Microeconomic Theory Assignment: Competitive Markets & Oligopoly

VerifiedAdded on 2022/07/28

|12

|1163

|23

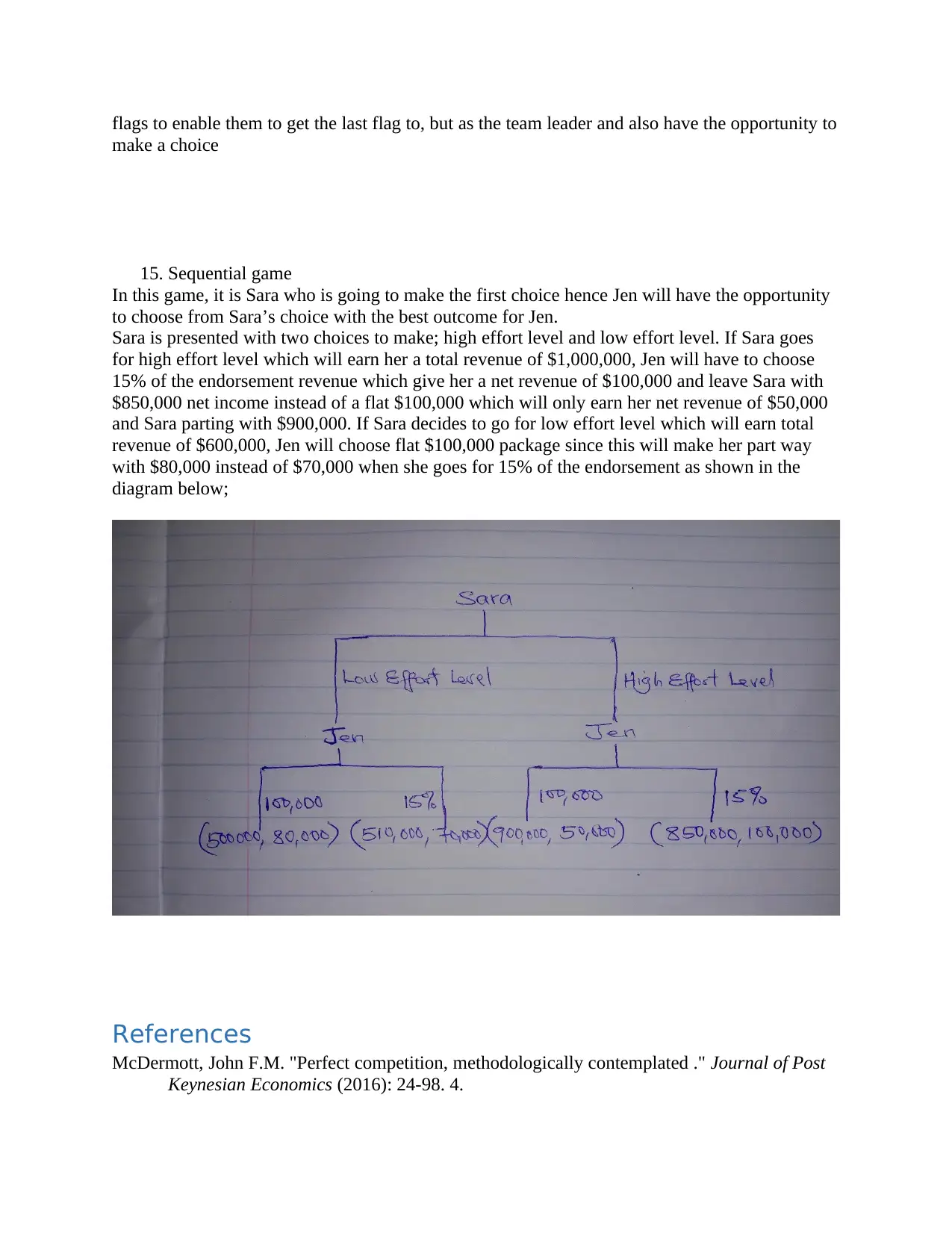

Homework Assignment

AI Summary

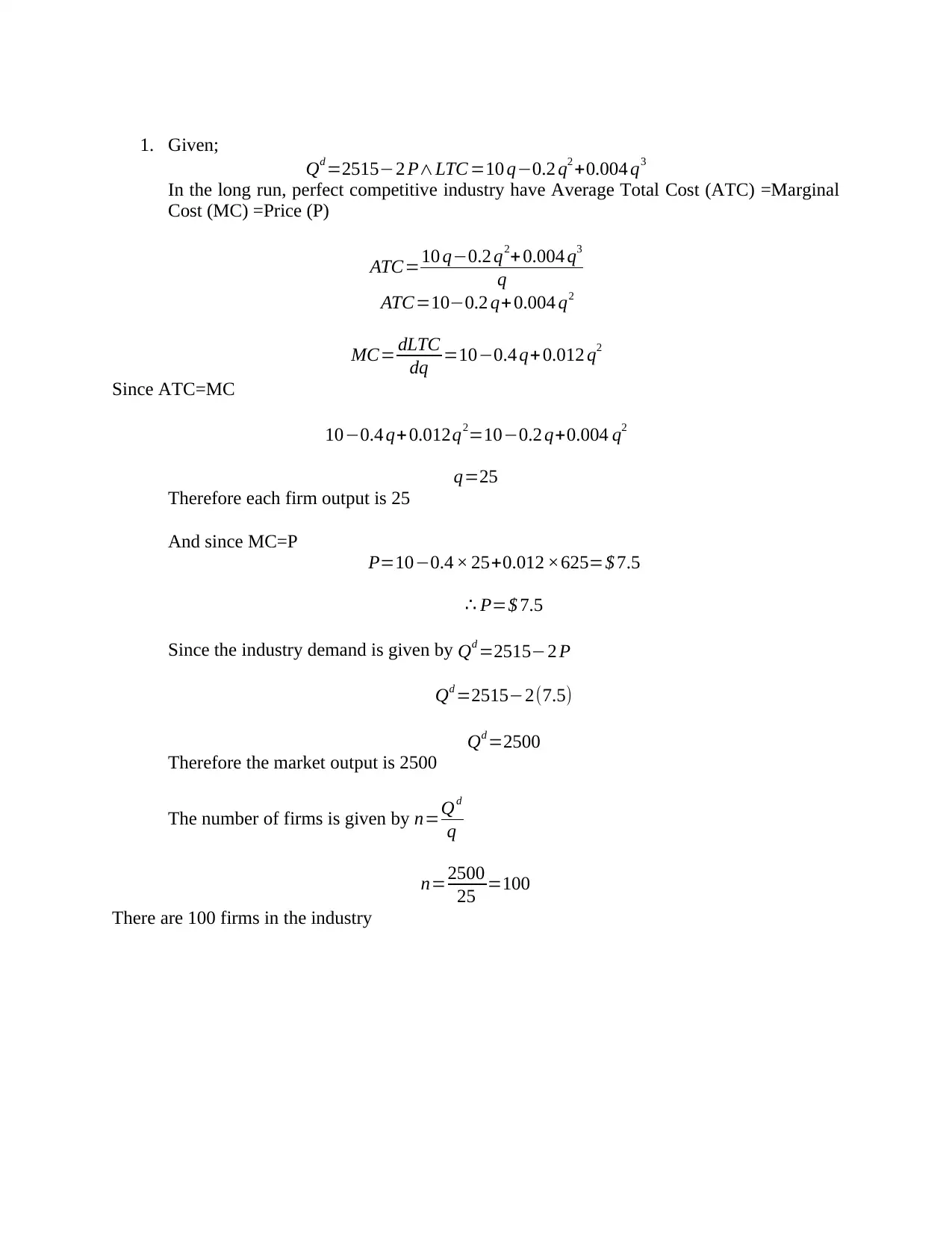

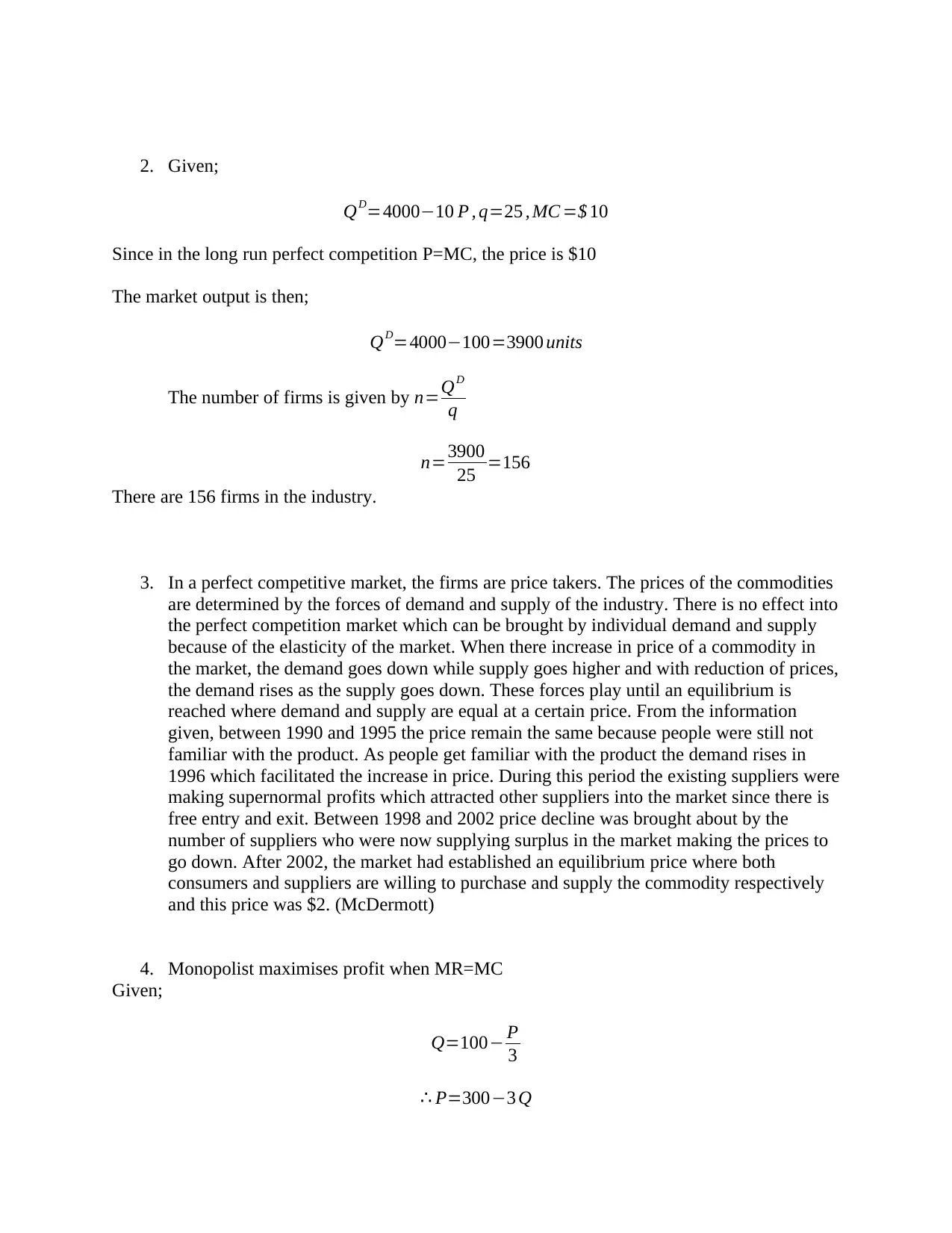

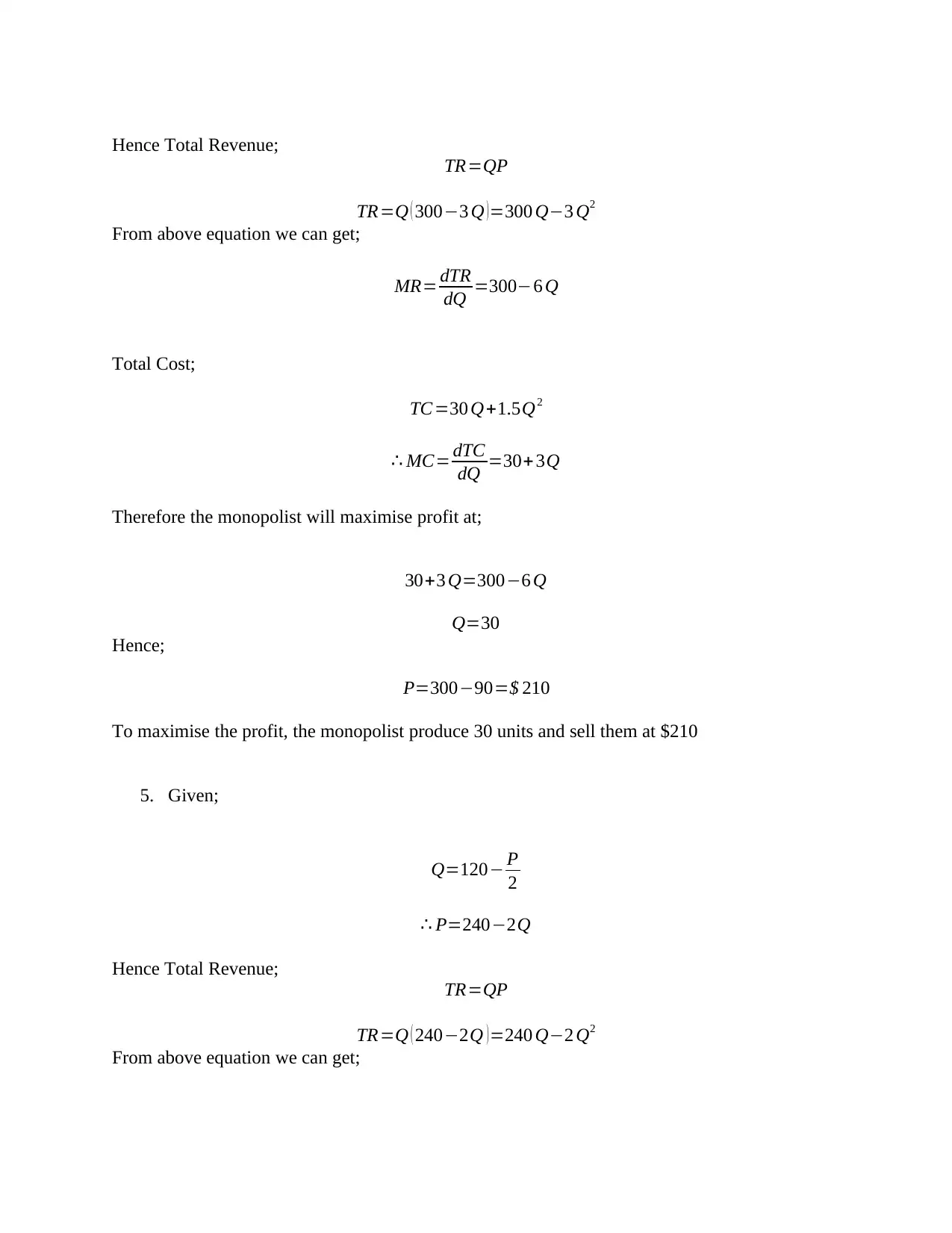

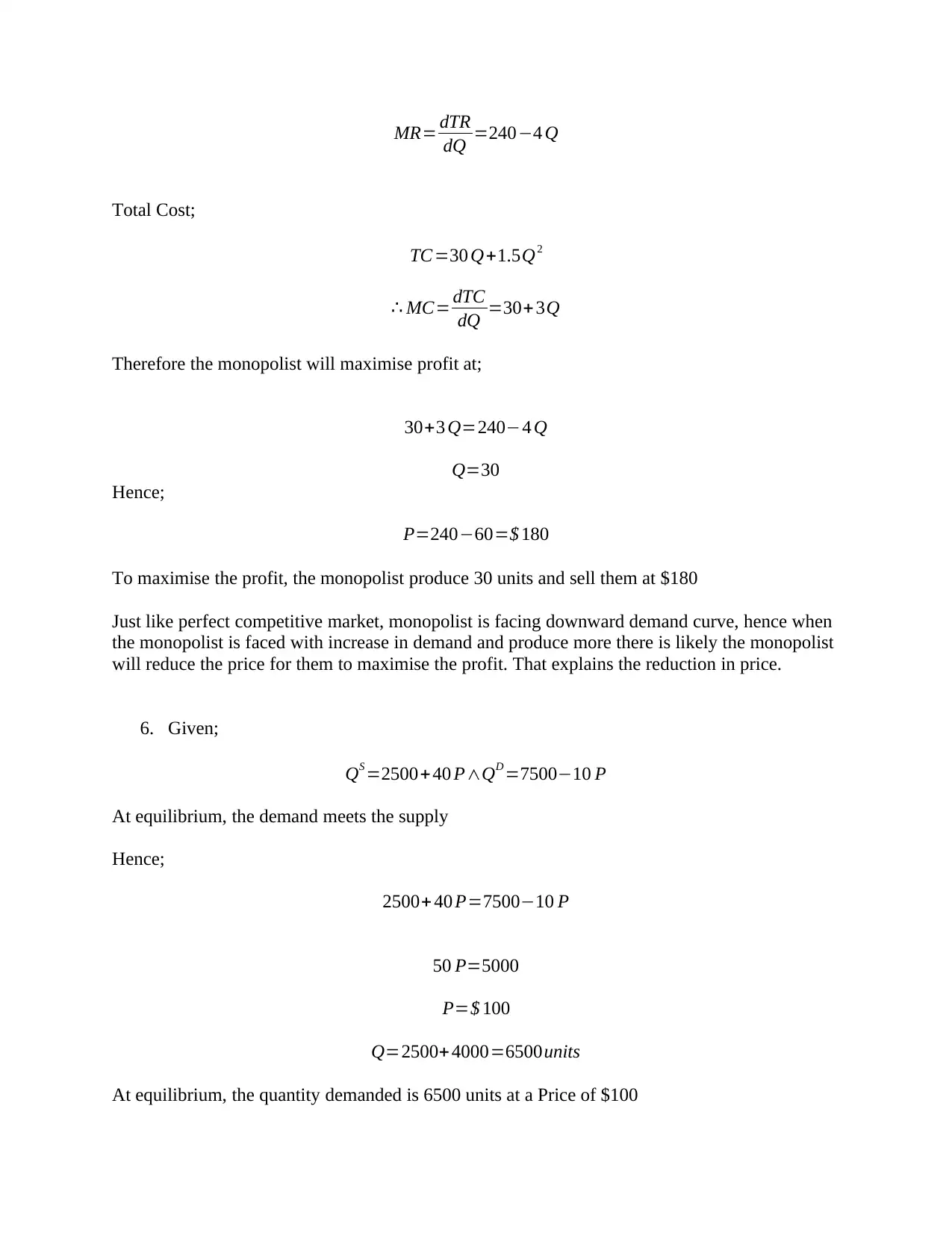

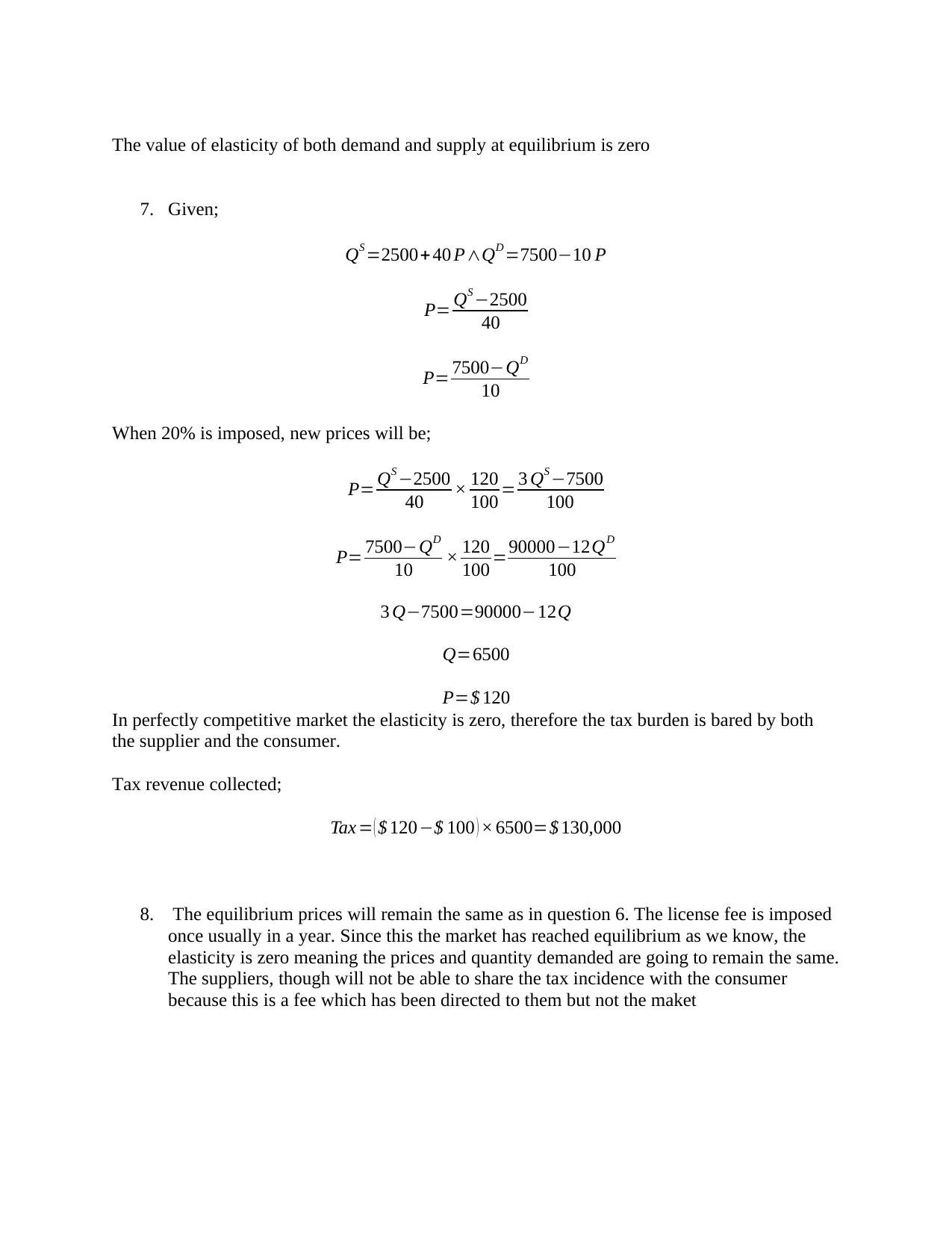

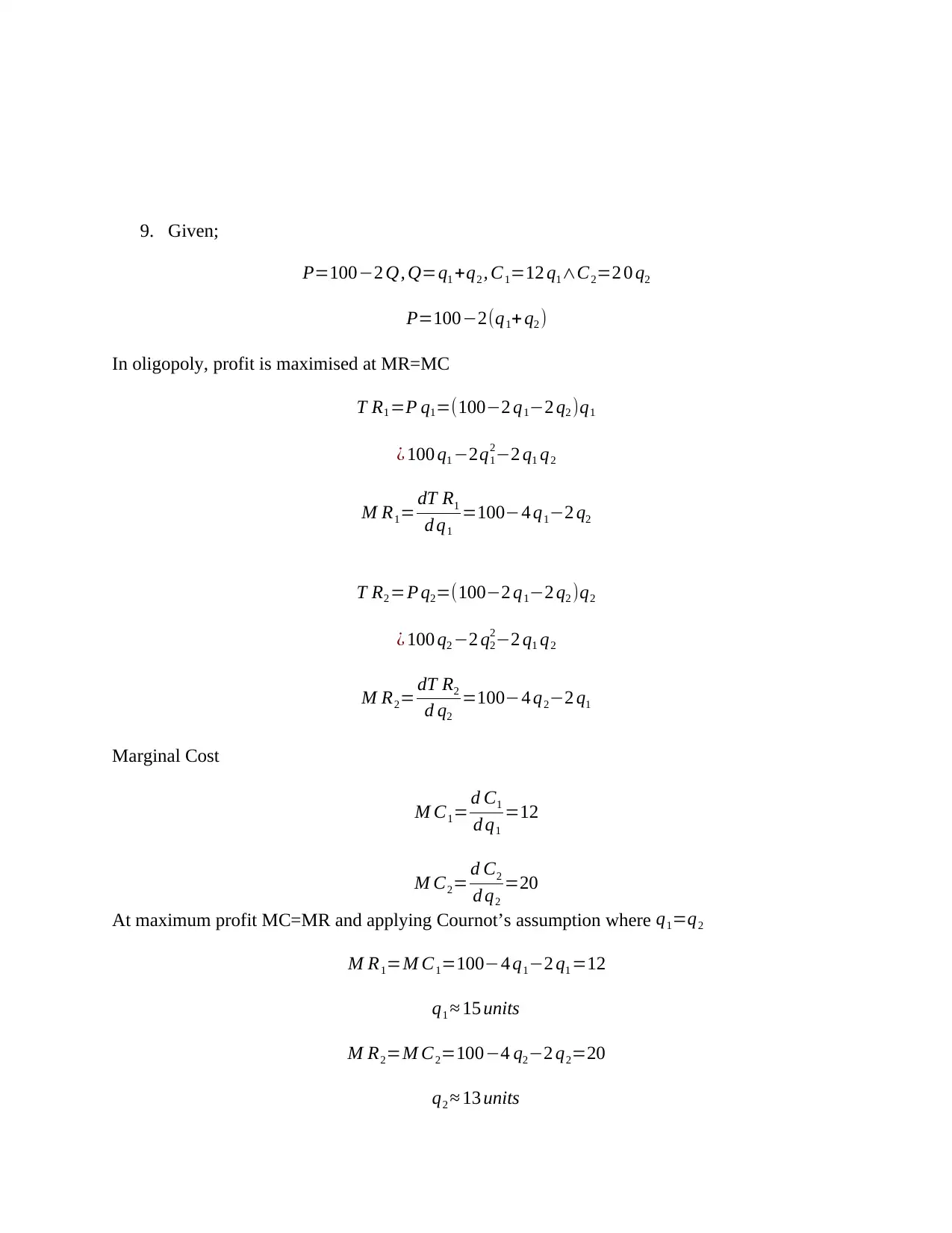

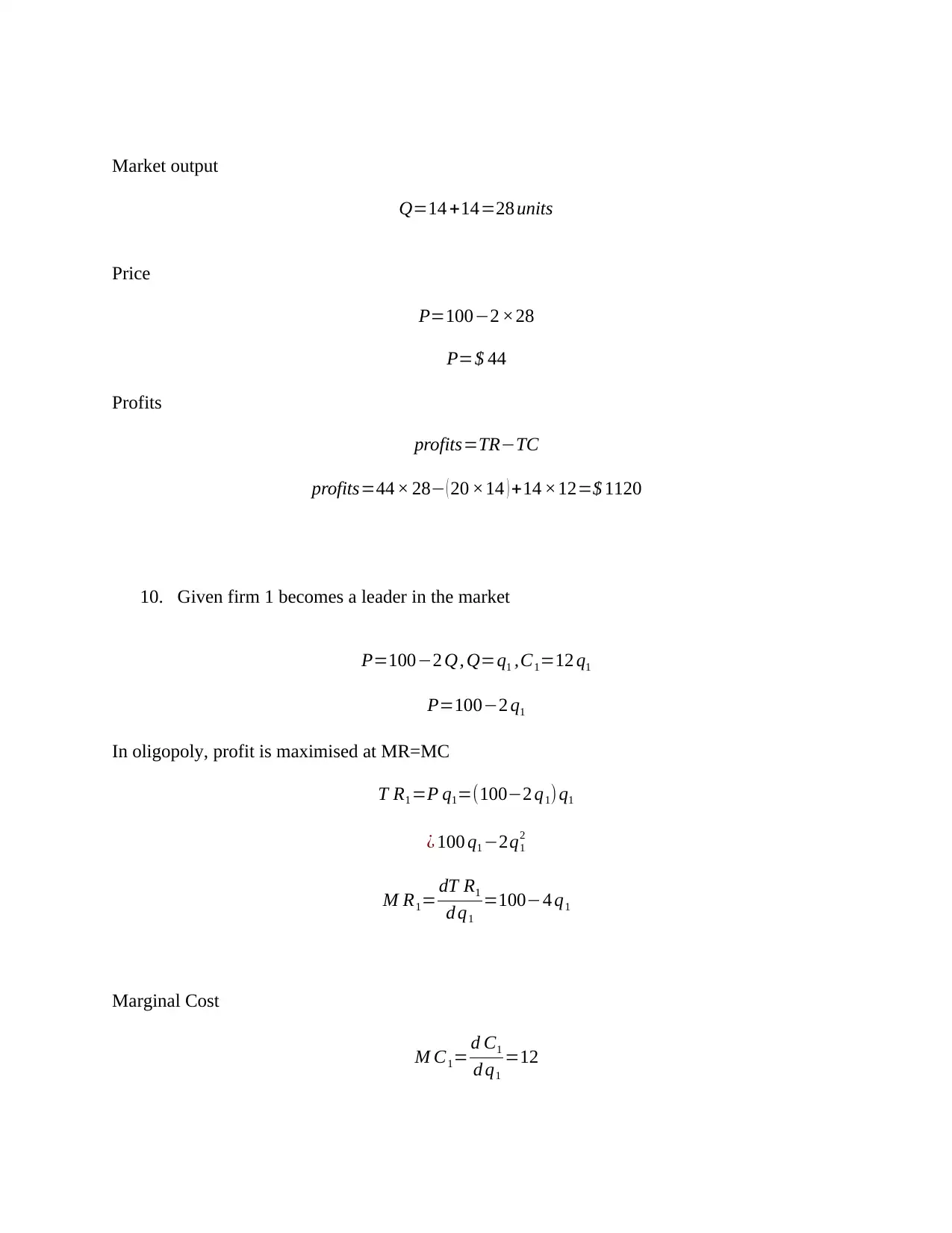

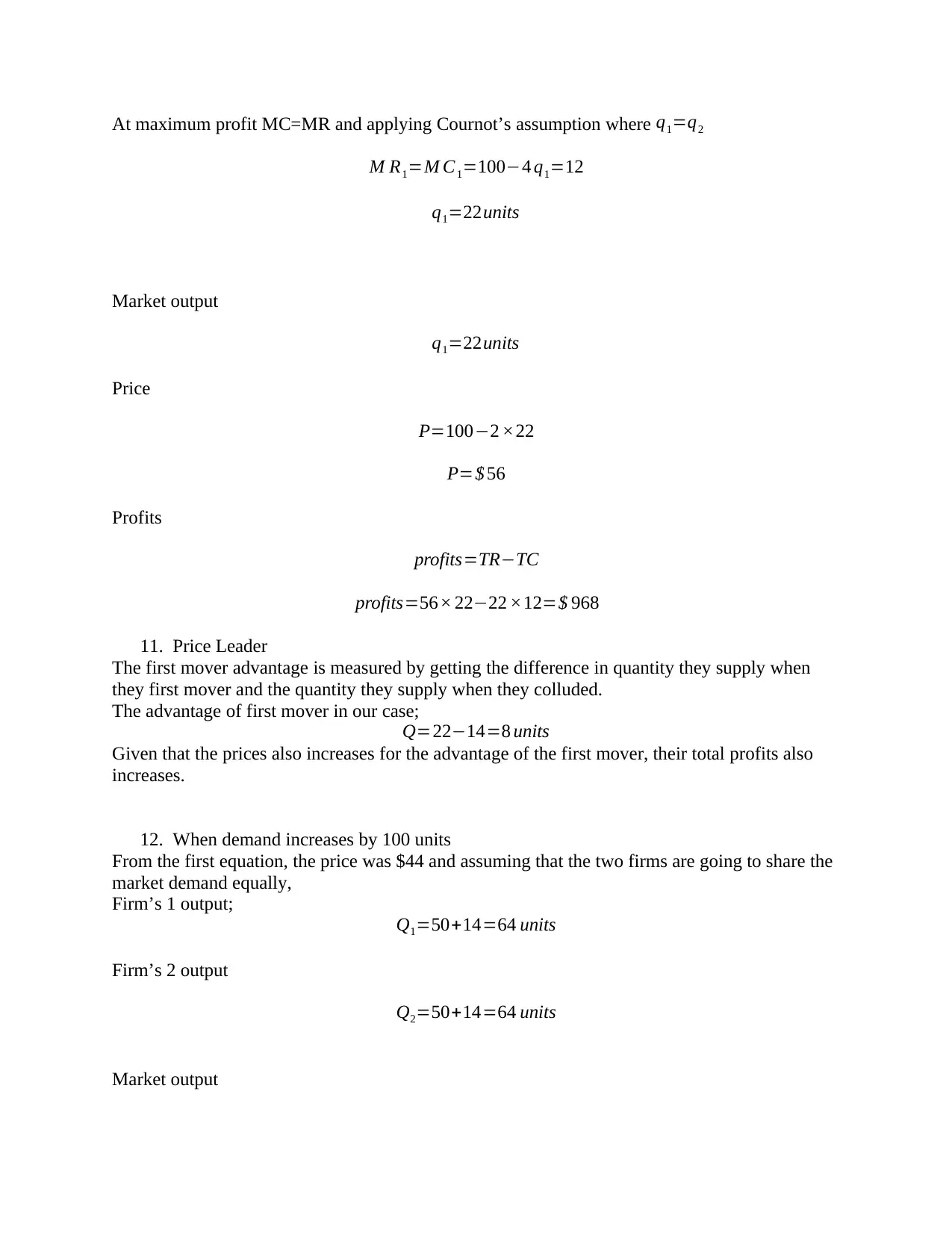

This assignment solution addresses several key concepts in microeconomic theory. It begins by analyzing long-run equilibrium in a perfectly competitive market, deriving output, price, and the number of firms. The solution then explores a scenario with given market demand and marginal cost to determine equilibrium values. A case study examines the calcium market, tracing price fluctuations and explaining them through supply and demand dynamics. The assignment further delves into monopoly, calculating profit-maximizing output and price. It also tackles oligopoly using the Cournot model, analyzing firm behavior and first-mover advantages. Additionally, the solution covers market equilibrium, price elasticity, tax burden, and game theory concepts like backward induction and sequential games, providing a comprehensive understanding of microeconomic principles.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.