MGT723 Research: Agency Theory and Carbon Disclosure in Australia

VerifiedAdded on 2023/06/11

|21

|4743

|325

Report

AI Summary

This report investigates the relationship between agency theory and carbon disclosure practices within Australian companies. It explores how corporate governance and leadership attributes influence a company's environmental responsibility and transparency in carbon emissions reporting. The research uses quantitative analysis of data collected from the Carbon Disclosure Project (CDP) survey, focusing on carbon disclosure scores, carbon emission scopes, and organizational initiatives. The findings suggest a strong awareness among Australian companies regarding sustainability and environmental concerns, with a significant majority actively engaging in initiatives to reduce carbon emissions. The report includes descriptive and inferential statistical analysis to test hypotheses related to the impact of organizational initiatives on voluntary disclosure scores, providing insights into the practical and theoretical implications for corporate environmental responsibility. The document also discusses the limitations of the study and suggests avenues for further research, emphasizing the importance of corporate accountability and sustainable practices.

Running Head: AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN

COMPANIES

Agency Theory and Carbon Disclosure in Australian Companies

Name of the Student

Name of the University

Author Note

COMPANIES

Agency Theory and Carbon Disclosure in Australian Companies

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

Acknowledgement

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand

that the source of ideas must be referenced and that quotation marks and a reference are required

when directly quoting anyone else’s words.

Acknowledgement

I certify that I have carefully reviewed the university’s academic misconduct policy. I understand

that the source of ideas must be referenced and that quotation marks and a reference are required

when directly quoting anyone else’s words.

2AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

Table of Contents

Introduction......................................................................................................................................3

Literature Review............................................................................................................................3

Practical Motivation.....................................................................................................................5

Theoretical Motivation................................................................................................................5

Conceptual Model............................................................................................................................6

Hypothesis.......................................................................................................................................6

Data Collection............................................................................................................................7

Data Analysis – Descriptive............................................................................................................7

Data Analysis – Inferential............................................................................................................13

Hypothesis Testing........................................................................................................................14

Discussion......................................................................................................................................17

Limitations and Further Research..................................................................................................18

References......................................................................................................................................20

Table of Contents

Introduction......................................................................................................................................3

Literature Review............................................................................................................................3

Practical Motivation.....................................................................................................................5

Theoretical Motivation................................................................................................................5

Conceptual Model............................................................................................................................6

Hypothesis.......................................................................................................................................6

Data Collection............................................................................................................................7

Data Analysis – Descriptive............................................................................................................7

Data Analysis – Inferential............................................................................................................13

Hypothesis Testing........................................................................................................................14

Discussion......................................................................................................................................17

Limitations and Further Research..................................................................................................18

References......................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

Introduction

There have been extensive effects of the corporate companies on the environment. This

creates a global crisis. It is extremely important to deal with this crisis. The reason why this

global crisis has occurred is due to the harmful gases that are emitted from the manufacturing

companies (Buniamin et al. 2010). The businesses of the companies are controlled and directed

by the corporate governance and their activities. The companies are provided with a lot of

restrictions and measurements by the corporate governance so that the emission of harmful gases

especially carbon dioxide is minimized. The businesses are also forced to take part in various

environmental activities such as tree plantation (Ioannou and Serafeim 2017).

The main aim of this research will be to emphasize the effects of the companies on the

environment. Thus, the main focus of this research will be towards the influence of the

leadership attributes of the companies on carbon disclosure. A new concept has been introduced

so that the actions can be taken for managing the opportunities and the risks that can be faced by

the company in the future years. Quantitative analysis will be performed to understand the effect

(Saka & Oshika 2014). The data has been collected for this research with the help of a survey.

Statistical analysis tool SPSS version 20 has been used for the analysis of the data. The dataset

contained information about almost 5000 industries but for all the industries, information was not

available completely. 306 industries have been found having valid information which will be

used for the study.

Literature Review

Australia is nowadays facing serious challenges with the rapid advancements of

technology. This has resulted in economic growth and development of the country. There has

Introduction

There have been extensive effects of the corporate companies on the environment. This

creates a global crisis. It is extremely important to deal with this crisis. The reason why this

global crisis has occurred is due to the harmful gases that are emitted from the manufacturing

companies (Buniamin et al. 2010). The businesses of the companies are controlled and directed

by the corporate governance and their activities. The companies are provided with a lot of

restrictions and measurements by the corporate governance so that the emission of harmful gases

especially carbon dioxide is minimized. The businesses are also forced to take part in various

environmental activities such as tree plantation (Ioannou and Serafeim 2017).

The main aim of this research will be to emphasize the effects of the companies on the

environment. Thus, the main focus of this research will be towards the influence of the

leadership attributes of the companies on carbon disclosure. A new concept has been introduced

so that the actions can be taken for managing the opportunities and the risks that can be faced by

the company in the future years. Quantitative analysis will be performed to understand the effect

(Saka & Oshika 2014). The data has been collected for this research with the help of a survey.

Statistical analysis tool SPSS version 20 has been used for the analysis of the data. The dataset

contained information about almost 5000 industries but for all the industries, information was not

available completely. 306 industries have been found having valid information which will be

used for the study.

Literature Review

Australia is nowadays facing serious challenges with the rapid advancements of

technology. This has resulted in economic growth and development of the country. There has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

been gradual growth of the Australian economy over the years. However, this growth in the

economy is challenged with the fall in the stock prices and the growth in the emission of the

harmful gases in the environment. These environmental issues include emission of solid waste,

air pollution, water pollution as well as water management. According to a research by Chang,

Yeh and Liu (2015), it has been known that the emission of these waste products will increase in

a considerable amount by the year 2020. This has created a challenge to achieve the sustainable

economy. As pointed out by Herold and Lee (2018), the environmental issues that are caused by

the industries are deforestation, dumping of wastes which are hazardous to the environment and

polluting the air and the water as well. Considering all these factors, the government has

considered taking various measures to keep the environment protected from any types of

pollution. Decomposition and trend analysis is usually constructed in order to understand the

relationship between the economic growth of the country and the environmental outcomes.

The corporate governance framework in place in Australia spreads beyond mere

submissions with regulatory requirements with main voluntary elements. More so, an extensive

number of provision throughout the federal and state legislation makes the corporate directors

accountable if the company fails to adhere to the multitude of requirements (Juliet 2015). There

are laws and guidelines that run a corporate which include the non-binding guidelines, soft law

and the hard law, together with the market and agency prospects, form a framework for corporate

governance (Trireksani, T. and Djajadikerta 2016). Satisfying the best practice of commercial

leadership and commentary on the environment are a manifestation to this tow, but

interconnected spheres of presentation. The concept that was introduced in a report in the 1966

tell companies and organization not only to be financially sound but also environmentally

account so as to ensure the rights future generation are taken into consideration. Taking of the

been gradual growth of the Australian economy over the years. However, this growth in the

economy is challenged with the fall in the stock prices and the growth in the emission of the

harmful gases in the environment. These environmental issues include emission of solid waste,

air pollution, water pollution as well as water management. According to a research by Chang,

Yeh and Liu (2015), it has been known that the emission of these waste products will increase in

a considerable amount by the year 2020. This has created a challenge to achieve the sustainable

economy. As pointed out by Herold and Lee (2018), the environmental issues that are caused by

the industries are deforestation, dumping of wastes which are hazardous to the environment and

polluting the air and the water as well. Considering all these factors, the government has

considered taking various measures to keep the environment protected from any types of

pollution. Decomposition and trend analysis is usually constructed in order to understand the

relationship between the economic growth of the country and the environmental outcomes.

The corporate governance framework in place in Australia spreads beyond mere

submissions with regulatory requirements with main voluntary elements. More so, an extensive

number of provision throughout the federal and state legislation makes the corporate directors

accountable if the company fails to adhere to the multitude of requirements (Juliet 2015). There

are laws and guidelines that run a corporate which include the non-binding guidelines, soft law

and the hard law, together with the market and agency prospects, form a framework for corporate

governance (Trireksani, T. and Djajadikerta 2016). Satisfying the best practice of commercial

leadership and commentary on the environment are a manifestation to this tow, but

interconnected spheres of presentation. The concept that was introduced in a report in the 1966

tell companies and organization not only to be financially sound but also environmentally

account so as to ensure the rights future generation are taken into consideration. Taking of the

5AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

right measurements to ensure the protection of the environment will reduce already caused

damage and therefore reduce the long-term effects to the next generation.

Practical Motivation

The most important crisis that is currently of major interest to the world as well as the

industries is the environmental pollution. This pollution supposedly affects the elements of

nature. Thus, the companies are forced to take part in activities to save the environment. It is

believed by several scientists that as environmental pollution increases with the emission of

harmful gases, people are getting more exposed towards environmental dangers. The carbon

release in the environment is increasing each day and this in turn increases the level of carbon

dioxide in the atmosphere. Thus, it is extremely important to reduce these emissions by the

companies. The companies have the potential to reduce the carbon emissions by their companies

by adopting necessary changes. The boards, stakeholders and the managers of the companies can

take the necessary decisions that will be helpful in controlling the amount of pollutant the

company releases in the atmosphere. Significant risks are brought to an organization as a result

of this emissions as well as to the investments of the shareholders. The organization is affected

either directly or indirectly by climatic changes indicated by natural calamities.

Theoretical Motivation

The motivation of the research stands to investigate whether good corporate leadership

practices are important in illustrating environmental responsibility of organizations in Australia.

The corporate governance framework in place in Australia spreads beyond mere submission s

with regulatory requirements with main voluntary elements. More so, an extensive number of

provision throughout the federal and state legislation makes the corporate directors accountable

right measurements to ensure the protection of the environment will reduce already caused

damage and therefore reduce the long-term effects to the next generation.

Practical Motivation

The most important crisis that is currently of major interest to the world as well as the

industries is the environmental pollution. This pollution supposedly affects the elements of

nature. Thus, the companies are forced to take part in activities to save the environment. It is

believed by several scientists that as environmental pollution increases with the emission of

harmful gases, people are getting more exposed towards environmental dangers. The carbon

release in the environment is increasing each day and this in turn increases the level of carbon

dioxide in the atmosphere. Thus, it is extremely important to reduce these emissions by the

companies. The companies have the potential to reduce the carbon emissions by their companies

by adopting necessary changes. The boards, stakeholders and the managers of the companies can

take the necessary decisions that will be helpful in controlling the amount of pollutant the

company releases in the atmosphere. Significant risks are brought to an organization as a result

of this emissions as well as to the investments of the shareholders. The organization is affected

either directly or indirectly by climatic changes indicated by natural calamities.

Theoretical Motivation

The motivation of the research stands to investigate whether good corporate leadership

practices are important in illustrating environmental responsibility of organizations in Australia.

The corporate governance framework in place in Australia spreads beyond mere submission s

with regulatory requirements with main voluntary elements. More so, an extensive number of

provision throughout the federal and state legislation makes the corporate directors accountable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

if the company fails to adhere to the multitude of requirements. Corporate sustainability is a main

concern that of the modern corporations to today, most environmental reporting is done

voluntarily, there has been an increase in the number of writers who have argued about the

effects of the corporate activities on the environment, and the feel that the companies should be

held accountable for their mistakes at a larger audience than just its stakeholders. The current

economic predicament has added a new phase of change which requires being instant rather than

that of a certain period. Increased competition, global competition, new technologies and fast-

changing environments call for a change in the management in organizations.

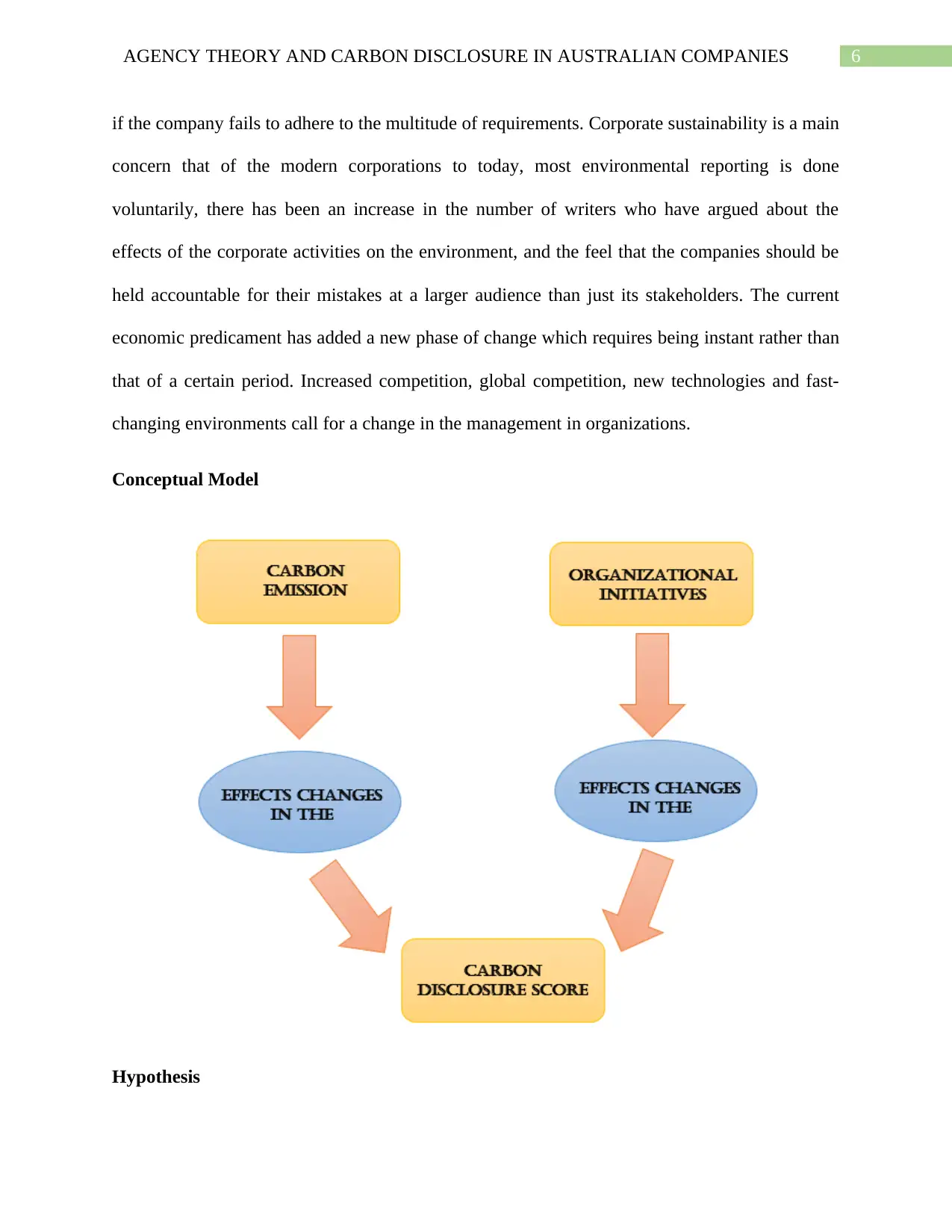

Conceptual Model

Hypothesis

if the company fails to adhere to the multitude of requirements. Corporate sustainability is a main

concern that of the modern corporations to today, most environmental reporting is done

voluntarily, there has been an increase in the number of writers who have argued about the

effects of the corporate activities on the environment, and the feel that the companies should be

held accountable for their mistakes at a larger audience than just its stakeholders. The current

economic predicament has added a new phase of change which requires being instant rather than

that of a certain period. Increased competition, global competition, new technologies and fast-

changing environments call for a change in the management in organizations.

Conceptual Model

Hypothesis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

Based on the literature review, the following hypothesis statements has been framed. The

Null Hypothesis and the Alternate Hypothesis that will be required in order to conduct the study

is described as follows:

Null Hypothesis (H0): There is no significant difference between the voluntary disclosure scores

on the basis of the organizational initiatives.

Alternate Hypothesis (HA): There are significant differences between the voluntary disclosure

scores on the basis of the organizational initiatives.

Data Collection

There is information about 306 different organizations in the dataset. All these

organizations had taken part in the survey conducted for the Carbon Disclosure Project (CDP).

More than 5000 industries had taken part in this survey. The information shared by the rest of the

industries over the selected years 2011 – 2016 has been found to be incomplete and thus has

been eliminated for the purpose of the survey. Three different variables from the entire dataset

has been considered suitable for this research. These include the carbon disclosure scores over

the years, the scope of the amount of carbon emissions by the companies over the years and

whether the organization has taken any initiatives against this problem of carbon emission.

Generalization of the results have been done as the results are available over time and only one

variable has been considered for each of the factors. Thus, the average of the disclosure scores,

adoption of different strategies and the emission of carbon over the years have been considered

as the measure for each of the variables. The necessary statistical analysis has been done on these

three transformed variables in order to test the stated hypothesis.

Data Analysis – Descriptive

Based on the literature review, the following hypothesis statements has been framed. The

Null Hypothesis and the Alternate Hypothesis that will be required in order to conduct the study

is described as follows:

Null Hypothesis (H0): There is no significant difference between the voluntary disclosure scores

on the basis of the organizational initiatives.

Alternate Hypothesis (HA): There are significant differences between the voluntary disclosure

scores on the basis of the organizational initiatives.

Data Collection

There is information about 306 different organizations in the dataset. All these

organizations had taken part in the survey conducted for the Carbon Disclosure Project (CDP).

More than 5000 industries had taken part in this survey. The information shared by the rest of the

industries over the selected years 2011 – 2016 has been found to be incomplete and thus has

been eliminated for the purpose of the survey. Three different variables from the entire dataset

has been considered suitable for this research. These include the carbon disclosure scores over

the years, the scope of the amount of carbon emissions by the companies over the years and

whether the organization has taken any initiatives against this problem of carbon emission.

Generalization of the results have been done as the results are available over time and only one

variable has been considered for each of the factors. Thus, the average of the disclosure scores,

adoption of different strategies and the emission of carbon over the years have been considered

as the measure for each of the variables. The necessary statistical analysis has been done on these

three transformed variables in order to test the stated hypothesis.

Data Analysis – Descriptive

8AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

The theoretical description of the data considered for the analysis is provided in table 2.

Depending on the nature of the variables as described in the table below, the following analysis

has been performed.

Table 2: Theoretical Description of the Data Considered

Theoretical

Construct

Proxy Measure

Dependent (DV),

Independent (IV) or

Control Variable

(CV)

Source

Disclosure Score

(Ratio scale)

Carbon Disclosure

score in CDP Survey

from the year 2009 to

2015

Dependent

(DV)

CDP Survey –

Disclosure Score

Scope 1 and 2 carbon

emission (Ratio scale)

Gross Global Scope 1

and Score 2

emissions mentioned

in CDP survey for all

1047 countries

Independent (IV) CDP Survey – Gross

Global Scope 1 and

Score 2 emission

figures in metric

tonnes units

Organizational

Initiatives (Nominal

Scale)

All the initiative

taken by the

organization in

categorical values

(Yes = 2 and No = 1)

Control Variable

(CV)

CDP Survey – Did

you have emissions

reduction initiatives

that were active?

The theoretical description of the data considered for the analysis is provided in table 2.

Depending on the nature of the variables as described in the table below, the following analysis

has been performed.

Table 2: Theoretical Description of the Data Considered

Theoretical

Construct

Proxy Measure

Dependent (DV),

Independent (IV) or

Control Variable

(CV)

Source

Disclosure Score

(Ratio scale)

Carbon Disclosure

score in CDP Survey

from the year 2009 to

2015

Dependent

(DV)

CDP Survey –

Disclosure Score

Scope 1 and 2 carbon

emission (Ratio scale)

Gross Global Scope 1

and Score 2

emissions mentioned

in CDP survey for all

1047 countries

Independent (IV) CDP Survey – Gross

Global Scope 1 and

Score 2 emission

figures in metric

tonnes units

Organizational

Initiatives (Nominal

Scale)

All the initiative

taken by the

organization in

categorical values

(Yes = 2 and No = 1)

Control Variable

(CV)

CDP Survey – Did

you have emissions

reduction initiatives

that were active?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

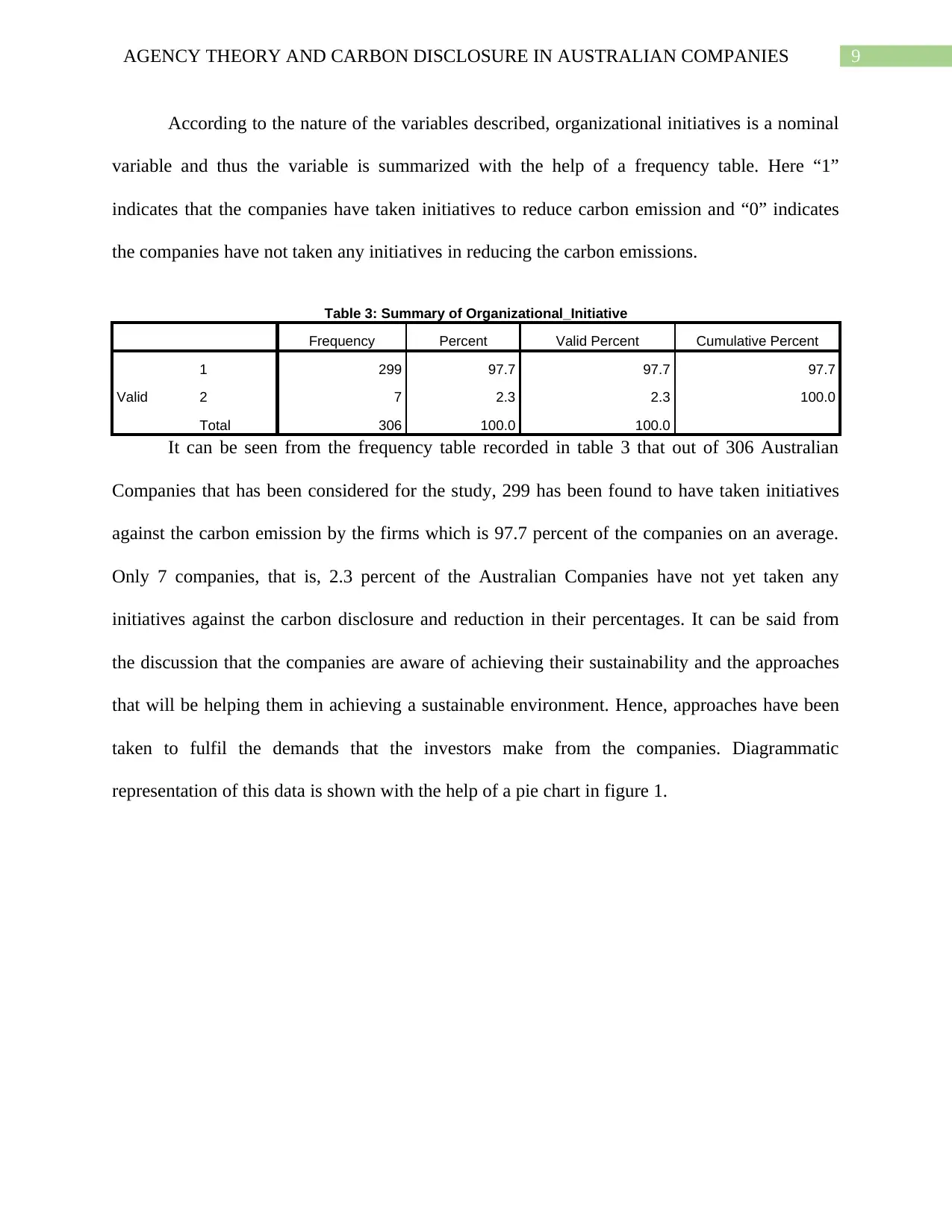

According to the nature of the variables described, organizational initiatives is a nominal

variable and thus the variable is summarized with the help of a frequency table. Here “1”

indicates that the companies have taken initiatives to reduce carbon emission and “0” indicates

the companies have not taken any initiatives in reducing the carbon emissions.

Table 3: Summary of Organizational_Initiative

Frequency Percent Valid Percent Cumulative Percent

Valid

1 299 97.7 97.7 97.7

2 7 2.3 2.3 100.0

Total 306 100.0 100.0

It can be seen from the frequency table recorded in table 3 that out of 306 Australian

Companies that has been considered for the study, 299 has been found to have taken initiatives

against the carbon emission by the firms which is 97.7 percent of the companies on an average.

Only 7 companies, that is, 2.3 percent of the Australian Companies have not yet taken any

initiatives against the carbon disclosure and reduction in their percentages. It can be said from

the discussion that the companies are aware of achieving their sustainability and the approaches

that will be helping them in achieving a sustainable environment. Hence, approaches have been

taken to fulfil the demands that the investors make from the companies. Diagrammatic

representation of this data is shown with the help of a pie chart in figure 1.

According to the nature of the variables described, organizational initiatives is a nominal

variable and thus the variable is summarized with the help of a frequency table. Here “1”

indicates that the companies have taken initiatives to reduce carbon emission and “0” indicates

the companies have not taken any initiatives in reducing the carbon emissions.

Table 3: Summary of Organizational_Initiative

Frequency Percent Valid Percent Cumulative Percent

Valid

1 299 97.7 97.7 97.7

2 7 2.3 2.3 100.0

Total 306 100.0 100.0

It can be seen from the frequency table recorded in table 3 that out of 306 Australian

Companies that has been considered for the study, 299 has been found to have taken initiatives

against the carbon emission by the firms which is 97.7 percent of the companies on an average.

Only 7 companies, that is, 2.3 percent of the Australian Companies have not yet taken any

initiatives against the carbon disclosure and reduction in their percentages. It can be said from

the discussion that the companies are aware of achieving their sustainability and the approaches

that will be helping them in achieving a sustainable environment. Hence, approaches have been

taken to fulfil the demands that the investors make from the companies. Diagrammatic

representation of this data is shown with the help of a pie chart in figure 1.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

Figure 1: Pie Chart Showing whether the companies have initiatives in reducing Carbon

Emissions

Other than the variable organizational initiatives, there are two other variables that have

been considered for the study. These are the carbon disclosure scores of the companies and

emissions of carbon by the companies. Both of these variables are presented in the ratio scale in

the dataset and thus can be used to evaluate the descriptive measures. Table 4 shows the

descriptive measures for the variables “carbon disclosure scores” and “carbon emissions”.

The disclosure scores of the companies are scored between “0” and “100”. The firm’s

position in the financial reports each year are indicated by the disclosure scores of the company

in that particular year. For the simplicity of the analysis, median scores of the carbon disclosure

scores over the years 2009 to 2015 have been considered. Considering the values in table 4. It

can be observed that the average disclosure score has been obtained as 78.44. Thus, it can be said

that the Australian companies are ranked around 78.44 in the financial reports. This can be said

as the standard deviation of the scores have been found to be 17.22, which is very less. Further, a

median score of 82 has been observed which indicates that 50 percent of the Australian

companies have a carbon disclosure score above 82 which is very commendable. It can also be

Figure 1: Pie Chart Showing whether the companies have initiatives in reducing Carbon

Emissions

Other than the variable organizational initiatives, there are two other variables that have

been considered for the study. These are the carbon disclosure scores of the companies and

emissions of carbon by the companies. Both of these variables are presented in the ratio scale in

the dataset and thus can be used to evaluate the descriptive measures. Table 4 shows the

descriptive measures for the variables “carbon disclosure scores” and “carbon emissions”.

The disclosure scores of the companies are scored between “0” and “100”. The firm’s

position in the financial reports each year are indicated by the disclosure scores of the company

in that particular year. For the simplicity of the analysis, median scores of the carbon disclosure

scores over the years 2009 to 2015 have been considered. Considering the values in table 4. It

can be observed that the average disclosure score has been obtained as 78.44. Thus, it can be said

that the Australian companies are ranked around 78.44 in the financial reports. This can be said

as the standard deviation of the scores have been found to be 17.22, which is very less. Further, a

median score of 82 has been observed which indicates that 50 percent of the Australian

companies have a carbon disclosure score above 82 which is very commendable. It can also be

11AGENCY THEORY AND CARBON DISCLOSURE IN AUSTRALIAN COMPANIES

seen from the skewness value that the data is not symmetric and is negatively skewed. This

indicates that the assumptions of normality have not been satisfied and also can be said that the

disclosure scores do not follow any distribution. Diagrammatic representation of this data is

shown with the help of a histogram in figure 2.

Another variable that has been considered is the emission of carbon from the companies.

The values of the variables are given in metric tonnes. For the simplicity of the analysis, average

of the amount of emission of carbon from the companies over the period of 2011 to 2017 have

been considered. Considering the values in table 4, it can be observed that the average amount of

carbon emission by the companies has been obtained as 12386.56. Thus, it can be said that the

Australian companies have a huge variation in the emission of carbon. This can be said as the

standard deviation of the emissions have been found to be 179438.62, which is very high.

Further, a median emission amount of 14.85 metric tonnes has been observed which indicates

that 50 percent of the Australian companies have a carbon disclosure score below 14.85 metric

tonnes. From the difference between the average emission amount and the median emission

amount, it can be said there are presence of outliers in the data. It can also be seen from the

skewness value that the data is not symmetric and is positively skewed. This indicates that the

assumptions of normality have not been satisfied and also can be said that the amount of carbon

emitted by the companies do not follow any distribution. Diagrammatic representation of this

data is shown with the help of a histogram in figure 3.

Table 4: Measures of Descriptive Statistics for Carbon Emission and Carbon Disclosure Scores

Disclosure_Scores Carbon_Emission

N Valid 306 306

Missing 0 0

Mean 78.4412 12386.5591

Std. Error of Mean .98446 10257.82293

seen from the skewness value that the data is not symmetric and is negatively skewed. This

indicates that the assumptions of normality have not been satisfied and also can be said that the

disclosure scores do not follow any distribution. Diagrammatic representation of this data is

shown with the help of a histogram in figure 2.

Another variable that has been considered is the emission of carbon from the companies.

The values of the variables are given in metric tonnes. For the simplicity of the analysis, average

of the amount of emission of carbon from the companies over the period of 2011 to 2017 have

been considered. Considering the values in table 4, it can be observed that the average amount of

carbon emission by the companies has been obtained as 12386.56. Thus, it can be said that the

Australian companies have a huge variation in the emission of carbon. This can be said as the

standard deviation of the emissions have been found to be 179438.62, which is very high.

Further, a median emission amount of 14.85 metric tonnes has been observed which indicates

that 50 percent of the Australian companies have a carbon disclosure score below 14.85 metric

tonnes. From the difference between the average emission amount and the median emission

amount, it can be said there are presence of outliers in the data. It can also be seen from the

skewness value that the data is not symmetric and is positively skewed. This indicates that the

assumptions of normality have not been satisfied and also can be said that the amount of carbon

emitted by the companies do not follow any distribution. Diagrammatic representation of this

data is shown with the help of a histogram in figure 3.

Table 4: Measures of Descriptive Statistics for Carbon Emission and Carbon Disclosure Scores

Disclosure_Scores Carbon_Emission

N Valid 306 306

Missing 0 0

Mean 78.4412 12386.5591

Std. Error of Mean .98446 10257.82293

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.