Microeconomics Assignment on Market Structures and Inflation Analysis

VerifiedAdded on 2020/03/16

|5

|1048

|50

Homework Assignment

AI Summary

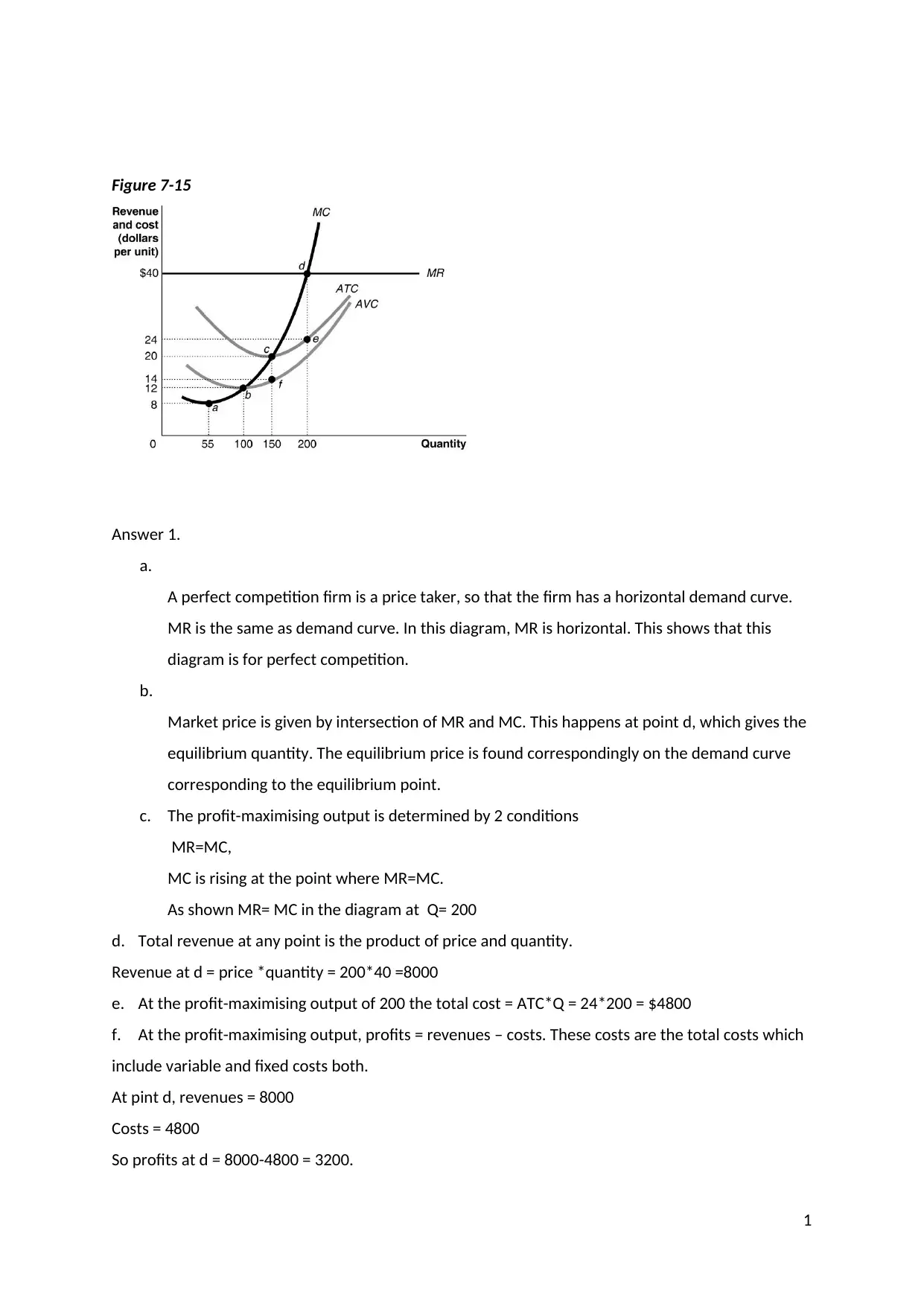

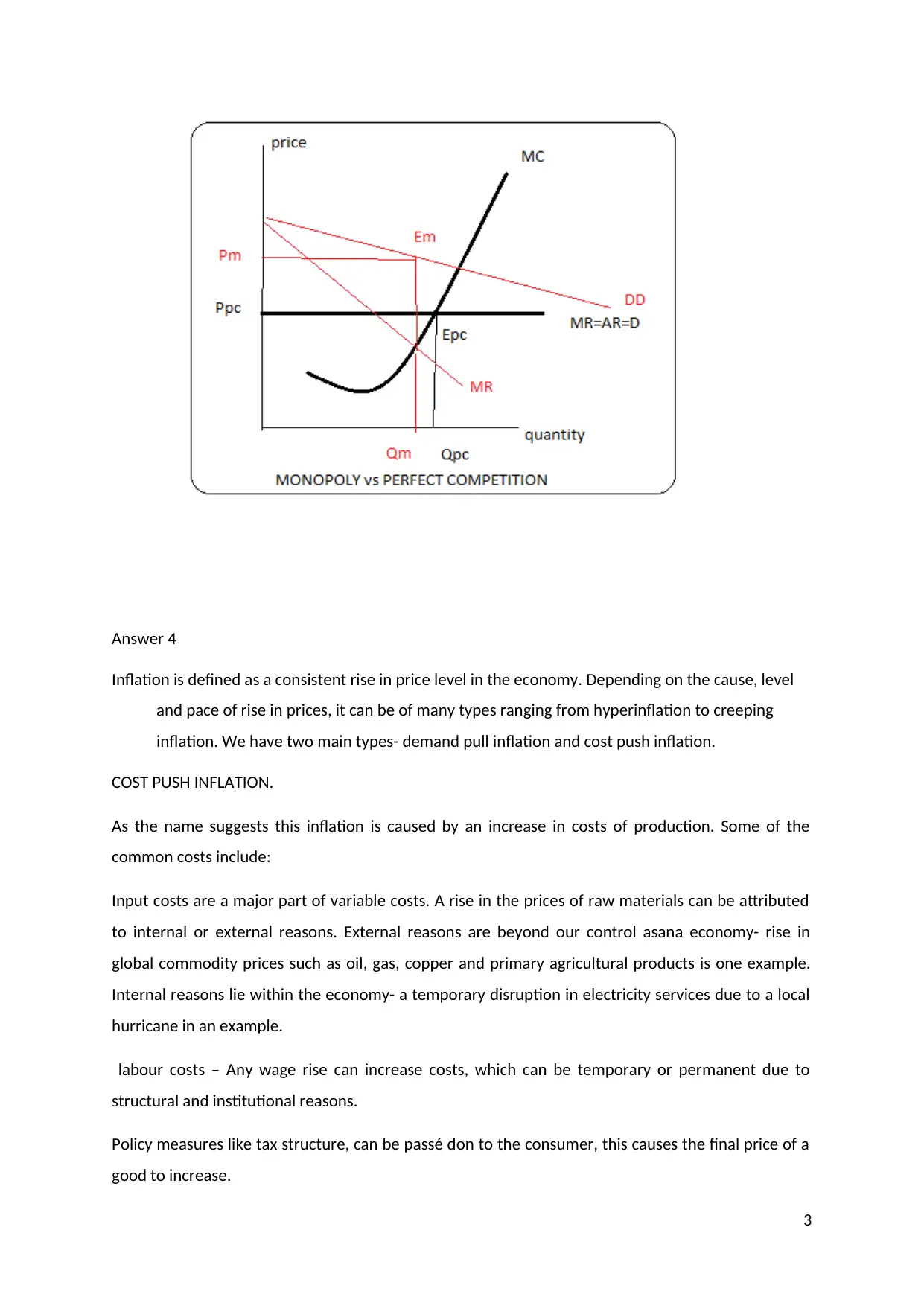

This economics assignment provides solutions to questions on microeconomic principles. The first part analyzes a perfectly competitive firm, determining profit-maximizing output, total revenue, total cost, and profits using marginal cost and revenue curves. It also identifies the firm's short-run supply curve and explains long-run profitability. The second part compares perfect competition and monopoly, highlighting the differences in equilibrium price and quantity, and the role of marginal revenue. The final part examines inflation, differentiating between cost-push and demand-pull inflation, and analyzing the causes of cost-push inflation in Pakistan, referencing rising fuel, food, and raw material prices, along with the elimination of energy subsidies. The assignment includes supporting diagrams and a bibliography of cited sources.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.