University Project: MIE377 Financial Optimization Models Project

VerifiedAdded on 2022/09/06

|5

|1018

|23

Project

AI Summary

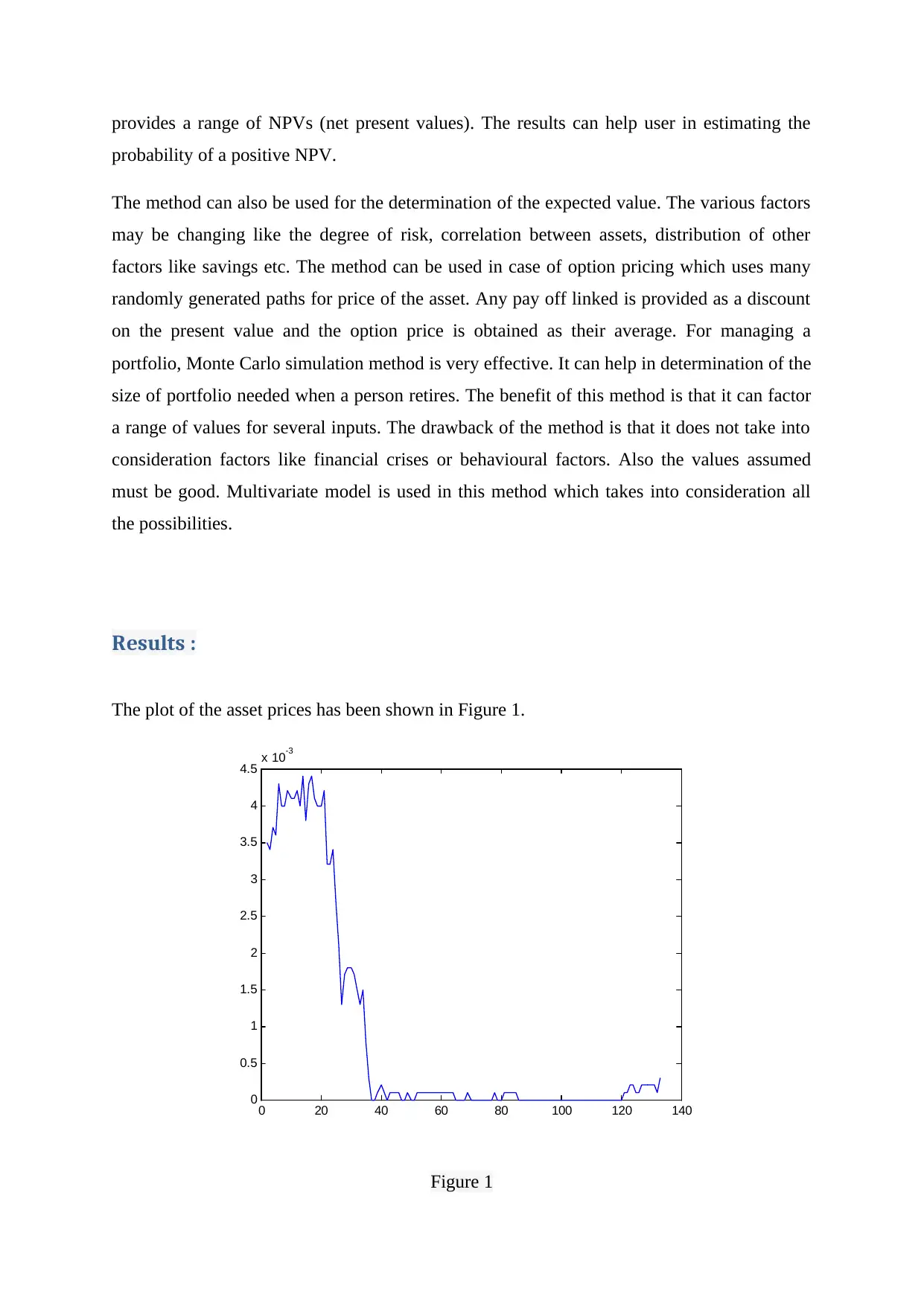

This project report presents a financial model developed using data from 20 U.S. stocks and a market risk-free rate, employing Conditional Value at Risk (CVaR) and Monte Carlo simulation methods. The methodology includes an explanation of CVaR for risk assessment and portfolio optimization, alongside the Monte Carlo method for statistical problem-solving and data sampling. The report details the application of these methods in MATLAB, providing a plot of asset prices and a conclusion summarizing the financial modeling process. The report also includes references to relevant literature on stochastic optimization and portfolio selection. This project was completed for the MIE377 course, replacing the final exam and Project 2.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.