Microeconomics Principles (ECON111) Assignment: Cashless Debit Card

VerifiedAdded on 2022/12/22

|9

|2223

|1

Essay

AI Summary

This assignment analyzes the Australian government's implementation of the cashless debit card for welfare payments, examining its economic justifications, ethical implications, and consistency with standard economic arguments. The analysis includes a microeconomic perspective, utilizing diagrams to illustrate budget constraints and consumer choices. It explores the ethical framework underlying the program, considering whether the system is justifiable on balance, and discusses arguments for and against the program based on different ethical perspectives. The assignment also addresses the question of whether the card should be applied to all government payment recipients, such as pensioners and students, and provides a detailed explanation of the rationale behind the conclusions. The student explores the arguments against the program and discusses alternative ethical frameworks to evaluate the program's impact on the freedom of choice and welfare of beneficiaries.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

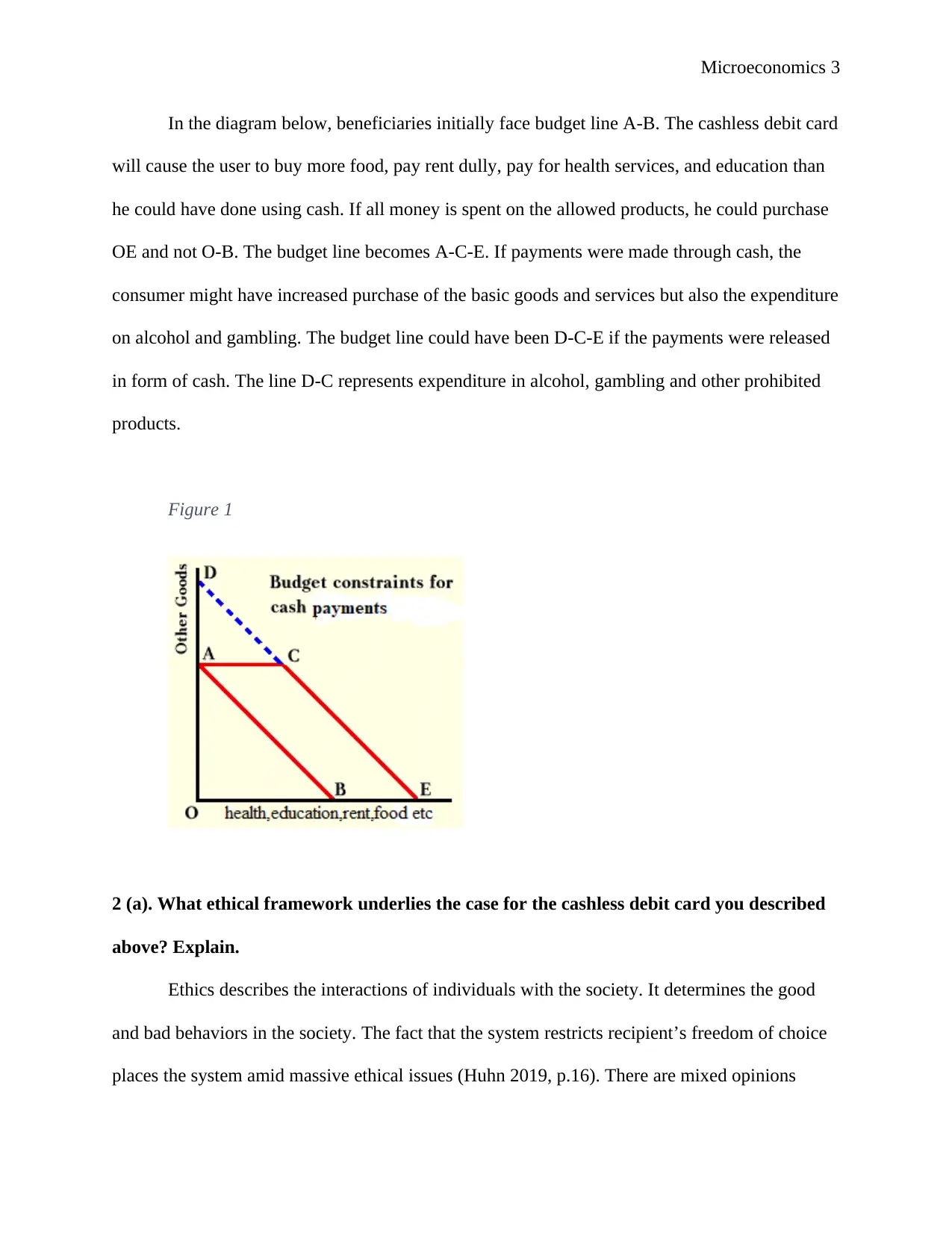

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.