Spring 2019 MGMT1600: Managerial Accounting Project Report Analysis

VerifiedAdded on 2022/12/27

|22

|5649

|1

Report

AI Summary

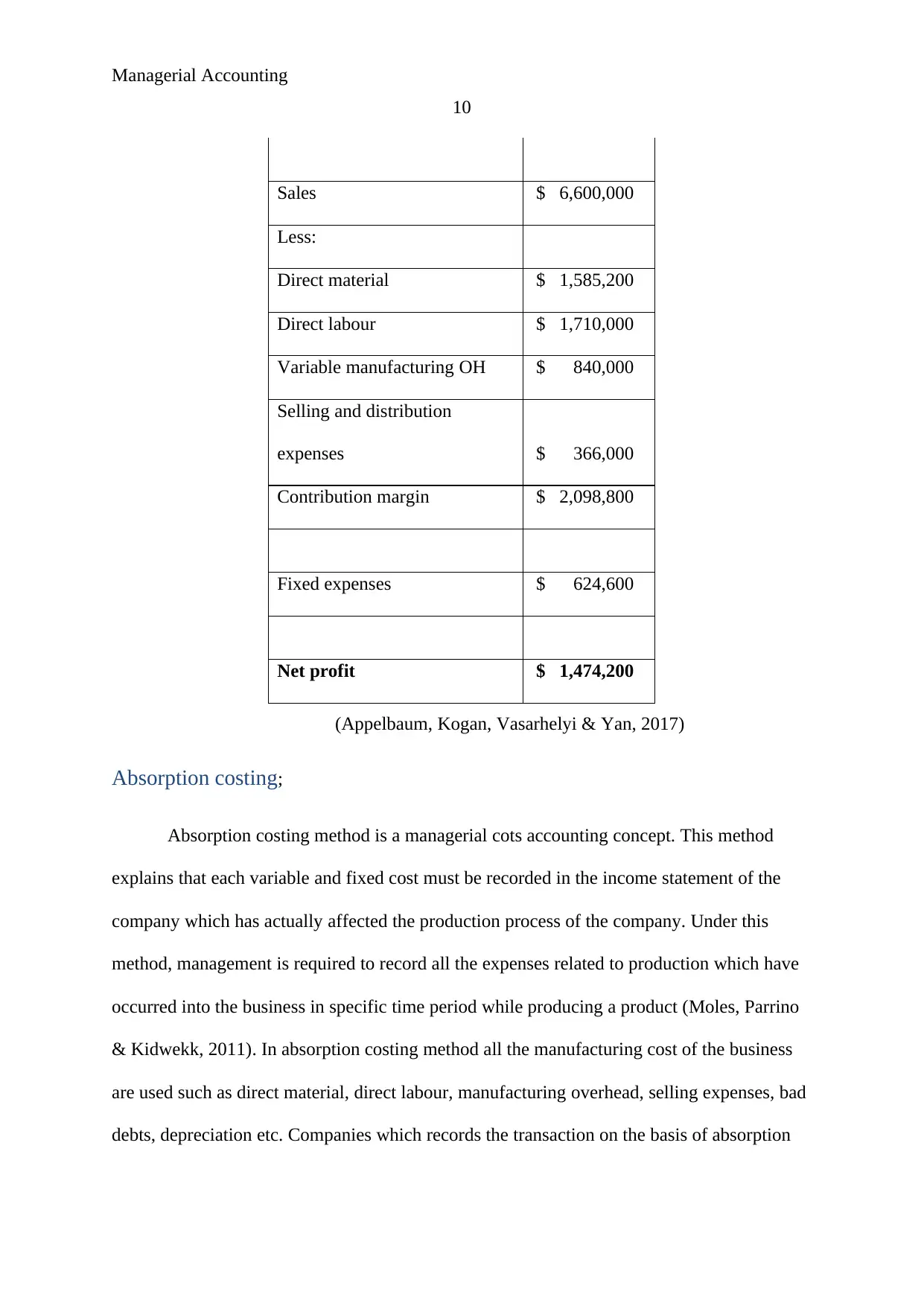

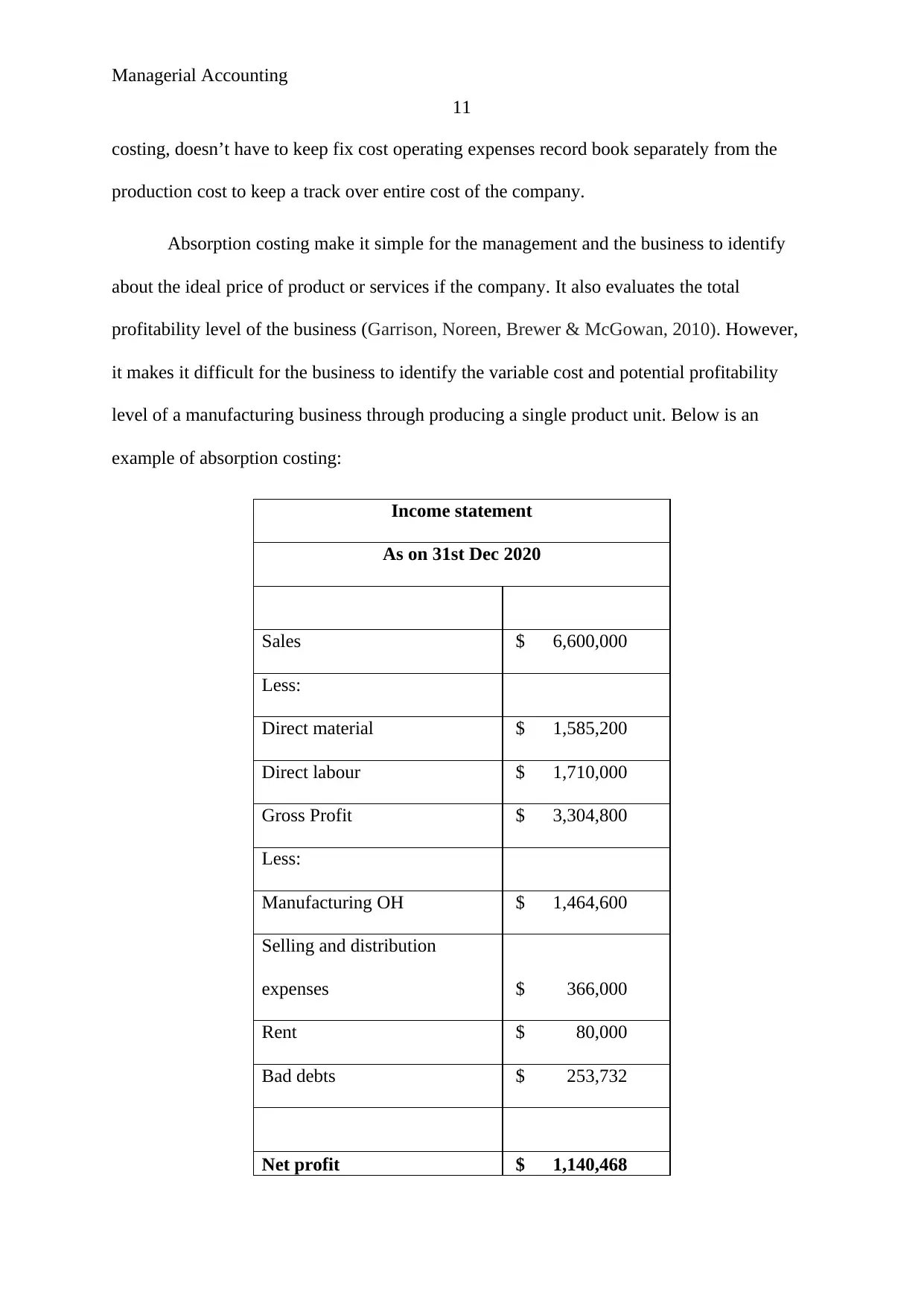

This report delves into the core concepts of managerial accounting, presenting a comprehensive analysis of various methods and their applications. It begins with an introduction to managerial accounting, emphasizing its significance in organizational performance and decision-making. The report then explores key accounting techniques, including ratio analysis, which assesses financial performance through liquidity, profitability, and solvency ratios. Budgetary control is examined, highlighting its role in setting financial goals and monitoring operational efficiency. Variance analysis is discussed, demonstrating how to evaluate the differences between budgeted and actual outcomes. Furthermore, the report covers variable and absorption costing methods, comparing their approaches to cost allocation and their impact on financial statements. The report includes detailed examples, formulas, and calculations to illustrate each concept, providing a practical understanding of how these methods can be applied in a professional setting. The report is divided into two parts, with the second part including detailed financial schedules, and concludes by summarizing the importance of managerial accounting in guiding strategic decisions and improving overall business outcomes.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.