MICPA's Report on IASB ED/2017/4: Amendments to IAS 16 Analysis

VerifiedAdded on 2023/06/13

|3

|579

|246

Report

AI Summary

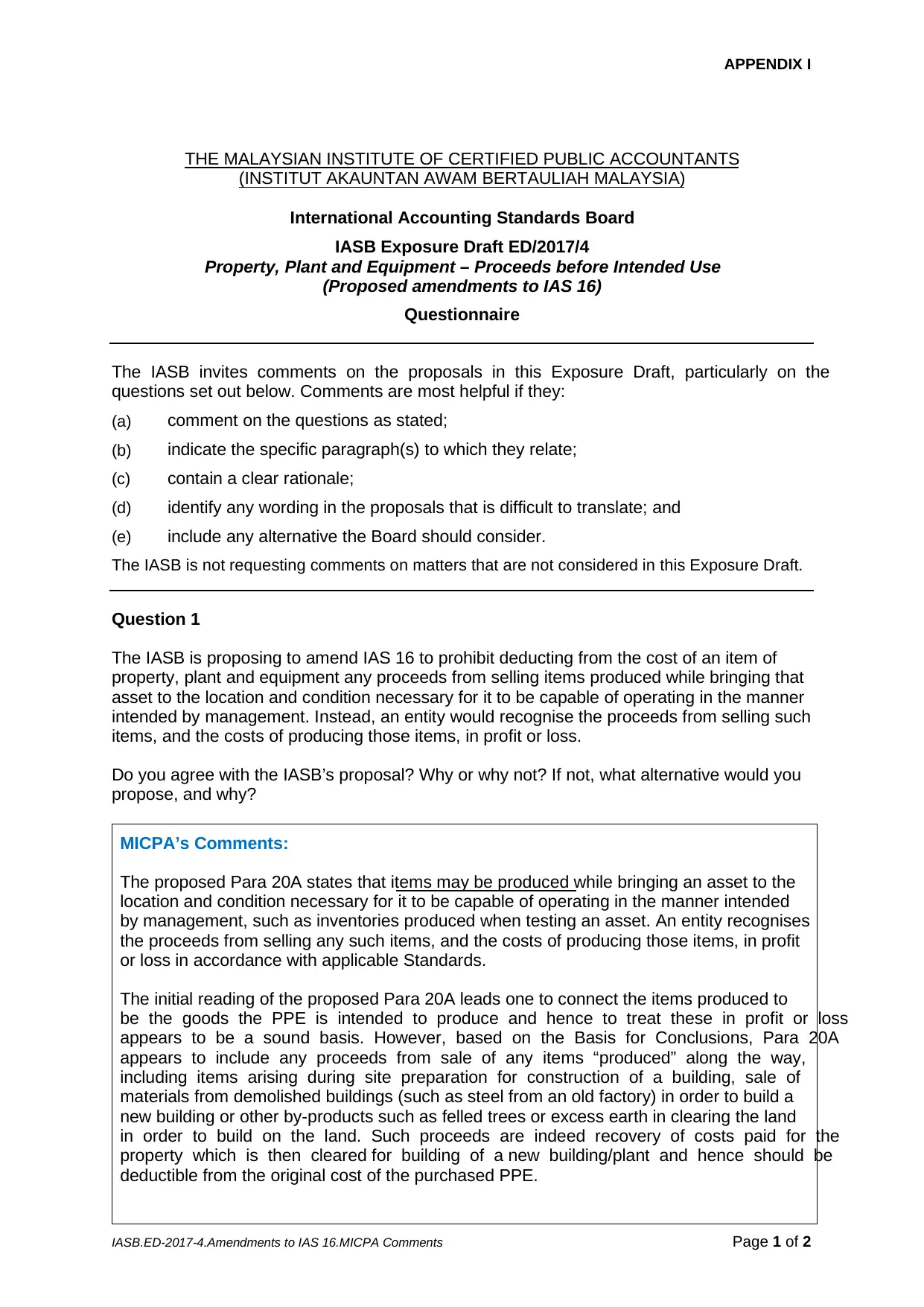

This report presents the Malaysian Institute of Certified Public Accountants' (MICPA) comments on the International Accounting Standards Board's (IASB) Exposure Draft ED/2017/4, which proposes amendments to IAS 16 concerning proceeds from selling items produced before an asset is ready for its intended use. MICPA generally agrees with the proposal to recognize these proceeds and related costs in profit or loss, but suggests clarifying that the amendment should not apply to proceeds from salvaged or similar items not produced in the ordinary course of business, such as materials from demolished buildings or excess earth from land clearing, as these represent a recovery of costs associated with the property's acquisition and preparation.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.