ACC00152: MicroNet Technology Distribution Channels Evaluation Report

VerifiedAdded on 2023/03/20

|5

|1269

|57

Report

AI Summary

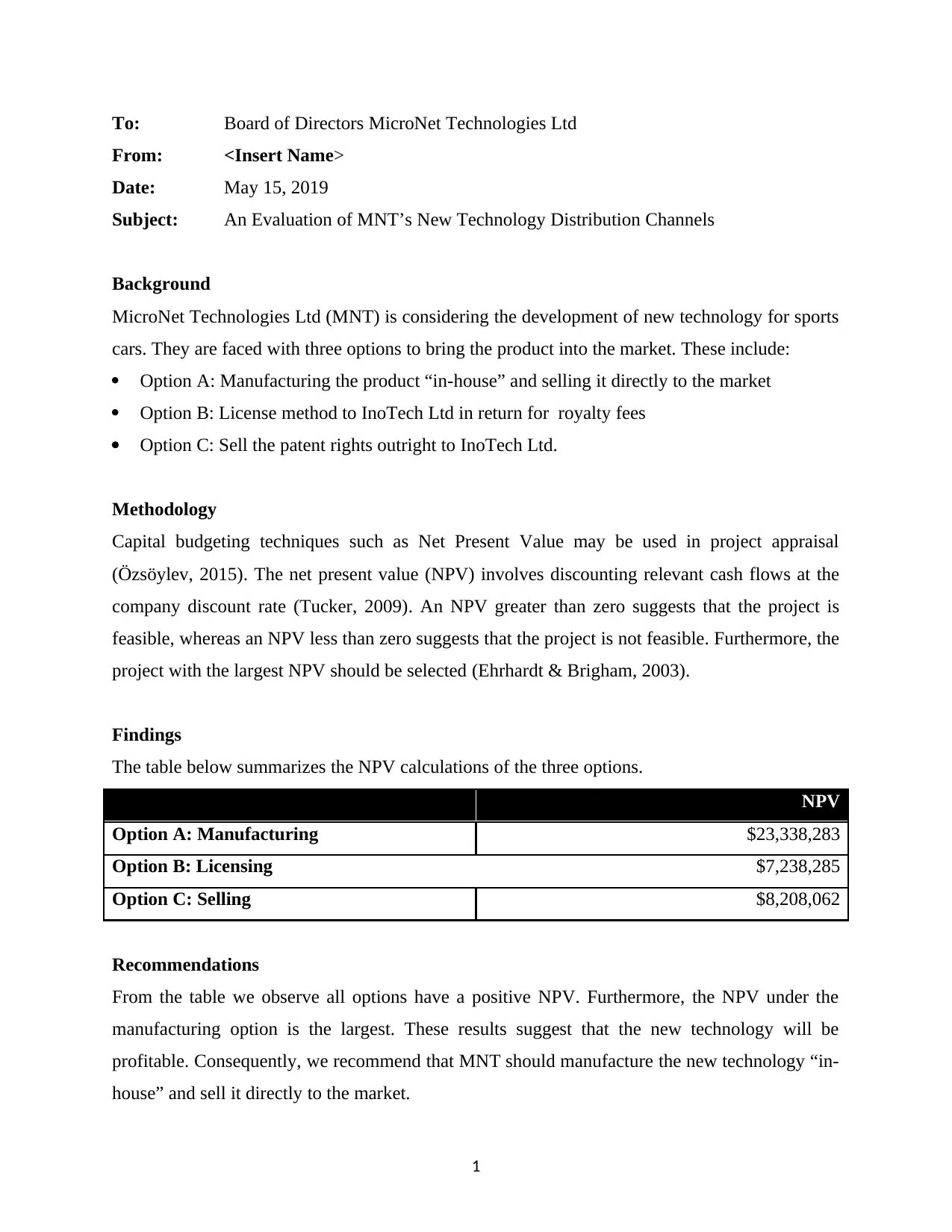

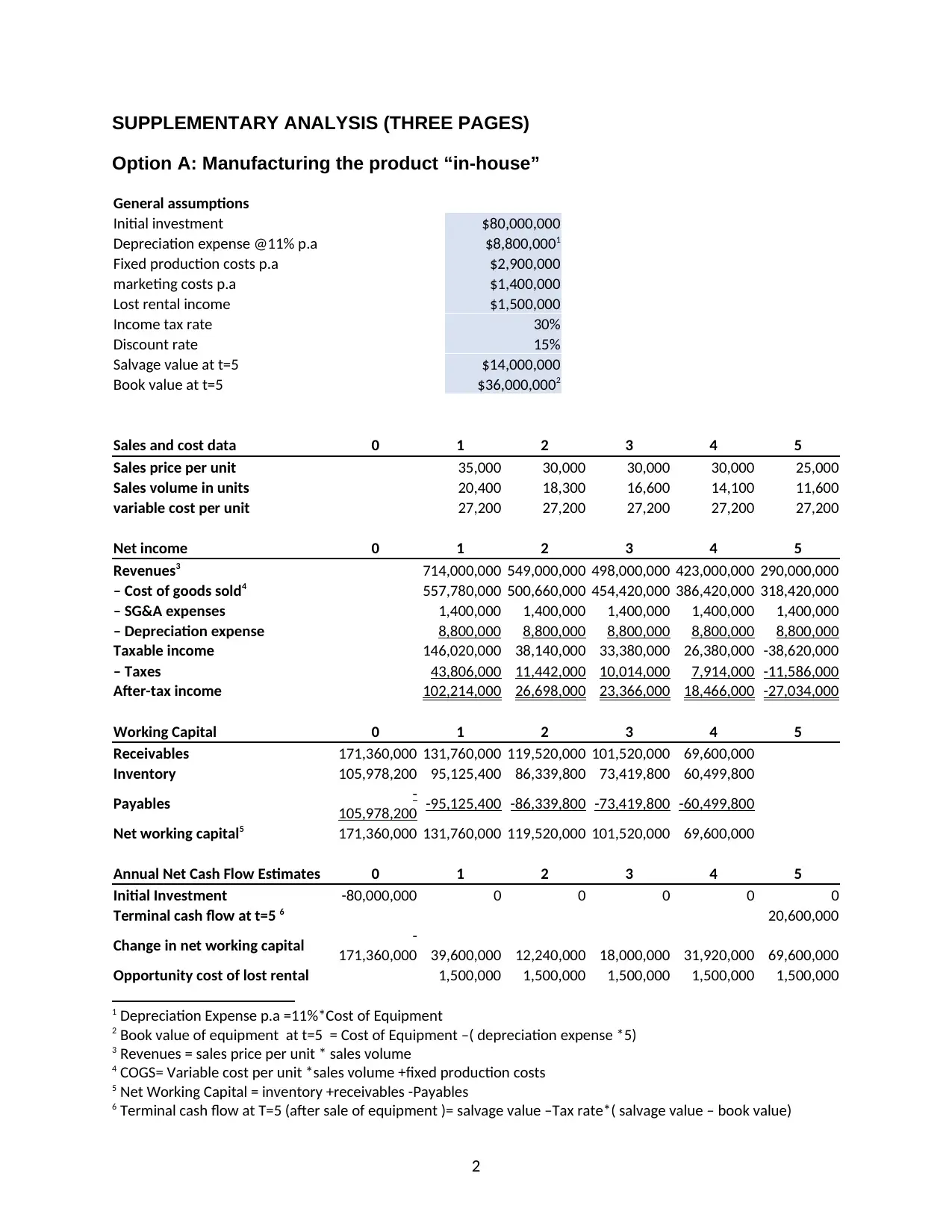

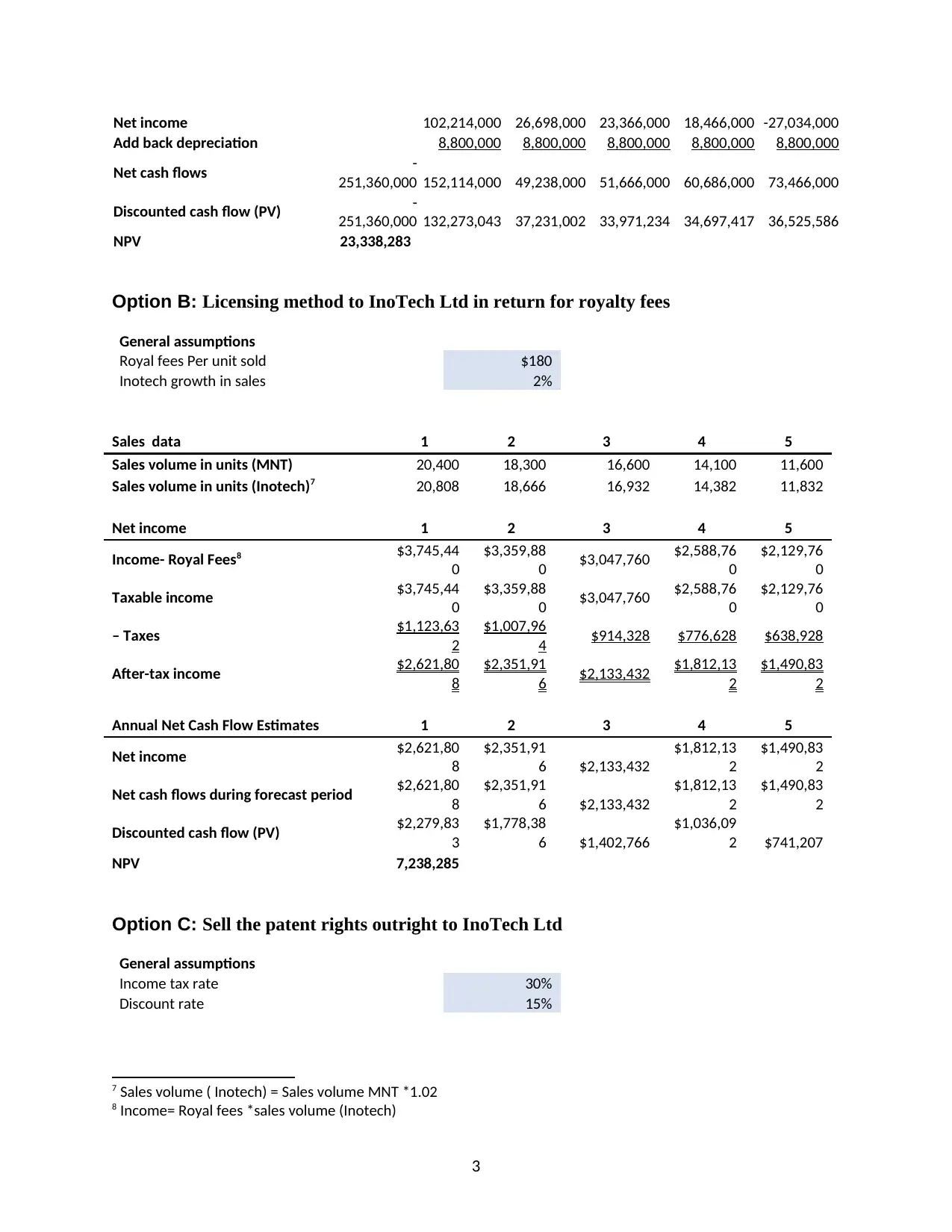

This report evaluates three technology distribution options for MicroNet Technologies Ltd (MNT): in-house manufacturing and direct sales (Option A), licensing to InoTech Ltd (Option B), and selling patent rights to InoTech Ltd (Option C). Using capital budgeting techniques, specifically Net Present Value (NPV), the report analyzes the financial viability of each option. The analysis includes detailed assumptions, sales and cost data, and cash flow estimates, along with supplementary analysis. The findings reveal that all three options have a positive NPV, with Option A (manufacturing) yielding the highest NPV. The report recommends that MNT manufacture the new technology in-house and sell it directly to the market. Furthermore, it suggests that while NPV is a valuable tool, MNT should also consider qualitative factors like competition and conduct sensitivity analysis to assess the impact of key assumptions on the forecasts, mitigating forecasting risks. References include sources on capital budgeting and factors affecting the cost of capital.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.