Managerial Accounting Assignment: Milano Co Break-Even Point Analysis

VerifiedAdded on 2022/08/18

|9

|1312

|23

Homework Assignment

AI Summary

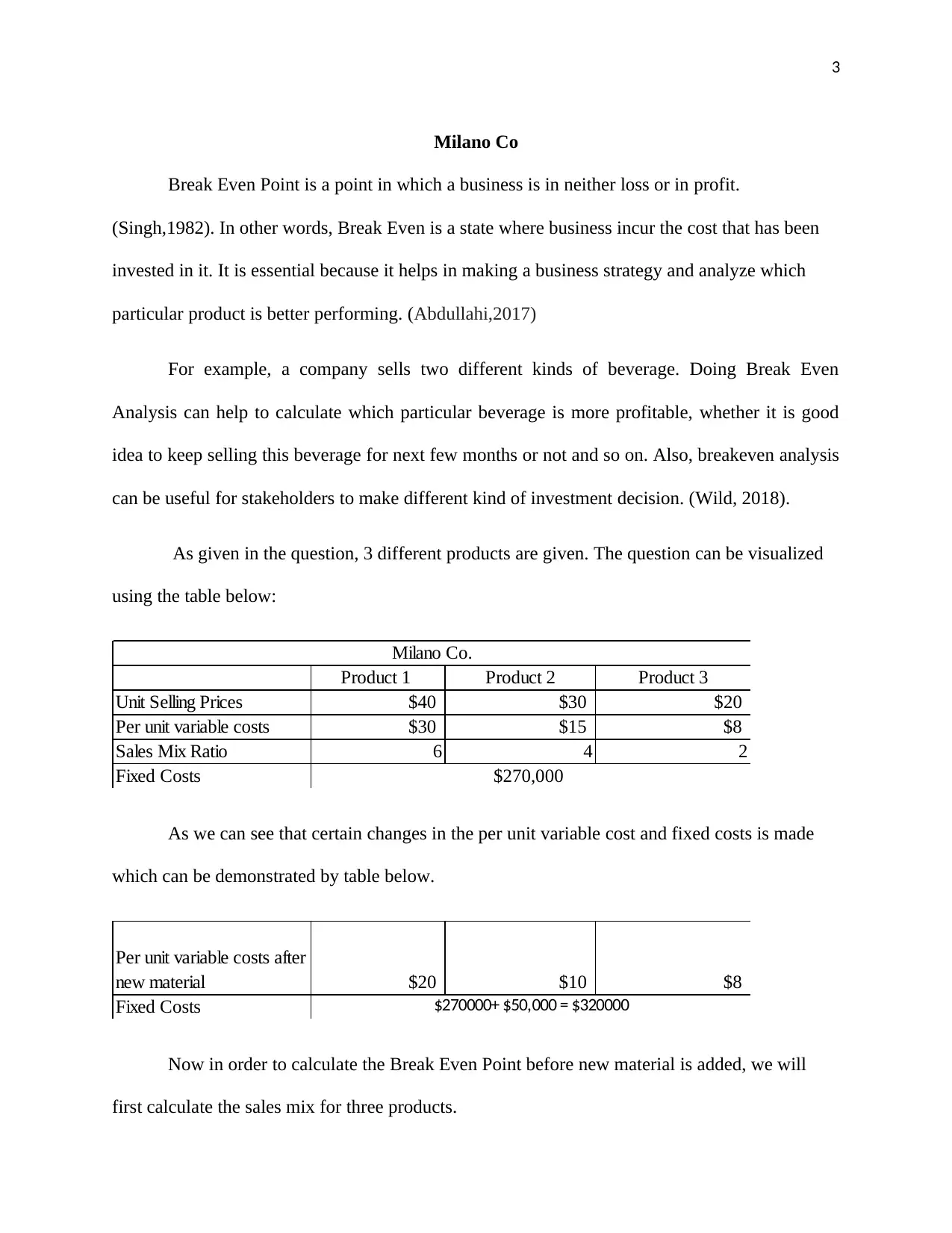

This assignment analyzes the break-even point for Milano Co, a case study in managerial accounting. The paper calculates the break-even point before and after incorporating changes in material and fixed costs. It begins by defining break-even analysis and its importance for business strategy and investment decisions. The analysis involves calculating the sales mix, contribution margin per unit (CMPU), and the combined CMPU for three products. The break-even point is then determined in both sales units and sales dollars for each product. The assignment then re-calculates the break-even point after the addition of new materials and an increase in fixed costs. The results demonstrate how changes in costs affect profitability and the break-even point, emphasizing the value of break-even analysis for managerial decision-making, including budgeting, cost control, risk analysis, and investment strategies. The conclusion highlights the use of break-even analysis to assess product performance and guide strategic adjustments for improved profitability.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.