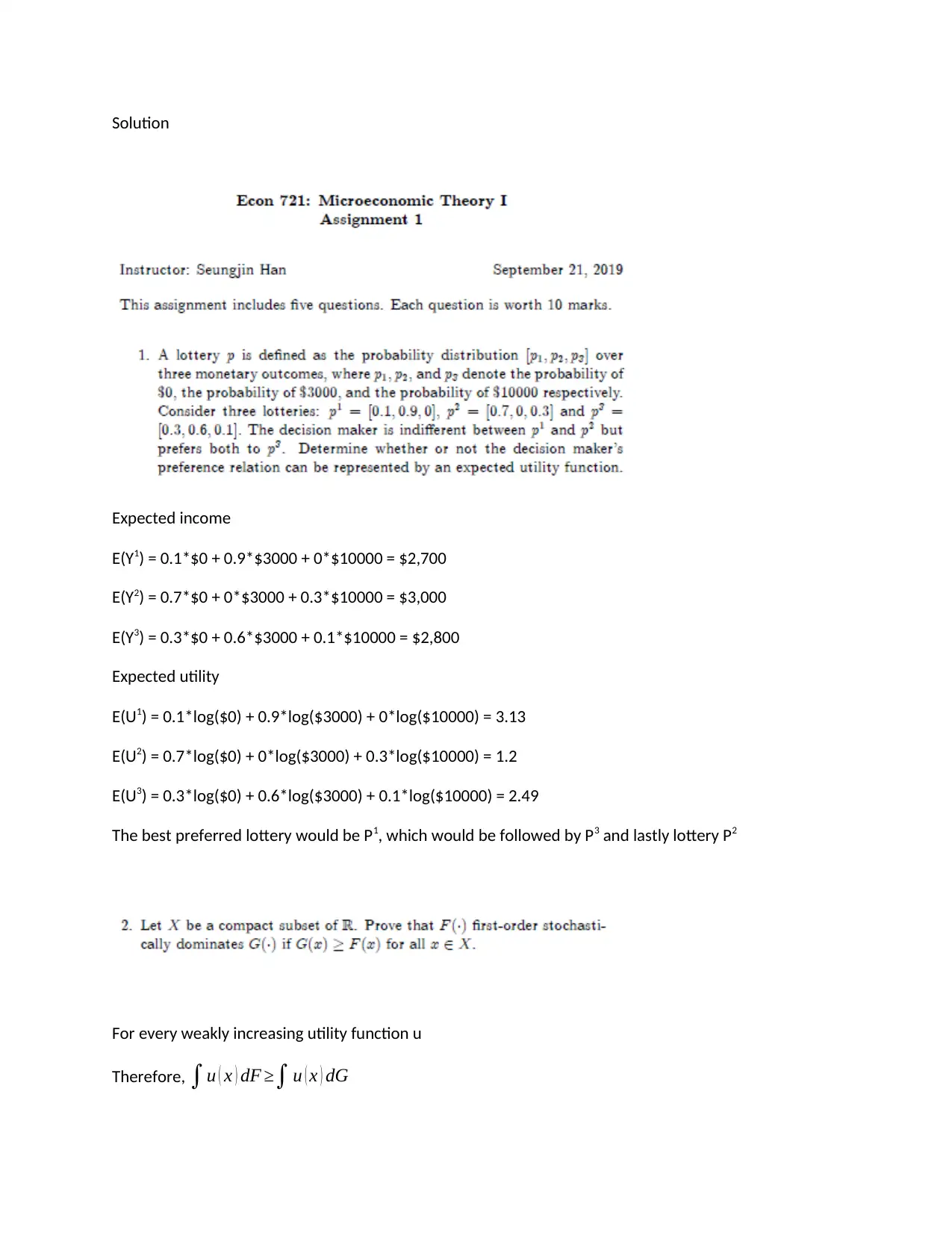

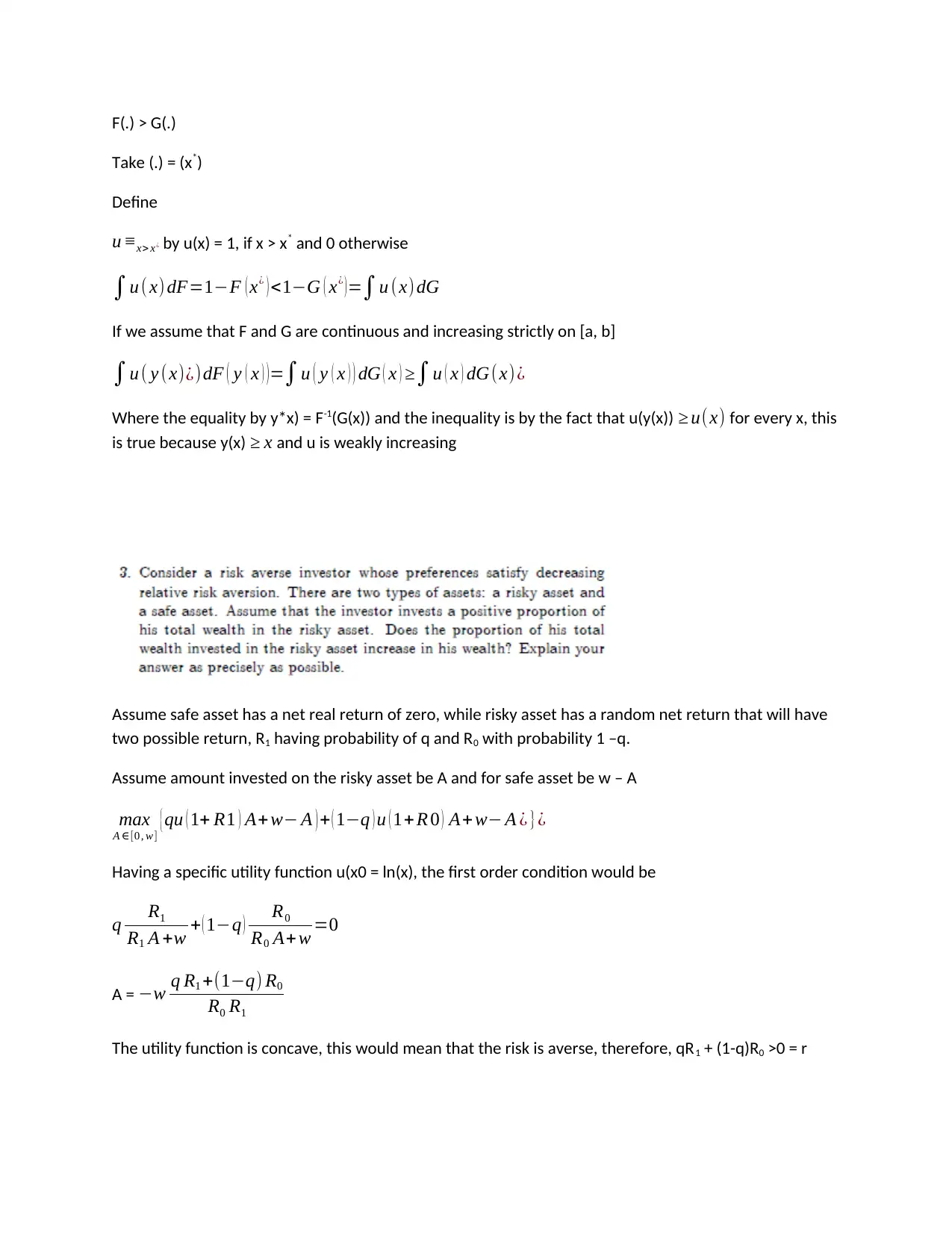

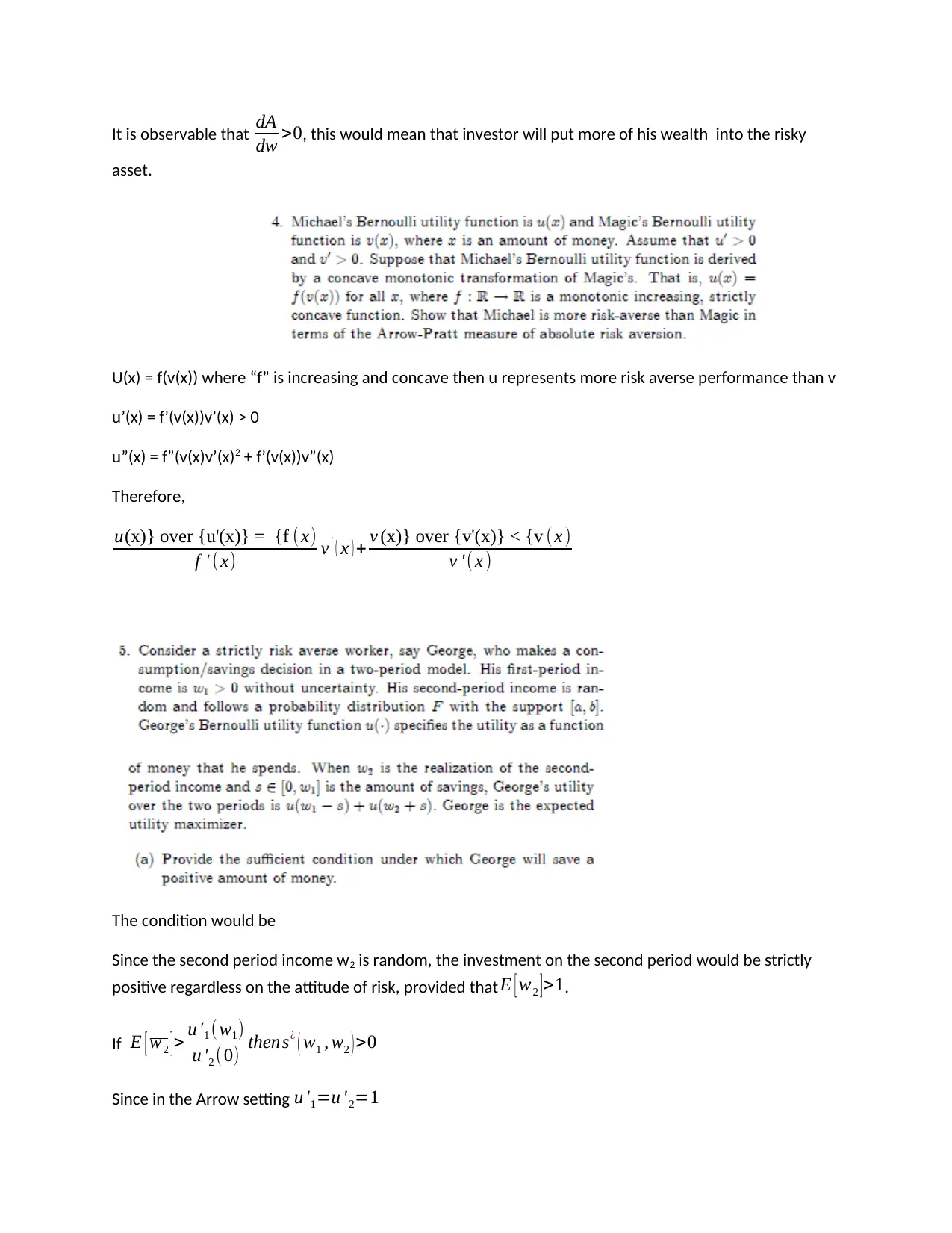

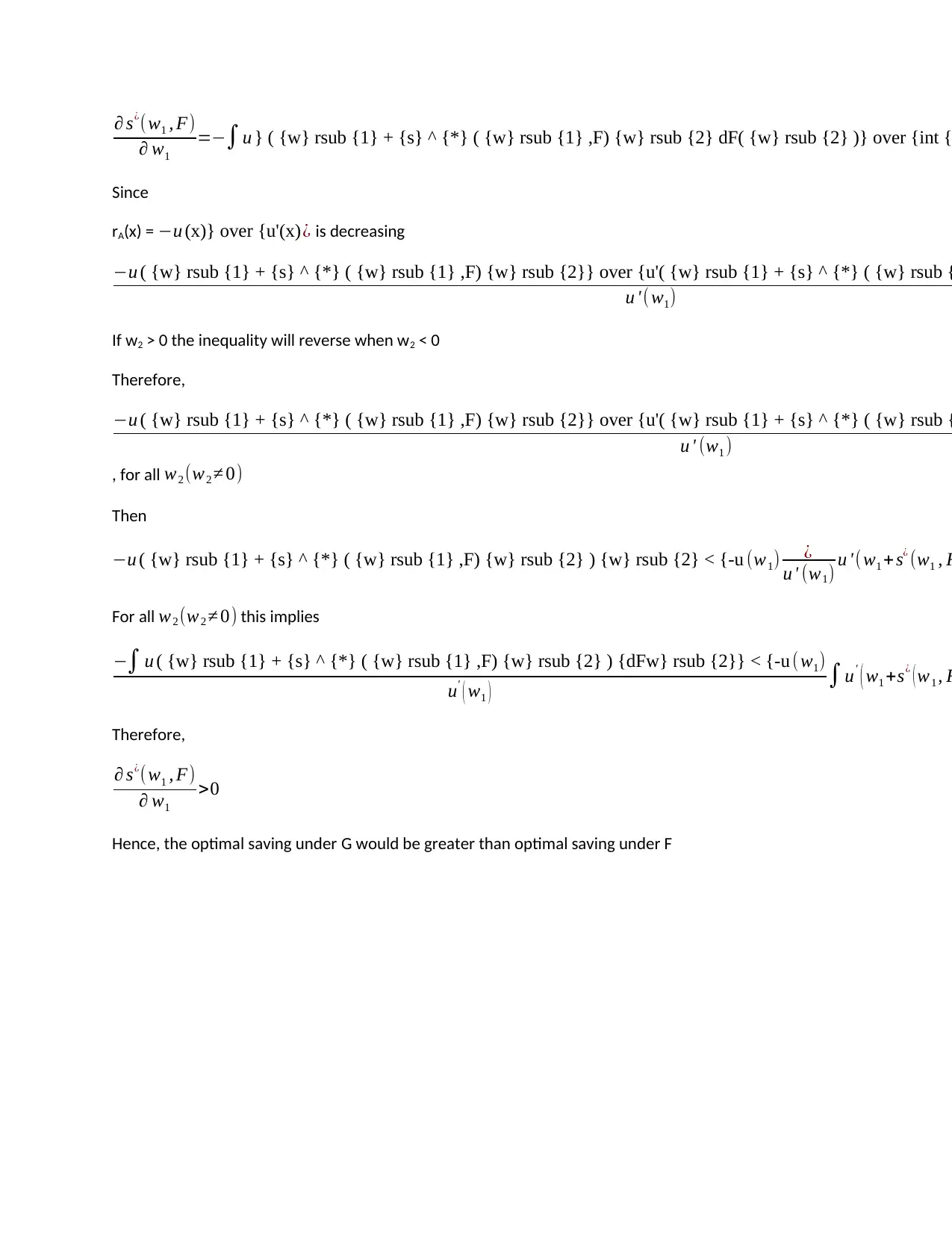

Econ 721, Microeconomic Theory I, Assignment 1: Uncertainty Problems

VerifiedAdded on 2022/10/14

|5

|644

|297

Homework Assignment

AI Summary

This document presents a detailed solution to Assignment 1 for Econ 721: Microeconomic Theory I. The solution addresses several key concepts in microeconomics, including expected utility, risk aversion, and portfolio choice under uncertainty. The assignment explores the preferences of a decision-maker across different lotteries and examines whether these preferences can be represented by an expected utility function. The solution demonstrates the application of stochastic dominance to compare probability distributions and analyzes the investment decisions of a risk-averse investor with decreasing relative risk aversion. Furthermore, the assignment delves into asset pricing and portfolio optimization, demonstrating the conditions under which an investor will allocate wealth into risky assets and the effects of changes in wealth on savings. The solution includes mathematical derivations and explanations to support the conclusions, providing a comprehensive understanding of the underlying economic principles.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.