PACC6007 Microeconomics Assignment: Demand, Supply, Cost & Elasticity

VerifiedAdded on 2024/05/20

|14

|1639

|234

Homework Assignment

AI Summary

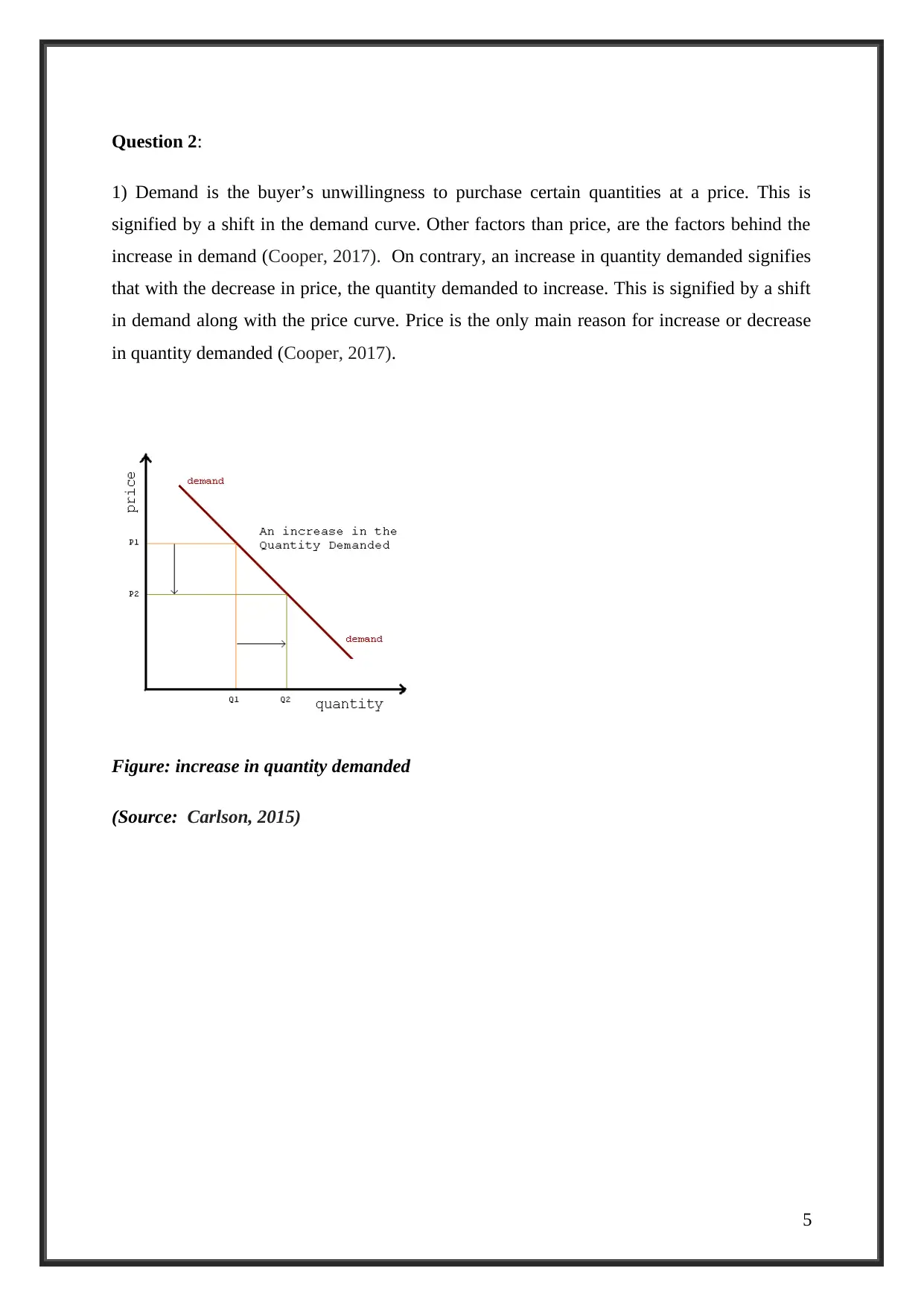

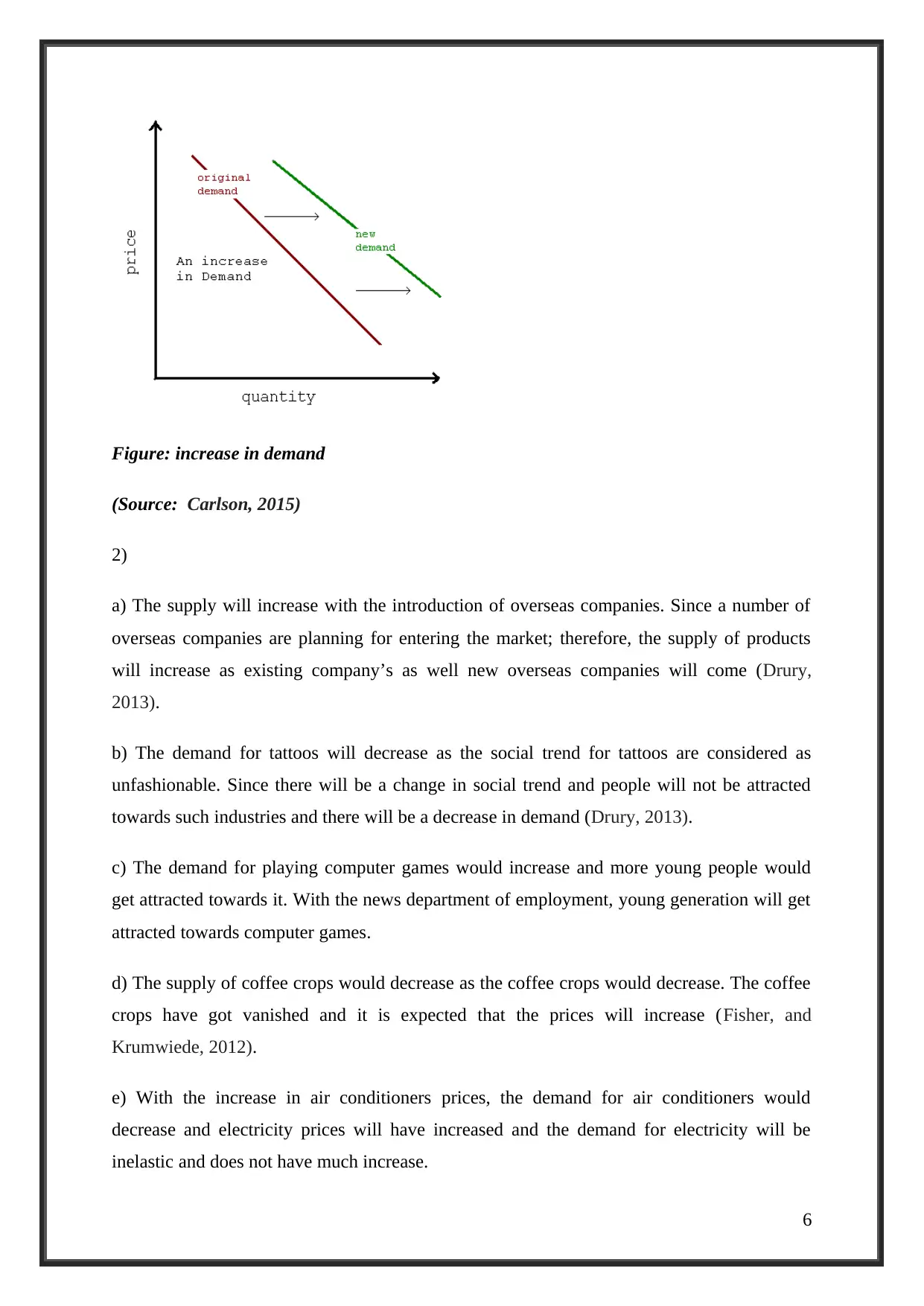

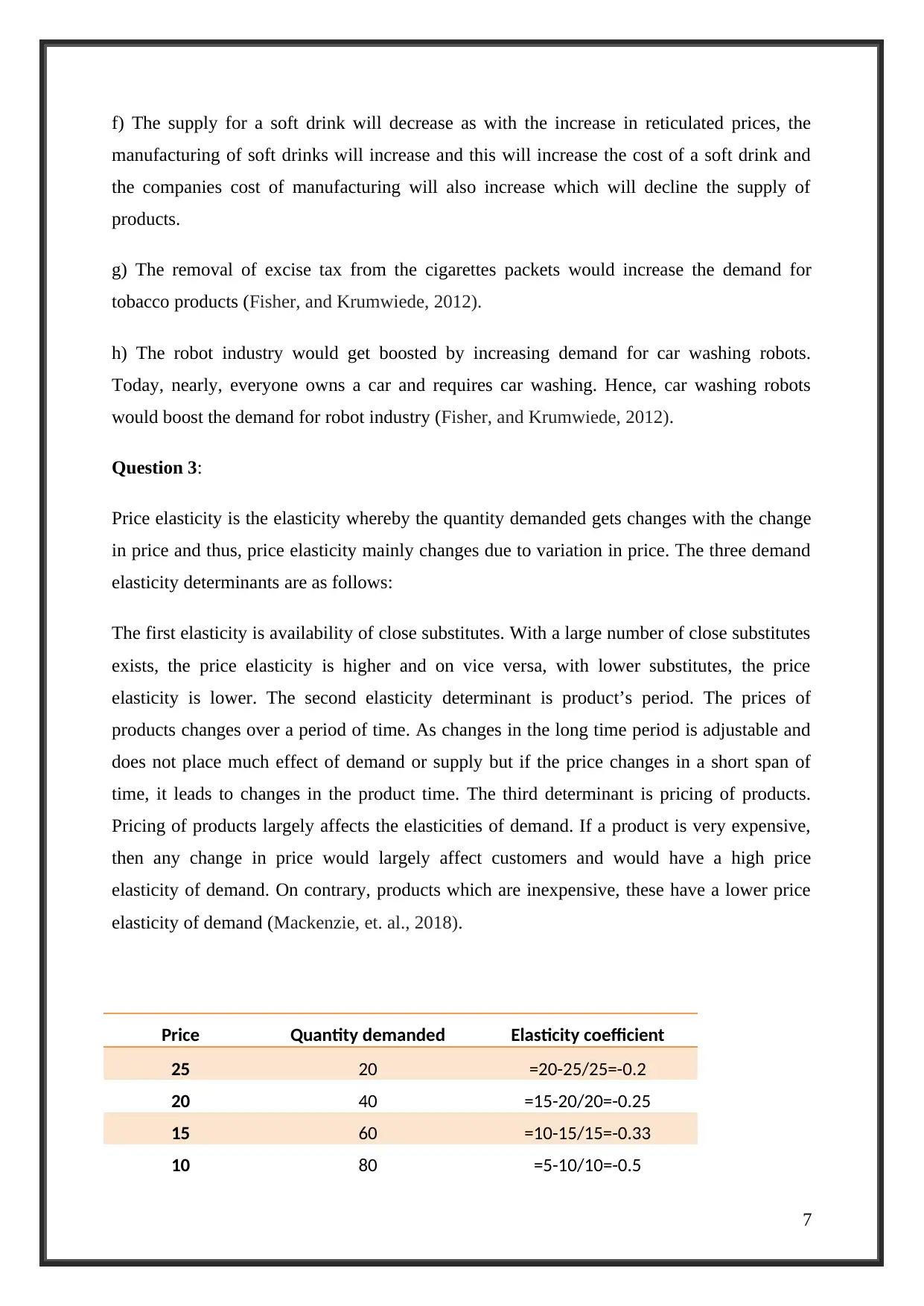

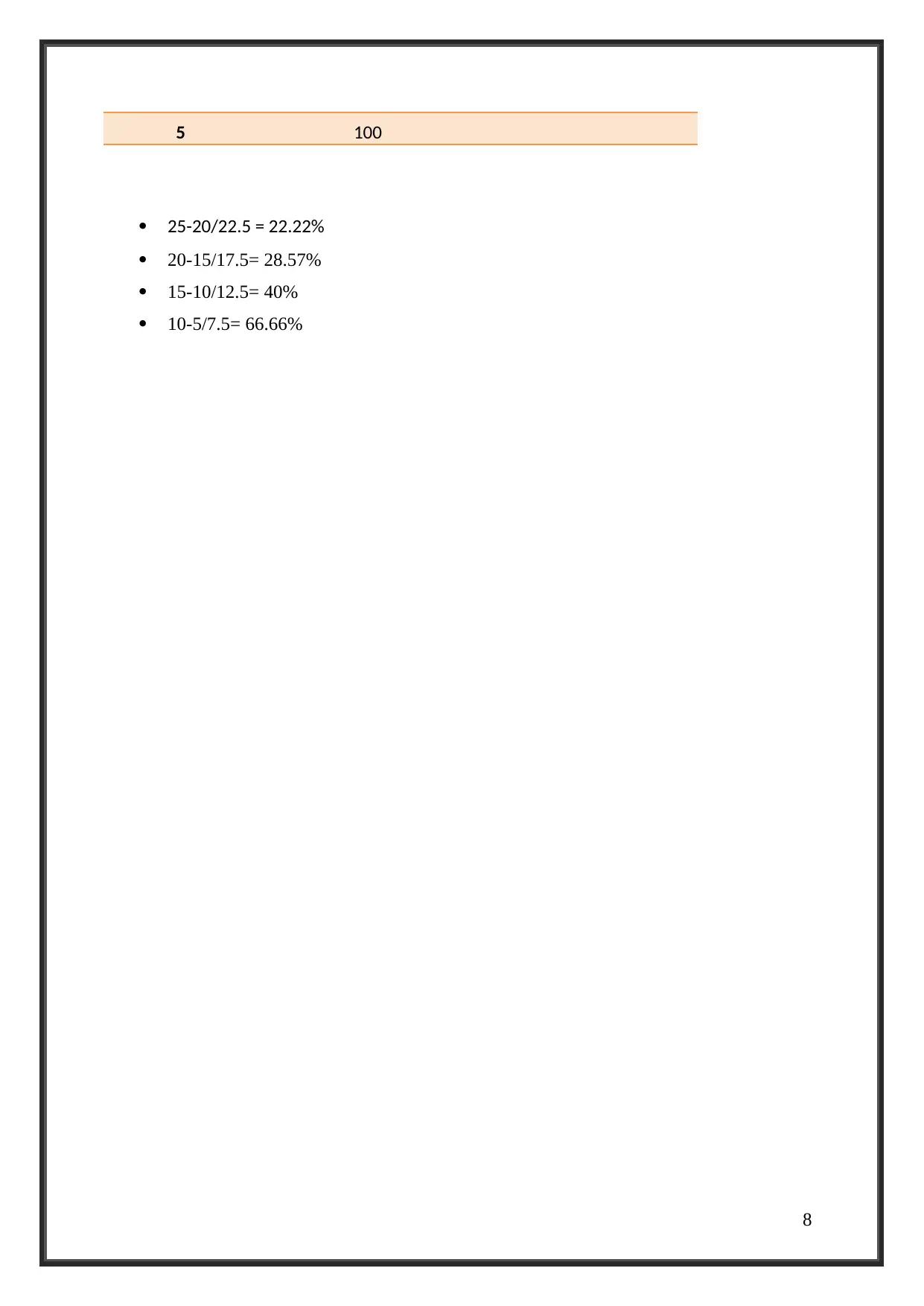

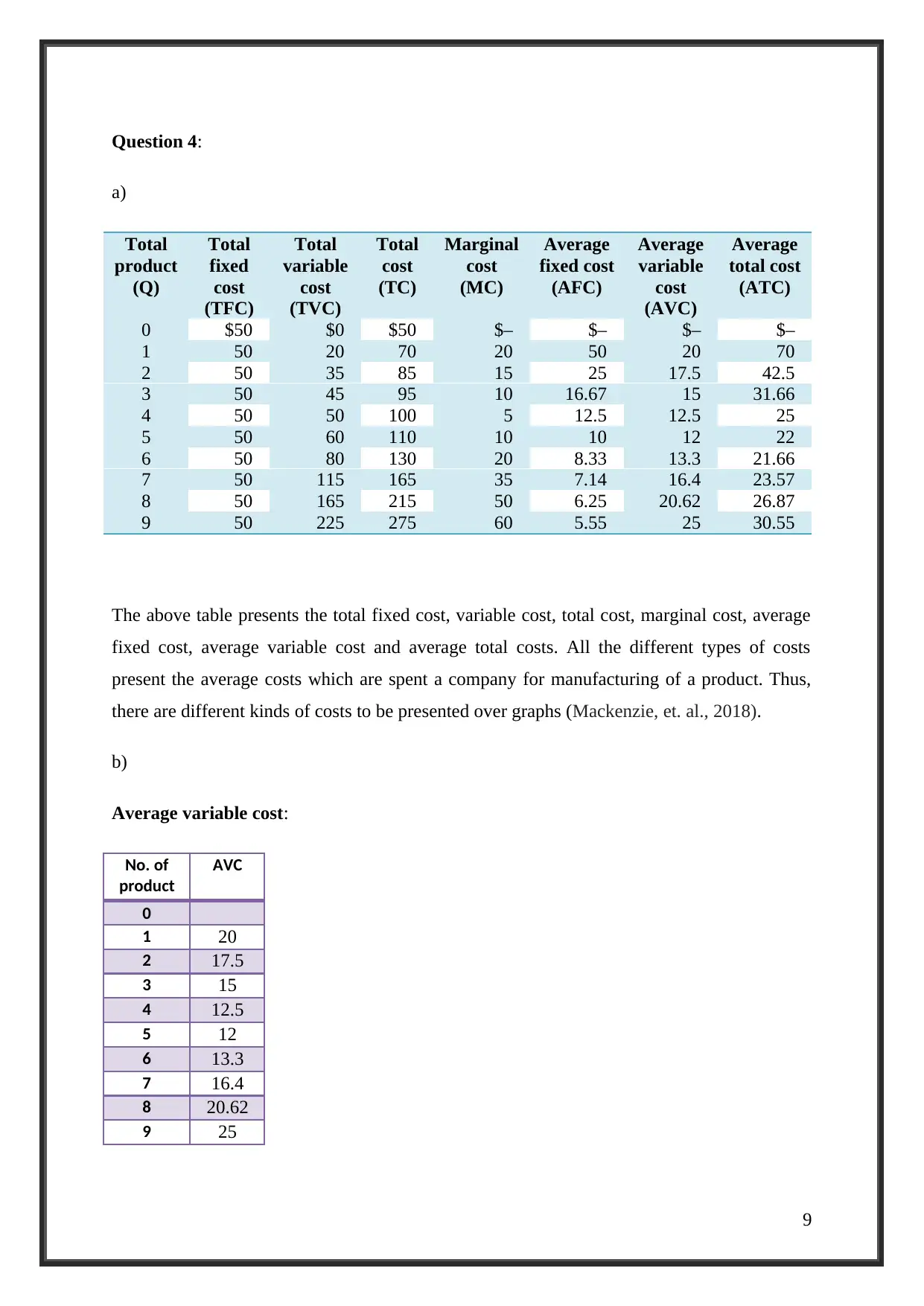

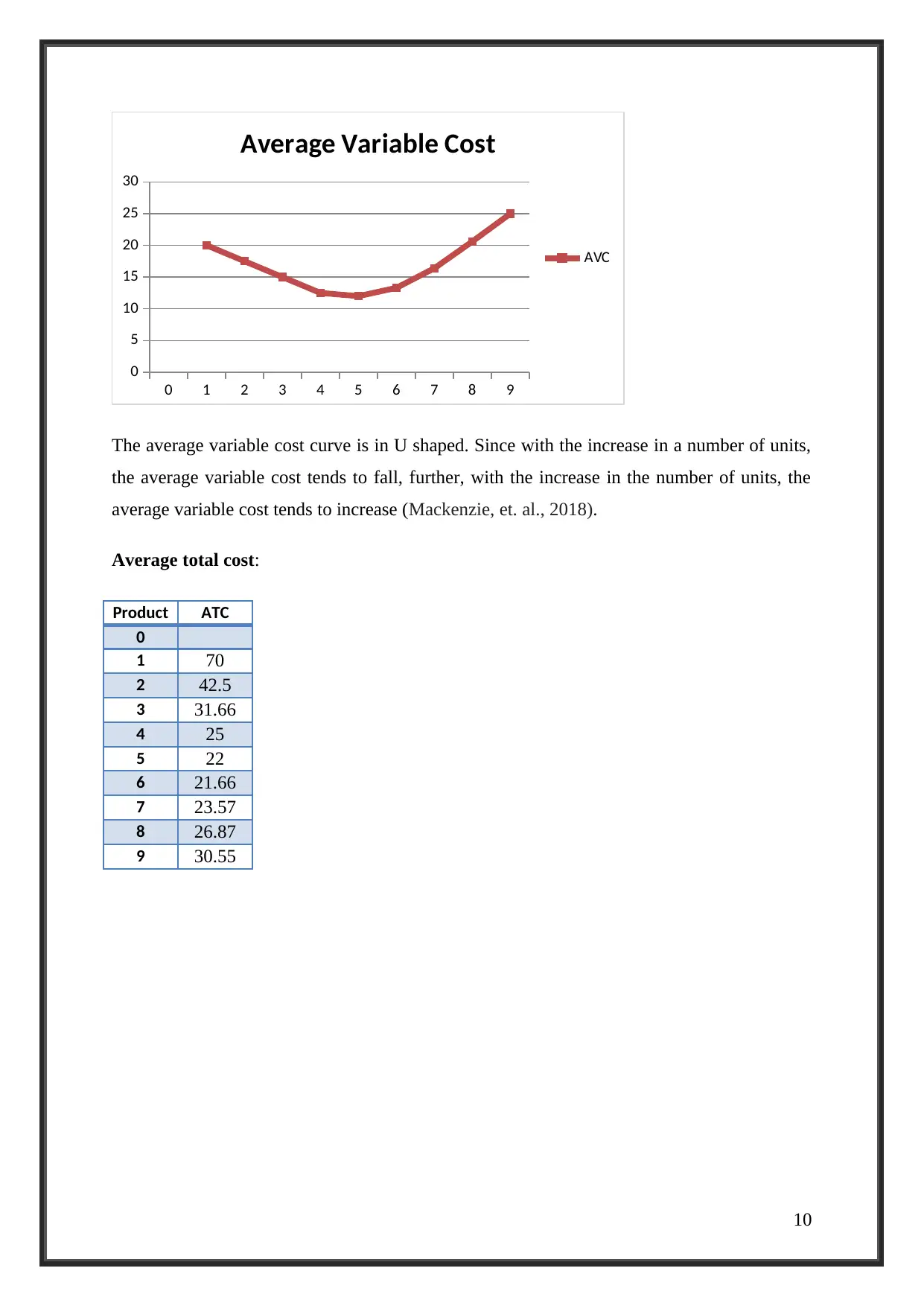

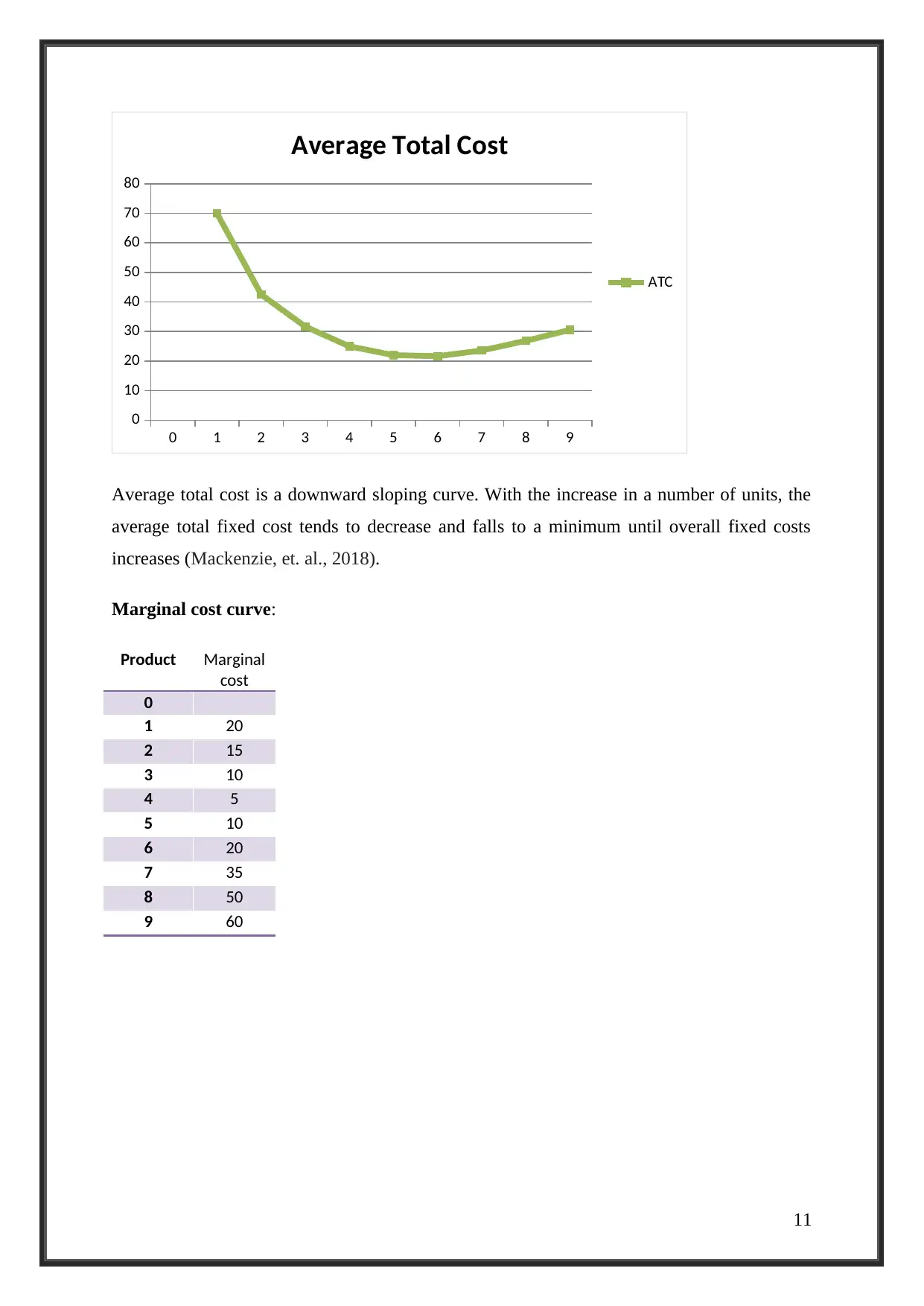

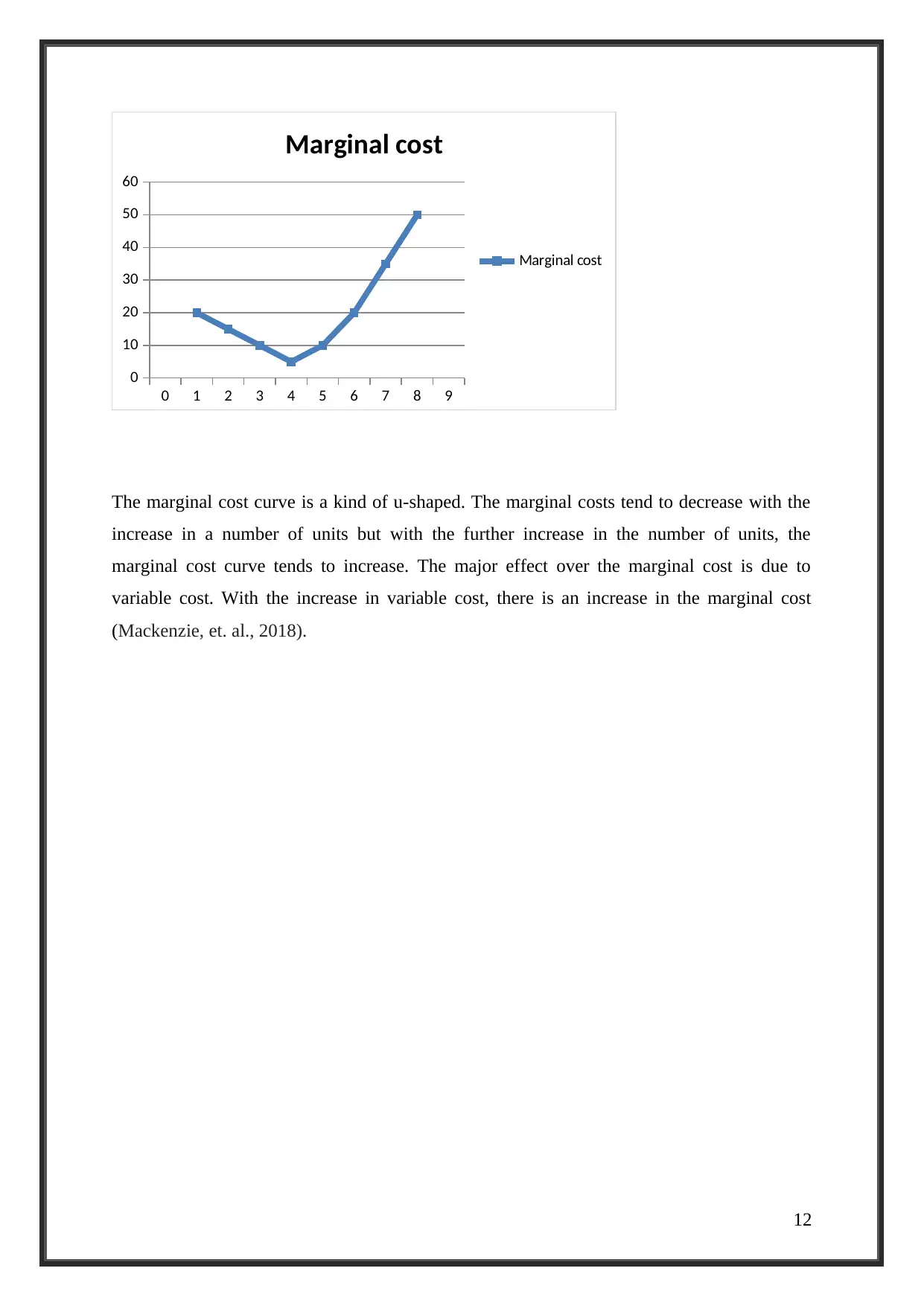

This assignment solution delves into fundamental microeconomic concepts, examining demand, supply, and their related factors. It differentiates between changes in demand and changes in quantity demanded, alongside analyzing the impact of overseas companies and social trends on market dynamics. The assignment further explores price elasticity, its determinants, and provides calculations for elasticity coefficients. Additionally, it includes a detailed cost analysis, presenting total fixed cost, total variable cost, total cost, marginal cost, average fixed cost, average variable cost, and average total costs, accompanied by graphical representations of average variable cost, average total cost, and marginal cost curves. Desklib offers a wide array of solved assignments and past papers to aid students in their academic pursuits.

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.