Microeconomics Assignment: Analyzing Market Structures and Cost Curves

VerifiedAdded on 2022/12/20

|8

|756

|57

Homework Assignment

AI Summary

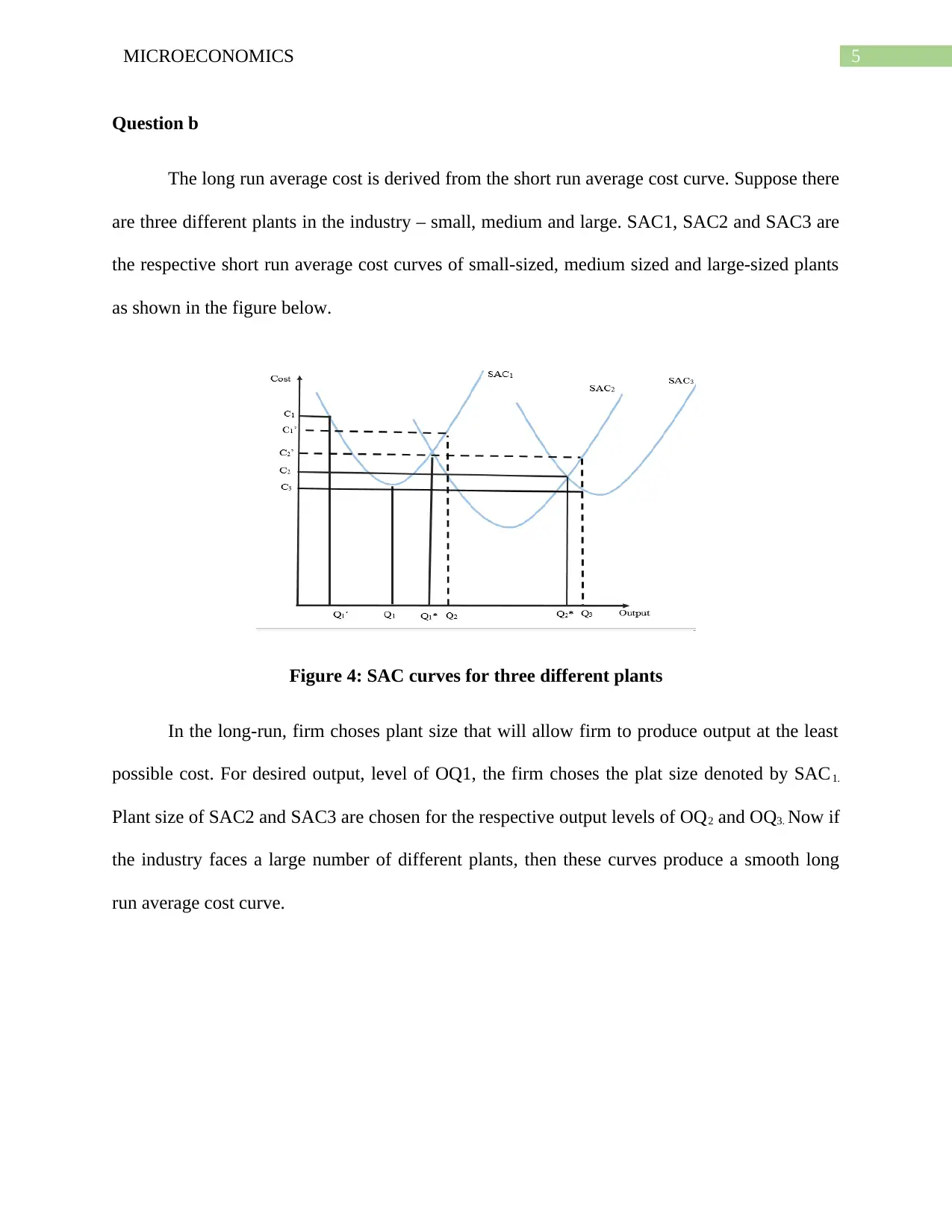

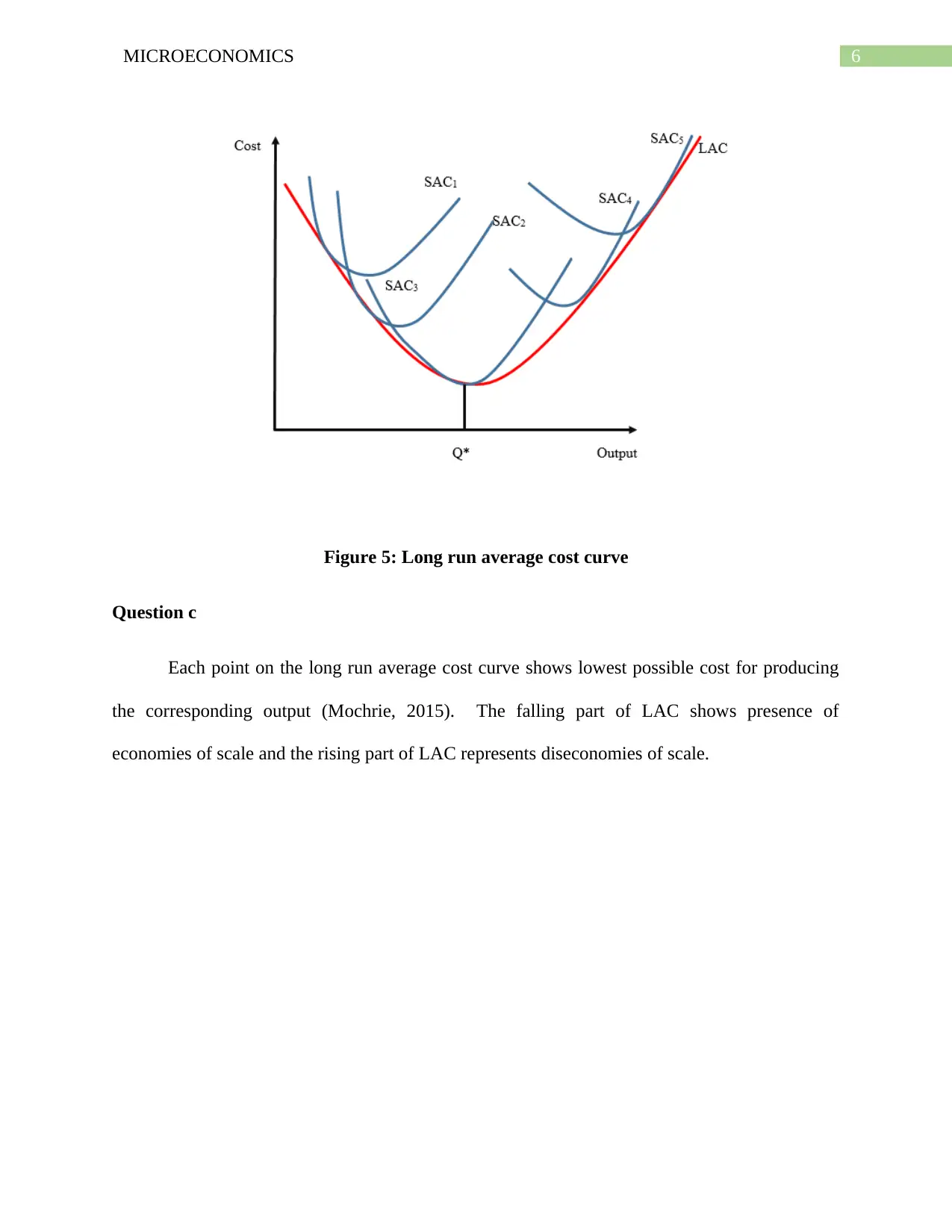

This microeconomics assignment solution addresses key concepts including allocative efficiency and market structures. Question 2 examines allocative efficiency in perfectly competitive markets and why monopolistically competitive firms fail to achieve it, using diagrams to illustrate the concepts. Question 3 explores the relationship between marginal product and marginal cost, explaining how a firm's marginal costs are minimized when its marginal product is maximized, again using diagrams to aid understanding. The solution also explains the derivation of the long-run average cost curve from multiple plant operations and identifies the significance of various portions of the long-run average cost curve, providing a comprehensive analysis of the topics.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.