Microeconomic Analysis Assignment: Economic Principles

VerifiedAdded on 2019/09/18

|13

|2708

|66

Homework Assignment

AI Summary

This assignment provides a detailed analysis of microeconomic concepts. It begins by examining the impact of tariffs on market equilibrium, including producer surplus and deadweight loss. The solution then explores different market structures, such as perfect competition, analyzing demand curves and the behavior of firms in both the short and long run. The assignment further delves into the concepts of opportunity costs and comparative advantage, using examples of international trade. It also examines closed and open economies, consumer surplus, and the effects of tariffs in an open economy. The analysis extends to monopoly, covering profit maximization, consumer surplus, and deadweight loss. The document continues by discussing monopolistic competition, highlighting its characteristics and efficiency compared to perfect competition. Finally, it examines oligopoly, including its features and the interdependence of firms. The document provides graphical representations and explanations throughout, offering a comprehensive understanding of the topics.

MICROECONOMIC ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Question 1:.................................................................................................................................3

Question 2:.................................................................................................................................4

Question 3:.................................................................................................................................4

Question 4:.................................................................................................................................6

Question 5:.................................................................................................................................6

Question 6:.................................................................................................................................7

Question 7:.................................................................................................................................9

Question 8:...............................................................................................................................10

Question 9:...............................................................................................................................11

Reference list............................................................................................................................12

Question 1:.................................................................................................................................3

Question 2:.................................................................................................................................4

Question 3:.................................................................................................................................4

Question 4:.................................................................................................................................6

Question 5:.................................................................................................................................6

Question 6:.................................................................................................................................7

Question 7:.................................................................................................................................9

Question 8:...............................................................................................................................10

Question 9:...............................................................................................................................11

Reference list............................................................................................................................12

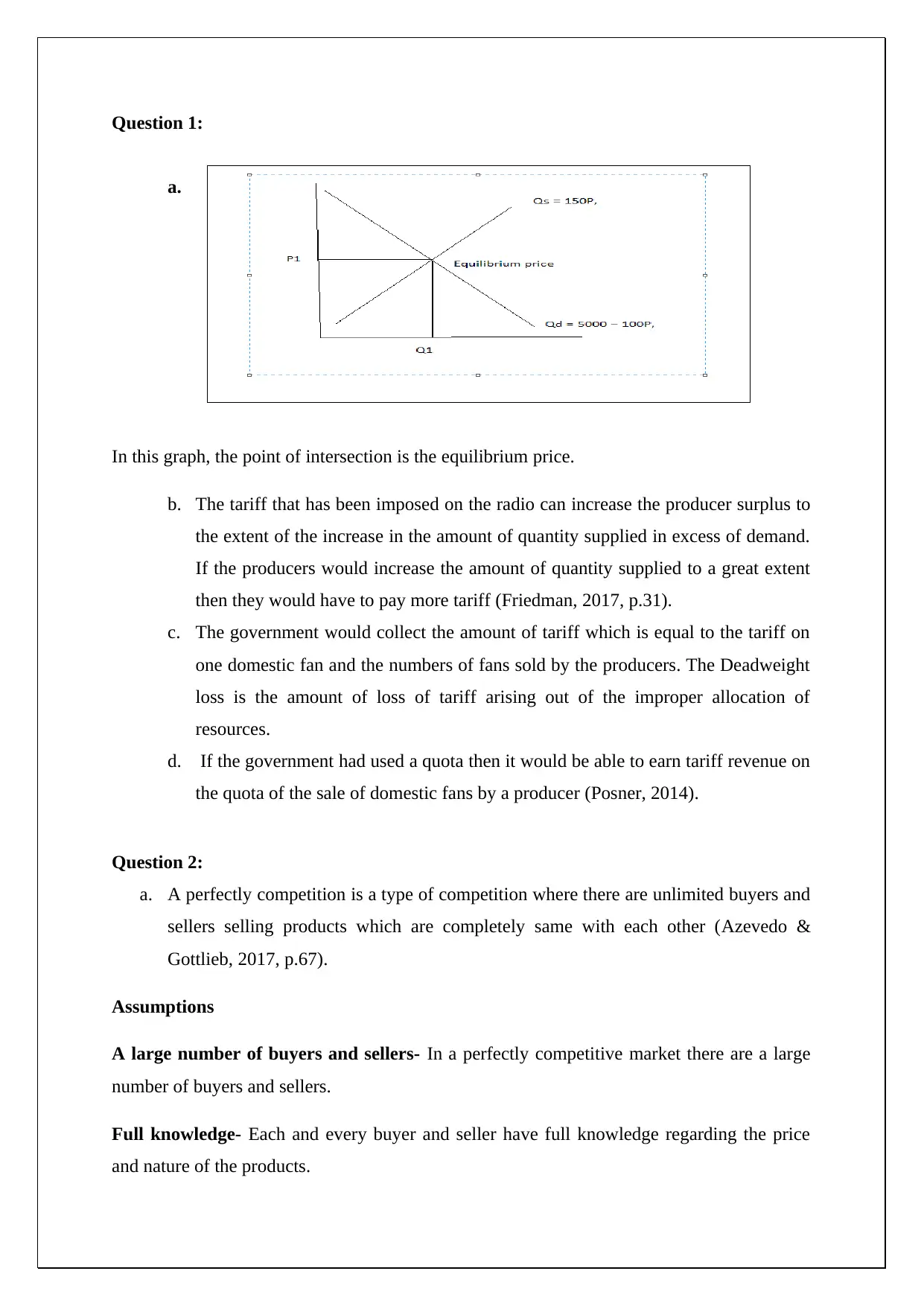

Question 1:

a.

In this graph, the point of intersection is the equilibrium price.

b. The tariff that has been imposed on the radio can increase the producer surplus to

the extent of the increase in the amount of quantity supplied in excess of demand.

If the producers would increase the amount of quantity supplied to a great extent

then they would have to pay more tariff (Friedman, 2017, p.31).

c. The government would collect the amount of tariff which is equal to the tariff on

one domestic fan and the numbers of fans sold by the producers. The Deadweight

loss is the amount of loss of tariff arising out of the improper allocation of

resources.

d. If the government had used a quota then it would be able to earn tariff revenue on

the quota of the sale of domestic fans by a producer (Posner, 2014).

Question 2:

a. A perfectly competition is a type of competition where there are unlimited buyers and

sellers selling products which are completely same with each other (Azevedo &

Gottlieb, 2017, p.67).

Assumptions

A large number of buyers and sellers- In a perfectly competitive market there are a large

number of buyers and sellers.

Full knowledge- Each and every buyer and seller have full knowledge regarding the price

and nature of the products.

a.

In this graph, the point of intersection is the equilibrium price.

b. The tariff that has been imposed on the radio can increase the producer surplus to

the extent of the increase in the amount of quantity supplied in excess of demand.

If the producers would increase the amount of quantity supplied to a great extent

then they would have to pay more tariff (Friedman, 2017, p.31).

c. The government would collect the amount of tariff which is equal to the tariff on

one domestic fan and the numbers of fans sold by the producers. The Deadweight

loss is the amount of loss of tariff arising out of the improper allocation of

resources.

d. If the government had used a quota then it would be able to earn tariff revenue on

the quota of the sale of domestic fans by a producer (Posner, 2014).

Question 2:

a. A perfectly competition is a type of competition where there are unlimited buyers and

sellers selling products which are completely same with each other (Azevedo &

Gottlieb, 2017, p.67).

Assumptions

A large number of buyers and sellers- In a perfectly competitive market there are a large

number of buyers and sellers.

Full knowledge- Each and every buyer and seller have full knowledge regarding the price

and nature of the products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fully homogenous products- Products sold by all the firms are fully same.

Free entry and exit- Existing firms can leave the industry and new firms can join the

industry at their own will.

b. Demand curve in the perfectly competitive market is fully horizontal or perfectly

elastic because the products are all same. Besides, buyers have full information

(Kirzner, 2015). Suppose a seller increases the price of his product slightly the buyers

would immediately move to other sellers. This shows that the firms are price takers.

c. In perfect competition, the demand curve of an individual firm is perfectly horizontal.

Irrespective of the quantity produced by the firm in a perfectly competitive market,

the price is the same, so the price is equal to MR.

Question 3:

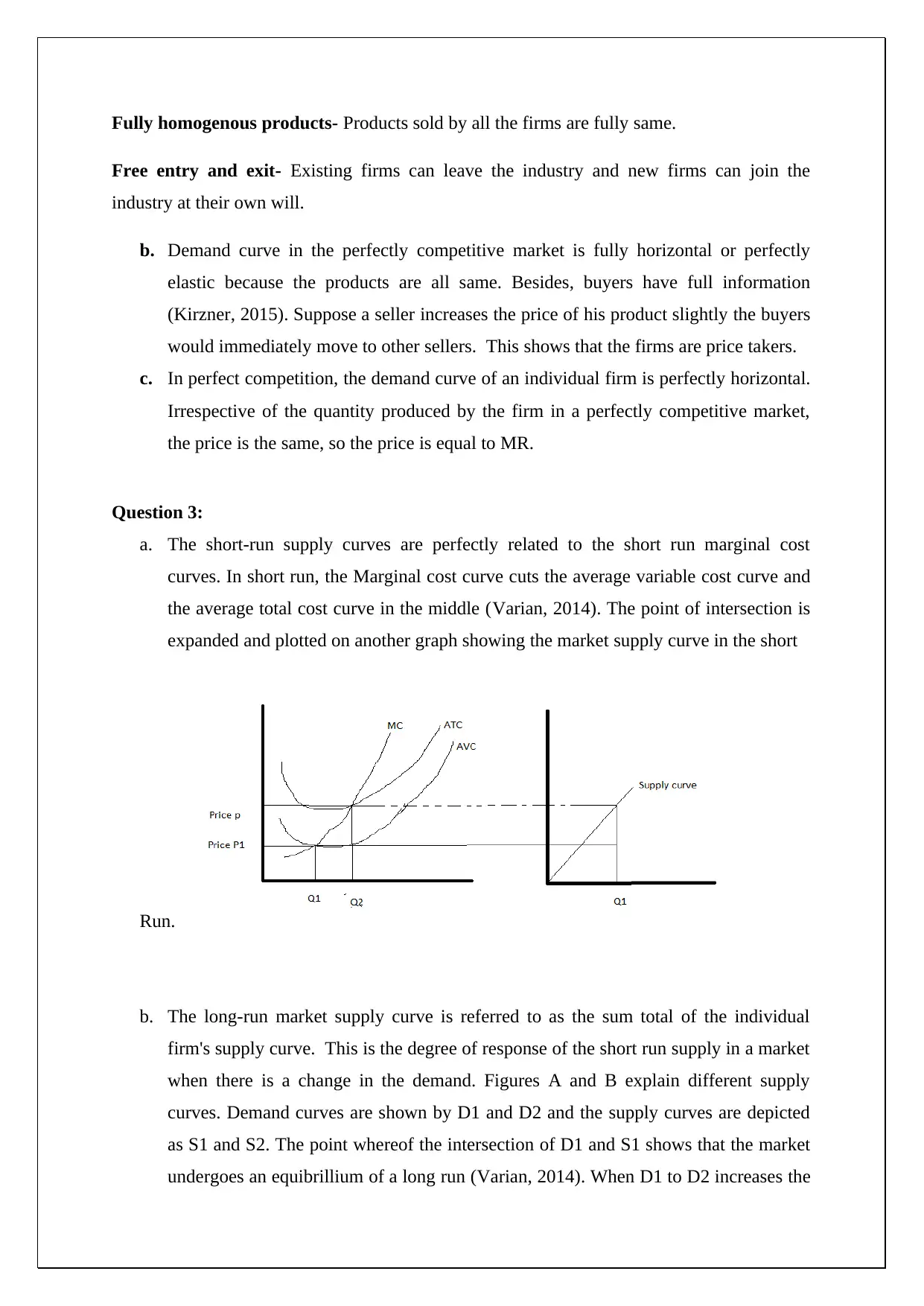

a. The short-run supply curves are perfectly related to the short run marginal cost

curves. In short run, the Marginal cost curve cuts the average variable cost curve and

the average total cost curve in the middle (Varian, 2014). The point of intersection is

expanded and plotted on another graph showing the market supply curve in the short

Run.

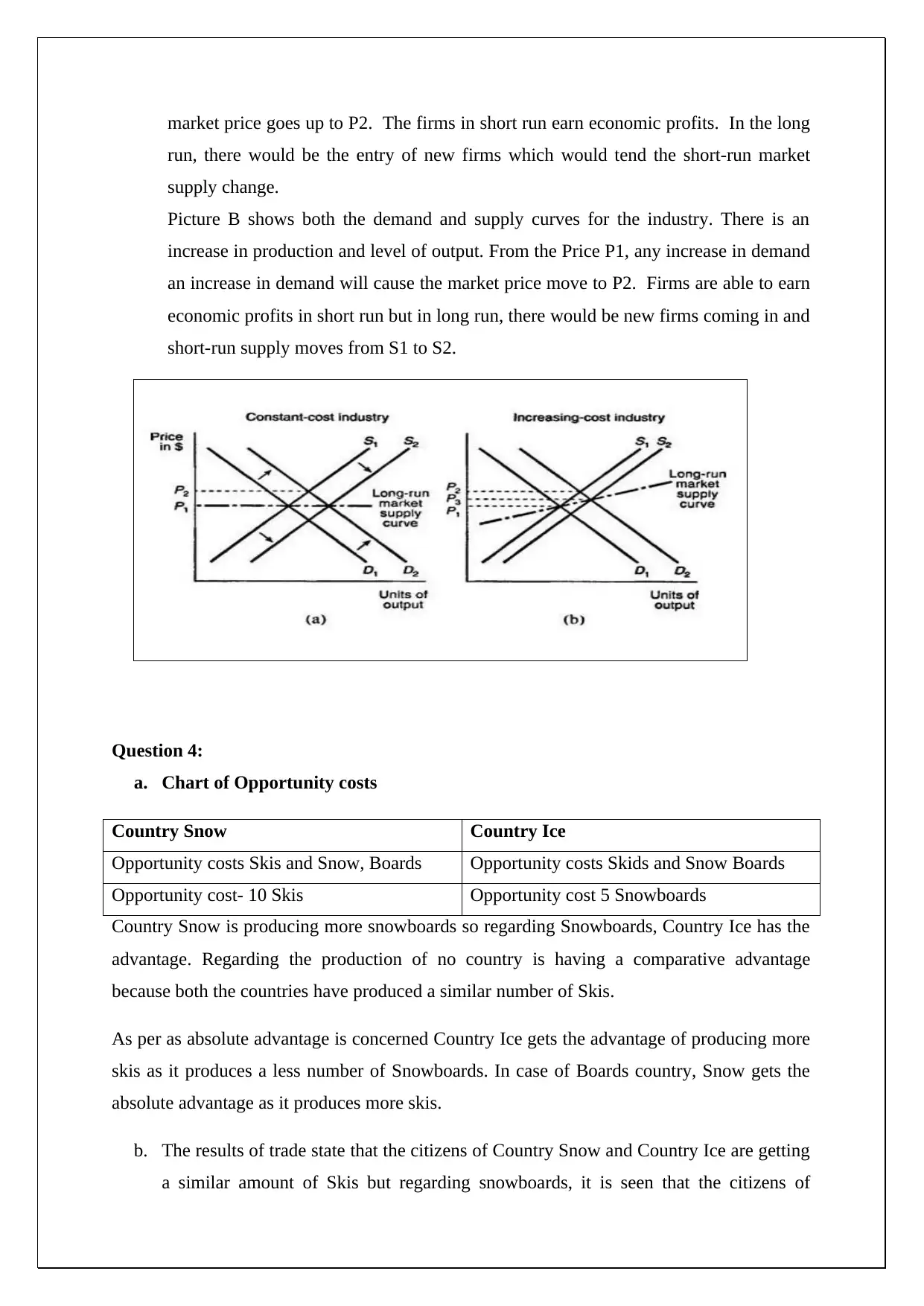

b. The long-run market supply curve is referred to as the sum total of the individual

firm's supply curve. This is the degree of response of the short run supply in a market

when there is a change in the demand. Figures A and B explain different supply

curves. Demand curves are shown by D1 and D2 and the supply curves are depicted

as S1 and S2. The point whereof the intersection of D1 and S1 shows that the market

undergoes an equibrillium of a long run (Varian, 2014). When D1 to D2 increases the

Free entry and exit- Existing firms can leave the industry and new firms can join the

industry at their own will.

b. Demand curve in the perfectly competitive market is fully horizontal or perfectly

elastic because the products are all same. Besides, buyers have full information

(Kirzner, 2015). Suppose a seller increases the price of his product slightly the buyers

would immediately move to other sellers. This shows that the firms are price takers.

c. In perfect competition, the demand curve of an individual firm is perfectly horizontal.

Irrespective of the quantity produced by the firm in a perfectly competitive market,

the price is the same, so the price is equal to MR.

Question 3:

a. The short-run supply curves are perfectly related to the short run marginal cost

curves. In short run, the Marginal cost curve cuts the average variable cost curve and

the average total cost curve in the middle (Varian, 2014). The point of intersection is

expanded and plotted on another graph showing the market supply curve in the short

Run.

b. The long-run market supply curve is referred to as the sum total of the individual

firm's supply curve. This is the degree of response of the short run supply in a market

when there is a change in the demand. Figures A and B explain different supply

curves. Demand curves are shown by D1 and D2 and the supply curves are depicted

as S1 and S2. The point whereof the intersection of D1 and S1 shows that the market

undergoes an equibrillium of a long run (Varian, 2014). When D1 to D2 increases the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

market price goes up to P2. The firms in short run earn economic profits. In the long

run, there would be the entry of new firms which would tend the short-run market

supply change.

Picture B shows both the demand and supply curves for the industry. There is an

increase in production and level of output. From the Price P1, any increase in demand

an increase in demand will cause the market price move to P2. Firms are able to earn

economic profits in short run but in long run, there would be new firms coming in and

short-run supply moves from S1 to S2.

Question 4:

a. Chart of Opportunity costs

Country Snow Country Ice

Opportunity costs Skis and Snow, Boards Opportunity costs Skids and Snow Boards

Opportunity cost- 10 Skis Opportunity cost 5 Snowboards

Country Snow is producing more snowboards so regarding Snowboards, Country Ice has the

advantage. Regarding the production of no country is having a comparative advantage

because both the countries have produced a similar number of Skis.

As per as absolute advantage is concerned Country Ice gets the advantage of producing more

skis as it produces a less number of Snowboards. In case of Boards country, Snow gets the

absolute advantage as it produces more skis.

b. The results of trade state that the citizens of Country Snow and Country Ice are getting

a similar amount of Skis but regarding snowboards, it is seen that the citizens of

run, there would be the entry of new firms which would tend the short-run market

supply change.

Picture B shows both the demand and supply curves for the industry. There is an

increase in production and level of output. From the Price P1, any increase in demand

an increase in demand will cause the market price move to P2. Firms are able to earn

economic profits in short run but in long run, there would be new firms coming in and

short-run supply moves from S1 to S2.

Question 4:

a. Chart of Opportunity costs

Country Snow Country Ice

Opportunity costs Skis and Snow, Boards Opportunity costs Skids and Snow Boards

Opportunity cost- 10 Skis Opportunity cost 5 Snowboards

Country Snow is producing more snowboards so regarding Snowboards, Country Ice has the

advantage. Regarding the production of no country is having a comparative advantage

because both the countries have produced a similar number of Skis.

As per as absolute advantage is concerned Country Ice gets the advantage of producing more

skis as it produces a less number of Snowboards. In case of Boards country, Snow gets the

absolute advantage as it produces more skis.

b. The results of trade state that the citizens of Country Snow and Country Ice are getting

a similar amount of Skis but regarding snowboards, it is seen that the citizens of

country Ice are getting less of snowboards (Shapiro, 2016). This is because the number

of snowboards produced is more in country Snow and less in country Ice (Kurzban et

al. 2013, p.661).

Question 5:

a. In case of a closed economy, there is no trade conducted with the other countries. So

if the CCC land remains a closed economy then the equilibrium price would be

considered by the price determined by the amount of quantity demanded by domestic

customers and the amount of coffee supplied by CCC land within the domestic

territory (Posner, 2014).

b. If the status of CCC land is changed from a closed economy to an open economy then

the CCC land would import and export coffee because in case of an open economy

trade can be conducted with outside economies. Hence CCC land can import and

export coffee.

c. When CCC land is in a closed economy the consumer surplus is the difference

between the amount which the domestic consumers decide to pay and the actual

amount that the domestic consumers have paid. When CCC land is in an open

economy the consumer surplus is the difference between the amount which the

domestic and foreign consumers decide to pay and the actual amount that the

domestic and foreign consumers have paid. No, domestic consumers would not be in

favour in opening the trade market because this would increase the supply and if

supply increases then a price of coffee of CCC land would also increase (Posner,

2014).

d. The tariff needs to be as big as the number of imports.

e. In this case, the amount of tariff charged should be equal to the amount of reduction

of imports because the reduction in imports can reduce foreign revenue. In such a

case the government of CCC land will have to raise tariff similar to that extent in

order to reach their revenue maximisation goal.

f. The amount of money received from tariff which has not been properly allocated to

the coffee business is the deadweight loss.

of snowboards produced is more in country Snow and less in country Ice (Kurzban et

al. 2013, p.661).

Question 5:

a. In case of a closed economy, there is no trade conducted with the other countries. So

if the CCC land remains a closed economy then the equilibrium price would be

considered by the price determined by the amount of quantity demanded by domestic

customers and the amount of coffee supplied by CCC land within the domestic

territory (Posner, 2014).

b. If the status of CCC land is changed from a closed economy to an open economy then

the CCC land would import and export coffee because in case of an open economy

trade can be conducted with outside economies. Hence CCC land can import and

export coffee.

c. When CCC land is in a closed economy the consumer surplus is the difference

between the amount which the domestic consumers decide to pay and the actual

amount that the domestic consumers have paid. When CCC land is in an open

economy the consumer surplus is the difference between the amount which the

domestic and foreign consumers decide to pay and the actual amount that the

domestic and foreign consumers have paid. No, domestic consumers would not be in

favour in opening the trade market because this would increase the supply and if

supply increases then a price of coffee of CCC land would also increase (Posner,

2014).

d. The tariff needs to be as big as the number of imports.

e. In this case, the amount of tariff charged should be equal to the amount of reduction

of imports because the reduction in imports can reduce foreign revenue. In such a

case the government of CCC land will have to raise tariff similar to that extent in

order to reach their revenue maximisation goal.

f. The amount of money received from tariff which has not been properly allocated to

the coffee business is the deadweight loss.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

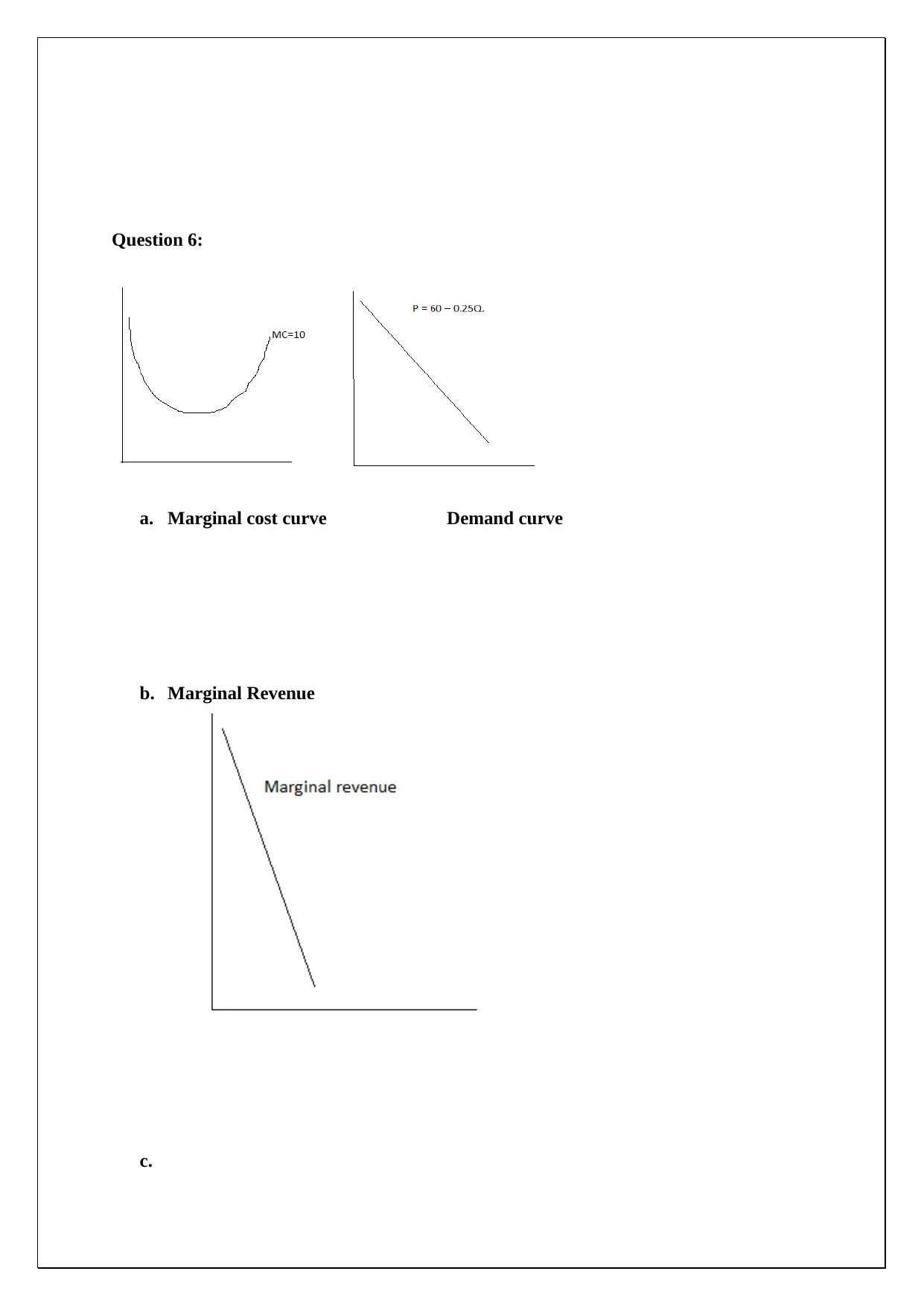

Question 6:

a. Marginal cost curve Demand curve

b. Marginal Revenue

c.

a. Marginal cost curve Demand curve

b. Marginal Revenue

c.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

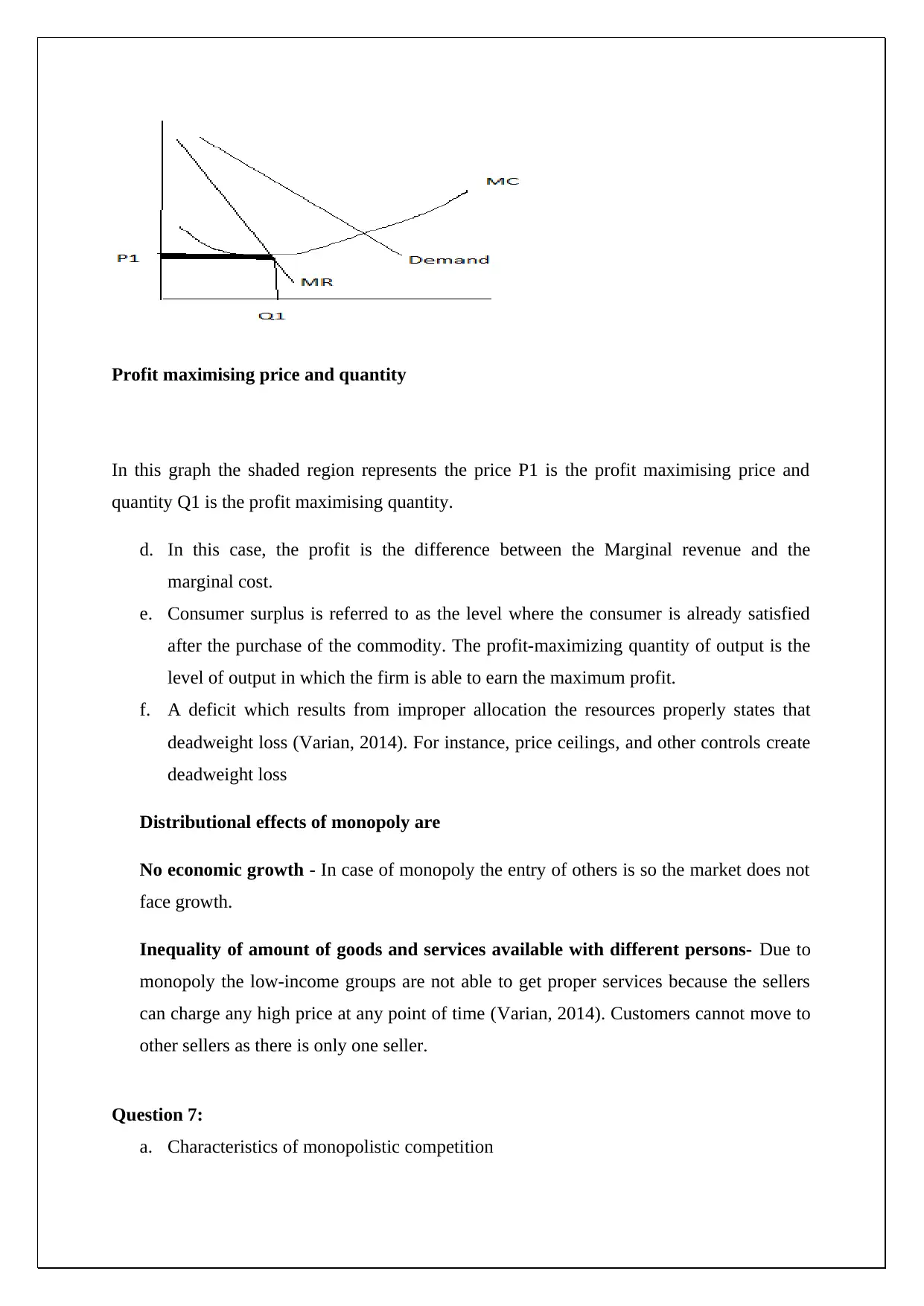

Profit maximising price and quantity

In this graph the shaded region represents the price P1 is the profit maximising price and

quantity Q1 is the profit maximising quantity.

d. In this case, the profit is the difference between the Marginal revenue and the

marginal cost.

e. Consumer surplus is referred to as the level where the consumer is already satisfied

after the purchase of the commodity. The profit-maximizing quantity of output is the

level of output in which the firm is able to earn the maximum profit.

f. A deficit which results from improper allocation the resources properly states that

deadweight loss (Varian, 2014). For instance, price ceilings, and other controls create

deadweight loss

Distributional effects of monopoly are

No economic growth - In case of monopoly the entry of others is so the market does not

face growth.

Inequality of amount of goods and services available with different persons- Due to

monopoly the low-income groups are not able to get proper services because the sellers

can charge any high price at any point of time (Varian, 2014). Customers cannot move to

other sellers as there is only one seller.

Question 7:

a. Characteristics of monopolistic competition

In this graph the shaded region represents the price P1 is the profit maximising price and

quantity Q1 is the profit maximising quantity.

d. In this case, the profit is the difference between the Marginal revenue and the

marginal cost.

e. Consumer surplus is referred to as the level where the consumer is already satisfied

after the purchase of the commodity. The profit-maximizing quantity of output is the

level of output in which the firm is able to earn the maximum profit.

f. A deficit which results from improper allocation the resources properly states that

deadweight loss (Varian, 2014). For instance, price ceilings, and other controls create

deadweight loss

Distributional effects of monopoly are

No economic growth - In case of monopoly the entry of others is so the market does not

face growth.

Inequality of amount of goods and services available with different persons- Due to

monopoly the low-income groups are not able to get proper services because the sellers

can charge any high price at any point of time (Varian, 2014). Customers cannot move to

other sellers as there is only one seller.

Question 7:

a. Characteristics of monopolistic competition

Numerous buyers and sellers- In case of Monopolistic competition there are

a large number of buyers and sellers. The firms in the industry have the power

to control their price and their output levels.

Highly distinguishable products- Products that are sold by the firms in the

monopolistic market are different but they are close substitutes for each other

(Kirzner, 2015). The products may have slight differences in terms of colour,

design but they are the same.

No barriers regarding entry and exit- In case of the monopolistic market

there are any barriers regarding entry and exit.

Huge selling costs- In case of monopolistic competition, the firms sell the

huge amount of costs on advertisements (Kirzner, 2015).

Actual knowledge not available- Buyers and the seller's do not have full

knowledge of the products. This is because there are a large number of

substitutes.

Negatively sloping demand curve- The demand curve of a perfectly elastic

market is negatively sloping.

b. Firms in monopolistic competition competitors with price and non-price policy.

Sometimes they try to decrease their price and sell their products in order to compete

with other firms (Kirzner, 2015). On the other hand, they also adopt non-price

policies which include giving guarantees and assured gifts on purchases.

c. In the perfectly competitive market, the firms have less efficiency because they

cannot change their price and earn profits which are possible in case of monopolistic

competition.

In terms of efficiency the monopolistic market is more profit because they can reduce

their price and get a large amount of sale whereas in perfect competition they are not

able to earn huge abnormal profits or excess capacity profits in the long run by

reducing price and selling in huge amount because all the products are fully same

(Qadir et al. 2014, p.282). On the other hand in case of perfect competition, the firms

are price takers. Price remains the same irrespective of the level of output or

production which does not occur in case of monopolistic competition.

a large number of buyers and sellers. The firms in the industry have the power

to control their price and their output levels.

Highly distinguishable products- Products that are sold by the firms in the

monopolistic market are different but they are close substitutes for each other

(Kirzner, 2015). The products may have slight differences in terms of colour,

design but they are the same.

No barriers regarding entry and exit- In case of the monopolistic market

there are any barriers regarding entry and exit.

Huge selling costs- In case of monopolistic competition, the firms sell the

huge amount of costs on advertisements (Kirzner, 2015).

Actual knowledge not available- Buyers and the seller's do not have full

knowledge of the products. This is because there are a large number of

substitutes.

Negatively sloping demand curve- The demand curve of a perfectly elastic

market is negatively sloping.

b. Firms in monopolistic competition competitors with price and non-price policy.

Sometimes they try to decrease their price and sell their products in order to compete

with other firms (Kirzner, 2015). On the other hand, they also adopt non-price

policies which include giving guarantees and assured gifts on purchases.

c. In the perfectly competitive market, the firms have less efficiency because they

cannot change their price and earn profits which are possible in case of monopolistic

competition.

In terms of efficiency the monopolistic market is more profit because they can reduce

their price and get a large amount of sale whereas in perfect competition they are not

able to earn huge abnormal profits or excess capacity profits in the long run by

reducing price and selling in huge amount because all the products are fully same

(Qadir et al. 2014, p.282). On the other hand in case of perfect competition, the firms

are price takers. Price remains the same irrespective of the level of output or

production which does not occur in case of monopolistic competition.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

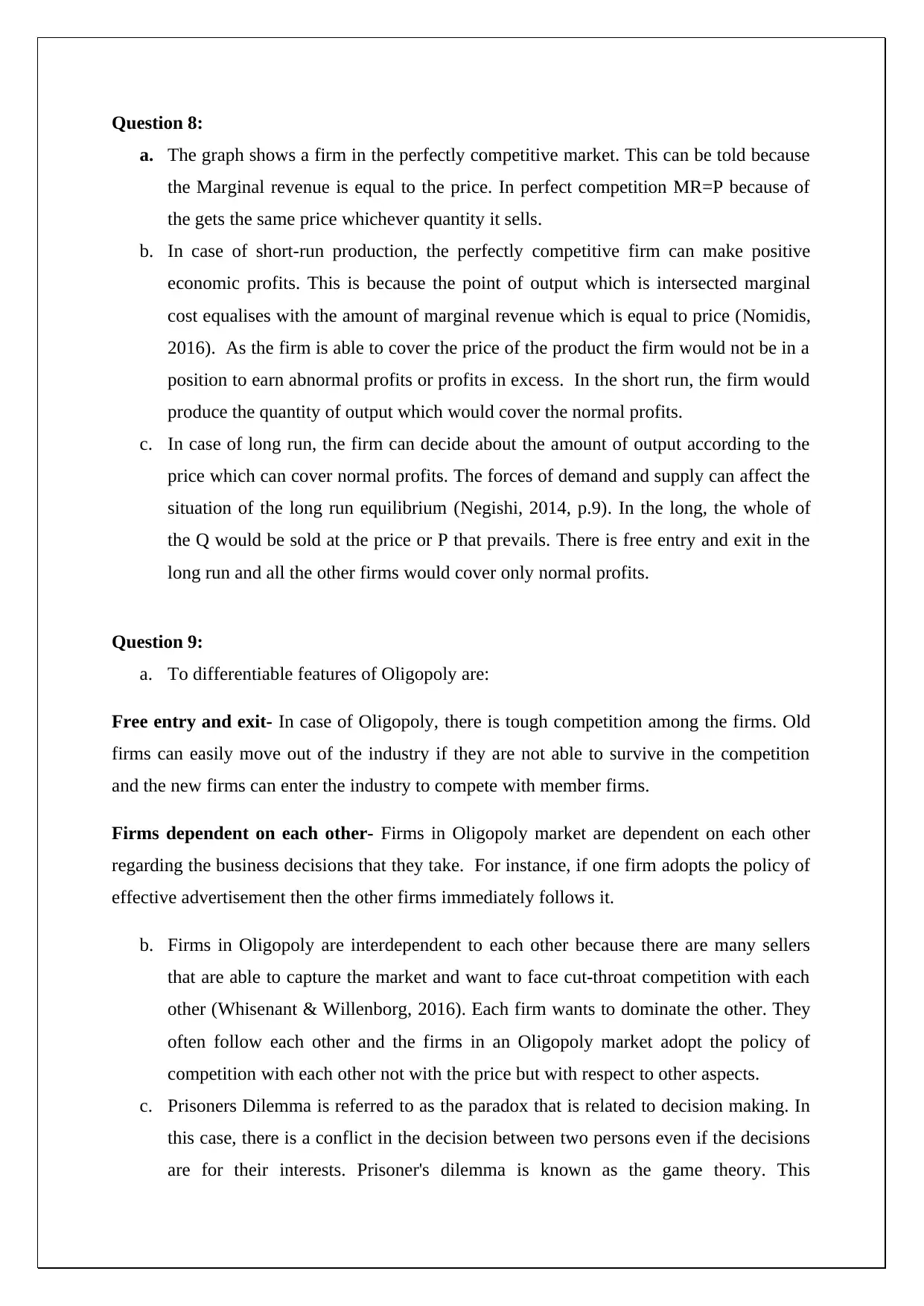

Question 8:

a. The graph shows a firm in the perfectly competitive market. This can be told because

the Marginal revenue is equal to the price. In perfect competition MR=P because of

the gets the same price whichever quantity it sells.

b. In case of short-run production, the perfectly competitive firm can make positive

economic profits. This is because the point of output which is intersected marginal

cost equalises with the amount of marginal revenue which is equal to price (Nomidis,

2016). As the firm is able to cover the price of the product the firm would not be in a

position to earn abnormal profits or profits in excess. In the short run, the firm would

produce the quantity of output which would cover the normal profits.

c. In case of long run, the firm can decide about the amount of output according to the

price which can cover normal profits. The forces of demand and supply can affect the

situation of the long run equilibrium (Negishi, 2014, p.9). In the long, the whole of

the Q would be sold at the price or P that prevails. There is free entry and exit in the

long run and all the other firms would cover only normal profits.

Question 9:

a. To differentiable features of Oligopoly are:

Free entry and exit- In case of Oligopoly, there is tough competition among the firms. Old

firms can easily move out of the industry if they are not able to survive in the competition

and the new firms can enter the industry to compete with member firms.

Firms dependent on each other- Firms in Oligopoly market are dependent on each other

regarding the business decisions that they take. For instance, if one firm adopts the policy of

effective advertisement then the other firms immediately follows it.

b. Firms in Oligopoly are interdependent to each other because there are many sellers

that are able to capture the market and want to face cut-throat competition with each

other (Whisenant & Willenborg, 2016). Each firm wants to dominate the other. They

often follow each other and the firms in an Oligopoly market adopt the policy of

competition with each other not with the price but with respect to other aspects.

c. Prisoners Dilemma is referred to as the paradox that is related to decision making. In

this case, there is a conflict in the decision between two persons even if the decisions

are for their interests. Prisoner's dilemma is known as the game theory. This

a. The graph shows a firm in the perfectly competitive market. This can be told because

the Marginal revenue is equal to the price. In perfect competition MR=P because of

the gets the same price whichever quantity it sells.

b. In case of short-run production, the perfectly competitive firm can make positive

economic profits. This is because the point of output which is intersected marginal

cost equalises with the amount of marginal revenue which is equal to price (Nomidis,

2016). As the firm is able to cover the price of the product the firm would not be in a

position to earn abnormal profits or profits in excess. In the short run, the firm would

produce the quantity of output which would cover the normal profits.

c. In case of long run, the firm can decide about the amount of output according to the

price which can cover normal profits. The forces of demand and supply can affect the

situation of the long run equilibrium (Negishi, 2014, p.9). In the long, the whole of

the Q would be sold at the price or P that prevails. There is free entry and exit in the

long run and all the other firms would cover only normal profits.

Question 9:

a. To differentiable features of Oligopoly are:

Free entry and exit- In case of Oligopoly, there is tough competition among the firms. Old

firms can easily move out of the industry if they are not able to survive in the competition

and the new firms can enter the industry to compete with member firms.

Firms dependent on each other- Firms in Oligopoly market are dependent on each other

regarding the business decisions that they take. For instance, if one firm adopts the policy of

effective advertisement then the other firms immediately follows it.

b. Firms in Oligopoly are interdependent to each other because there are many sellers

that are able to capture the market and want to face cut-throat competition with each

other (Whisenant & Willenborg, 2016). Each firm wants to dominate the other. They

often follow each other and the firms in an Oligopoly market adopt the policy of

competition with each other not with the price but with respect to other aspects.

c. Prisoners Dilemma is referred to as the paradox that is related to decision making. In

this case, there is a conflict in the decision between two persons even if the decisions

are for their interests. Prisoner's dilemma is known as the game theory. This

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

explanation is related to Oligopoly because business firms in an Oligopoly

competition undertake certain decisions but they are not sure about the actions that

their competitors would take if they would execute their decision (Ishii & Zhang,

2017, p.513). The concept of prisoner's dilemma establishes the idea of the selfish

behaviour of rival firms contrary to the best outcomes for both the firms.

competition undertake certain decisions but they are not sure about the actions that

their competitors would take if they would execute their decision (Ishii & Zhang,

2017, p.513). The concept of prisoner's dilemma establishes the idea of the selfish

behaviour of rival firms contrary to the best outcomes for both the firms.

Reference list

Azevedo, E. M., & Gottlieb, D. (2017). Perfect competition in markets with adverse

selection. Econometrica, 85(1), 67-105.

Friedman, M., (2017). The quantity theory of money (pp. 1-31). Palgrave Macmillan UK.

Ishii, J., & Zhang, D. H. (2017). Options compensation as a commitment mechanism in

oligopoly competition. Managerial and Decision Economics, 38(4), 513-525.

Kirzner, I. M. (2015). Competition and entrepreneurship. University of Chicago Press.

Kurzban, R., Duckworth, A., Kable, J. W., & Myers, J. (2013). An opportunity cost model of

subjective effort and task performance. Behavioral and Brain Sciences, 36(6), 661-679.

Negishi, T. (2014). Firms and Production. In Elements of Neo-Walrasian Economics (pp. 9-

27). Springer Japan.

Nomidis, D. (2016). A Revision of the Theory of Perfect Competition and of Value.

Posner, R.A., (2014). Economic analysis of law. Wolters Kluwer Law & Business.

Qadir, M., Quillérou, E., Nangia, V., Murtaza, G., Singh, M., Thomas, R. J., ... & Noble, A.

D. (2014, November). Economics of salt‐induced land degradation and restoration.

In Natural Resources Forum (Vol. 38, No. 4, pp. 282-295).

Shapiro, M. D. (2016). Supply shocks in macroeconomics (pp. 1-7). Palgrave Macmillan UK.

Varian, H. R. (2014). Intermediate Microeconomics: A Modern Approach: Ninth

International Student Edition. WW Norton & Company.

Varian, H. R. (2014). Intermediate Microeconomics: A Modern Approach: Ninth

International Student Edition. WW Norton & Company.

Whisenant, S., & Willenborg, M. (2016). Price Competition Within the Large Audit Firm

Oligopoly: A Panel Data Analysis of Initial Engagements.

Azevedo, E. M., & Gottlieb, D. (2017). Perfect competition in markets with adverse

selection. Econometrica, 85(1), 67-105.

Friedman, M., (2017). The quantity theory of money (pp. 1-31). Palgrave Macmillan UK.

Ishii, J., & Zhang, D. H. (2017). Options compensation as a commitment mechanism in

oligopoly competition. Managerial and Decision Economics, 38(4), 513-525.

Kirzner, I. M. (2015). Competition and entrepreneurship. University of Chicago Press.

Kurzban, R., Duckworth, A., Kable, J. W., & Myers, J. (2013). An opportunity cost model of

subjective effort and task performance. Behavioral and Brain Sciences, 36(6), 661-679.

Negishi, T. (2014). Firms and Production. In Elements of Neo-Walrasian Economics (pp. 9-

27). Springer Japan.

Nomidis, D. (2016). A Revision of the Theory of Perfect Competition and of Value.

Posner, R.A., (2014). Economic analysis of law. Wolters Kluwer Law & Business.

Qadir, M., Quillérou, E., Nangia, V., Murtaza, G., Singh, M., Thomas, R. J., ... & Noble, A.

D. (2014, November). Economics of salt‐induced land degradation and restoration.

In Natural Resources Forum (Vol. 38, No. 4, pp. 282-295).

Shapiro, M. D. (2016). Supply shocks in macroeconomics (pp. 1-7). Palgrave Macmillan UK.

Varian, H. R. (2014). Intermediate Microeconomics: A Modern Approach: Ninth

International Student Edition. WW Norton & Company.

Varian, H. R. (2014). Intermediate Microeconomics: A Modern Approach: Ninth

International Student Edition. WW Norton & Company.

Whisenant, S., & Willenborg, M. (2016). Price Competition Within the Large Audit Firm

Oligopoly: A Panel Data Analysis of Initial Engagements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.