Accounting Financial Analysis Report: Q2 2019 Results

VerifiedAdded on 2023/04/22

|12

|2279

|444

Report

AI Summary

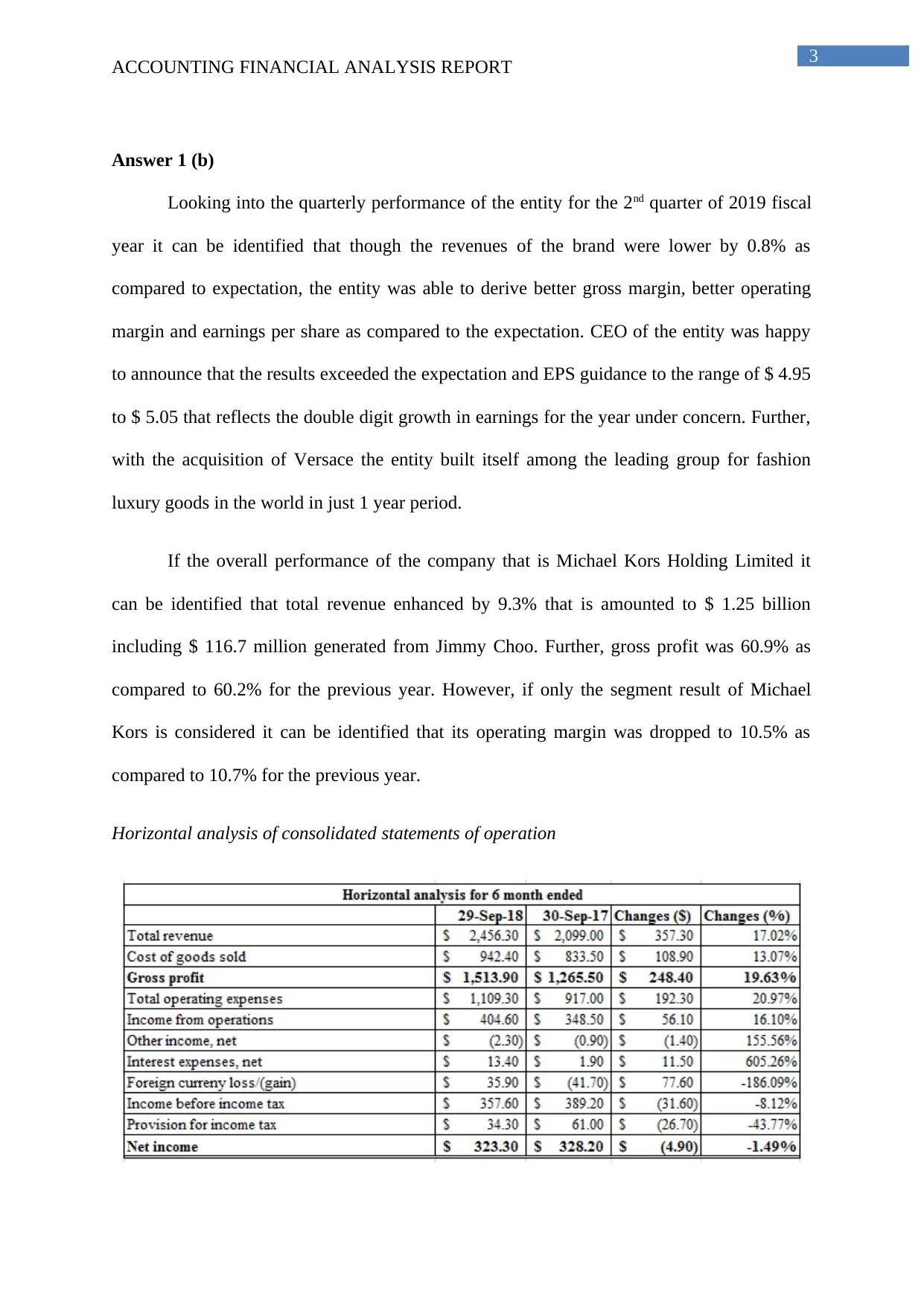

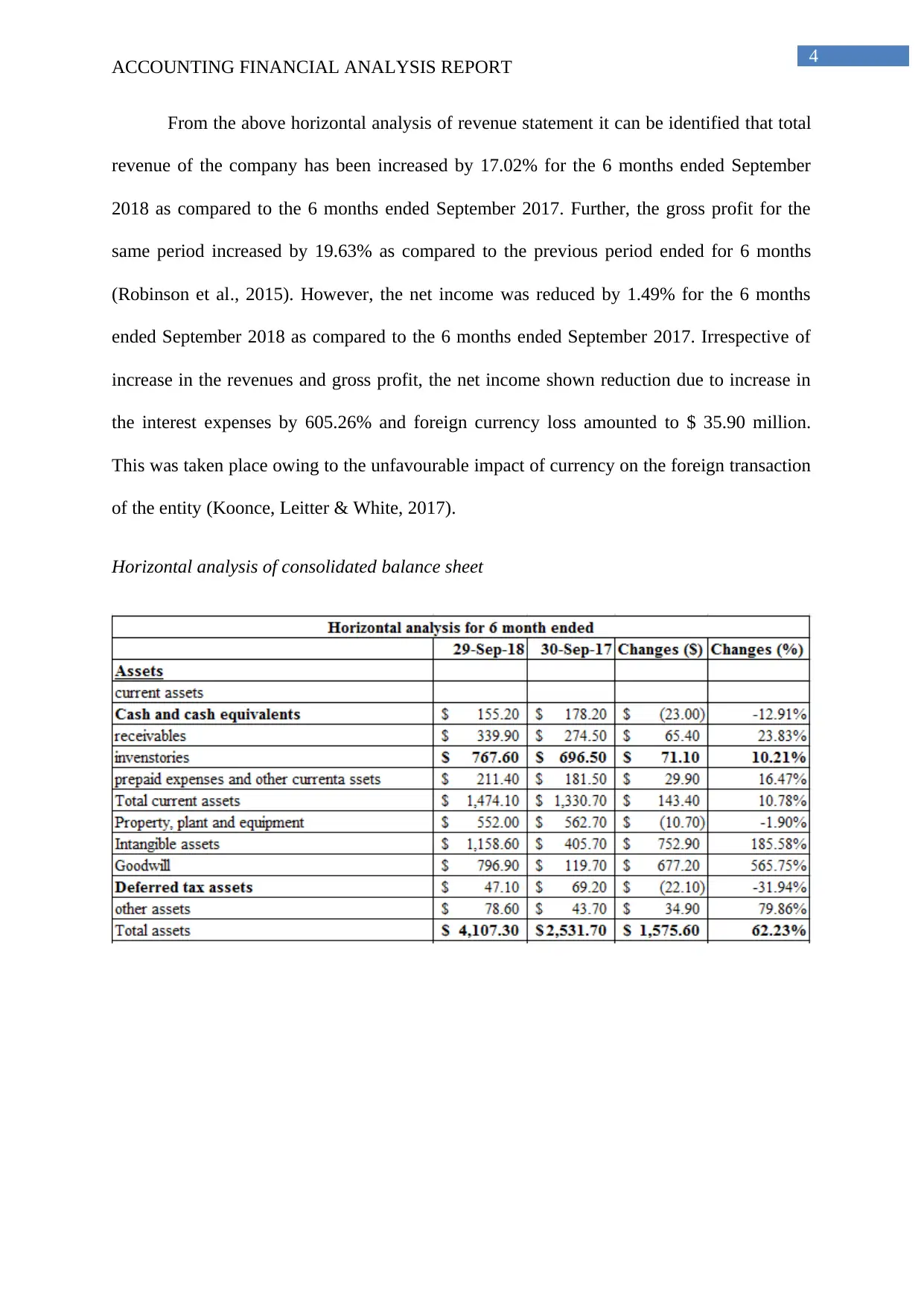

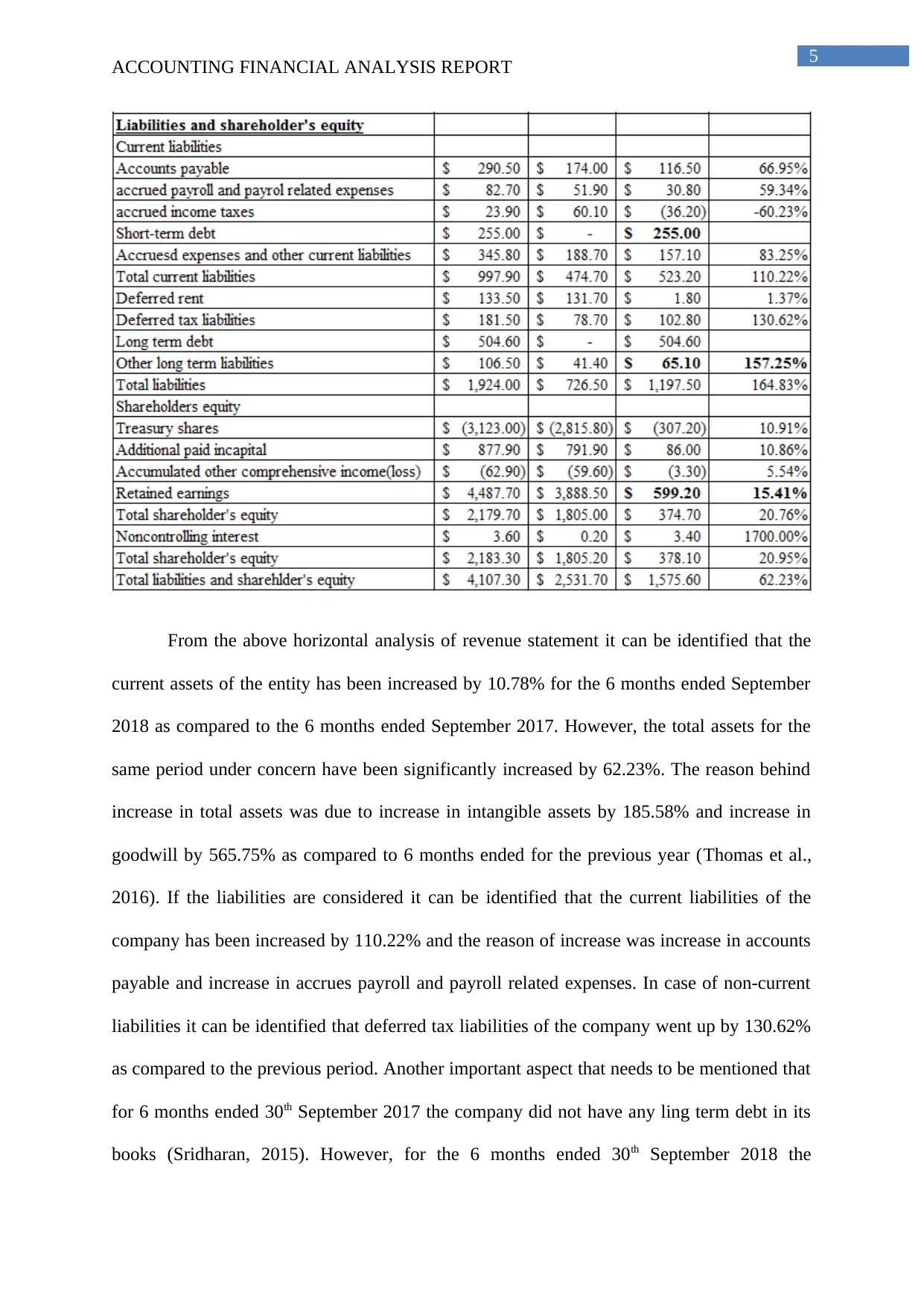

This report provides a comprehensive financial analysis of Michael Kors Holdings Limited, focusing on the company's performance in the second quarter of fiscal year 2019. The analysis begins with an overview of the company's financial highlights, including revenue, gross margin, operating margin, and earnings per share, comparing them to expectations and previous periods. It includes horizontal analyses of the consolidated statements of operations and balance sheets, examining trends in revenue, gross profit, net income, assets, liabilities, and shareholder's equity. The report identifies key stakeholders, such as shareholders, and highlights information relevant to them, including net income and earnings per share. It also assesses the financial statements attached to the press release, noting the precision of the figures and the use of materiality. The report further details the company's assets, shareholder's equity, and liabilities, including credit sales. Finally, it examines the company's risks, particularly those associated with the acquisition of Versace, and discusses the potential impacts on the company's financial position and earnings. The report is based on a press release and financial statements, offering a snapshot of the company's financial health and strategic decisions.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.