Financial Strength and Weakness Analysis of Microsoft (2015)

VerifiedAdded on 2020/01/07

|7

|1229

|175

Report

AI Summary

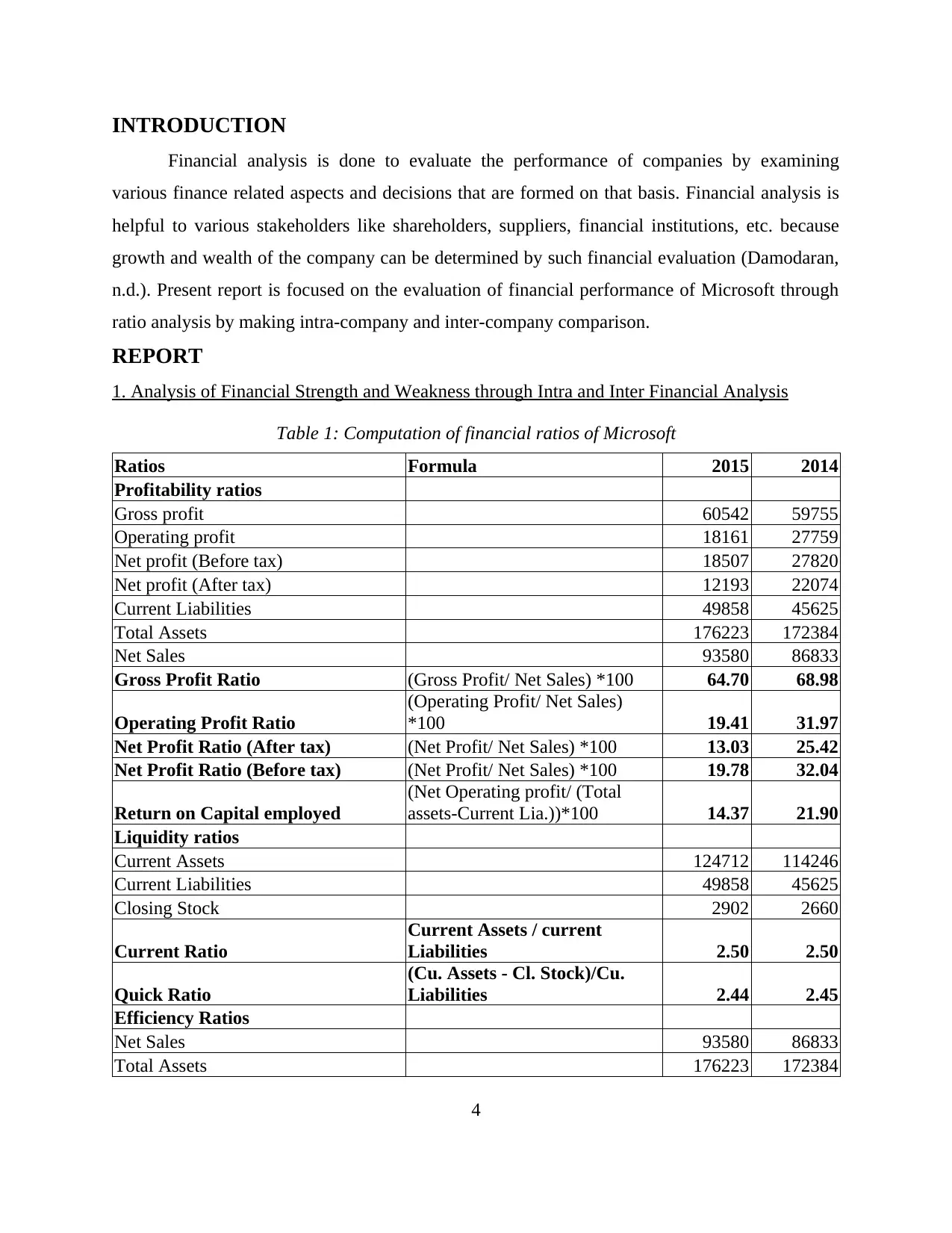

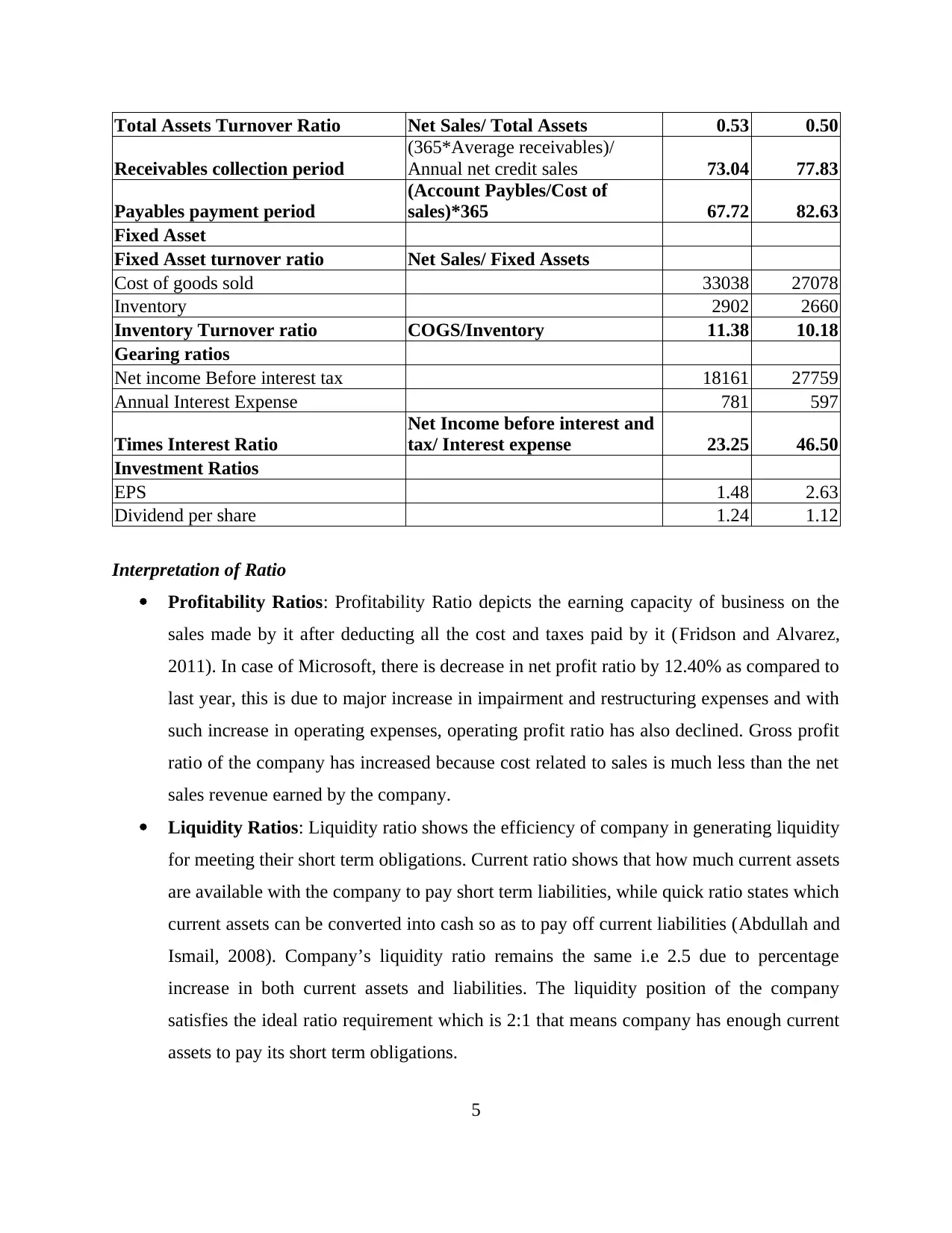

This report presents a financial analysis of Microsoft, focusing on its performance in 2015. The analysis employs various financial ratios, including profitability, liquidity, efficiency, gearing, and investment ratios, to evaluate the company's financial strength and weaknesses. The report provides a detailed computation of these ratios, comparing the results with the previous year (2014) to identify trends and changes in financial health. Key findings include a decrease in net profit ratio due to increased expenses, and a stable liquidity position. The report also discusses efficiency and gearing ratios, along with investment ratios, offering insights into Microsoft's financial management and investment strategies. The analysis is supported by references to relevant financial literature and Microsoft's annual reports.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.