Economics Assignment: Microeconomic Principles and Market Dynamics

VerifiedAdded on 2020/03/07

|14

|1907

|409

Homework Assignment

AI Summary

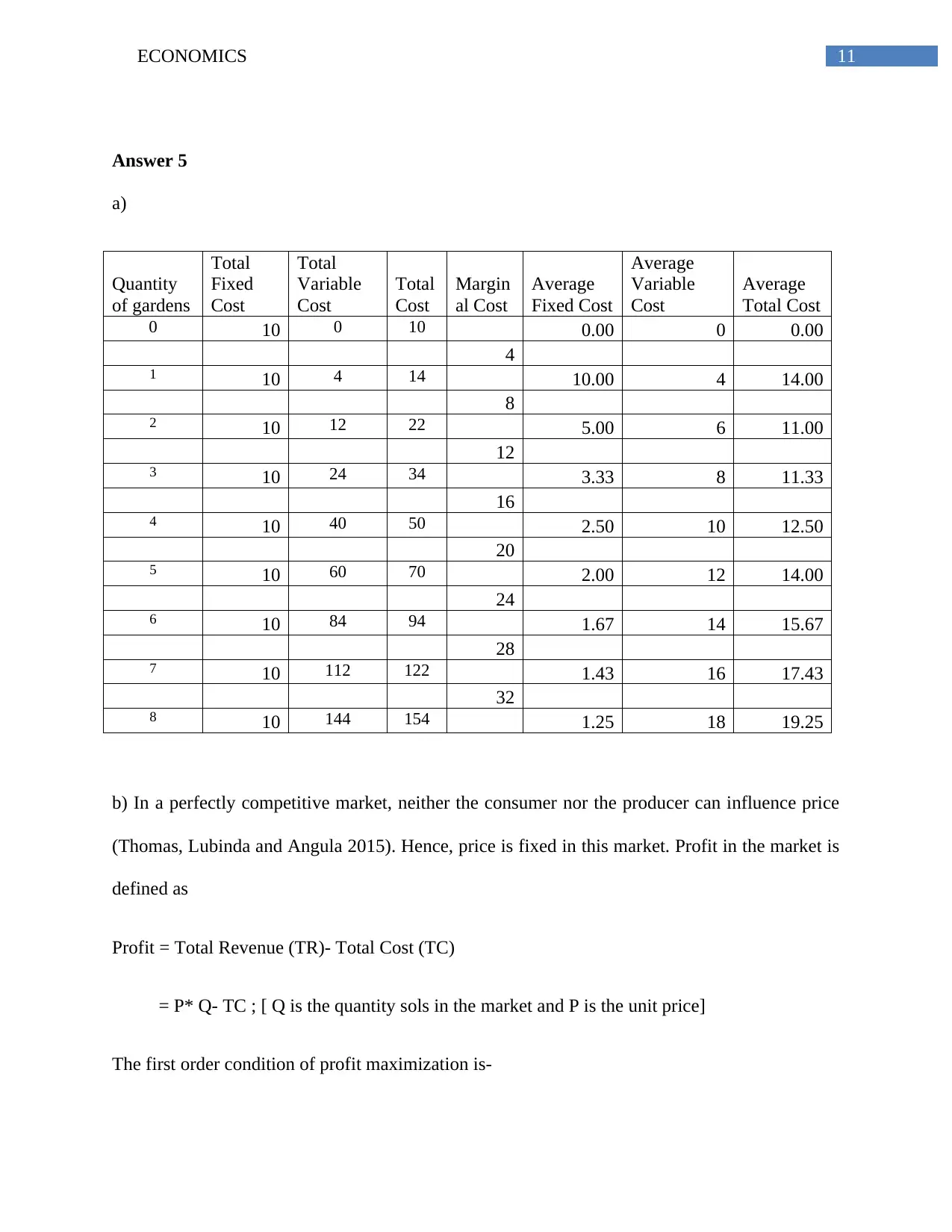

This economics assignment explores fundamental microeconomic principles. It begins by analyzing the production possibility curve and the concept of scarcity, illustrating how limited resources necessitate trade-offs. The assignment then delves into market dynamics, examining supply and demand schedules, equilibrium price and quantity, and consumer and producer surplus. It further investigates how shifts in demand, such as those caused by seasonal changes, affect market outcomes. The assignment also covers government interventions like price floors and their impact on market efficiency and welfare. Elasticity of demand is analyzed in the context of airline tickets, demonstrating how price changes affect consumer behavior. Finally, the assignment explores cost structures in a perfectly competitive market, determining profit-maximizing output levels and illustrating the relationship between marginal cost, average cost, and market price. The assignment concludes with references to relevant economic literature.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.