Report: Impact of Microeconomic Theories on Small Business Operations

VerifiedAdded on 2022/07/28

|15

|2607

|22

Report

AI Summary

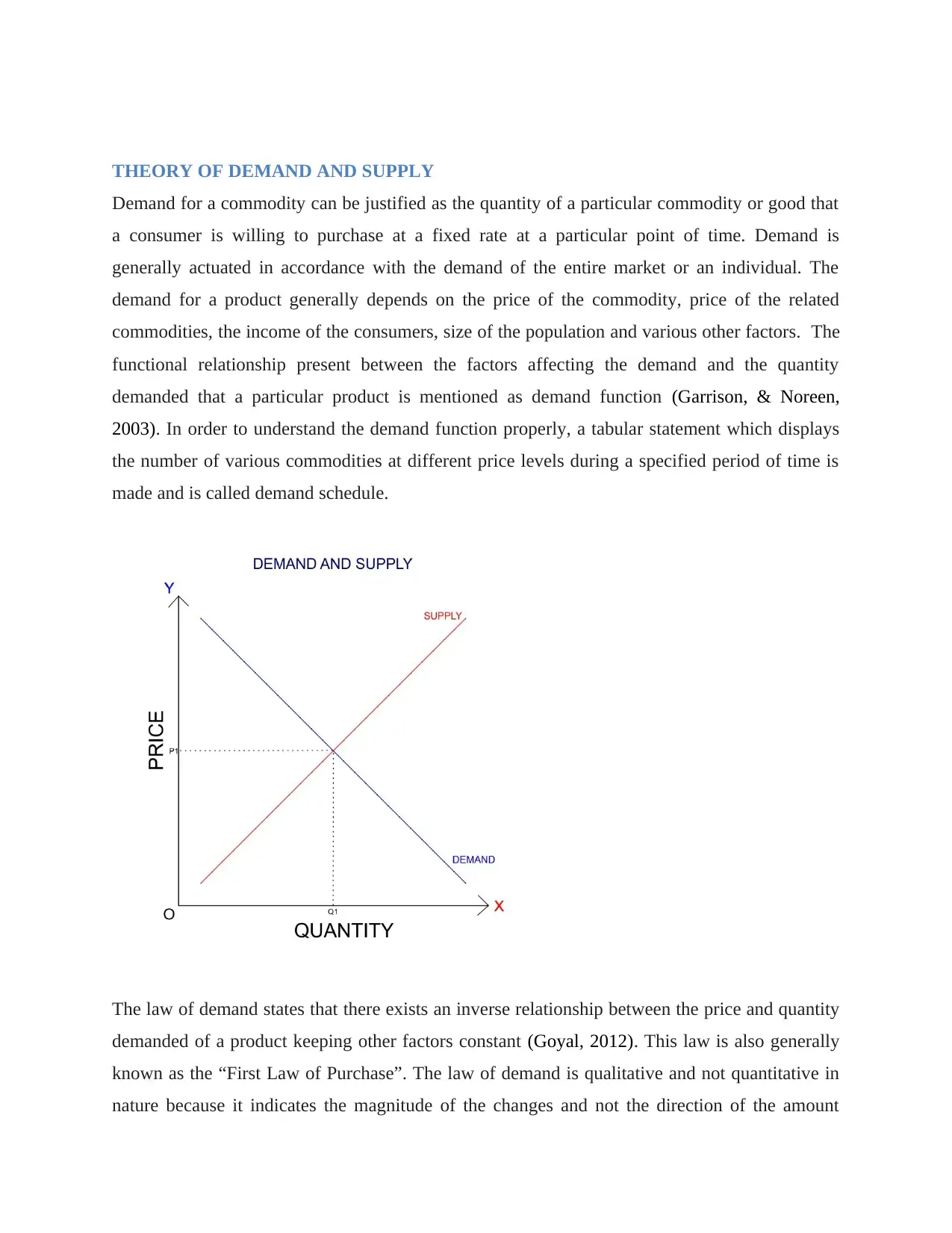

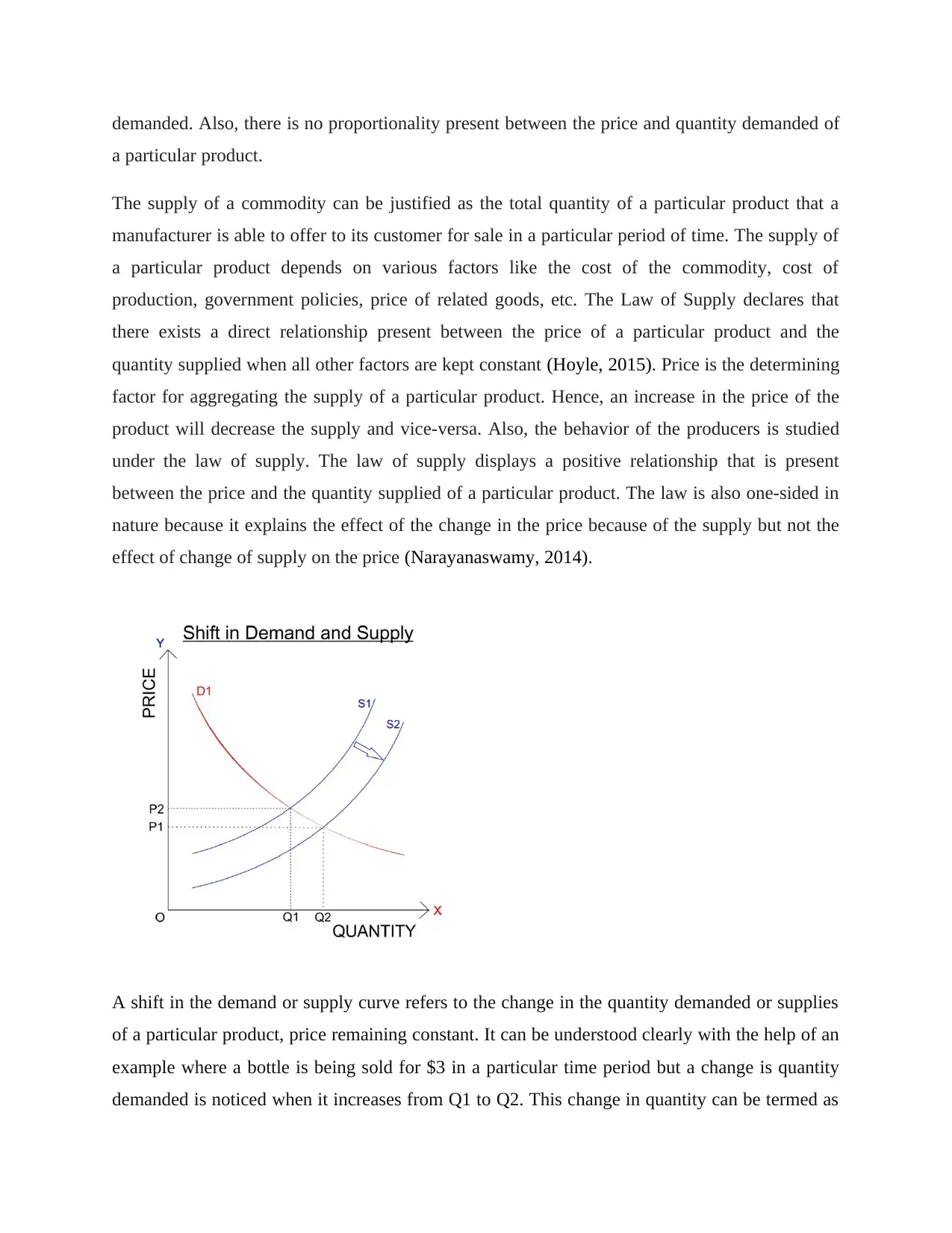

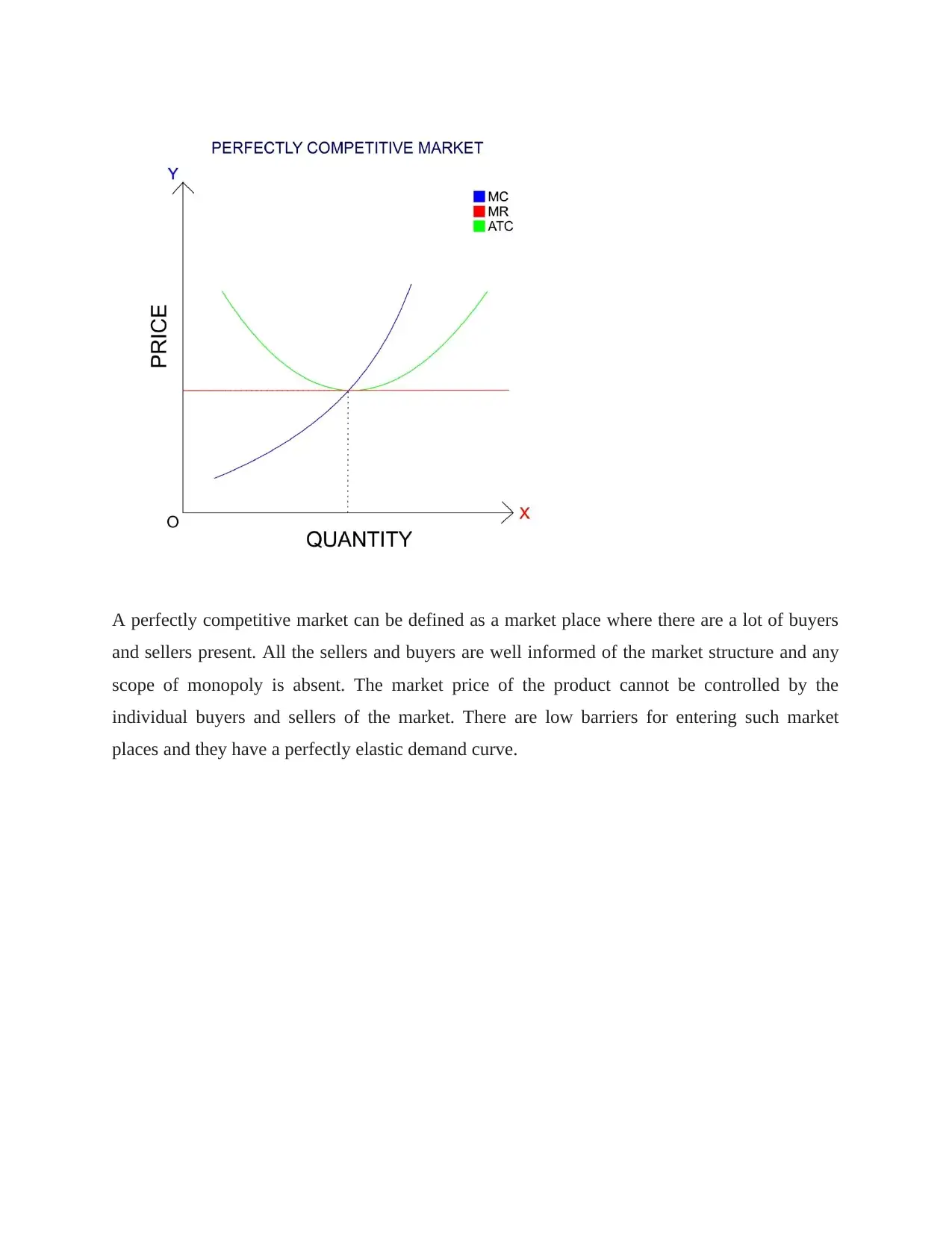

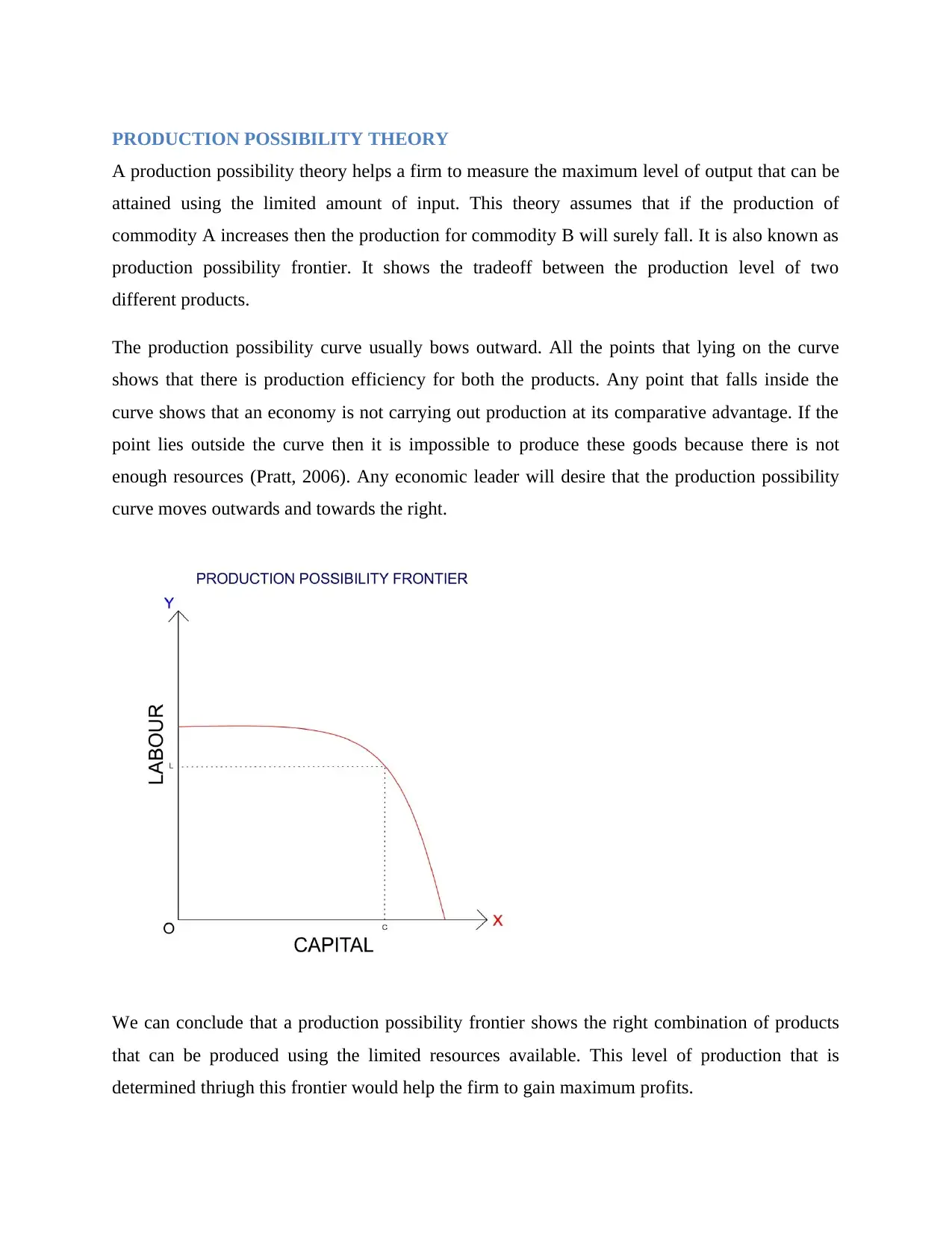

This report delves into the application of microeconomic theories within the context of small business operations. It begins with an introduction to the fundamental principles of microeconomics, emphasizing their importance in effective business management. The core of the report examines several key theories, including the theory of production and cost, which explores factors of production, cost functions (fixed, variable, average, and marginal), and their impact on profit. The theory of demand and supply is then discussed, focusing on demand schedules, the law of demand and supply, and shifts in demand and supply curves. Next, the report explores the theory of market structure, differentiating between various market types such as monopolistic competition, oligopoly, monopoly, and perfect competition. The production possibility theory, which helps firms measure the maximum level of output, is also analyzed. The report concludes by highlighting the practical implications of these microeconomic theories for small businesses, emphasizing how they can guide decision-making and contribute to overall business success.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.