Microeconomics: Analyzing Consumer Behavior with Utility and Insurance

VerifiedAdded on 2023/06/18

|9

|2528

|387

Essay

AI Summary

This essay delves into microeconomic principles, focusing on expected utility theory and prospect theory within the context of consumer behavior and insurance markets. It examines a consumer's decision-making process in a two-state model, analyzing how individuals make choices under uncertainty and how fair insurance markets function. The essay further explores the concept of loss aversion and bounded rationality, contrasting it with rational behavior. It discusses the value function in prospect theory, emphasizing the role of reference points in shaping risk attitudes. Additionally, it compares the utility function used in prospect theory with the expected utility theory, highlighting the differences in how they model individual preferences and choices under risk and uncertainty. This resource is available on Desklib, a platform offering a wealth of study materials, including past papers and solved assignments, to support students in their academic endeavors.

Integrated Essay and Exercise:

Microeconomics

Microeconomics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1.............................................................................................................................4

QUESTION 3.............................................................................................................................6

a) Describing the loss aversion and utilization of it to illustrate the difference between the

rational and bounded rational behaviour...............................................................................6

b) Discussing the value function in prospect theory and role of reference point............7

c) Describing utility function used in prospect theory and comparing it with expected

utility......................................................................................................................................8

REFERENCES.........................................................................................................................10

QUESTION 1.............................................................................................................................4

QUESTION 3.............................................................................................................................6

a) Describing the loss aversion and utilization of it to illustrate the difference between the

rational and bounded rational behaviour...............................................................................6

b) Discussing the value function in prospect theory and role of reference point............7

c) Describing utility function used in prospect theory and comparing it with expected

utility......................................................................................................................................8

REFERENCES.........................................................................................................................10

QUESTION 1

Microeconomics accounts for the branch of economics which involves the study of

the implications of the incentives and decisions which results into affecting the usage and

distribution of the resources. It provides an analysis of how the individuals and the businesses

carried out and gets benefits from the efficient sources. This essay provides an insight into the

consumer facing two-state model pertaining to an insurance problem.

The expected utility approach refers to the usage of the tools for the purpose of

analyzing the situations within which the individuals require to undertake the decision

without knowing the outcomes which might occur due to that decision which is also known

as decision under uncertainty. The expected utility theory in respect to the decision making is

computed by multiplying the value of each possible actions by the probability in regard to the

outcome occurred (Expected utility decision theory. 2020). This concept is used to elucidate

the decisions made under the situation of risk. This concept is having a wider application over

the decisions pertaining to the businesses which includes insurance, capital expenditure,

operations etc.The expected utility theory was developed in the year 1944 with the purpose of

dealing with the situations of quantifiable risk. It needed preferences to exhibit the two

additional axioms of continuity and independence (Li and Xu, 2017). Let’s assume that the

state of nature can be represented by s = 1…each having its probability of occurring of Ps and

the probabilities is always Ps >= 0. As per the expected utility theory if the consumers are

having rational preferences which clearly exhibits independence and after which the agents

will behave like they have maximized the expected value of their utility. In the similar way,

the firms or the business entities can assume to maximize the expected profits E [π (x)] over

different states of the world. In addition to this, the nature of the budget constraint will vary

considerably based on the situation undertaken. The most easiest situation isthe 2 state set up

with p1 = p and p2 = 1 − p. Individuals maximizeE [u (x)] = pu (x1) + (1 − p) u (x2).

A fair insurance market mainly accounts for the market for the purpose of buying

and selling the state contingent income. The prices in respect to the state contingent income

basically has some connection with respect to the probability of that state occurring. For

instance, if the state 1 is likely to occur then the price in regard to the state 1 contingent

income will be higher as there is a greater chance of payoff (Meyers and Van Hoyweghen,

2018). On the other side, if the state 1 is less likely to occur then in that case, the price of

state 1 contingent income will be lower as there is lower possibility of a payoff. This can be

further effectively understood with the help of an example in respect to a particular type of

Microeconomics accounts for the branch of economics which involves the study of

the implications of the incentives and decisions which results into affecting the usage and

distribution of the resources. It provides an analysis of how the individuals and the businesses

carried out and gets benefits from the efficient sources. This essay provides an insight into the

consumer facing two-state model pertaining to an insurance problem.

The expected utility approach refers to the usage of the tools for the purpose of

analyzing the situations within which the individuals require to undertake the decision

without knowing the outcomes which might occur due to that decision which is also known

as decision under uncertainty. The expected utility theory in respect to the decision making is

computed by multiplying the value of each possible actions by the probability in regard to the

outcome occurred (Expected utility decision theory. 2020). This concept is used to elucidate

the decisions made under the situation of risk. This concept is having a wider application over

the decisions pertaining to the businesses which includes insurance, capital expenditure,

operations etc.The expected utility theory was developed in the year 1944 with the purpose of

dealing with the situations of quantifiable risk. It needed preferences to exhibit the two

additional axioms of continuity and independence (Li and Xu, 2017). Let’s assume that the

state of nature can be represented by s = 1…each having its probability of occurring of Ps and

the probabilities is always Ps >= 0. As per the expected utility theory if the consumers are

having rational preferences which clearly exhibits independence and after which the agents

will behave like they have maximized the expected value of their utility. In the similar way,

the firms or the business entities can assume to maximize the expected profits E [π (x)] over

different states of the world. In addition to this, the nature of the budget constraint will vary

considerably based on the situation undertaken. The most easiest situation isthe 2 state set up

with p1 = p and p2 = 1 − p. Individuals maximizeE [u (x)] = pu (x1) + (1 − p) u (x2).

A fair insurance market mainly accounts for the market for the purpose of buying

and selling the state contingent income. The prices in respect to the state contingent income

basically has some connection with respect to the probability of that state occurring. For

instance, if the state 1 is likely to occur then the price in regard to the state 1 contingent

income will be higher as there is a greater chance of payoff (Meyers and Van Hoyweghen,

2018). On the other side, if the state 1 is less likely to occur then in that case, the price of

state 1 contingent income will be lower as there is lower possibility of a payoff. This can be

further effectively understood with the help of an example in respect to a particular type of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

market called the fair insurance market. It means that the whether the individual buys or sells

state contingent income, it is expected to break even on an average. Under this, some of the

time money is paid while in the other times money is received. It is fair, on an average when

the amount you pay is not equivalent to the amount one receives.Let’s assume the state 1

contingent income, X units ofwhich incurs the cost of p1. If the state 1 in reality occurs then

in that case each unit brings in unit of money. If the state 1 does not occur then in that case

nothing is received from each unit. Therefore, these two stated events happen with the greater

probability of π1 and π2 respectively. In simple terms, the proportion of π1 of the time 1 unit

of the State 1 contingent income results into bringing in 1 unit of money while a proportion

of π2 of the time it results into bringing nothing. On an average, it represents π1 x 1 + π2 x 0

= π1 in money. In order it to be fairthis must to equivalent to the price of state 1 contingent

income which consequently leads to giving the condition for the fair state 1 contingent

income or for the fair insurance purpose: p1 = π1 and p2 = π2.

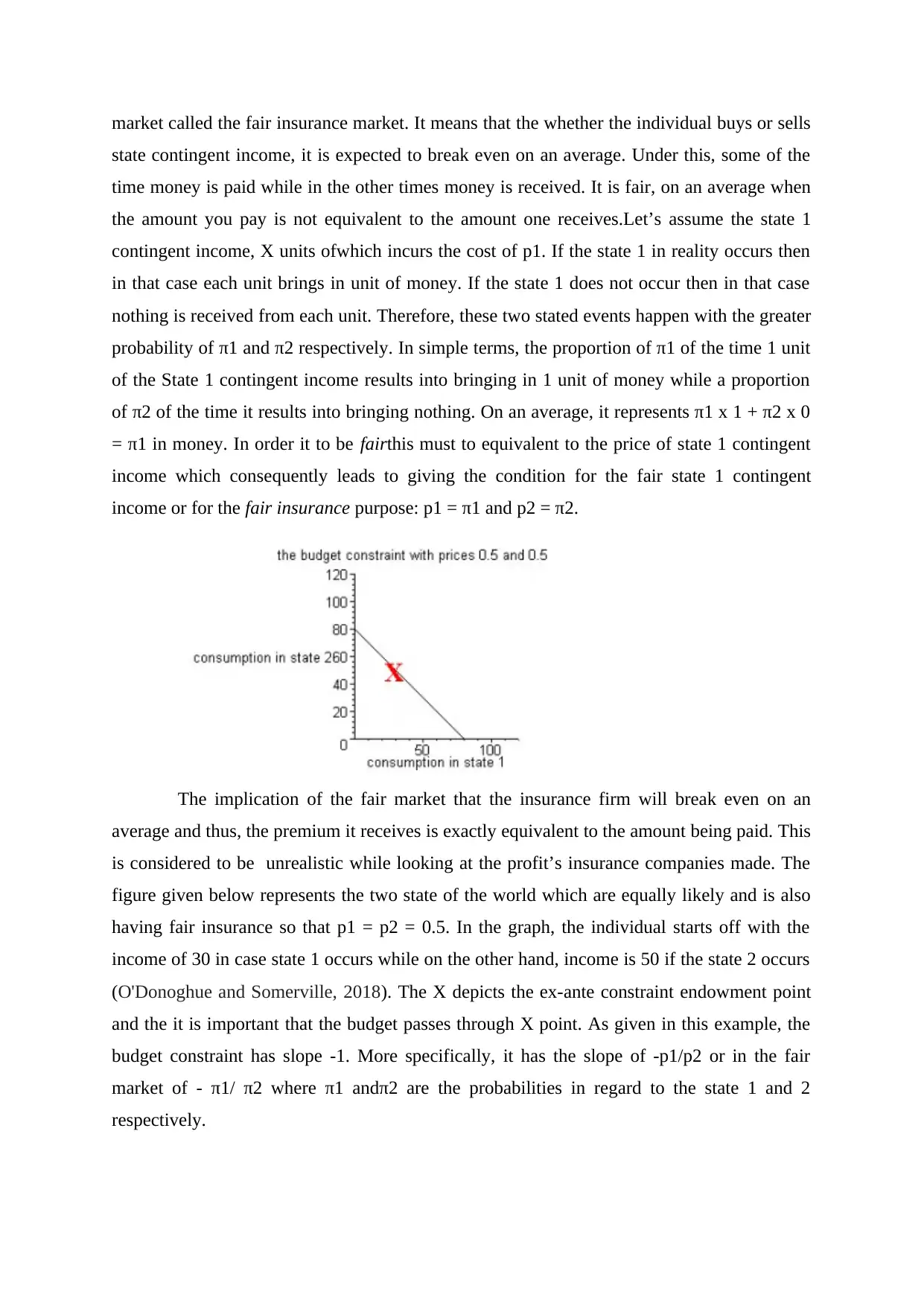

The implication of the fair market that the insurance firm will break even on an

average and thus, the premium it receives is exactly equivalent to the amount being paid. This

is considered to be unrealistic while looking at the profit’s insurance companies made. The

figure given below represents the two state of the world which are equally likely and is also

having fair insurance so that p1 = p2 = 0.5. In the graph, the individual starts off with the

income of 30 in case state 1 occurs while on the other hand, income is 50 if the state 2 occurs

(O'Donoghue and Somerville, 2018). The X depicts the ex-ante constraint endowment point

and the it is important that the budget passes through X point. As given in this example, the

budget constraint has slope -1. More specifically, it has the slope of -p1/p2 or in the fair

market of - π1/ π2 where π1 andπ2 are the probabilities in regard to the state 1 and 2

respectively.

state contingent income, it is expected to break even on an average. Under this, some of the

time money is paid while in the other times money is received. It is fair, on an average when

the amount you pay is not equivalent to the amount one receives.Let’s assume the state 1

contingent income, X units ofwhich incurs the cost of p1. If the state 1 in reality occurs then

in that case each unit brings in unit of money. If the state 1 does not occur then in that case

nothing is received from each unit. Therefore, these two stated events happen with the greater

probability of π1 and π2 respectively. In simple terms, the proportion of π1 of the time 1 unit

of the State 1 contingent income results into bringing in 1 unit of money while a proportion

of π2 of the time it results into bringing nothing. On an average, it represents π1 x 1 + π2 x 0

= π1 in money. In order it to be fairthis must to equivalent to the price of state 1 contingent

income which consequently leads to giving the condition for the fair state 1 contingent

income or for the fair insurance purpose: p1 = π1 and p2 = π2.

The implication of the fair market that the insurance firm will break even on an

average and thus, the premium it receives is exactly equivalent to the amount being paid. This

is considered to be unrealistic while looking at the profit’s insurance companies made. The

figure given below represents the two state of the world which are equally likely and is also

having fair insurance so that p1 = p2 = 0.5. In the graph, the individual starts off with the

income of 30 in case state 1 occurs while on the other hand, income is 50 if the state 2 occurs

(O'Donoghue and Somerville, 2018). The X depicts the ex-ante constraint endowment point

and the it is important that the budget passes through X point. As given in this example, the

budget constraint has slope -1. More specifically, it has the slope of -p1/p2 or in the fair

market of - π1/ π2 where π1 andπ2 are the probabilities in regard to the state 1 and 2

respectively.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

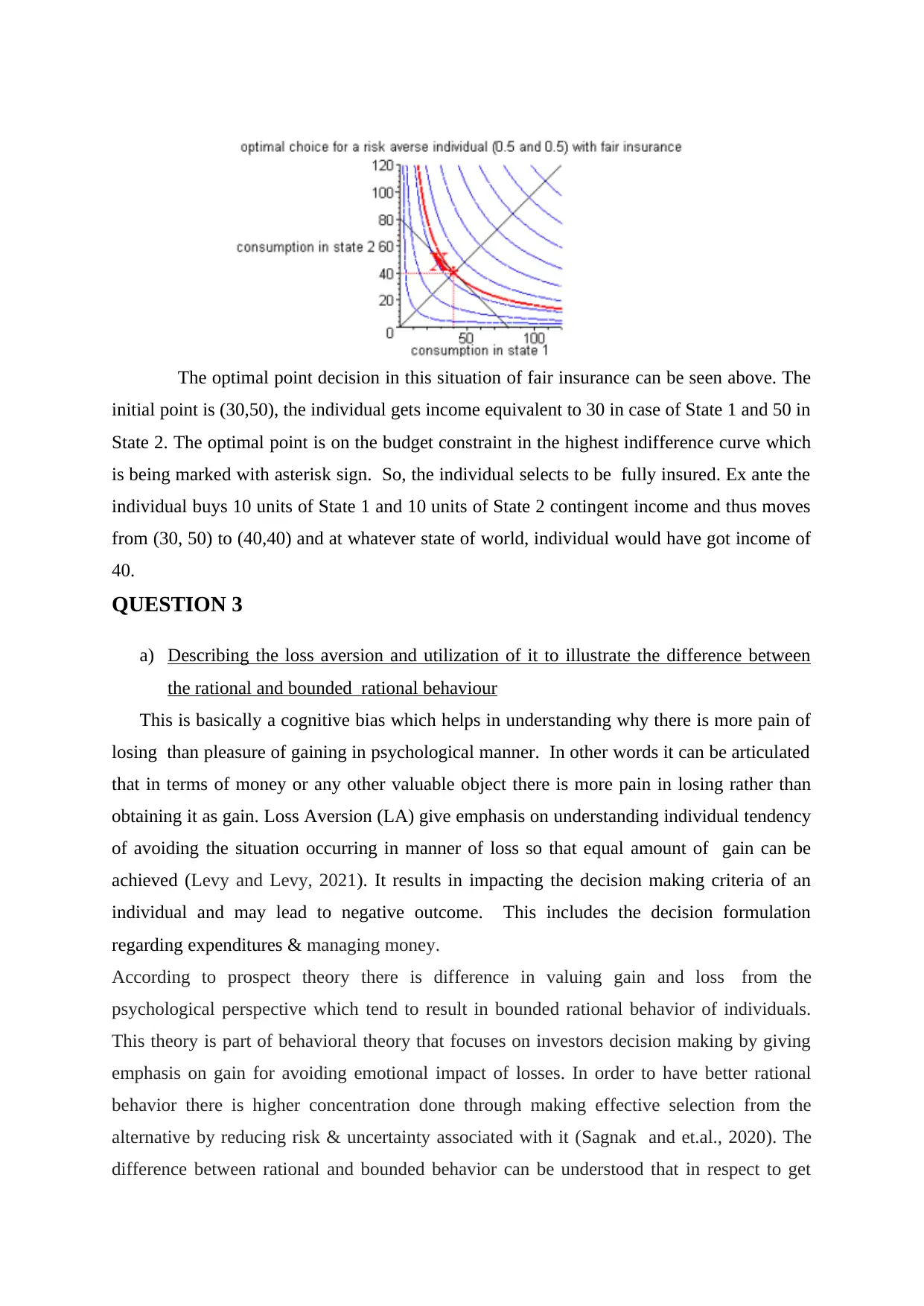

The optimal point decision in this situation of fair insurance can be seen above. The

initial point is (30,50), the individual gets income equivalent to 30 in case of State 1 and 50 in

State 2. The optimal point is on the budget constraint in the highest indifference curve which

is being marked with asterisk sign. So, the individual selects to be fully insured. Ex ante the

individual buys 10 units of State 1 and 10 units of State 2 contingent income and thus moves

from (30, 50) to (40,40) and at whatever state of world, individual would have got income of

40.

QUESTION 3

a) Describing the loss aversion and utilization of it to illustrate the difference between

the rational and bounded rational behaviour

This is basically a cognitive bias which helps in understanding why there is more pain of

losing than pleasure of gaining in psychological manner. In other words it can be articulated

that in terms of money or any other valuable object there is more pain in losing rather than

obtaining it as gain. Loss Aversion (LA) give emphasis on understanding individual tendency

of avoiding the situation occurring in manner of loss so that equal amount of gain can be

achieved (Levy and Levy, 2021). It results in impacting the decision making criteria of an

individual and may lead to negative outcome. This includes the decision formulation

regarding expenditures & managing money.

According to prospect theory there is difference in valuing gain and loss from the

psychological perspective which tend to result in bounded rational behavior of individuals.

This theory is part of behavioral theory that focuses on investors decision making by giving

emphasis on gain for avoiding emotional impact of losses. In order to have better rational

behavior there is higher concentration done through making effective selection from the

alternative by reducing risk & uncertainty associated with it (Sagnak and et.al., 2020). The

difference between rational and bounded behavior can be understood that in respect to get

initial point is (30,50), the individual gets income equivalent to 30 in case of State 1 and 50 in

State 2. The optimal point is on the budget constraint in the highest indifference curve which

is being marked with asterisk sign. So, the individual selects to be fully insured. Ex ante the

individual buys 10 units of State 1 and 10 units of State 2 contingent income and thus moves

from (30, 50) to (40,40) and at whatever state of world, individual would have got income of

40.

QUESTION 3

a) Describing the loss aversion and utilization of it to illustrate the difference between

the rational and bounded rational behaviour

This is basically a cognitive bias which helps in understanding why there is more pain of

losing than pleasure of gaining in psychological manner. In other words it can be articulated

that in terms of money or any other valuable object there is more pain in losing rather than

obtaining it as gain. Loss Aversion (LA) give emphasis on understanding individual tendency

of avoiding the situation occurring in manner of loss so that equal amount of gain can be

achieved (Levy and Levy, 2021). It results in impacting the decision making criteria of an

individual and may lead to negative outcome. This includes the decision formulation

regarding expenditures & managing money.

According to prospect theory there is difference in valuing gain and loss from the

psychological perspective which tend to result in bounded rational behavior of individuals.

This theory is part of behavioral theory that focuses on investors decision making by giving

emphasis on gain for avoiding emotional impact of losses. In order to have better rational

behavior there is higher concentration done through making effective selection from the

alternative by reducing risk & uncertainty associated with it (Sagnak and et.al., 2020). The

difference between rational and bounded behavior can be understood that in respect to get

higher gain individual becomes ready to persue those options that have risk for getting

expected utility to a reference point. As per the rational behavior there is proper framework

for making decision through social & economic decisions. In bounded rational behavior there

is limitation of available information & cognitive perspective and finite duration for making

decision. Bounded rational behavior is due to cognitive limitations of minds, information and

finite time that leads to an inappropriate decision. This happens due to lack of resources

available to reach optimal solution. On the other side there is sufficient resources available

to make proper decision that can provide effectual outcome that are optimal. On the basis of

this, it can be articulated that the difference between mentioned type of behavior obtains due

to presence of resources that lead to make ration or bounded behavior.

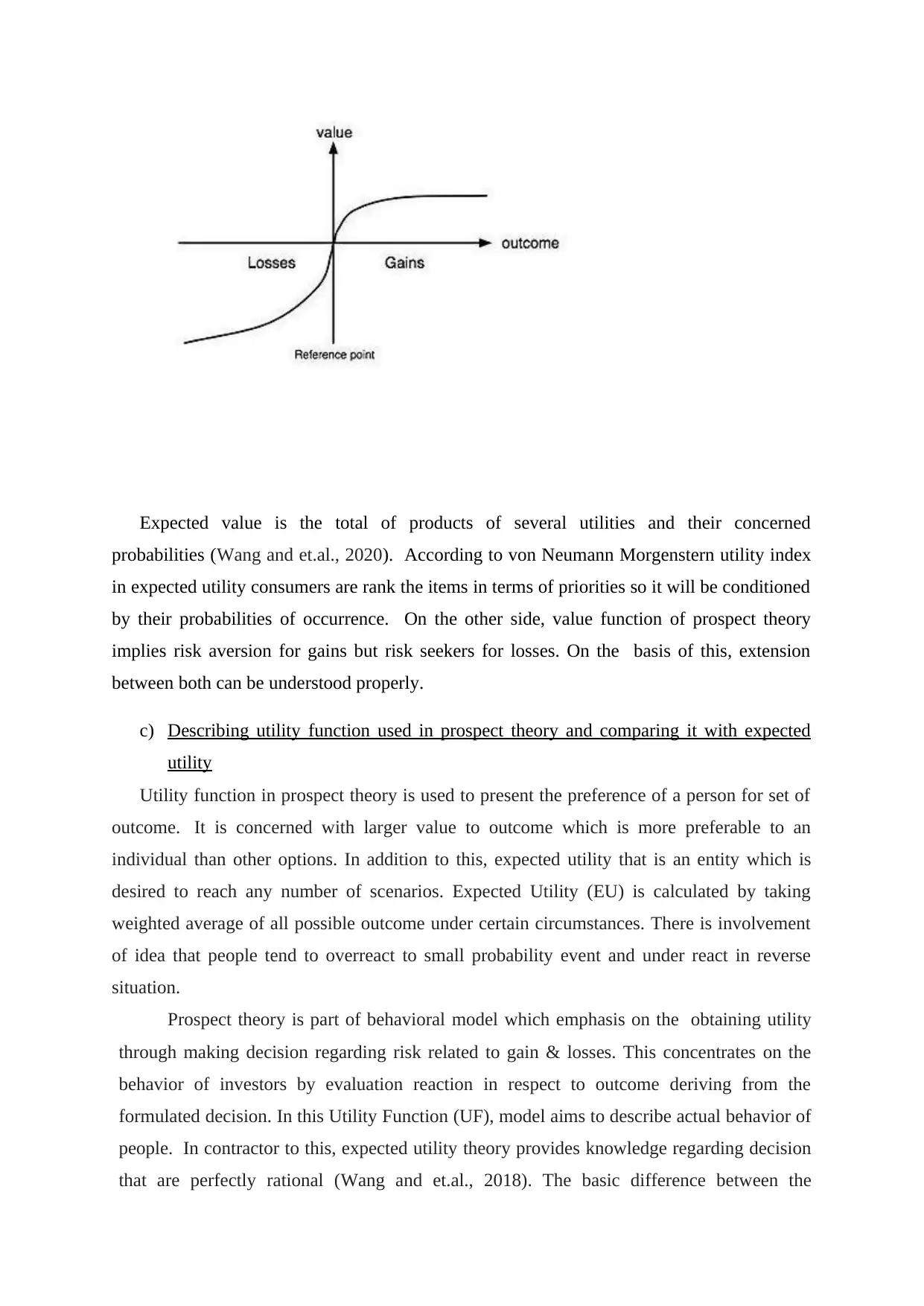

b) Discussing the value function in prospect theory and role of reference point

According to this specified theory, individuals are the risk averse in respect of gains

and on the other side there is threat seeking regarding losses which results in having S

shaped value function. In this prospect theory there is involvement of different type of risk

options which replaces the utility function with value which results in wealth level in terms

of relative loss or gains. Below mentioned diagram can be taken into consideration for

making better evaluation of value function & reference point.

The value function exhibits the psychophysics of diminishing sensitivity. There is

marginal influence of alteration in value diminishes with the distant from relevant reference

point. Reference point play role of determining how an outcome is perceived in prospect

theory. There is strong argument regarding the people evaluation in respect to the results.

This is revealed from the behavior and key preference is formulated as a consistency property

for attitudes toward probabilities (Wang, Wang and Martínez, 2017). From the evaluation of

below mentioned diagram it can be on x axis outcome and on y axis value is plotted.

According to this model, reference point is dependent of several factors and creates risk

attitude. In order to express the effect of reference point on the decision there is replacement

of utility function of an individual with value function. In addition to this, it is both outcome

& reference point.

expected utility to a reference point. As per the rational behavior there is proper framework

for making decision through social & economic decisions. In bounded rational behavior there

is limitation of available information & cognitive perspective and finite duration for making

decision. Bounded rational behavior is due to cognitive limitations of minds, information and

finite time that leads to an inappropriate decision. This happens due to lack of resources

available to reach optimal solution. On the other side there is sufficient resources available

to make proper decision that can provide effectual outcome that are optimal. On the basis of

this, it can be articulated that the difference between mentioned type of behavior obtains due

to presence of resources that lead to make ration or bounded behavior.

b) Discussing the value function in prospect theory and role of reference point

According to this specified theory, individuals are the risk averse in respect of gains

and on the other side there is threat seeking regarding losses which results in having S

shaped value function. In this prospect theory there is involvement of different type of risk

options which replaces the utility function with value which results in wealth level in terms

of relative loss or gains. Below mentioned diagram can be taken into consideration for

making better evaluation of value function & reference point.

The value function exhibits the psychophysics of diminishing sensitivity. There is

marginal influence of alteration in value diminishes with the distant from relevant reference

point. Reference point play role of determining how an outcome is perceived in prospect

theory. There is strong argument regarding the people evaluation in respect to the results.

This is revealed from the behavior and key preference is formulated as a consistency property

for attitudes toward probabilities (Wang, Wang and Martínez, 2017). From the evaluation of

below mentioned diagram it can be on x axis outcome and on y axis value is plotted.

According to this model, reference point is dependent of several factors and creates risk

attitude. In order to express the effect of reference point on the decision there is replacement

of utility function of an individual with value function. In addition to this, it is both outcome

& reference point.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expected value is the total of products of several utilities and their concerned

probabilities (Wang and et.al., 2020). According to von Neumann Morgenstern utility index

in expected utility consumers are rank the items in terms of priorities so it will be conditioned

by their probabilities of occurrence. On the other side, value function of prospect theory

implies risk aversion for gains but risk seekers for losses. On the basis of this, extension

between both can be understood properly.

c) Describing utility function used in prospect theory and comparing it with expected

utility

Utility function in prospect theory is used to present the preference of a person for set of

outcome. It is concerned with larger value to outcome which is more preferable to an

individual than other options. In addition to this, expected utility that is an entity which is

desired to reach any number of scenarios. Expected Utility (EU) is calculated by taking

weighted average of all possible outcome under certain circumstances. There is involvement

of idea that people tend to overreact to small probability event and under react in reverse

situation.

Prospect theory is part of behavioral model which emphasis on the obtaining utility

through making decision regarding risk related to gain & losses. This concentrates on the

behavior of investors by evaluation reaction in respect to outcome deriving from the

formulated decision. In this Utility Function (UF), model aims to describe actual behavior of

people. In contractor to this, expected utility theory provides knowledge regarding decision

that are perfectly rational (Wang and et.al., 2018). The basic difference between the

probabilities (Wang and et.al., 2020). According to von Neumann Morgenstern utility index

in expected utility consumers are rank the items in terms of priorities so it will be conditioned

by their probabilities of occurrence. On the other side, value function of prospect theory

implies risk aversion for gains but risk seekers for losses. On the basis of this, extension

between both can be understood properly.

c) Describing utility function used in prospect theory and comparing it with expected

utility

Utility function in prospect theory is used to present the preference of a person for set of

outcome. It is concerned with larger value to outcome which is more preferable to an

individual than other options. In addition to this, expected utility that is an entity which is

desired to reach any number of scenarios. Expected Utility (EU) is calculated by taking

weighted average of all possible outcome under certain circumstances. There is involvement

of idea that people tend to overreact to small probability event and under react in reverse

situation.

Prospect theory is part of behavioral model which emphasis on the obtaining utility

through making decision regarding risk related to gain & losses. This concentrates on the

behavior of investors by evaluation reaction in respect to outcome deriving from the

formulated decision. In this Utility Function (UF), model aims to describe actual behavior of

people. In contractor to this, expected utility theory provides knowledge regarding decision

that are perfectly rational (Wang and et.al., 2018). The basic difference between the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

mentioned subject matter can be highlighted that EU is associate with weighted average

utilities of possible outcomes. Utility function of stated criteria as compared to EU measures

the extent to which the outcome is preferred to choices. This is weighted as per the

probabilities that ct will lead to the concerned outcome. EU is more rigorous terms that

describes relationship to choices available to investors. UF is rank results in best, middle

and worst manner whereas EU provides distinct suggestion in the two versions of problems.

Expected utility is fickle and liable to change its advice when there is different explanation

of same issue. From the analysis it can be referred as there is difference in EU & UF in the

mentioned areas that makes them effective to accomplish the purpose of concerned theory.

utilities of possible outcomes. Utility function of stated criteria as compared to EU measures

the extent to which the outcome is preferred to choices. This is weighted as per the

probabilities that ct will lead to the concerned outcome. EU is more rigorous terms that

describes relationship to choices available to investors. UF is rank results in best, middle

and worst manner whereas EU provides distinct suggestion in the two versions of problems.

Expected utility is fickle and liable to change its advice when there is different explanation

of same issue. From the analysis it can be referred as there is difference in EU & UF in the

mentioned areas that makes them effective to accomplish the purpose of concerned theory.

REFERENCES

Books and Journals

Levy, H. and Levy, M., 2021. Prospect theory, constant relative risk aversion, and the

investment horizon. PloS one. 16(4). p.e0248904.

Li, Y. and Xu, Z.Q., 2017. Optimal insurance design with a bonus. Insurance: Mathematics

and Economics. 77. pp.111-118.

Meyers, G. and Van Hoyweghen, I., 2018. Enacting actuarial fairness in insurance: From fair

discrimination to behaviour-based fairness. Science as Culture. 27(4). pp.413-438.

O'Donoghue, T. and Somerville, J., 2018. Modeling risk aversion in economics. Journal of

Economic Perspectives. 32(2). pp.91-114.

Sagnak, M. and et.al., 2020. Decision-making for risk evaluation: integration of prospect

theory with failure modes and effects analysis (FMEA). International

Journal of Quality & Reliability Management.

Wang, L., Wang, Y. M. and Martínez, L., 2017. A group decision method based on prospect

theory for emergency situations. Information Sciences. 418. pp.119-

135.

Wang, T., Li, H and et.al., 2020. A prospect theory-based three-way decision

model. Knowledge-Based Systems. 203. p.106129.

Wang, W. and et.al., 2018. A risk evaluation and prioritization method for FMEA with

prospect theory and Choquet integral. Safety science. 110. pp.152-163.

Online

Expected utilitydecision theory. 2020. [Online]. Available

Through:<https://www.britannica.com/topic/expected-utility>.

Books and Journals

Levy, H. and Levy, M., 2021. Prospect theory, constant relative risk aversion, and the

investment horizon. PloS one. 16(4). p.e0248904.

Li, Y. and Xu, Z.Q., 2017. Optimal insurance design with a bonus. Insurance: Mathematics

and Economics. 77. pp.111-118.

Meyers, G. and Van Hoyweghen, I., 2018. Enacting actuarial fairness in insurance: From fair

discrimination to behaviour-based fairness. Science as Culture. 27(4). pp.413-438.

O'Donoghue, T. and Somerville, J., 2018. Modeling risk aversion in economics. Journal of

Economic Perspectives. 32(2). pp.91-114.

Sagnak, M. and et.al., 2020. Decision-making for risk evaluation: integration of prospect

theory with failure modes and effects analysis (FMEA). International

Journal of Quality & Reliability Management.

Wang, L., Wang, Y. M. and Martínez, L., 2017. A group decision method based on prospect

theory for emergency situations. Information Sciences. 418. pp.119-

135.

Wang, T., Li, H and et.al., 2020. A prospect theory-based three-way decision

model. Knowledge-Based Systems. 203. p.106129.

Wang, W. and et.al., 2018. A risk evaluation and prioritization method for FMEA with

prospect theory and Choquet integral. Safety science. 110. pp.152-163.

Online

Expected utilitydecision theory. 2020. [Online]. Available

Through:<https://www.britannica.com/topic/expected-utility>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.