University Economics Assignment: Problems and Solutions

VerifiedAdded on 2023/01/20

|11

|1889

|47

Homework Assignment

AI Summary

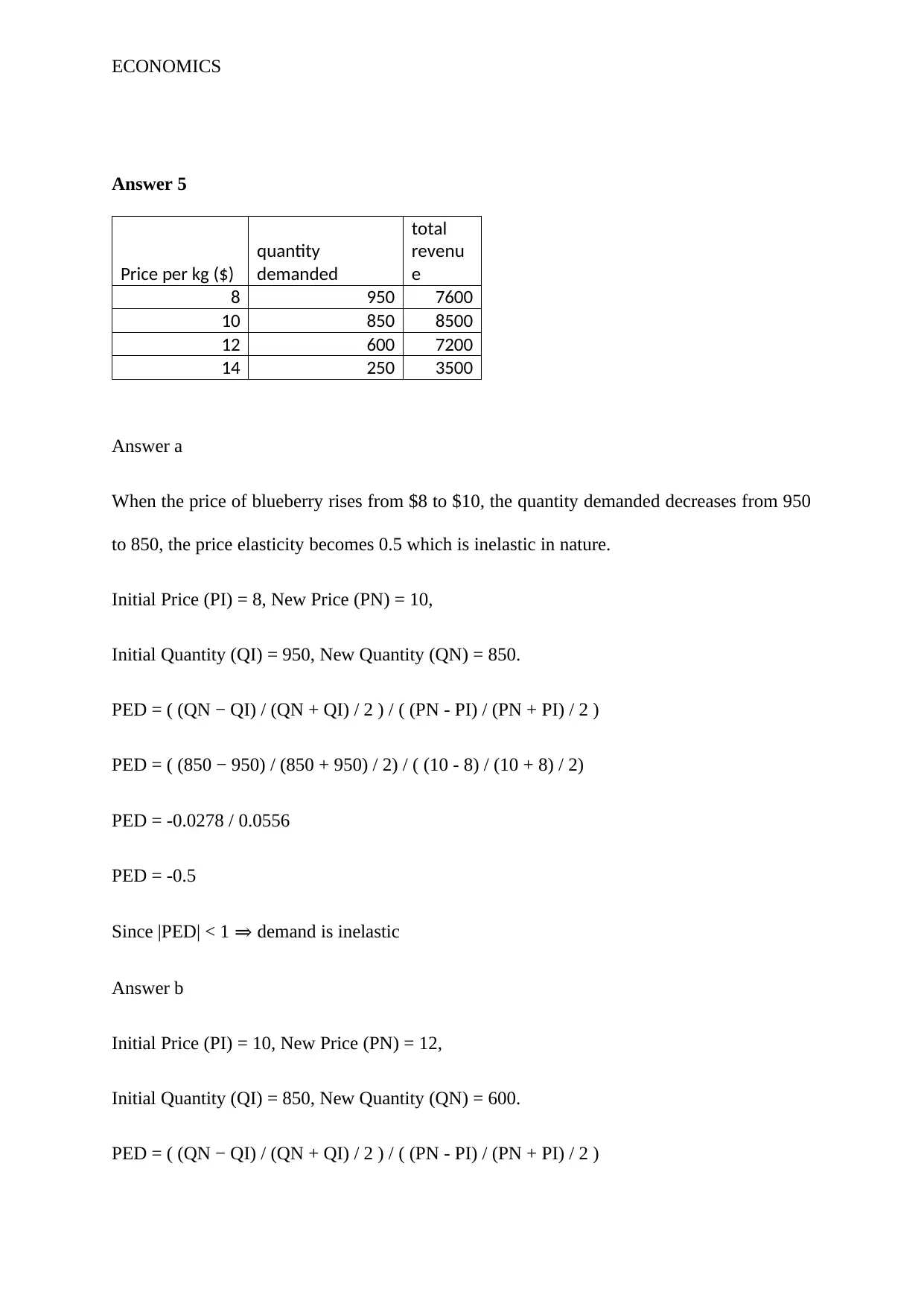

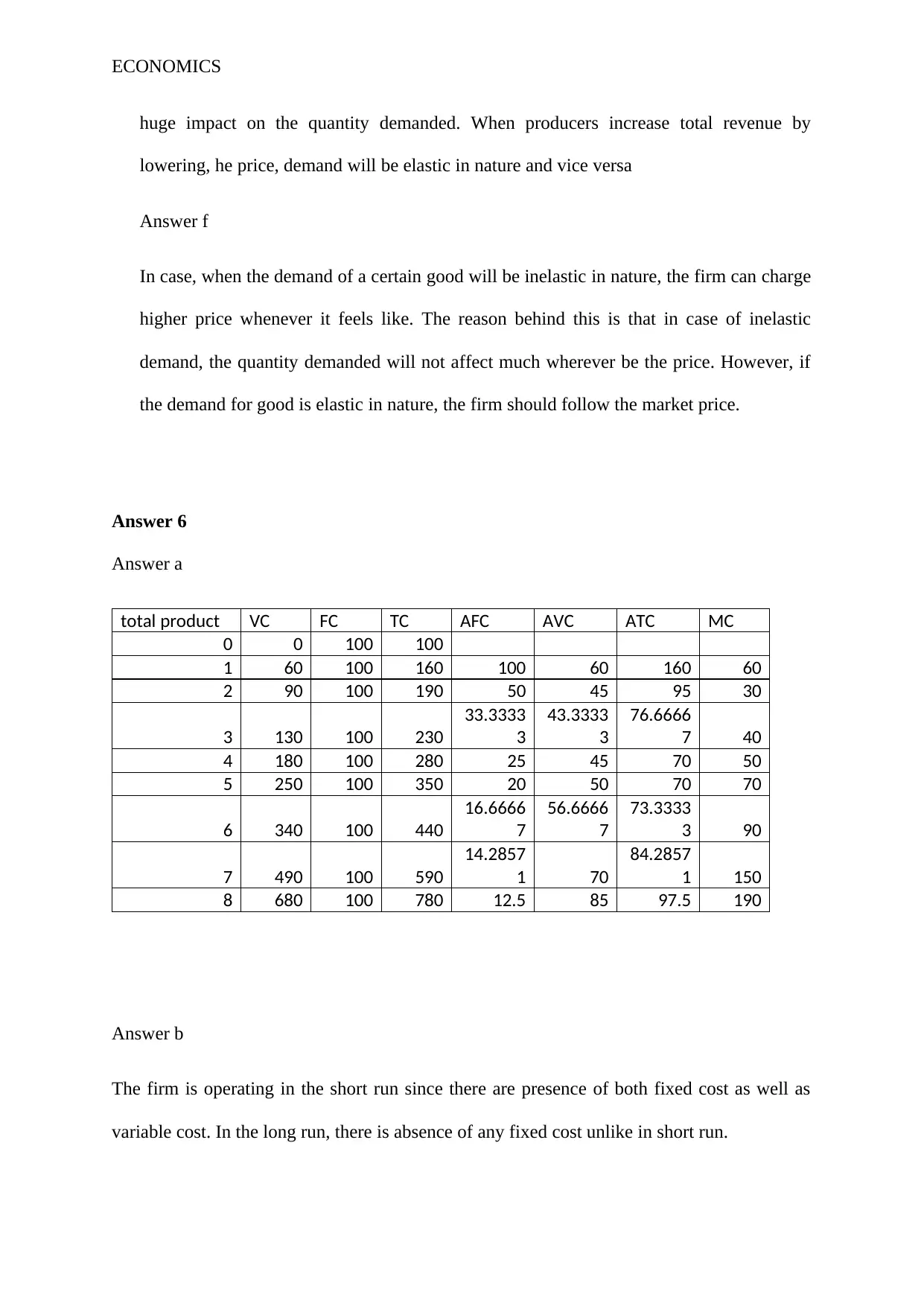

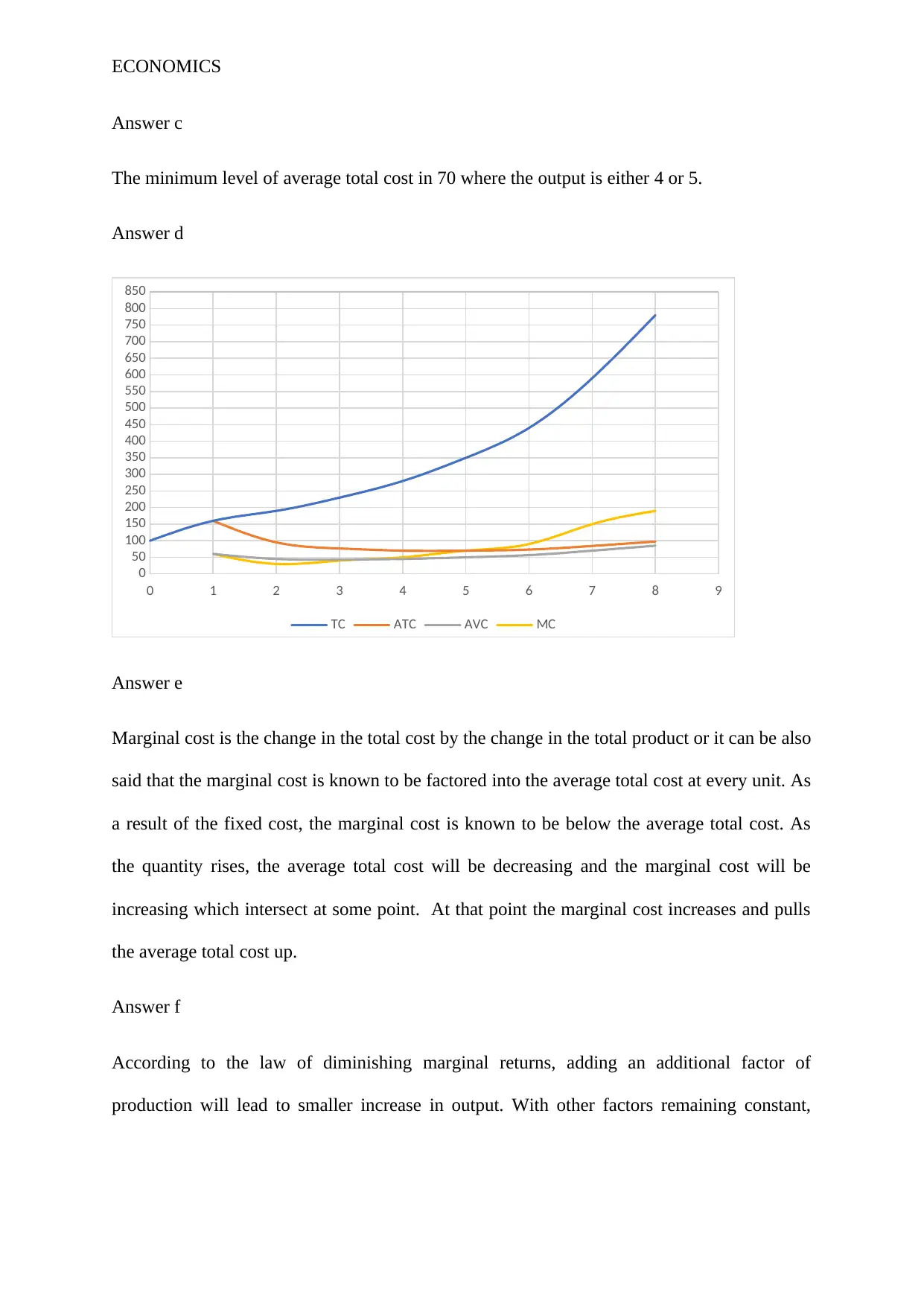

This document provides a comprehensive set of solutions to an economics assignment. The assignment covers key microeconomic concepts, including the economic problem, the three fundamental economic questions, positive and normative economics, and the impact of various factors on the production possibility curve. It also delves into demand and supply analysis, exploring price elasticity, factors affecting demand, and the relationship between price and total revenue. Furthermore, the assignment addresses externalities, illustrating the impact of loud music and vaccinations. Finally, it examines cost analysis, covering total product, fixed and variable costs, marginal cost, and the law of diminishing marginal returns. The solutions are supported by relevant economic theories and include calculations where necessary. The assignment concludes with a reference list of academic resources.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.