Cost of Capital Analysis for Midland Energy Resources (FIN 632)

VerifiedAdded on 2021/11/17

|8

|1650

|61

Report

AI Summary

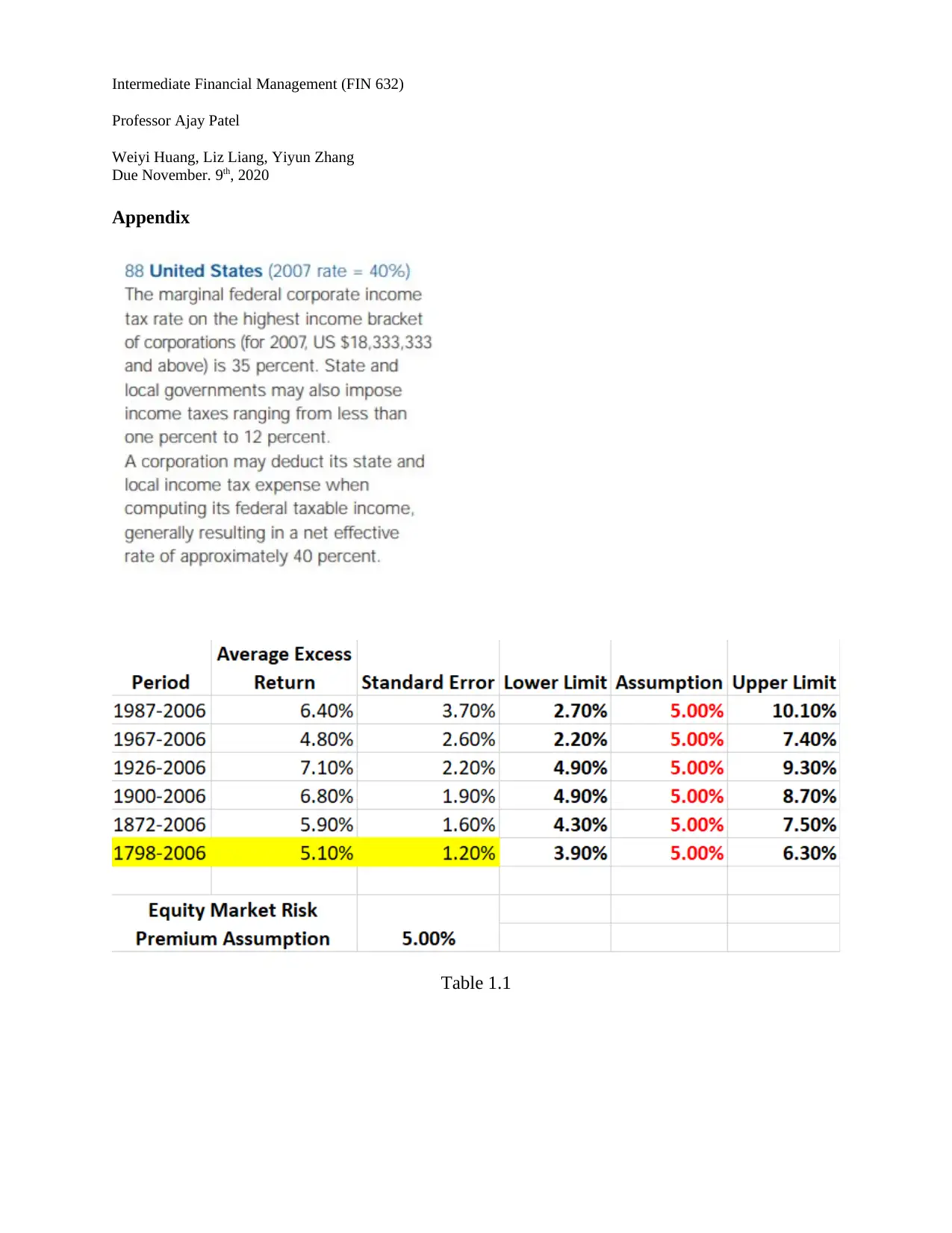

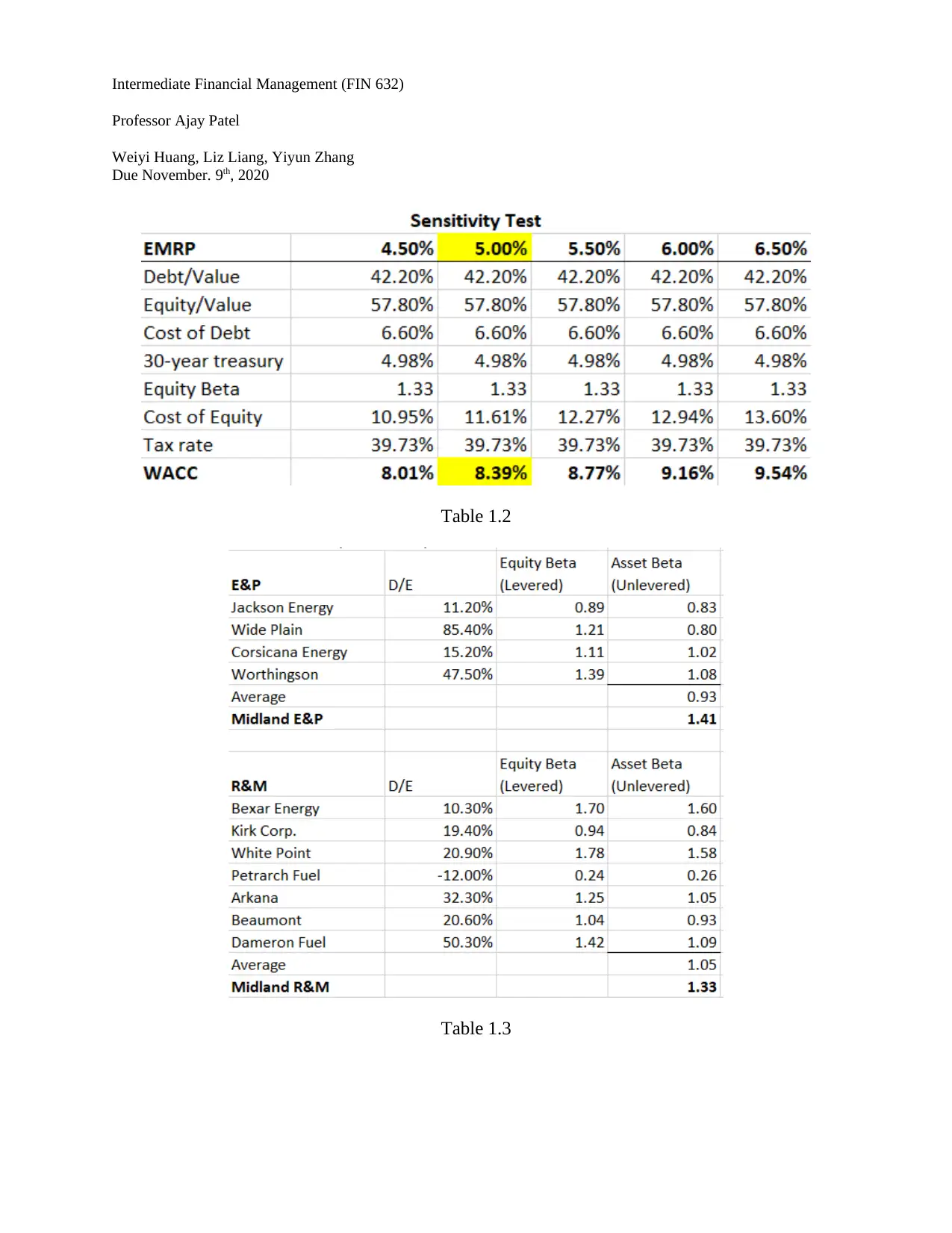

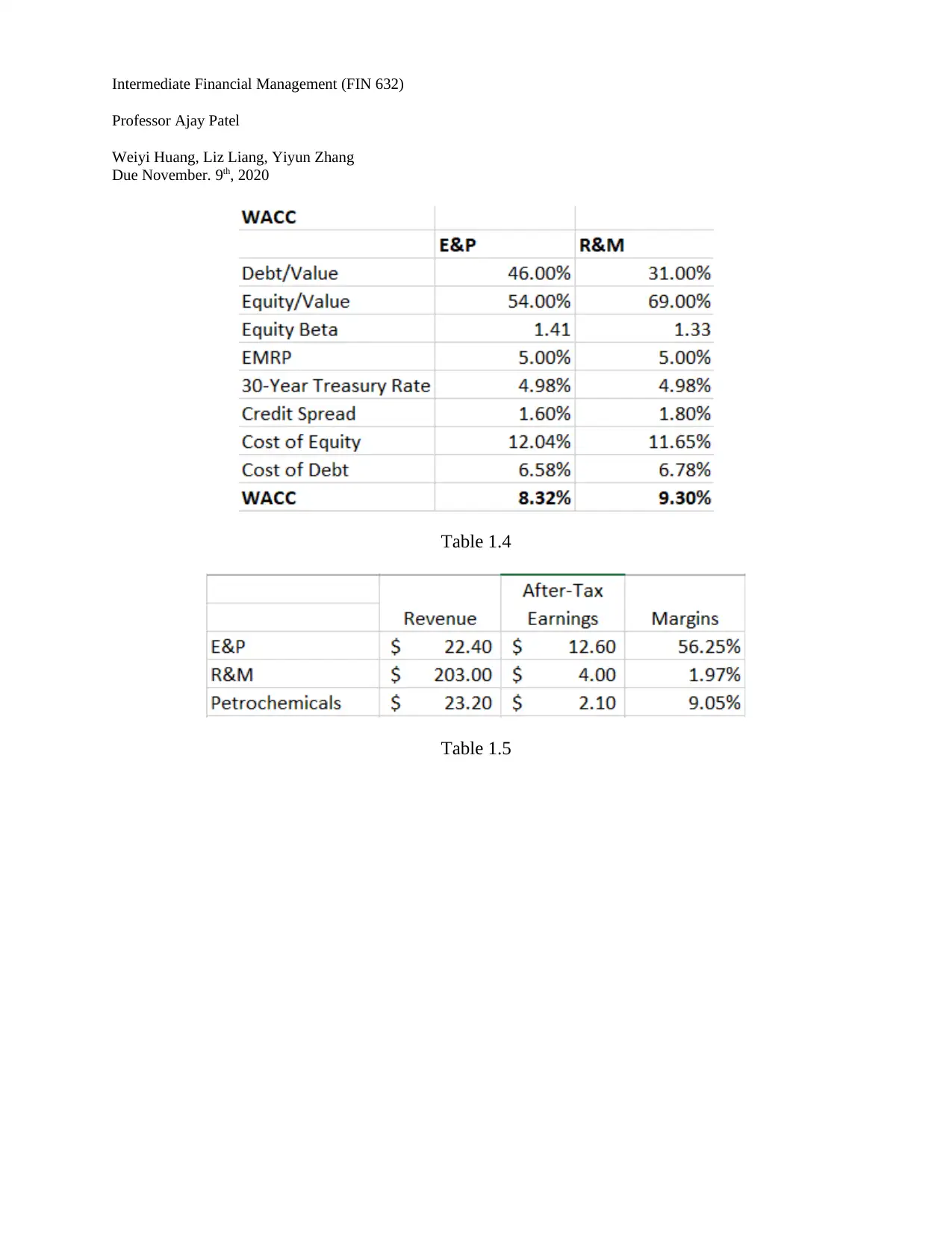

This report provides a comprehensive cost of capital analysis for Midland Energy Resources, Inc. The analysis begins with an executive summary that highlights the goal of minimizing costs and optimizing capital structure. The report then delves into the case problem, which involves assessing the appropriateness of the CFO's cost of capital calculations at both the corporate and divisional levels. The report calculates a consolidated WACC of 8.39% and recommends separate WACC calculations for the company's three divisions: Exploration & Production, Refining and Marketing, and Petrochemicals, with results of 8.32%, 9.30%, and 7.05%, respectively. The analysis includes assumptions regarding tax rates, risk-free rates, and the equity market risk premium. The report also explores the differences in WACC across the divisions, considering factors such as profitability, credit ratings, capital spending, and target capital structures. Sensitivity analysis is performed, and recommendations are made for the application of different hurdle rates based on the company's projections for each division. The report uses data from exhibits and comparable companies to support its findings and provides detailed calculations for the cost of debt and equity. The report concludes that Mortensen’s estimates would not be appropriate for all applications and suggests better estimates for different levels.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.