MGT723 Research Project Semester 2 2018: Carbon Reduction in Firms

VerifiedAdded on 2023/06/03

|20

|5042

|305

Report

AI Summary

This research project, a progress report for MGT723, investigates why some firms achieve greater carbon reductions than others, focusing on the integration of climate change into business strategies. The study employs a survey methodology using data from the CDP database, examining companies in Australia, Belgium, and Brazil. It explores the influence of stakeholder theory, environmental policies, and managerial incentives on carbon emission reduction. The report includes descriptive statistics, frequency distributions, and inferential statistics such as correlation and regression analysis to determine the relationship between independent and dependent variables. The findings highlight the importance of favorable climate regulations and policies in enhancing carbon reduction efforts within firms. The study also examines the role of the board and senior management in climate change responsibility and whether companies offer incentives for climate change management. The research aims to provide insights into the factors that drive carbon reduction and contribute to the understanding of sustainable business practices.

MGT723 Research Project

Semester 2 2018

Assessment Task 2: progress report

Student Name: Ashish Subedi

Draft Research Question: why some firms have achieved greater carbon reduction than others.

Submission Date: 14 september2018

Student ID: 1101763

Location: South bank Campus

Semester 2 2018

Assessment Task 2: progress report

Student Name: Ashish Subedi

Draft Research Question: why some firms have achieved greater carbon reduction than others.

Submission Date: 14 september2018

Student ID: 1101763

Location: South bank Campus

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The research proposes climate change integration into business strategy and state whether it

helps in carbon emission reduction. The research method of the study relates to the disclosures

retrieved with the use of survey technique which is available in the website of the CDP. The

study also states the purpose of considering sample of companies to participate in the survey.

The main idea of the study is explained with the response of the descriptive design. The study

will use the disclosure percentages as per the climate change which needs to be integrated into

the perception of the pressure taken from the consumers which may have a considerable amount

of impact on the performance of market. This analysis will consist of the descriptive analysis

along with combination of inferential statistical tools. The objectives pertaining to the analysis

will be measurable as per the independent variable affecting the dependent variable. As the

companies has self-reported the statistics, this is speculated in terms of the performance of the

company and various other factors which may be measured as political influences and social

influences. In case survey of the study is larger than the size then the disclosure of the carbon

emissions will be able to show whether a company will be able to actively take part in the

strategy for showing the main agents which are responsible for the emissions. Theoretical

Construct has been taken from the Climate change integrated into business strategy which has

shown climate change integration with the topic of carbon emission will depend on the strategies

integrated by the business. Carbon emission reduction has been depicted with the dependent

variable which is included under the scope of the study of carbon emissions. Motivation

construct are considered to be important as the companies may decide to be benefitted financially

relating to these incentives (Moriarty, 2014).

The research proposes climate change integration into business strategy and state whether it

helps in carbon emission reduction. The research method of the study relates to the disclosures

retrieved with the use of survey technique which is available in the website of the CDP. The

study also states the purpose of considering sample of companies to participate in the survey.

The main idea of the study is explained with the response of the descriptive design. The study

will use the disclosure percentages as per the climate change which needs to be integrated into

the perception of the pressure taken from the consumers which may have a considerable amount

of impact on the performance of market. This analysis will consist of the descriptive analysis

along with combination of inferential statistical tools. The objectives pertaining to the analysis

will be measurable as per the independent variable affecting the dependent variable. As the

companies has self-reported the statistics, this is speculated in terms of the performance of the

company and various other factors which may be measured as political influences and social

influences. In case survey of the study is larger than the size then the disclosure of the carbon

emissions will be able to show whether a company will be able to actively take part in the

strategy for showing the main agents which are responsible for the emissions. Theoretical

Construct has been taken from the Climate change integrated into business strategy which has

shown climate change integration with the topic of carbon emission will depend on the strategies

integrated by the business. Carbon emission reduction has been depicted with the dependent

variable which is included under the scope of the study of carbon emissions. Motivation

construct are considered to be important as the companies may decide to be benefitted financially

relating to these incentives (Moriarty, 2014).

Literature Review

Stakeholder theory as suggested by Dr Edward Freeman, the brain behind the idea, argues that

shareholders are among the many shareholders in accompanied. In this theory the stakeholder

ecosystem is made up of any individual who has in any way invested in or has taken part in a

firm. The stakeholders of a firm include company’s plants, environmentalists, government

agencies and its employees among other stakeholders (McNabb 2015).

According to Freeman, the actual success of a firm to a great extent depends on meeting the

needs and demands of the various stakeholders. This is in contravention ion of just meeting the

needs of only those people who may reap from the stock issued (McNabb 2015). In his work, the

philosopher suggests that the stakeholders of a firm are defined by the group of people on which

their support forms the basis of continuous existence of the company.

Favourable environmental policies and regulations, promotion of environmental conservation as

well as incorporation of the need to conserve the environment as part of the missions of a

company can be attributed to be some of the underlying reasons for some firms having greater

carbon reduction than others.

Conceptual Model

Normative and managerial motivations both have an influence on the process of decision making

in offering suggestions on the various strategies to the stakeholder theory. Such motivations are

important in the analysis of the interaction between the company and the stakeholder (McNabb

2015).

Following the broad question posed:

“Why have some firms achieved greater carbon reductions that others”

A metaphoric approach to stakeholder theory is thus adopted in which identification of the

motivations have been done through the various theories to be underlying factors in the process

of decision making by the management and the stakeholders (Hitt & Duane Ireland 2017). The

empirical parts of this research aim at the identification and determination whether such

motivations that have been identified by the theory have a role to play when it comes to the

process of decision making by the management of the various firms. Below is a conceptual

Stakeholder theory as suggested by Dr Edward Freeman, the brain behind the idea, argues that

shareholders are among the many shareholders in accompanied. In this theory the stakeholder

ecosystem is made up of any individual who has in any way invested in or has taken part in a

firm. The stakeholders of a firm include company’s plants, environmentalists, government

agencies and its employees among other stakeholders (McNabb 2015).

According to Freeman, the actual success of a firm to a great extent depends on meeting the

needs and demands of the various stakeholders. This is in contravention ion of just meeting the

needs of only those people who may reap from the stock issued (McNabb 2015). In his work, the

philosopher suggests that the stakeholders of a firm are defined by the group of people on which

their support forms the basis of continuous existence of the company.

Favourable environmental policies and regulations, promotion of environmental conservation as

well as incorporation of the need to conserve the environment as part of the missions of a

company can be attributed to be some of the underlying reasons for some firms having greater

carbon reduction than others.

Conceptual Model

Normative and managerial motivations both have an influence on the process of decision making

in offering suggestions on the various strategies to the stakeholder theory. Such motivations are

important in the analysis of the interaction between the company and the stakeholder (McNabb

2015).

Following the broad question posed:

“Why have some firms achieved greater carbon reductions that others”

A metaphoric approach to stakeholder theory is thus adopted in which identification of the

motivations have been done through the various theories to be underlying factors in the process

of decision making by the management and the stakeholders (Hitt & Duane Ireland 2017). The

empirical parts of this research aim at the identification and determination whether such

motivations that have been identified by the theory have a role to play when it comes to the

process of decision making by the management of the various firms. Below is a conceptual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

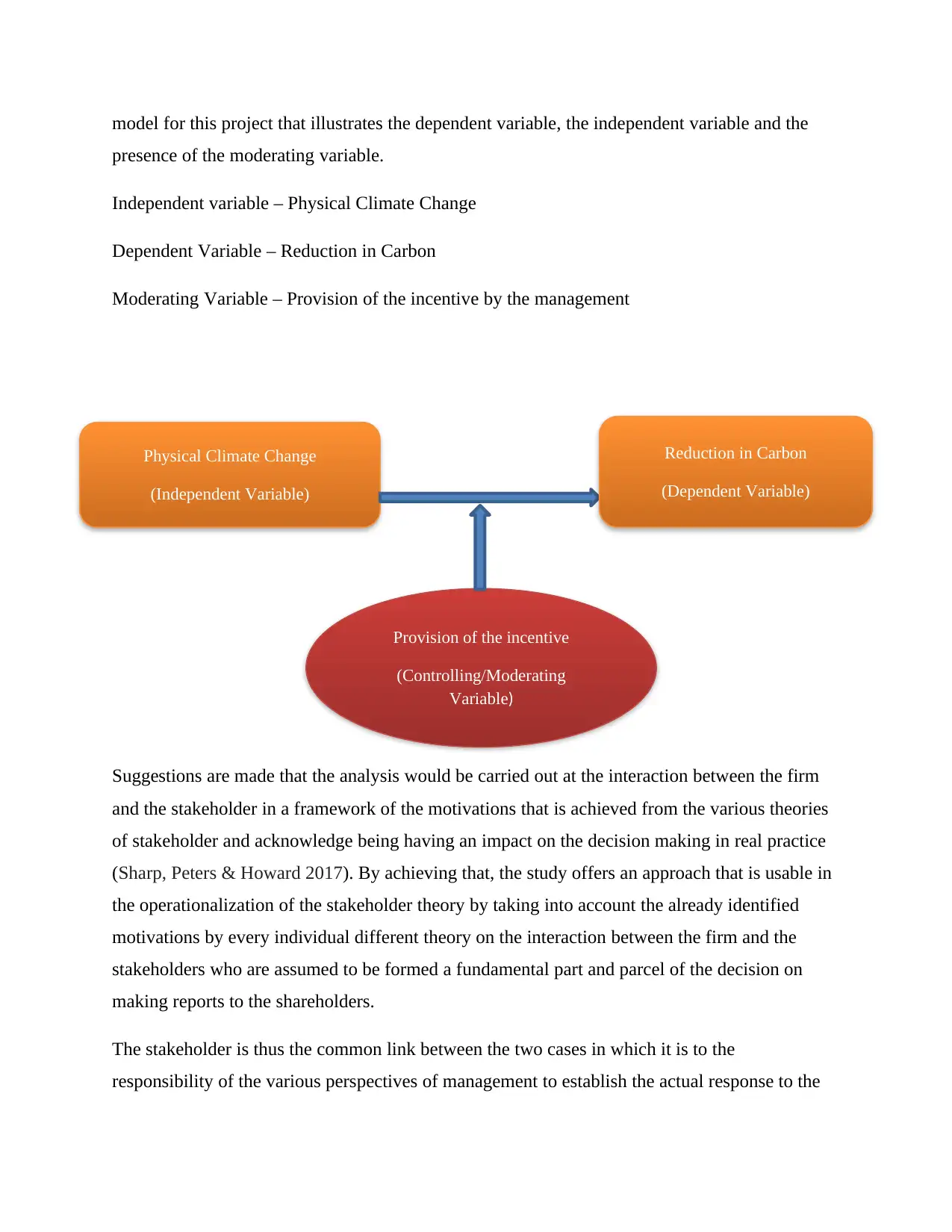

model for this project that illustrates the dependent variable, the independent variable and the

presence of the moderating variable.

Independent variable – Physical Climate Change

Dependent Variable – Reduction in Carbon

Moderating Variable – Provision of the incentive by the management

Suggestions are made that the analysis would be carried out at the interaction between the firm

and the stakeholder in a framework of the motivations that is achieved from the various theories

of stakeholder and acknowledge being having an impact on the decision making in real practice

(Sharp, Peters & Howard 2017). By achieving that, the study offers an approach that is usable in

the operationalization of the stakeholder theory by taking into account the already identified

motivations by every individual different theory on the interaction between the firm and the

stakeholders who are assumed to be formed a fundamental part and parcel of the decision on

making reports to the shareholders.

The stakeholder is thus the common link between the two cases in which it is to the

responsibility of the various perspectives of management to establish the actual response to the

Physical Climate Change

(Independent Variable)

Provision of the incentive

(Controlling/Moderating

Variable)

Reduction in Carbon

(Dependent Variable)

presence of the moderating variable.

Independent variable – Physical Climate Change

Dependent Variable – Reduction in Carbon

Moderating Variable – Provision of the incentive by the management

Suggestions are made that the analysis would be carried out at the interaction between the firm

and the stakeholder in a framework of the motivations that is achieved from the various theories

of stakeholder and acknowledge being having an impact on the decision making in real practice

(Sharp, Peters & Howard 2017). By achieving that, the study offers an approach that is usable in

the operationalization of the stakeholder theory by taking into account the already identified

motivations by every individual different theory on the interaction between the firm and the

stakeholders who are assumed to be formed a fundamental part and parcel of the decision on

making reports to the shareholders.

The stakeholder is thus the common link between the two cases in which it is to the

responsibility of the various perspectives of management to establish the actual response to the

Physical Climate Change

(Independent Variable)

Provision of the incentive

(Controlling/Moderating

Variable)

Reduction in Carbon

(Dependent Variable)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

anticipated stakeholders. On the other hand, the normative perspective provides suggestion that

the firm has a role to play in attaining the intrinsic rights of the various stakeholders through the

provision of environmental information (El-Nasr, Drachen & Canossa 2016).

The dependent variable in the study is reduction in carbon

The year in which the study was conducted is the moderating or control variable (Ahuja

2017)

The physical climate change of the various countries form the independent variable

Hypotheses

The null and alternative hypotheses to be tested for this study can be formulated as follows;

Ho: Favourable climatic regulations and policies enhance higher carbon reduction in firms

H1: Favourable climatic regulations and policies do not enhance higher carbon reduction in firms

Research Method

This research adopted survey for gathering of data for analysis and achievement of the objectives

of the study which were the reasons behind some firms having greater carbon reductions than

others (Saghafian, Austin & Traub 2015). Approximately 550 firms were sampled in the study to

offer a wide range of the independent variable. The survey was found to be simple, convenient,

precise in its results and low cost as some of its main strengths. Rigidity of the technique besides

as well as the possibility of deliberately providing false or inaccurate information was the main

drawbacks of surveys as the technique.

Data collection

Data was obtained from a CPD database that contain all the carbon emissions data for all the

countries around the globe. The dataset are categorized for the different industries in different

countries working on different sectors of economy. We considered the 2012 data set for three

countries; Australia, Belgium and Brazil which have achieved greater carbon reduction. There

were a total of 218 observations (industries) considered for this study with 80 companies from

Australia, 11 companies from Belgium and 127 companies from Brazil. A separate excel file is

submitted together with this report. This paper applied both descriptive and inferential statistics

the firm has a role to play in attaining the intrinsic rights of the various stakeholders through the

provision of environmental information (El-Nasr, Drachen & Canossa 2016).

The dependent variable in the study is reduction in carbon

The year in which the study was conducted is the moderating or control variable (Ahuja

2017)

The physical climate change of the various countries form the independent variable

Hypotheses

The null and alternative hypotheses to be tested for this study can be formulated as follows;

Ho: Favourable climatic regulations and policies enhance higher carbon reduction in firms

H1: Favourable climatic regulations and policies do not enhance higher carbon reduction in firms

Research Method

This research adopted survey for gathering of data for analysis and achievement of the objectives

of the study which were the reasons behind some firms having greater carbon reductions than

others (Saghafian, Austin & Traub 2015). Approximately 550 firms were sampled in the study to

offer a wide range of the independent variable. The survey was found to be simple, convenient,

precise in its results and low cost as some of its main strengths. Rigidity of the technique besides

as well as the possibility of deliberately providing false or inaccurate information was the main

drawbacks of surveys as the technique.

Data collection

Data was obtained from a CPD database that contain all the carbon emissions data for all the

countries around the globe. The dataset are categorized for the different industries in different

countries working on different sectors of economy. We considered the 2012 data set for three

countries; Australia, Belgium and Brazil which have achieved greater carbon reduction. There

were a total of 218 observations (industries) considered for this study with 80 companies from

Australia, 11 companies from Belgium and 127 companies from Brazil. A separate excel file is

submitted together with this report. This paper applied both descriptive and inferential statistics

to investigate the relationship between the dependent variables and the independent variable with

reference to the moderating variable.

Data Analysis

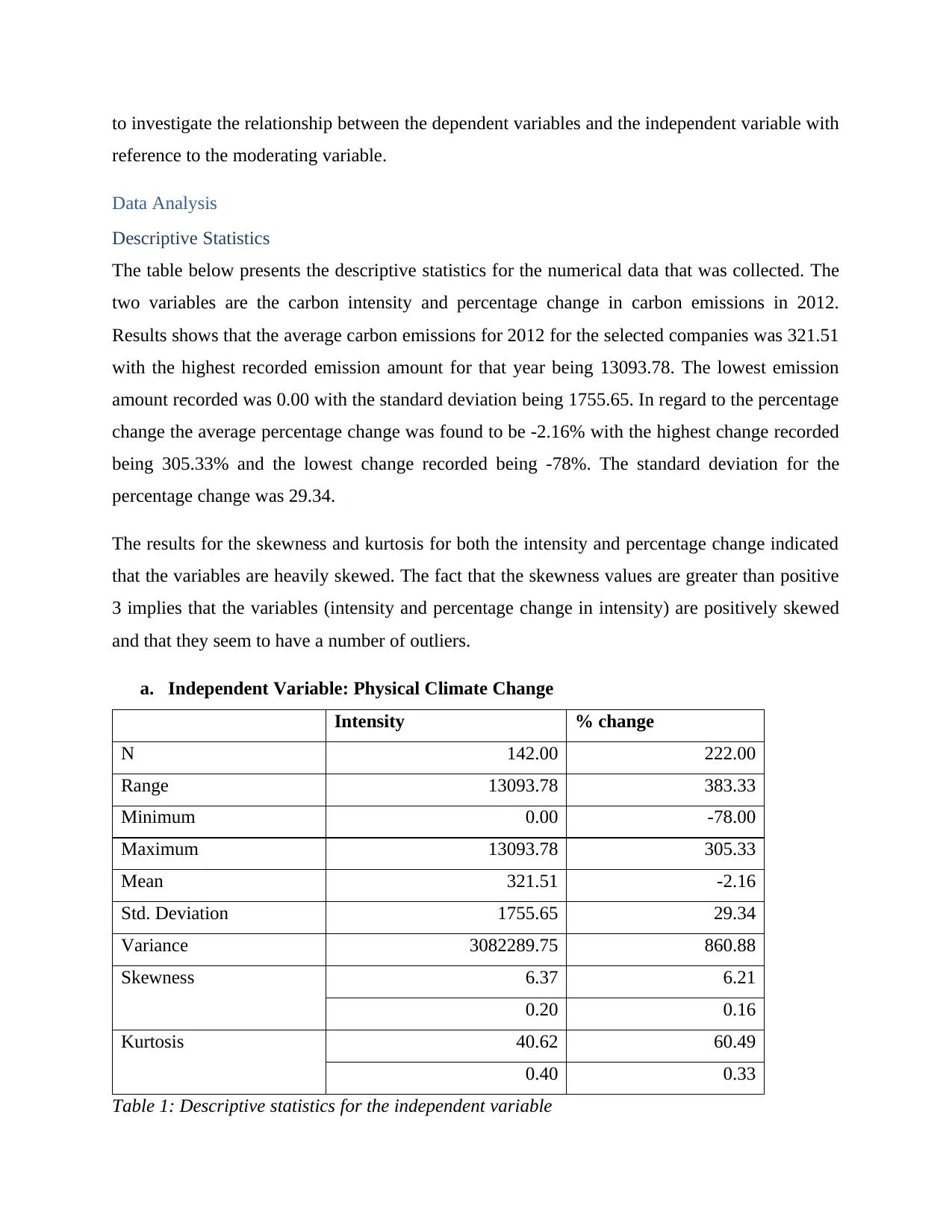

Descriptive Statistics

The table below presents the descriptive statistics for the numerical data that was collected. The

two variables are the carbon intensity and percentage change in carbon emissions in 2012.

Results shows that the average carbon emissions for 2012 for the selected companies was 321.51

with the highest recorded emission amount for that year being 13093.78. The lowest emission

amount recorded was 0.00 with the standard deviation being 1755.65. In regard to the percentage

change the average percentage change was found to be -2.16% with the highest change recorded

being 305.33% and the lowest change recorded being -78%. The standard deviation for the

percentage change was 29.34.

The results for the skewness and kurtosis for both the intensity and percentage change indicated

that the variables are heavily skewed. The fact that the skewness values are greater than positive

3 implies that the variables (intensity and percentage change in intensity) are positively skewed

and that they seem to have a number of outliers.

a. Independent Variable: Physical Climate Change

Intensity % change

N 142.00 222.00

Range 13093.78 383.33

Minimum 0.00 -78.00

Maximum 13093.78 305.33

Mean 321.51 -2.16

Std. Deviation 1755.65 29.34

Variance 3082289.75 860.88

Skewness 6.37 6.21

0.20 0.16

Kurtosis 40.62 60.49

0.40 0.33

Table 1: Descriptive statistics for the independent variable

reference to the moderating variable.

Data Analysis

Descriptive Statistics

The table below presents the descriptive statistics for the numerical data that was collected. The

two variables are the carbon intensity and percentage change in carbon emissions in 2012.

Results shows that the average carbon emissions for 2012 for the selected companies was 321.51

with the highest recorded emission amount for that year being 13093.78. The lowest emission

amount recorded was 0.00 with the standard deviation being 1755.65. In regard to the percentage

change the average percentage change was found to be -2.16% with the highest change recorded

being 305.33% and the lowest change recorded being -78%. The standard deviation for the

percentage change was 29.34.

The results for the skewness and kurtosis for both the intensity and percentage change indicated

that the variables are heavily skewed. The fact that the skewness values are greater than positive

3 implies that the variables (intensity and percentage change in intensity) are positively skewed

and that they seem to have a number of outliers.

a. Independent Variable: Physical Climate Change

Intensity % change

N 142.00 222.00

Range 13093.78 383.33

Minimum 0.00 -78.00

Maximum 13093.78 305.33

Mean 321.51 -2.16

Std. Deviation 1755.65 29.34

Variance 3082289.75 860.88

Skewness 6.37 6.21

0.20 0.16

Kurtosis 40.62 60.49

0.40 0.33

Table 1: Descriptive statistics for the independent variable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

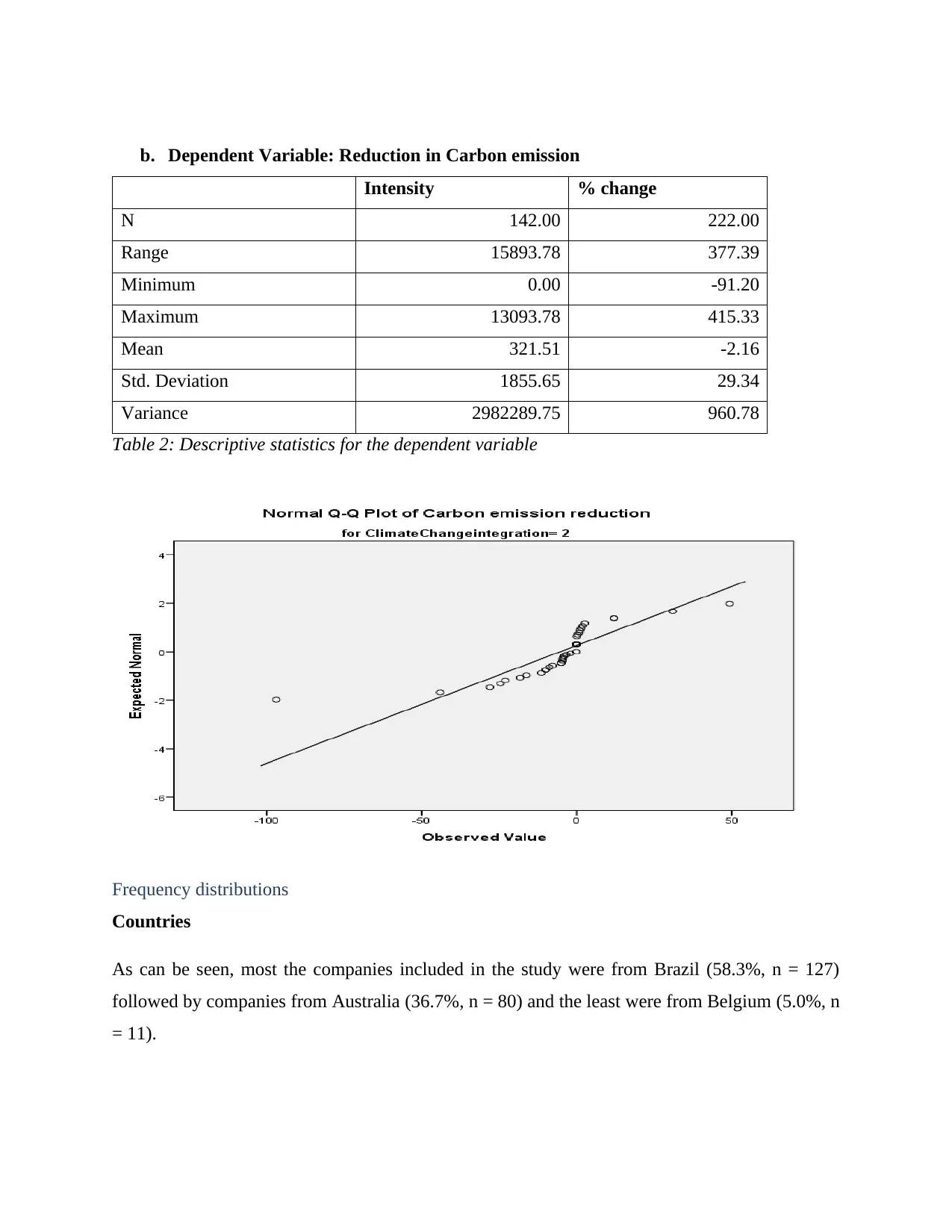

b. Dependent Variable: Reduction in Carbon emission

Intensity % change

N 142.00 222.00

Range 15893.78 377.39

Minimum 0.00 -91.20

Maximum 13093.78 415.33

Mean 321.51 -2.16

Std. Deviation 1855.65 29.34

Variance 2982289.75 960.78

Table 2: Descriptive statistics for the dependent variable

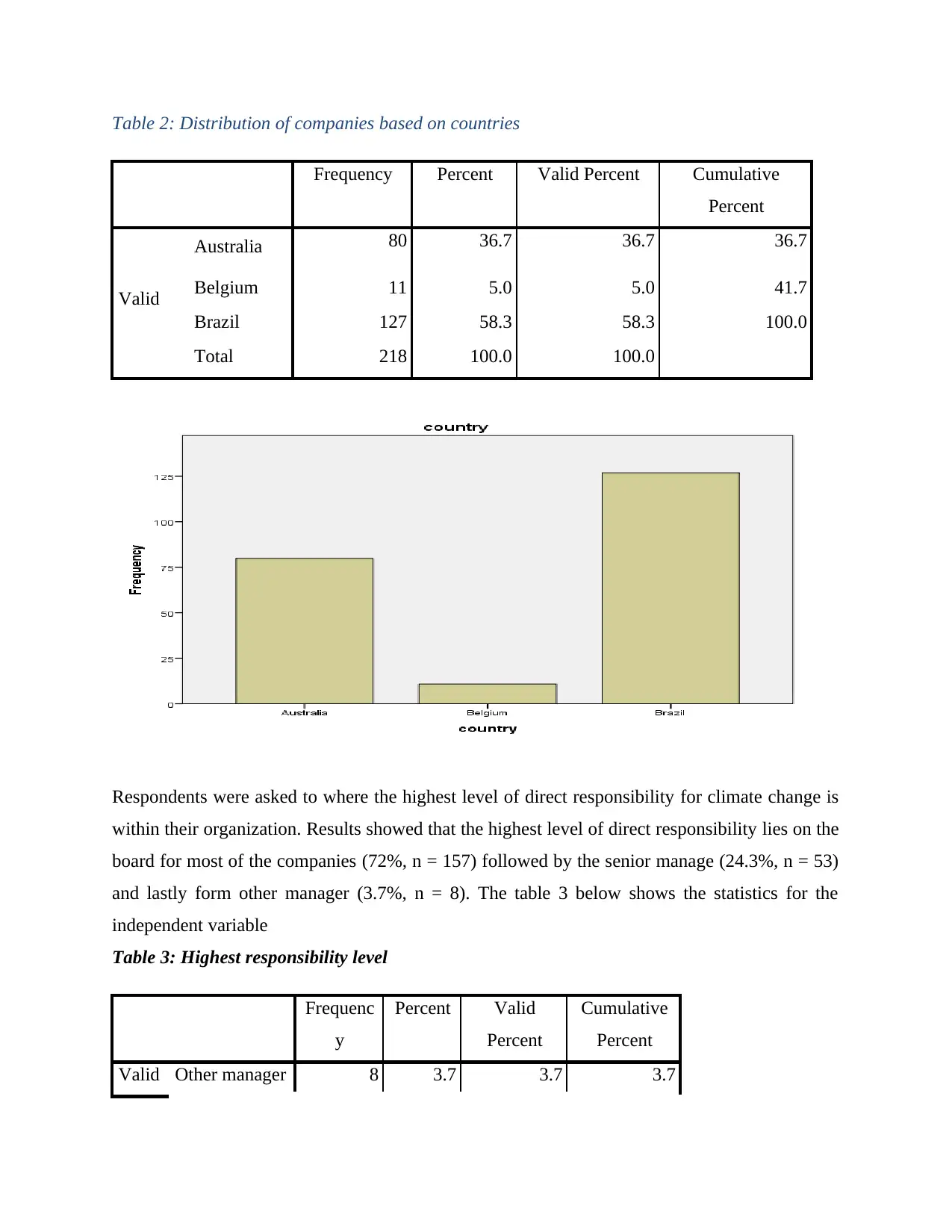

Frequency distributions

Countries

As can be seen, most the companies included in the study were from Brazil (58.3%, n = 127)

followed by companies from Australia (36.7%, n = 80) and the least were from Belgium (5.0%, n

= 11).

Intensity % change

N 142.00 222.00

Range 15893.78 377.39

Minimum 0.00 -91.20

Maximum 13093.78 415.33

Mean 321.51 -2.16

Std. Deviation 1855.65 29.34

Variance 2982289.75 960.78

Table 2: Descriptive statistics for the dependent variable

Frequency distributions

Countries

As can be seen, most the companies included in the study were from Brazil (58.3%, n = 127)

followed by companies from Australia (36.7%, n = 80) and the least were from Belgium (5.0%, n

= 11).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 2: Distribution of companies based on countries

Frequency Percent Valid Percent Cumulative

Percent

Valid

Australia 80 36.7 36.7 36.7

Belgium 11 5.0 5.0 41.7

Brazil 127 58.3 58.3 100.0

Total 218 100.0 100.0

Respondents were asked to where the highest level of direct responsibility for climate change is

within their organization. Results showed that the highest level of direct responsibility lies on the

board for most of the companies (72%, n = 157) followed by the senior manage (24.3%, n = 53)

and lastly form other manager (3.7%, n = 8). The table 3 below shows the statistics for the

independent variable

Table 3: Highest responsibility level

Frequenc

y

Percent Valid

Percent

Cumulative

Percent

Valid Other manager 8 3.7 3.7 3.7

Frequency Percent Valid Percent Cumulative

Percent

Valid

Australia 80 36.7 36.7 36.7

Belgium 11 5.0 5.0 41.7

Brazil 127 58.3 58.3 100.0

Total 218 100.0 100.0

Respondents were asked to where the highest level of direct responsibility for climate change is

within their organization. Results showed that the highest level of direct responsibility lies on the

board for most of the companies (72%, n = 157) followed by the senior manage (24.3%, n = 53)

and lastly form other manager (3.7%, n = 8). The table 3 below shows the statistics for the

independent variable

Table 3: Highest responsibility level

Frequenc

y

Percent Valid

Percent

Cumulative

Percent

Valid Other manager 8 3.7 3.7 3.7

Senior

manager

53 24.3 24.3 28.0

Board 157 72.0 72.0 100.0

Total 218 100.0 100.0

In regard to whether the Company provides incentives for the management of climate change

issues, including the attainment of targets. Slightly more than half of the companies (50.9%, n =

111) said to offer incentives while 49.1% (n = 107) did not offer incentives for the management

of climate change issues (moderating variable).

Provision of incentives

Frequency Percent Valid

Percent

Cumulative

Percent

Valid

Yes 111 50.9 50.9 50.9

No 107 49.1 49.1 100.0

Total 218 100.0 100.0

Lastly, the survey sought to understand whether the companies have climate change integrated

into their business strategy. 70.4% (n = 152) had the climate change integrated into their business

strategy while the rest 29.6% (n = 64) did not have.

Is climate change integrated into your business strategy?

Frequency Percent Valid Percent Cumulative Percent

Valid

Yes 152 69.7 70.4 70.4

No 64 29.4 29.6 100.0

Total 216 99.1 100.0

Missing 999 2 .9

Total 218 100.0

manager

53 24.3 24.3 28.0

Board 157 72.0 72.0 100.0

Total 218 100.0 100.0

In regard to whether the Company provides incentives for the management of climate change

issues, including the attainment of targets. Slightly more than half of the companies (50.9%, n =

111) said to offer incentives while 49.1% (n = 107) did not offer incentives for the management

of climate change issues (moderating variable).

Provision of incentives

Frequency Percent Valid

Percent

Cumulative

Percent

Valid

Yes 111 50.9 50.9 50.9

No 107 49.1 49.1 100.0

Total 218 100.0 100.0

Lastly, the survey sought to understand whether the companies have climate change integrated

into their business strategy. 70.4% (n = 152) had the climate change integrated into their business

strategy while the rest 29.6% (n = 64) did not have.

Is climate change integrated into your business strategy?

Frequency Percent Valid Percent Cumulative Percent

Valid

Yes 152 69.7 70.4 70.4

No 64 29.4 29.6 100.0

Total 216 99.1 100.0

Missing 999 2 .9

Total 218 100.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inferential Statistics

For the inferential statistics, correlation analysis, regression analysis and hypothesis testing was

conducted to determine “Why have some firms achieved greater carbon reductions that others”

and the relationship that exist between the dependent and independent variables.

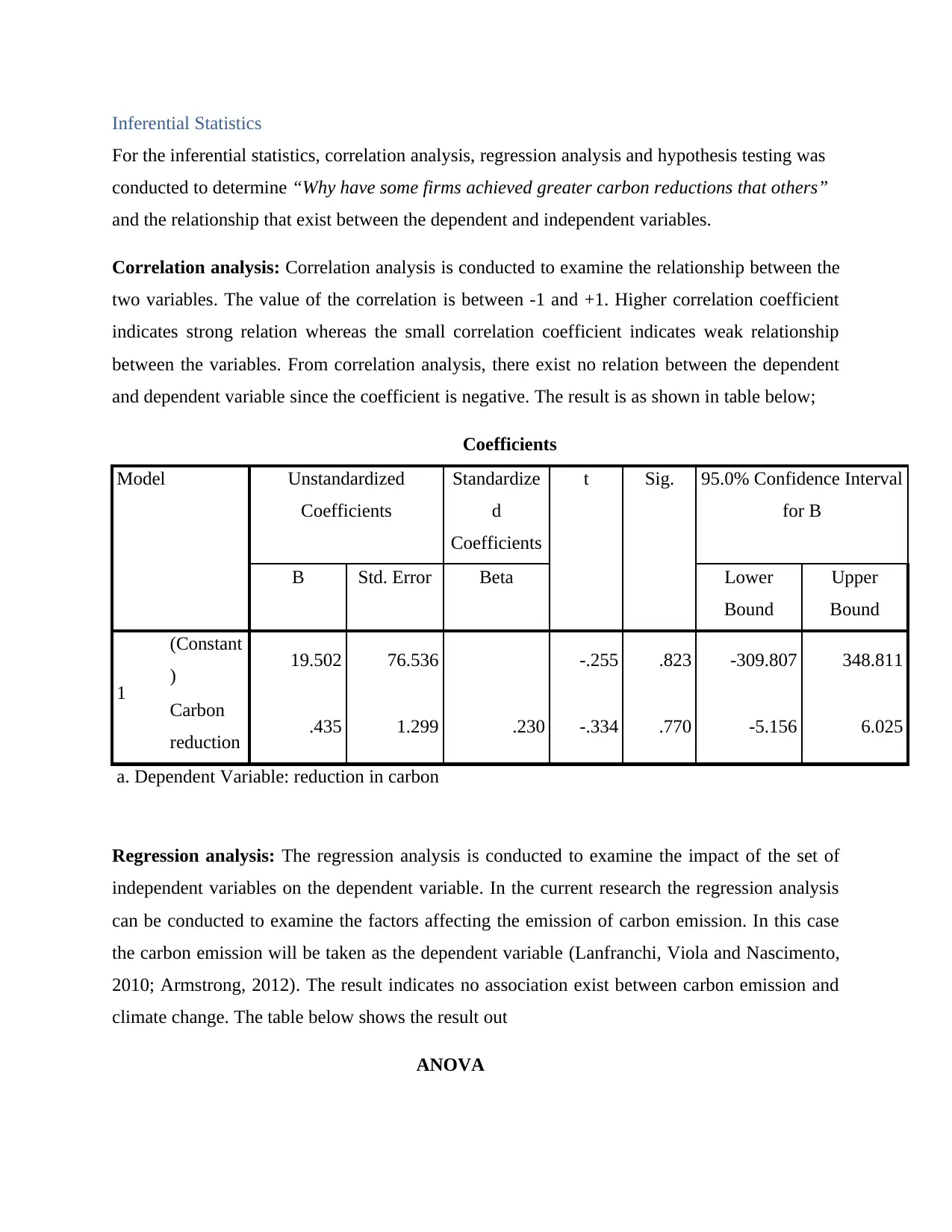

Correlation analysis: Correlation analysis is conducted to examine the relationship between the

two variables. The value of the correlation is between -1 and +1. Higher correlation coefficient

indicates strong relation whereas the small correlation coefficient indicates weak relationship

between the variables. From correlation analysis, there exist no relation between the dependent

and dependent variable since the coefficient is negative. The result is as shown in table below;

Coefficients

Model Unstandardized

Coefficients

Standardize

d

Coefficients

t Sig. 95.0% Confidence Interval

for B

B Std. Error Beta Lower

Bound

Upper

Bound

1

(Constant

) 19.502 76.536 -.255 .823 -309.807 348.811

Carbon

reduction .435 1.299 .230 -.334 .770 -5.156 6.025

a. Dependent Variable: reduction in carbon

Regression analysis: The regression analysis is conducted to examine the impact of the set of

independent variables on the dependent variable. In the current research the regression analysis

can be conducted to examine the factors affecting the emission of carbon emission. In this case

the carbon emission will be taken as the dependent variable (Lanfranchi, Viola and Nascimento,

2010; Armstrong, 2012). The result indicates no association exist between carbon emission and

climate change. The table below shows the result out

ANOVA

For the inferential statistics, correlation analysis, regression analysis and hypothesis testing was

conducted to determine “Why have some firms achieved greater carbon reductions that others”

and the relationship that exist between the dependent and independent variables.

Correlation analysis: Correlation analysis is conducted to examine the relationship between the

two variables. The value of the correlation is between -1 and +1. Higher correlation coefficient

indicates strong relation whereas the small correlation coefficient indicates weak relationship

between the variables. From correlation analysis, there exist no relation between the dependent

and dependent variable since the coefficient is negative. The result is as shown in table below;

Coefficients

Model Unstandardized

Coefficients

Standardize

d

Coefficients

t Sig. 95.0% Confidence Interval

for B

B Std. Error Beta Lower

Bound

Upper

Bound

1

(Constant

) 19.502 76.536 -.255 .823 -309.807 348.811

Carbon

reduction .435 1.299 .230 -.334 .770 -5.156 6.025

a. Dependent Variable: reduction in carbon

Regression analysis: The regression analysis is conducted to examine the impact of the set of

independent variables on the dependent variable. In the current research the regression analysis

can be conducted to examine the factors affecting the emission of carbon emission. In this case

the carbon emission will be taken as the dependent variable (Lanfranchi, Viola and Nascimento,

2010; Armstrong, 2012). The result indicates no association exist between carbon emission and

climate change. The table below shows the result out

ANOVA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

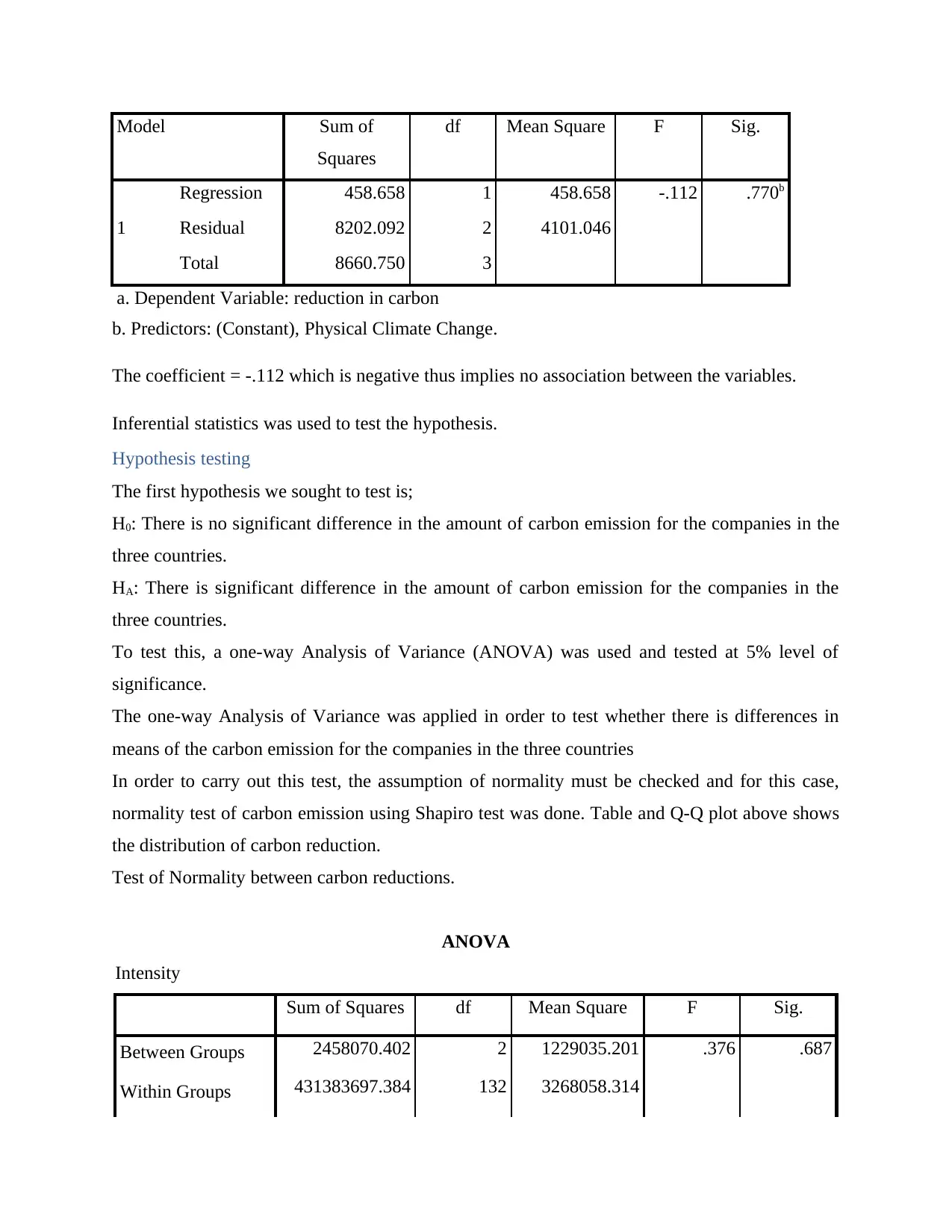

Model Sum of

Squares

df Mean Square F Sig.

1

Regression 458.658 1 458.658 -.112 .770b

Residual 8202.092 2 4101.046

Total 8660.750 3

a. Dependent Variable: reduction in carbon

b. Predictors: (Constant), Physical Climate Change.

The coefficient = -.112 which is negative thus implies no association between the variables.

Inferential statistics was used to test the hypothesis.

Hypothesis testing

The first hypothesis we sought to test is;

H0: There is no significant difference in the amount of carbon emission for the companies in the

three countries.

HA: There is significant difference in the amount of carbon emission for the companies in the

three countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance.

The one-way Analysis of Variance was applied in order to test whether there is differences in

means of the carbon emission for the companies in the three countries

In order to carry out this test, the assumption of normality must be checked and for this case,

normality test of carbon emission using Shapiro test was done. Table and Q-Q plot above shows

the distribution of carbon reduction.

Test of Normality between carbon reductions.

ANOVA

Intensity

Sum of Squares df Mean Square F Sig.

Between Groups 2458070.402 2 1229035.201 .376 .687

Within Groups 431383697.384 132 3268058.314

Squares

df Mean Square F Sig.

1

Regression 458.658 1 458.658 -.112 .770b

Residual 8202.092 2 4101.046

Total 8660.750 3

a. Dependent Variable: reduction in carbon

b. Predictors: (Constant), Physical Climate Change.

The coefficient = -.112 which is negative thus implies no association between the variables.

Inferential statistics was used to test the hypothesis.

Hypothesis testing

The first hypothesis we sought to test is;

H0: There is no significant difference in the amount of carbon emission for the companies in the

three countries.

HA: There is significant difference in the amount of carbon emission for the companies in the

three countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance.

The one-way Analysis of Variance was applied in order to test whether there is differences in

means of the carbon emission for the companies in the three countries

In order to carry out this test, the assumption of normality must be checked and for this case,

normality test of carbon emission using Shapiro test was done. Table and Q-Q plot above shows

the distribution of carbon reduction.

Test of Normality between carbon reductions.

ANOVA

Intensity

Sum of Squares df Mean Square F Sig.

Between Groups 2458070.402 2 1229035.201 .376 .687

Within Groups 431383697.384 132 3268058.314

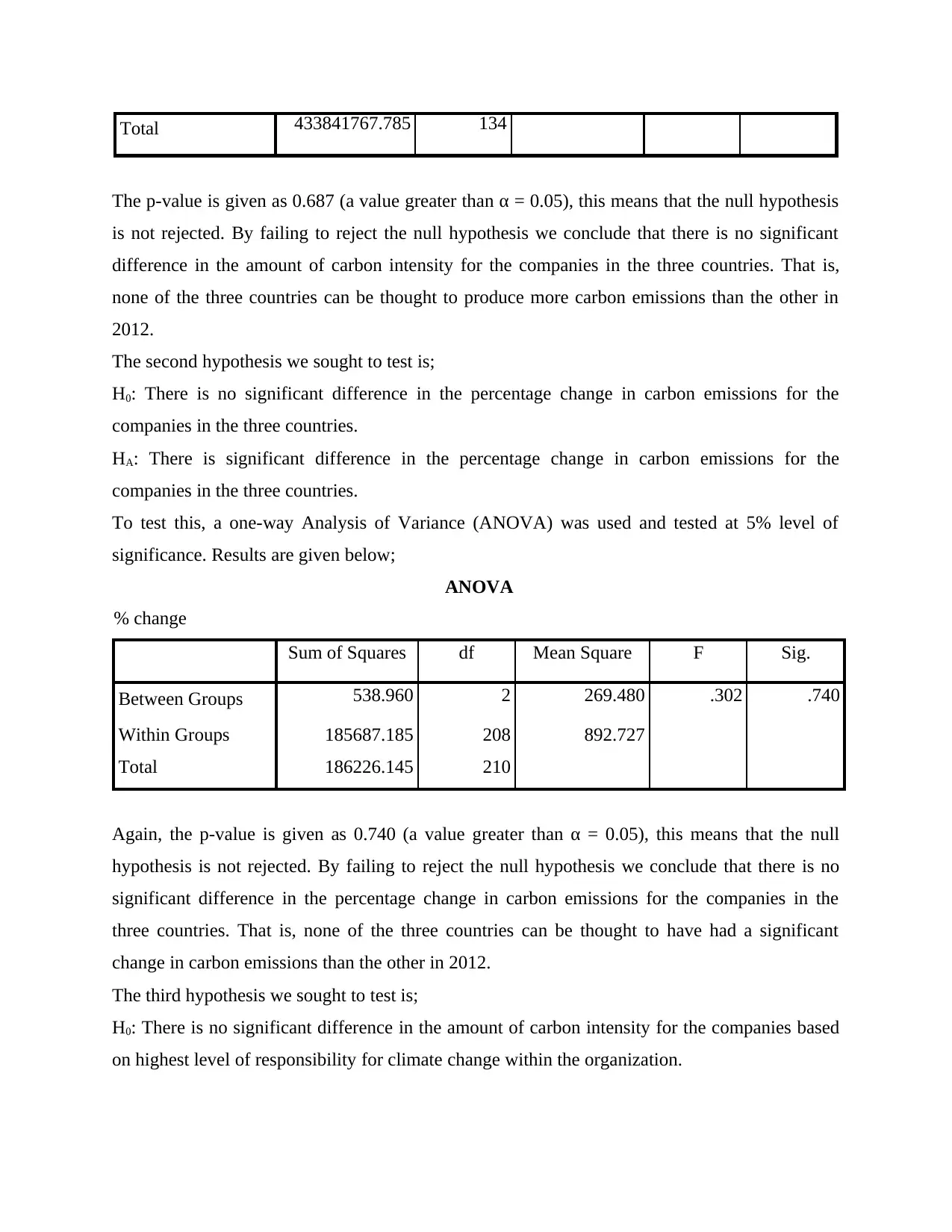

Total 433841767.785 134

The p-value is given as 0.687 (a value greater than α = 0.05), this means that the null hypothesis

is not rejected. By failing to reject the null hypothesis we conclude that there is no significant

difference in the amount of carbon intensity for the companies in the three countries. That is,

none of the three countries can be thought to produce more carbon emissions than the other in

2012.

The second hypothesis we sought to test is;

H0: There is no significant difference in the percentage change in carbon emissions for the

companies in the three countries.

HA: There is significant difference in the percentage change in carbon emissions for the

companies in the three countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance. Results are given below;

ANOVA

% change

Sum of Squares df Mean Square F Sig.

Between Groups 538.960 2 269.480 .302 .740

Within Groups 185687.185 208 892.727

Total 186226.145 210

Again, the p-value is given as 0.740 (a value greater than α = 0.05), this means that the null

hypothesis is not rejected. By failing to reject the null hypothesis we conclude that there is no

significant difference in the percentage change in carbon emissions for the companies in the

three countries. That is, none of the three countries can be thought to have had a significant

change in carbon emissions than the other in 2012.

The third hypothesis we sought to test is;

H0: There is no significant difference in the amount of carbon intensity for the companies based

on highest level of responsibility for climate change within the organization.

The p-value is given as 0.687 (a value greater than α = 0.05), this means that the null hypothesis

is not rejected. By failing to reject the null hypothesis we conclude that there is no significant

difference in the amount of carbon intensity for the companies in the three countries. That is,

none of the three countries can be thought to produce more carbon emissions than the other in

2012.

The second hypothesis we sought to test is;

H0: There is no significant difference in the percentage change in carbon emissions for the

companies in the three countries.

HA: There is significant difference in the percentage change in carbon emissions for the

companies in the three countries.

To test this, a one-way Analysis of Variance (ANOVA) was used and tested at 5% level of

significance. Results are given below;

ANOVA

% change

Sum of Squares df Mean Square F Sig.

Between Groups 538.960 2 269.480 .302 .740

Within Groups 185687.185 208 892.727

Total 186226.145 210

Again, the p-value is given as 0.740 (a value greater than α = 0.05), this means that the null

hypothesis is not rejected. By failing to reject the null hypothesis we conclude that there is no

significant difference in the percentage change in carbon emissions for the companies in the

three countries. That is, none of the three countries can be thought to have had a significant

change in carbon emissions than the other in 2012.

The third hypothesis we sought to test is;

H0: There is no significant difference in the amount of carbon intensity for the companies based

on highest level of responsibility for climate change within the organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.