Evaluation of Proposed Taxes in the UK Aviation Industry

VerifiedAdded on 2022/12/29

|8

|1349

|44

Report

AI Summary

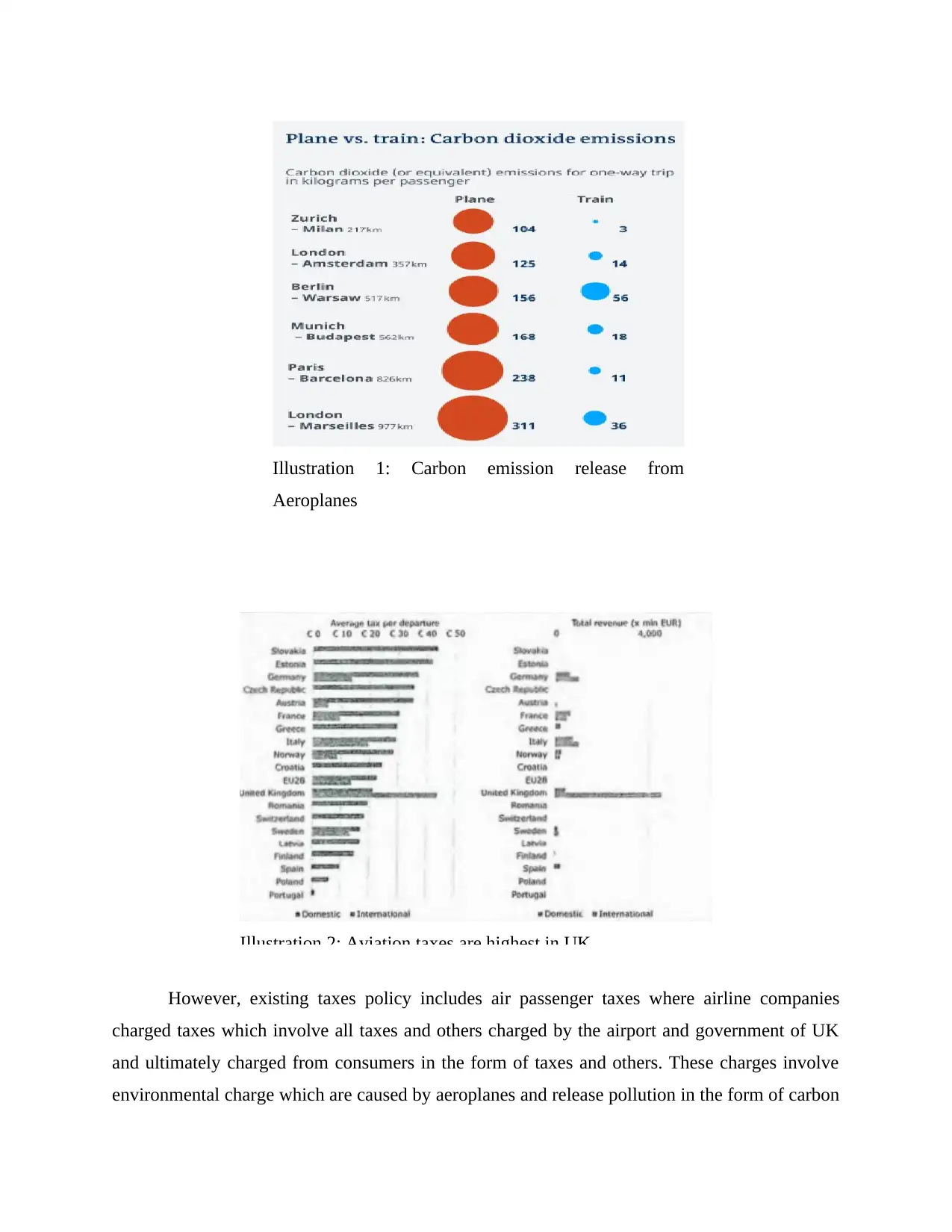

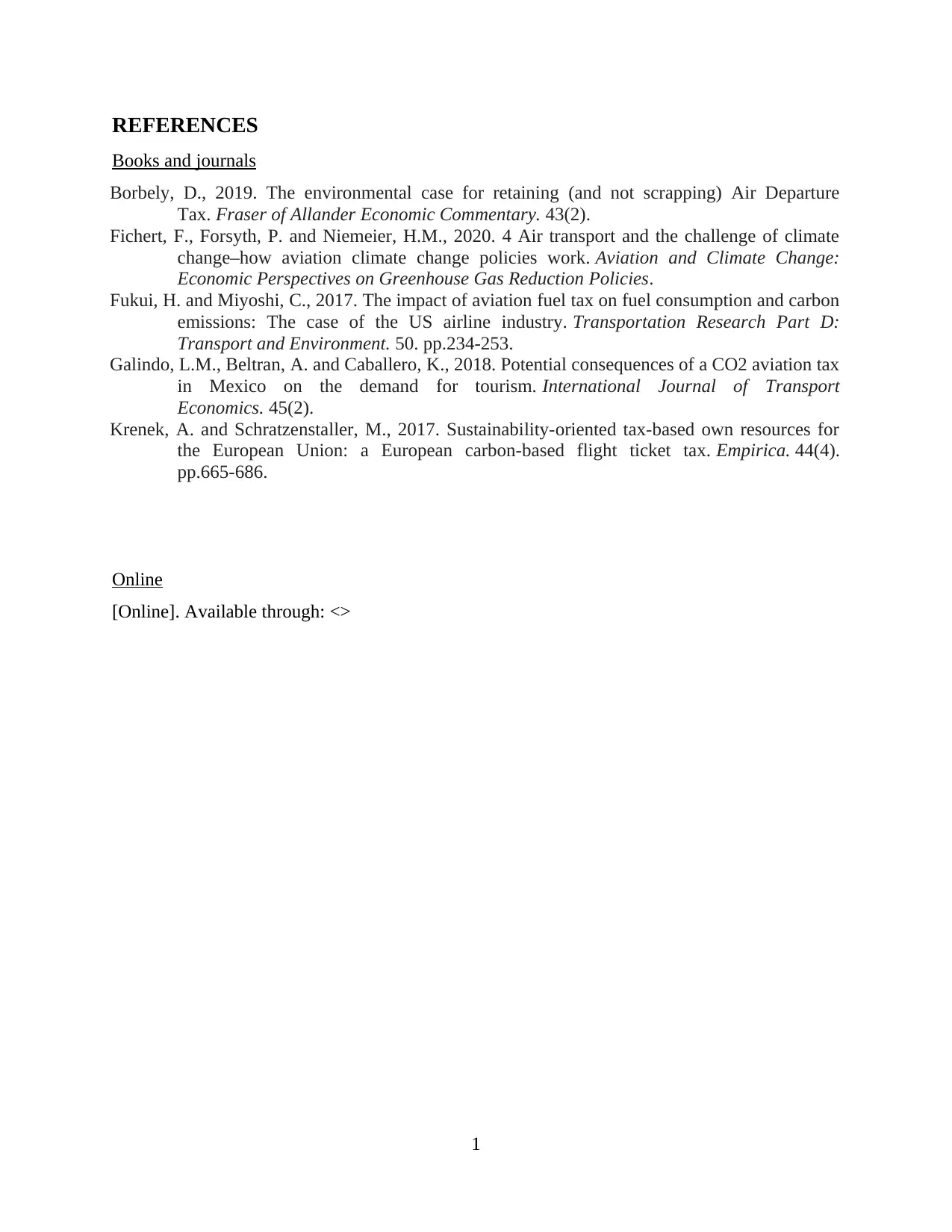

This report examines proposed tax structures for the UK aviation industry, focusing on microeconomic principles. It analyzes the existing tax scenario, which involves various charges collected from passengers, and proposes a new structure that segregates costs into social and environmental taxes, fuel charges, and other fees. The proposed tax structure suggests separating social charges, fuel taxes, and other charges, and implementing a rebate policy for frequent flyers. The report evaluates the potential benefits of these proposals, including increased revenue, ethical working environments, and passenger savings. It also evaluates the impact of carbon emissions and climate change. The analysis concludes that the proposed tax can promote social and environmental development. The study also references the impact of Covid-19 and discusses the need for ethical practices within the aviation industry to mitigate environmental damage and promote passenger-friendly policies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.