt to common stock.

Conversion of preferred to common stocks.

The financial statement of MFG states that the major non cash financing activities are - issue

of MFG shares for the acquisition of Airlie Funds Management Pty Limited, which is around

97,113$ and according to note 18 (A) and issue of issue of MFG shares under the SPP of

around 5,439$. These amounts have been in the form of current or non-current financing

activities. The disclosure is very essential for the Board to the stake holder as this affects the

decision making of the stakeholders.

Going concern Risk:

It is the principle that the entity will remain in a business for a long period. It means

that the entity will not halt its operations and liquidate its assets. This is also the method of

the company to make enough money to be kept running. The MFG is a stable company. The

funds to run the company is 170,333$ from the operating activities. The debt that the

company is owning now is less. The cash and cash equivalent are excess in amount as

compared to the liabilities of the company (Whittington & Margheim, 2003).

Risk : Financial risk is a state when the company is liquidating or not able to generate

enough cash. This can be mitigated if the audit is done and material miss-statement is

recognized at early stage. The auditors work is to achieve the low level of audit risk. This can

be done by mitigating the inherent risk which is a risk of material miss-statement in the

financial statement. This risk arises due to the error or omission due to lapse of control and

leading to material miss-statement. Control risk is a arising due to failure in the relevant

controls of entity. Detection risk is risk when auditor fails to detect a material miss-statement

in the financials report (Mock & Wright, 1999).

Exchange of non-cash assets.

Conversion of debt to common stock.

Conversion of preferred to common stocks.

The financial statement of MFG states that the major non cash financing activities are - issue

of MFG shares for the acquisition of Airlie Funds Management Pty Limited, which is around

97,113$ and according to note 18 (A) and issue of issue of MFG shares under the SPP of

around 5,439$. These amounts have been in the form of current or non-current financing

activities. The disclosure is very essential for the Board to the stake holder as this affects the

decision making of the stakeholders.

Going concern Risk:

It is the principle that the entity will remain in a business for a long period. It means

that the entity will not halt its operations and liquidate its assets. This is also the method of

the company to make enough money to be kept running. The MFG is a stable company. The

funds to run the company is 170,333$ from the operating activities. The debt that the

company is owning now is less. The cash and cash equivalent are excess in amount as

compared to the liabilities of the company (Whittington & Margheim, 2003).

Risk : Financial risk is a state when the company is liquidating or not able to generate

enough cash. This can be mitigated if the audit is done and material miss-statement is

recognized at early stage. The auditors work is to achieve the low level of audit risk. This can

be done by mitigating the inherent risk which is a risk of material miss-statement in the

financial statement. This risk arises due to the error or omission due to lapse of control and

leading to material miss-statement. Control risk is a arising due to failure in the relevant

controls of entity. Detection risk is risk when auditor fails to detect a material miss-statement

in the financials report (Mock & Wright, 1999).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9REPORT ON THE AUDIT OF MFG

If the Companies fund is analyzed we can find that the company is earning good amount of

revenue as the out of expense is less in comparison. Thus, there is no such risks at present and

the company will be continuing its operation smoothly.

Opinions expressed by the auditors:

In the opinion of the auditor the financial report of the Group was in accordance with

the Corporations Act 2001, including:

(i)The financial report was giving the true and fair value of the consolidated financial position

of the Group as of 30Th June, 2018.

(ii) The company is complying with Australian Accounting Standards and the Corporations

Regulations 2001.

(iii)The Remuneration Report of Magellan Financial Group 30June 2018, complies with

section 300A of the Corporations Act 2001.

If the Companies fund is analyzed we can find that the company is earning good amount of

revenue as the out of expense is less in comparison. Thus, there is no such risks at present and

the company will be continuing its operation smoothly.

Opinions expressed by the auditors:

In the opinion of the auditor the financial report of the Group was in accordance with

the Corporations Act 2001, including:

(i)The financial report was giving the true and fair value of the consolidated financial position

of the Group as of 30Th June, 2018.

(ii) The company is complying with Australian Accounting Standards and the Corporations

Regulations 2001.

(iii)The Remuneration Report of Magellan Financial Group 30June 2018, complies with

section 300A of the Corporations Act 2001.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10REPORT ON THE AUDIT OF MFG

References:

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate

bankruptcy. The journal of finance, 23(4), 589-609.

Becker, C. L., DeFond, M. L., Jiambalvo, J., & Subramanyam, K. R. (1998). The effect of

audit quality on earnings management. Contemporary accounting research, 15(1), 1-

24.

DeAngelo, L. E. (1991). Auditor size and audit quality. Journal of accounting and

economics, 3(3), 183-199.

Fukukawa, H., & Mock, T. J. (2011). Audit risk assessments using belief versus probability.

Auditing: A Journal of Practice & Theory, 30(1), 75-99.

Hao, J., & Liu, Q. (2017). The Impact of Australian Accounting Education on Repatriates'

Career Development. Australian Accounting Review, 27(1), 52-60.

Klein, A. (2002). Audit committee, board of director characteristics, and earnings

management. Journal of accounting and economics, 33(3), 375-400.

Mock, T. J., & Wright, A. M. (1999). Are audit program plans risk-adjusted?. Auditing: A

Journal of Practice & Theory, 18(1), 55-74.

Schwartz, J. (2016). Should Mutual Funds Invest in Startups: A Case Study of Fidelity

Magellan Fund's Investments in Unicorns (and Other Startups) and the Regulatory

Implications. NCL Rev., 95, 1341.

Whittington, R., & Margheim, L. (2003). The effects of risk, materiality, and assertion

subjectivity on external auditors' reliance on internal auditors. Auditing, 12(1), 50.

References:

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate

bankruptcy. The journal of finance, 23(4), 589-609.

Becker, C. L., DeFond, M. L., Jiambalvo, J., & Subramanyam, K. R. (1998). The effect of

audit quality on earnings management. Contemporary accounting research, 15(1), 1-

24.

DeAngelo, L. E. (1991). Auditor size and audit quality. Journal of accounting and

economics, 3(3), 183-199.

Fukukawa, H., & Mock, T. J. (2011). Audit risk assessments using belief versus probability.

Auditing: A Journal of Practice & Theory, 30(1), 75-99.

Hao, J., & Liu, Q. (2017). The Impact of Australian Accounting Education on Repatriates'

Career Development. Australian Accounting Review, 27(1), 52-60.

Klein, A. (2002). Audit committee, board of director characteristics, and earnings

management. Journal of accounting and economics, 33(3), 375-400.

Mock, T. J., & Wright, A. M. (1999). Are audit program plans risk-adjusted?. Auditing: A

Journal of Practice & Theory, 18(1), 55-74.

Schwartz, J. (2016). Should Mutual Funds Invest in Startups: A Case Study of Fidelity

Magellan Fund's Investments in Unicorns (and Other Startups) and the Regulatory

Implications. NCL Rev., 95, 1341.

Whittington, R., & Margheim, L. (2003). The effects of risk, materiality, and assertion

subjectivity on external auditors' reliance on internal auditors. Auditing, 12(1), 50.

11REPORT ON THE AUDIT OF MFG

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.