Principles of Economics Assignment: Microeconomics Analysis (BB106)

VerifiedAdded on 2022/09/15

|8

|1355

|14

Homework Assignment

AI Summary

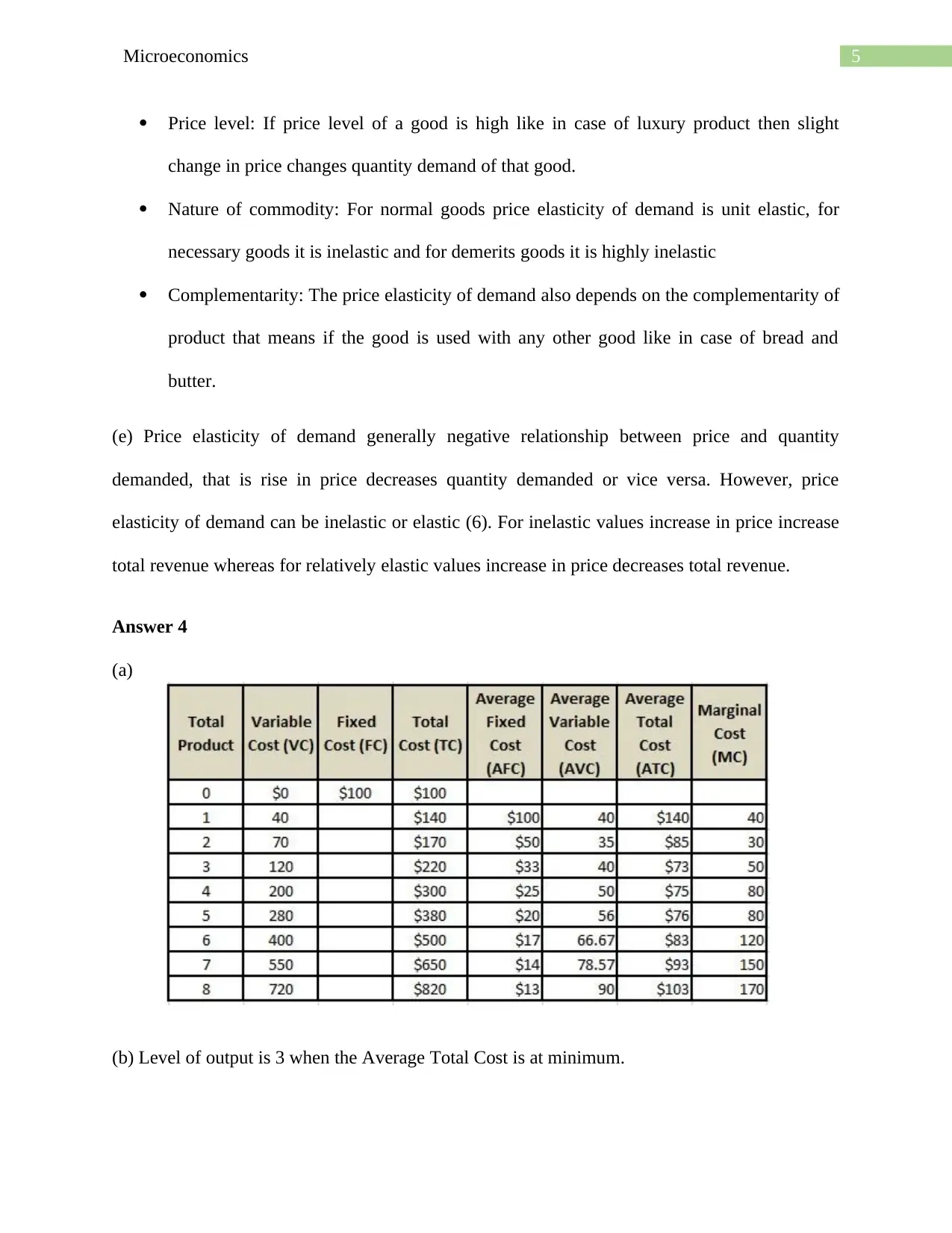

This document presents a comprehensive solution to a microeconomics assignment, addressing core economic principles. The assignment explores the concept of scarcity in the mining industry and the fundamental economic questions of what, how, and for whom to produce, using the example of an economics textbook. It further analyzes the production possibility frontier (PPF) and factors that cause shifts. The assignment then delves into demand and supply dynamics, including factors influencing demand, the impact of supply shifts on market equilibrium, and the concept of market failure and externalities. The analysis extends to price elasticity of demand, calculating elasticity values and identifying factors affecting it. Finally, the solution examines cost and revenue concepts, including average total cost, marginal cost, diminishing marginal returns, and diseconomies of scale. The assignment is thoroughly referenced, providing a strong understanding of microeconomic principles.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.