BBM102/05 Microeconomics TMA 2 Assignment: Economies, Markets

VerifiedAdded on 2023/06/03

|12

|1564

|202

Homework Assignment

AI Summary

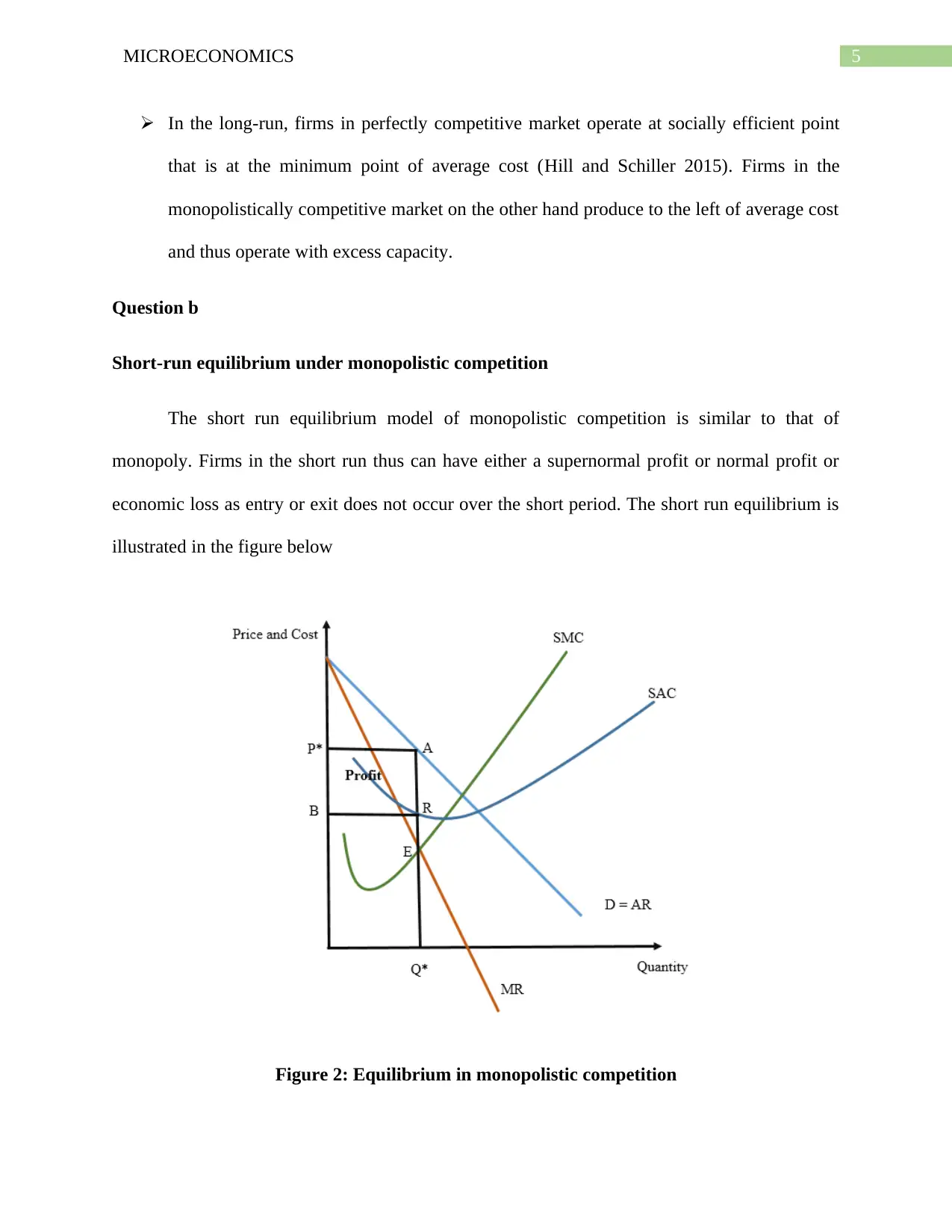

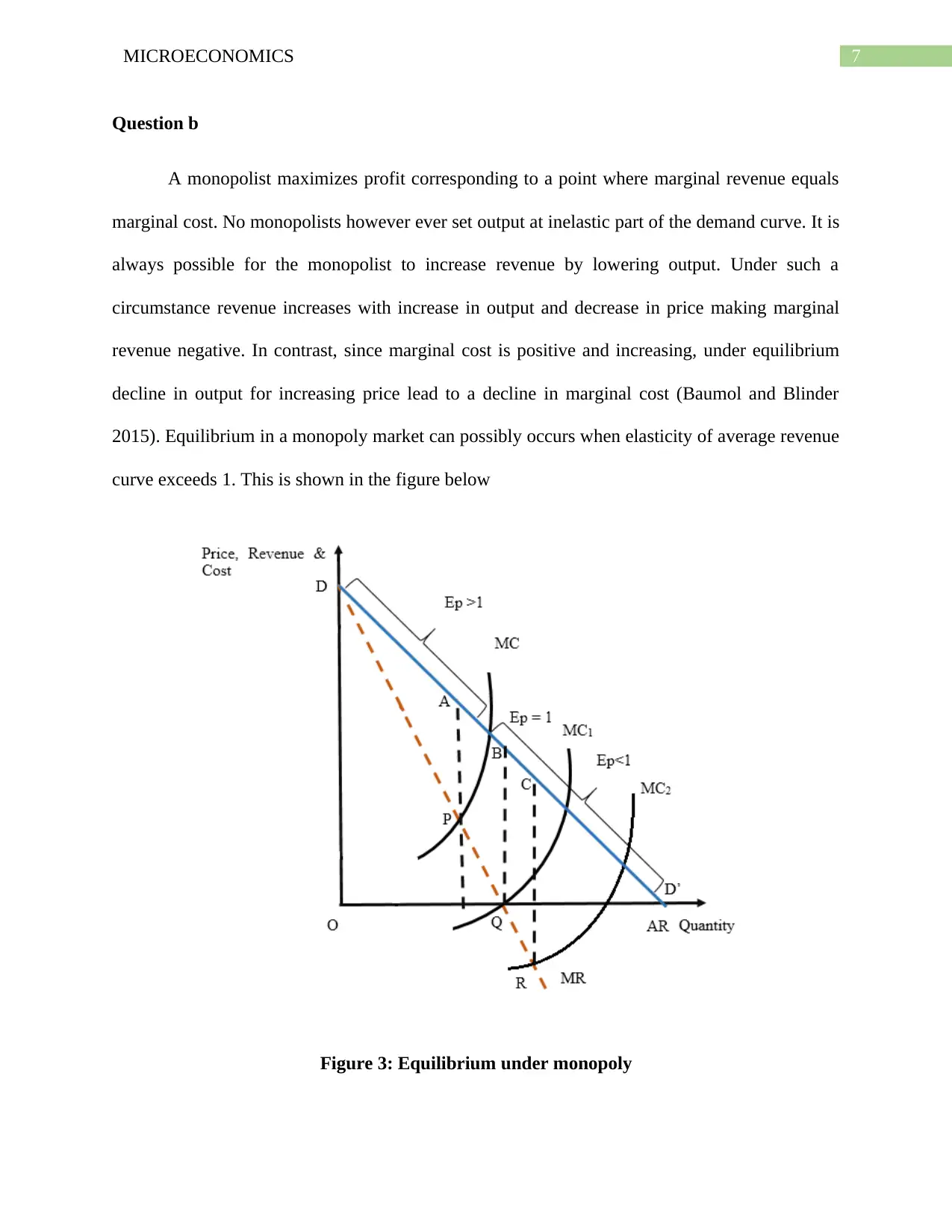

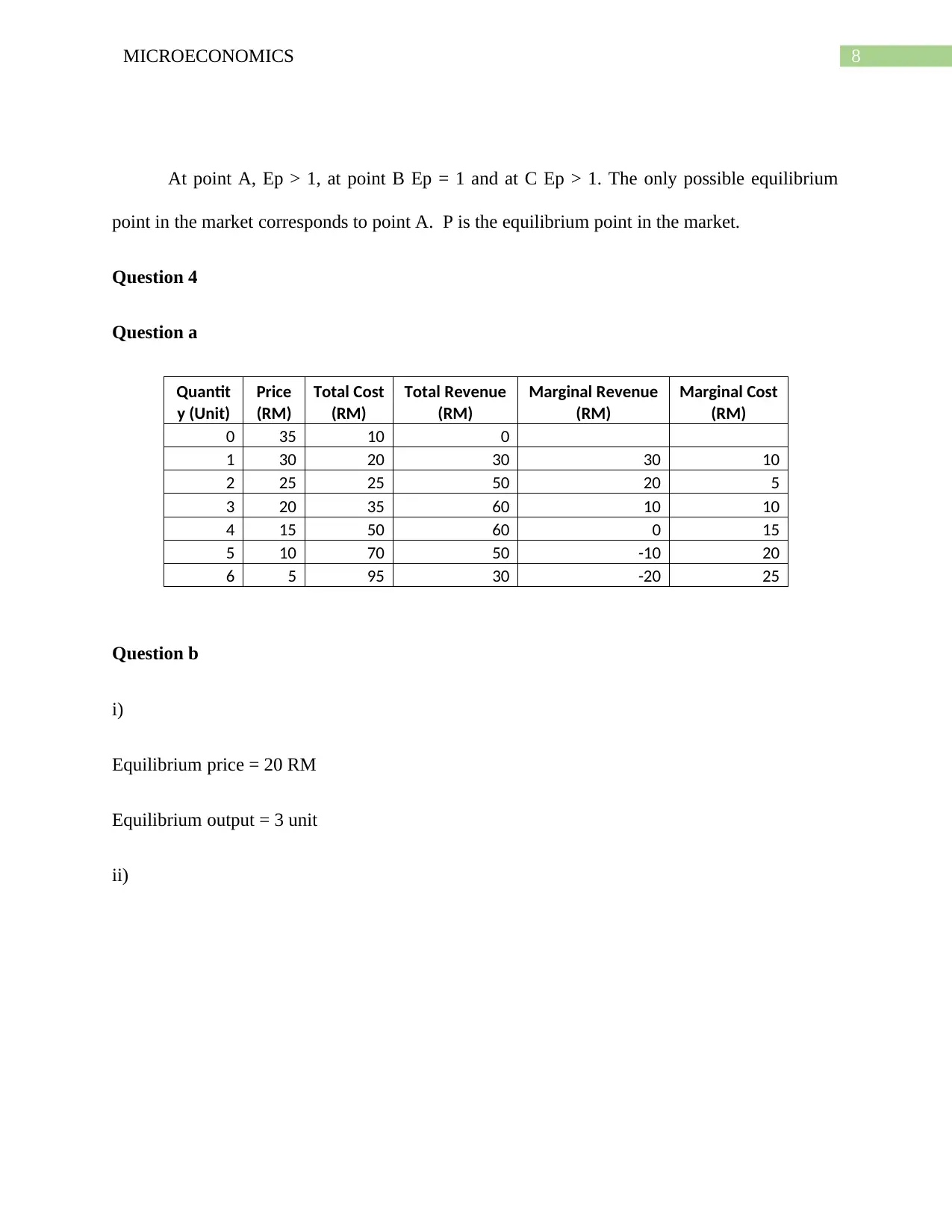

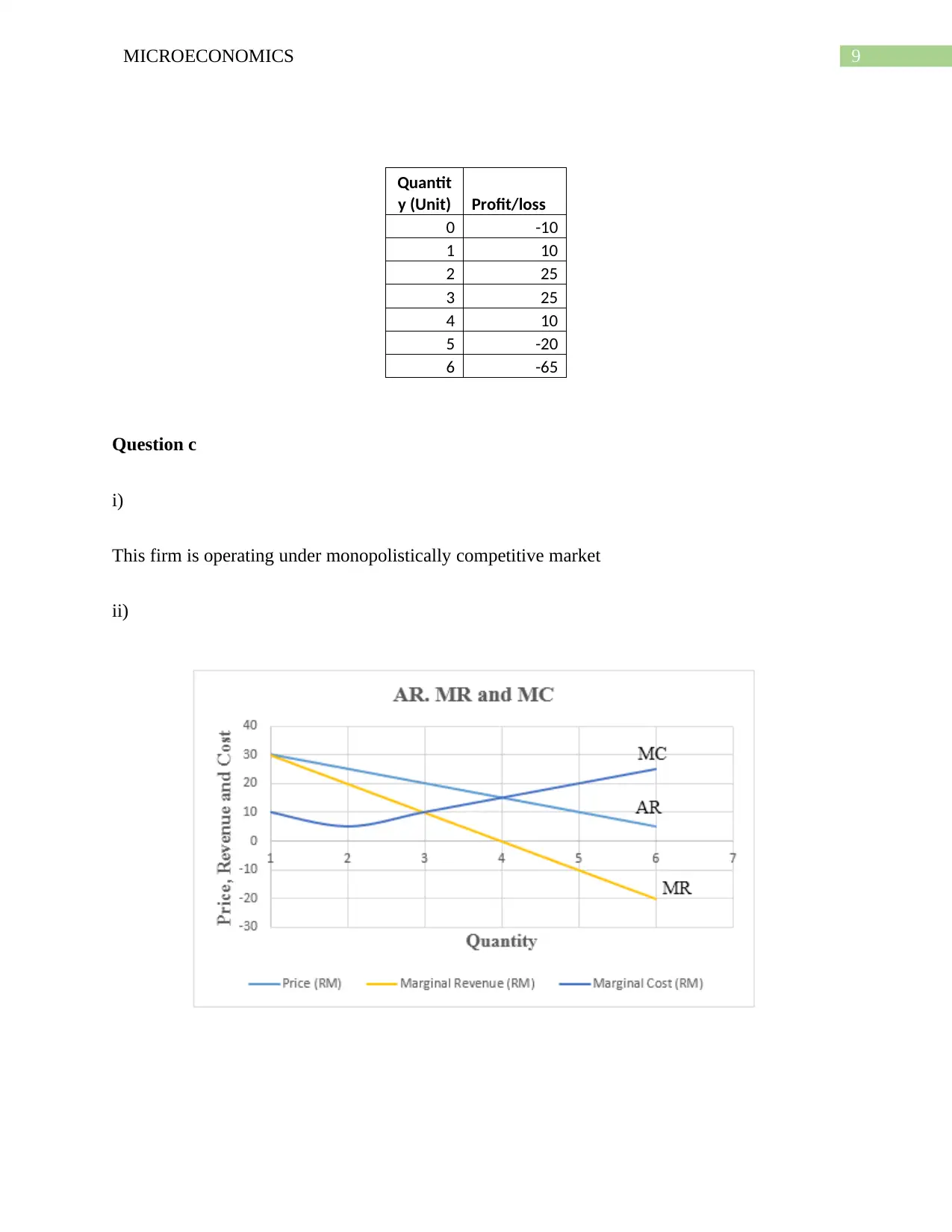

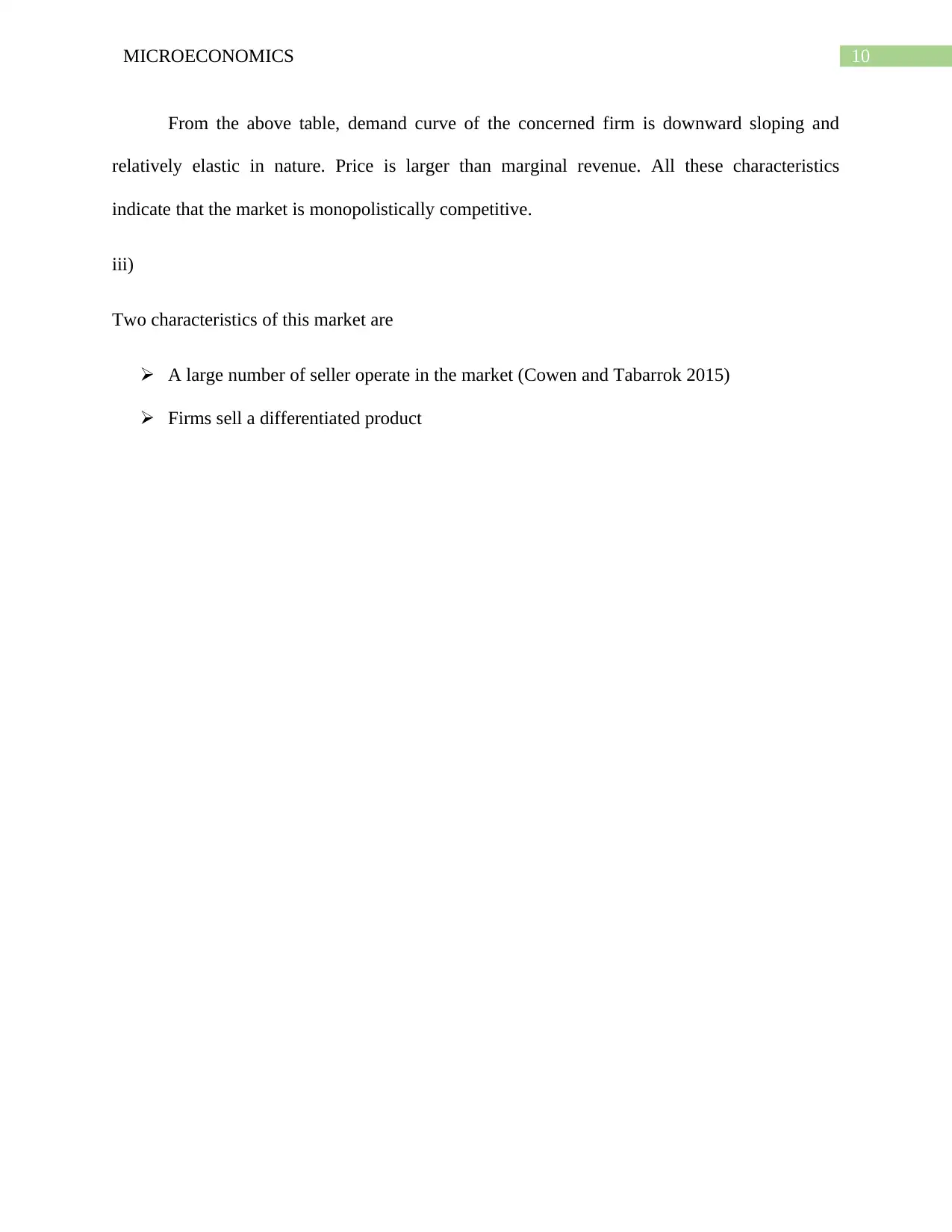

This assignment is a solution to a Tutor-Marked Assignment (TMA 2) for the BBM102/05 Microeconomics course at Wawasan Open University. The assignment covers key microeconomic concepts from Units 3 and 4. Question 1 explores economies and diseconomies of scale, examining the factors that contribute to each. Question 2 analyzes and compares perfect and monopolistic competition, including their similarities, differences, and short-run equilibrium. Question 3 delves into monopoly power, identifying sources such as location and government restrictions, and explaining profit maximization. Question 4 presents a numerical problem involving cost, revenue, and profit calculations, and also requires the identification of market characteristics. The assignment provides detailed explanations, diagrams, and calculations to illustrate the concepts.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.