Financial Reporting for Business: Performance and Pension Analysis

VerifiedAdded on 2023/01/09

|19

|3681

|62

Report

AI Summary

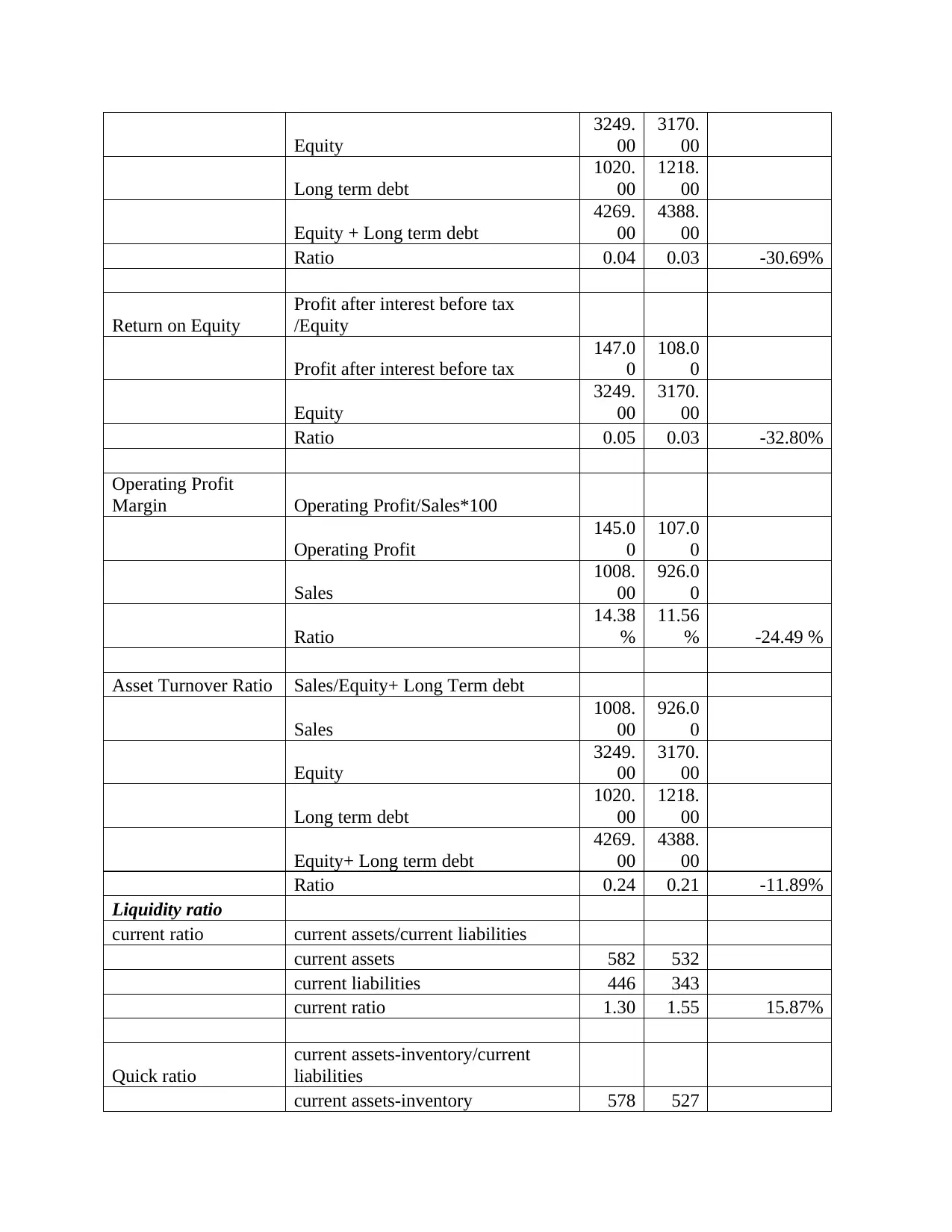

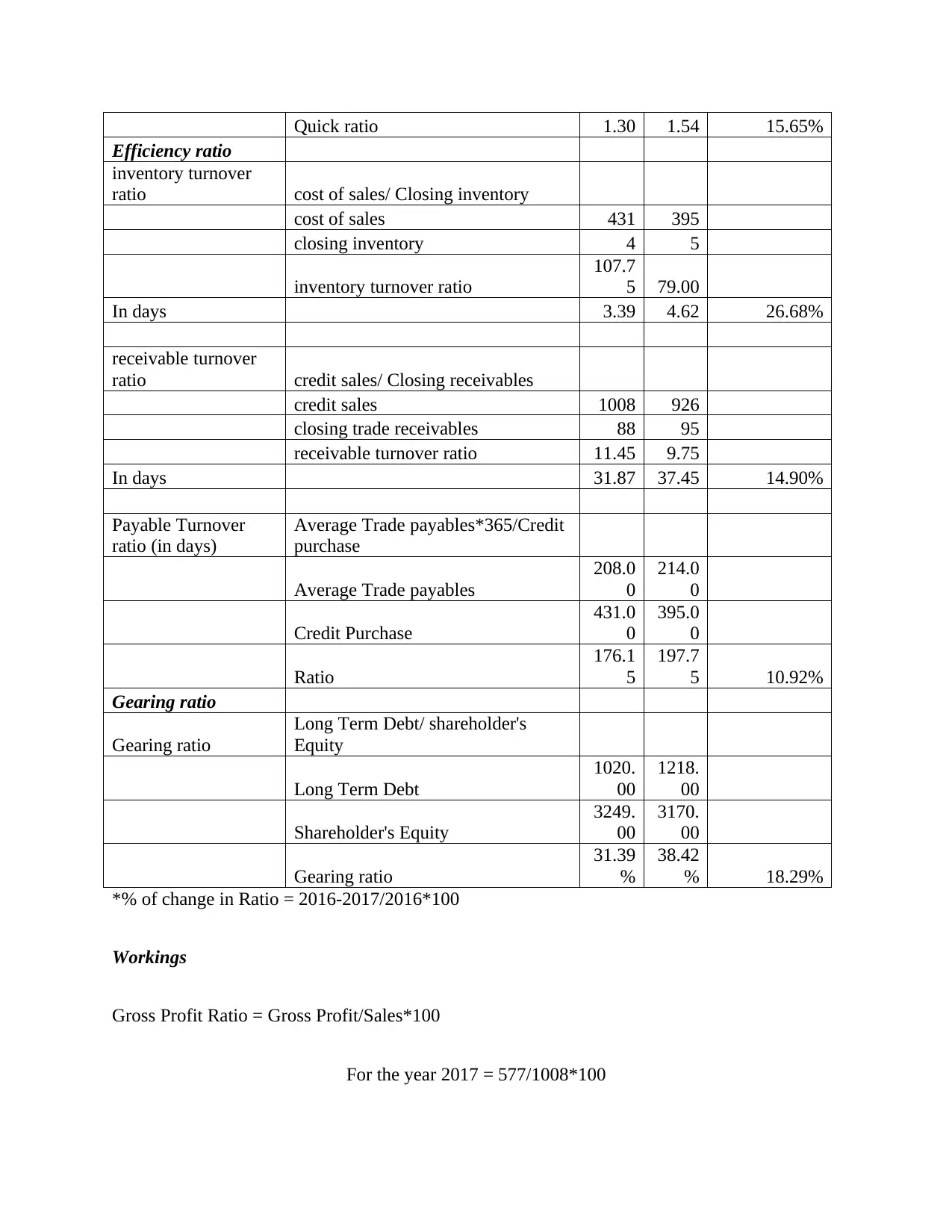

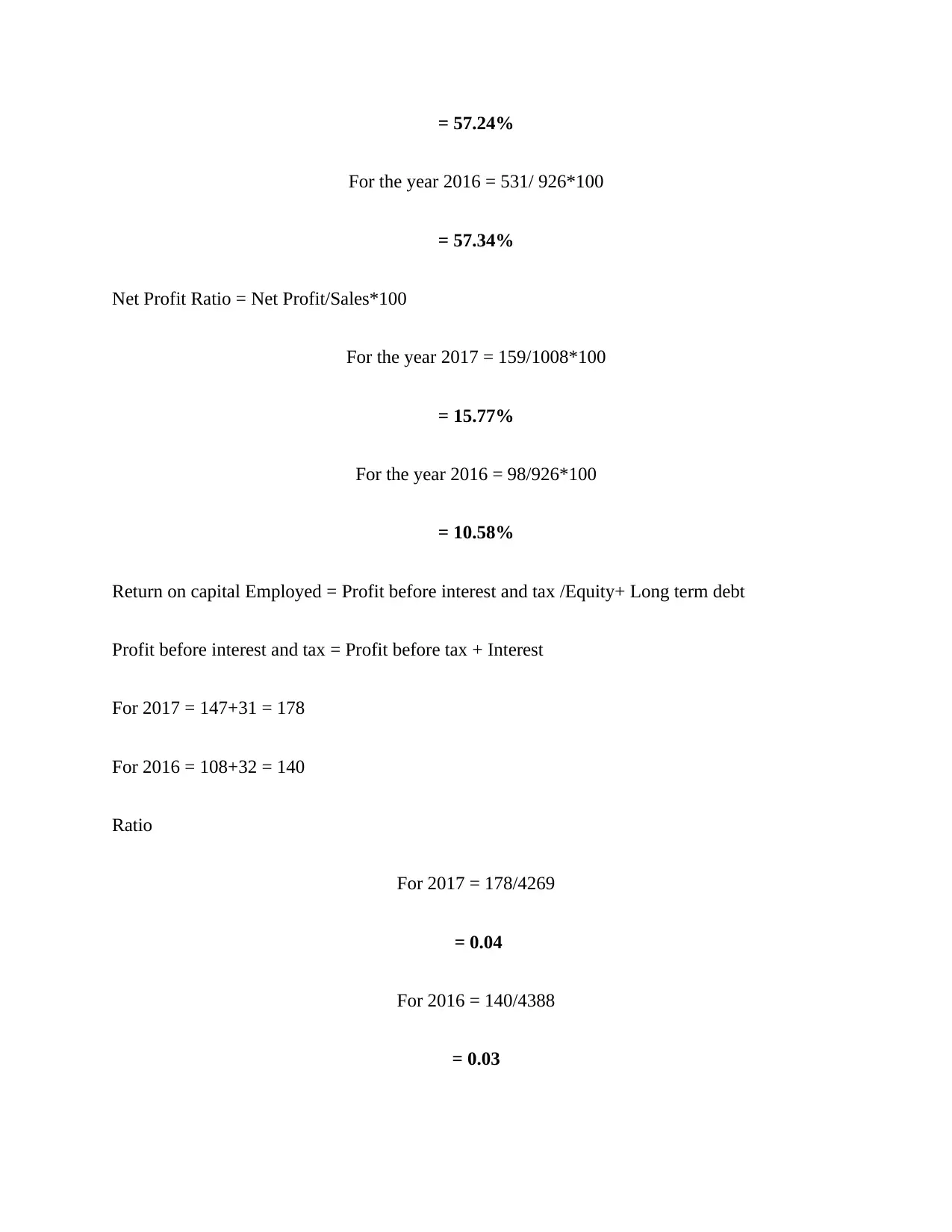

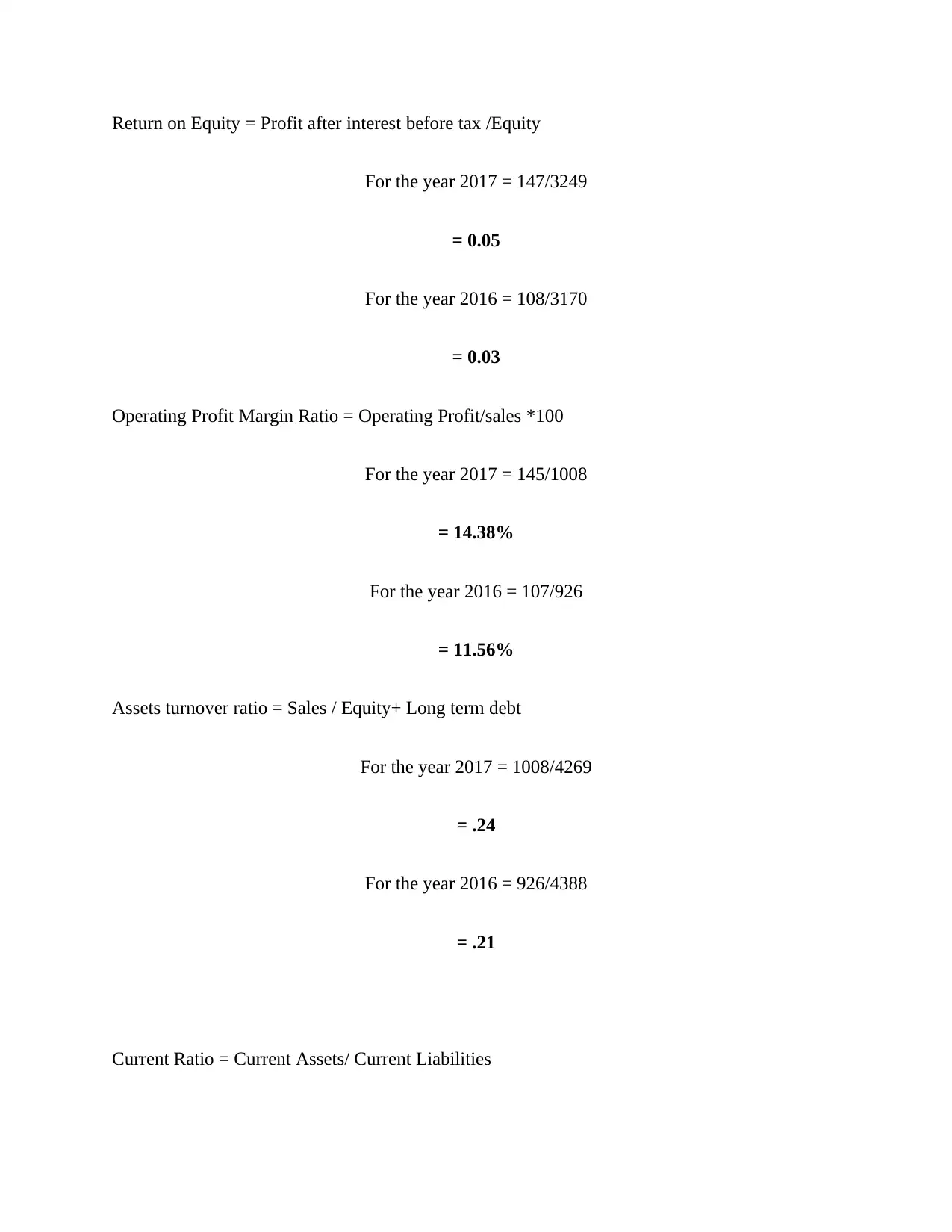

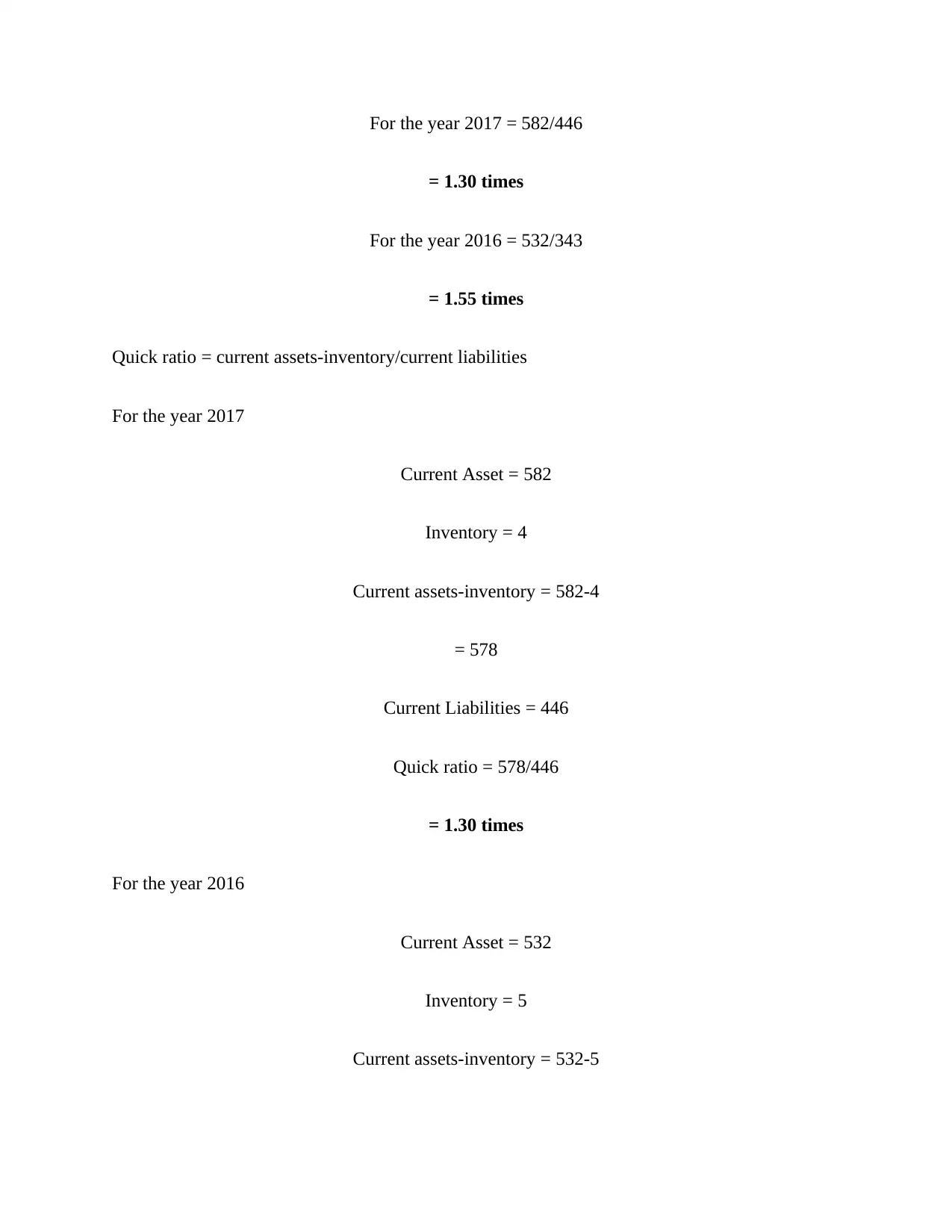

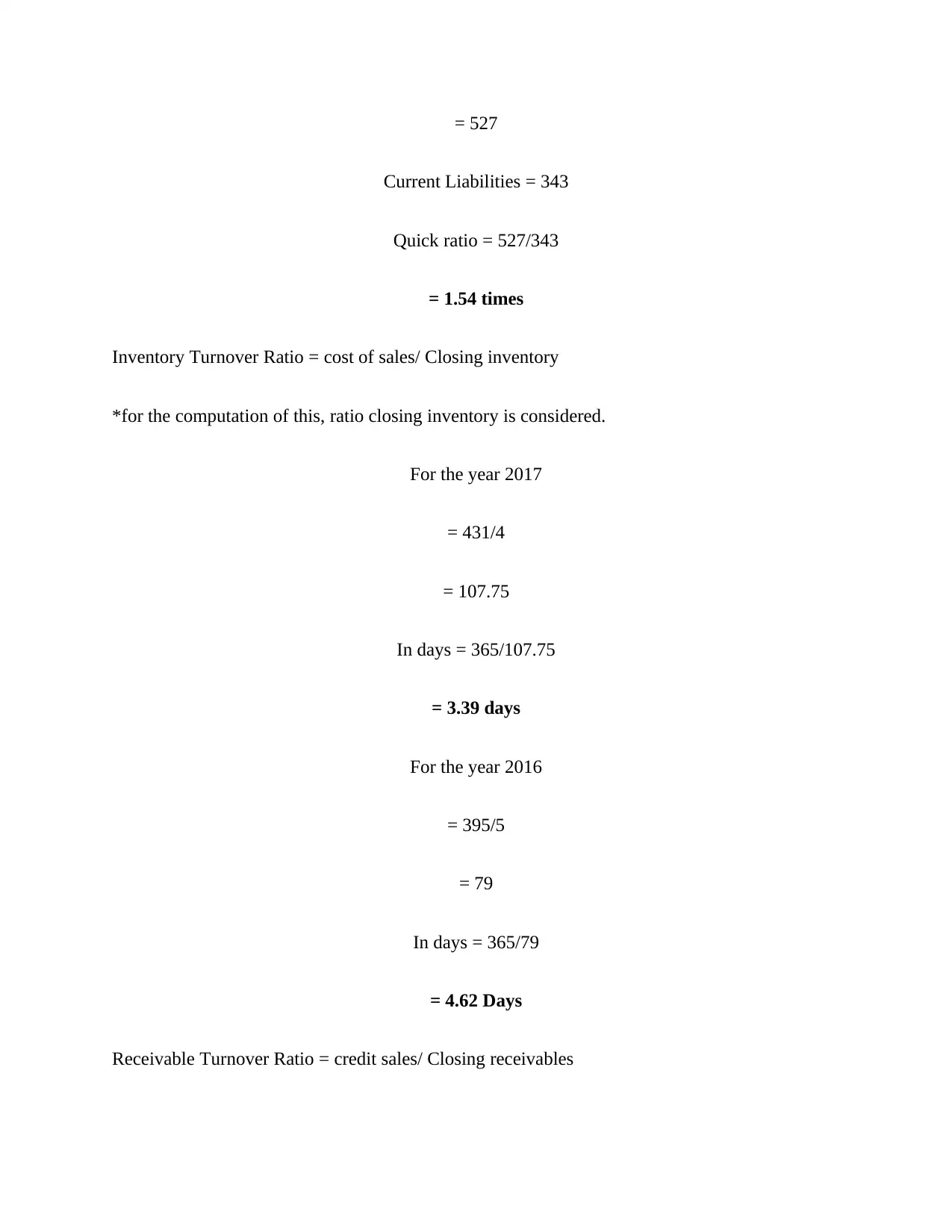

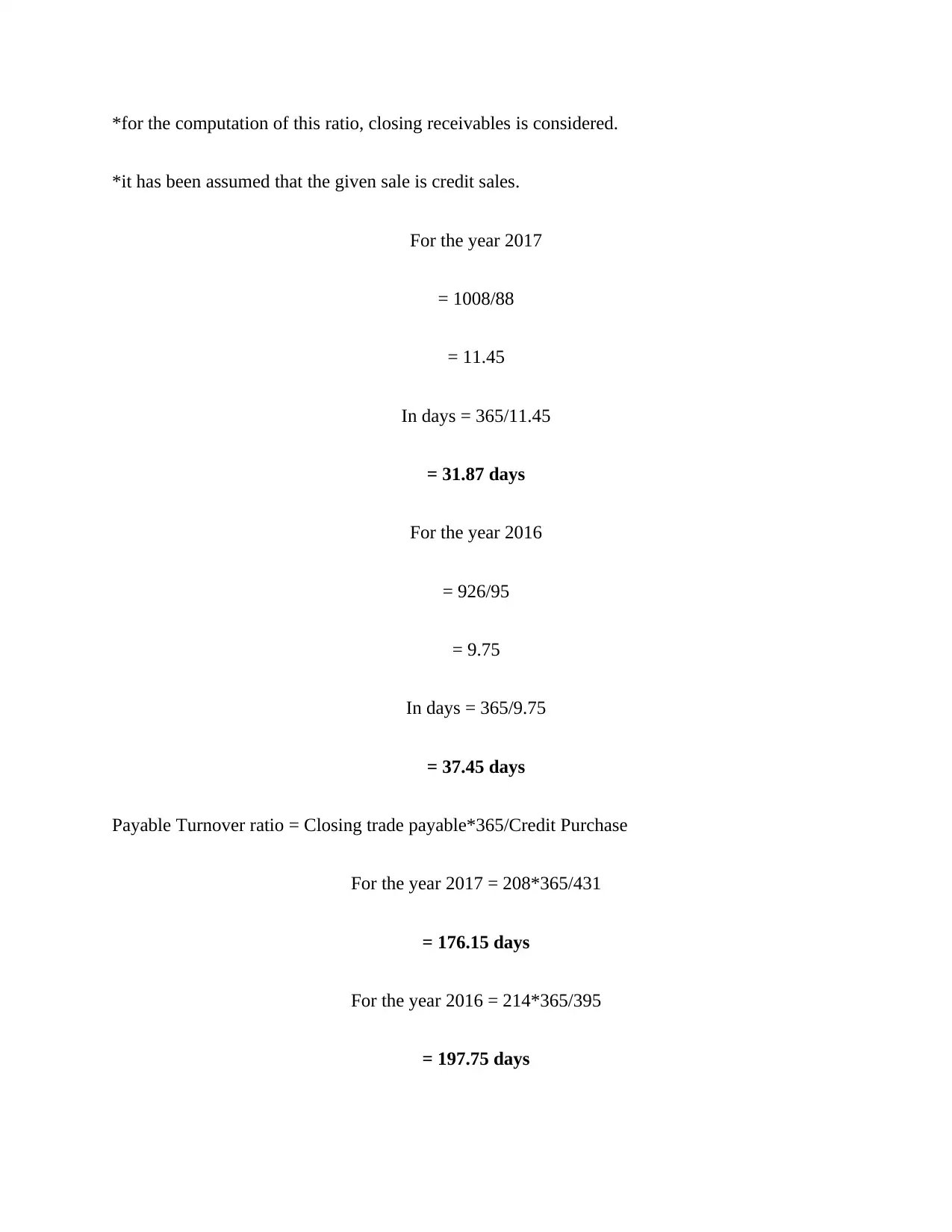

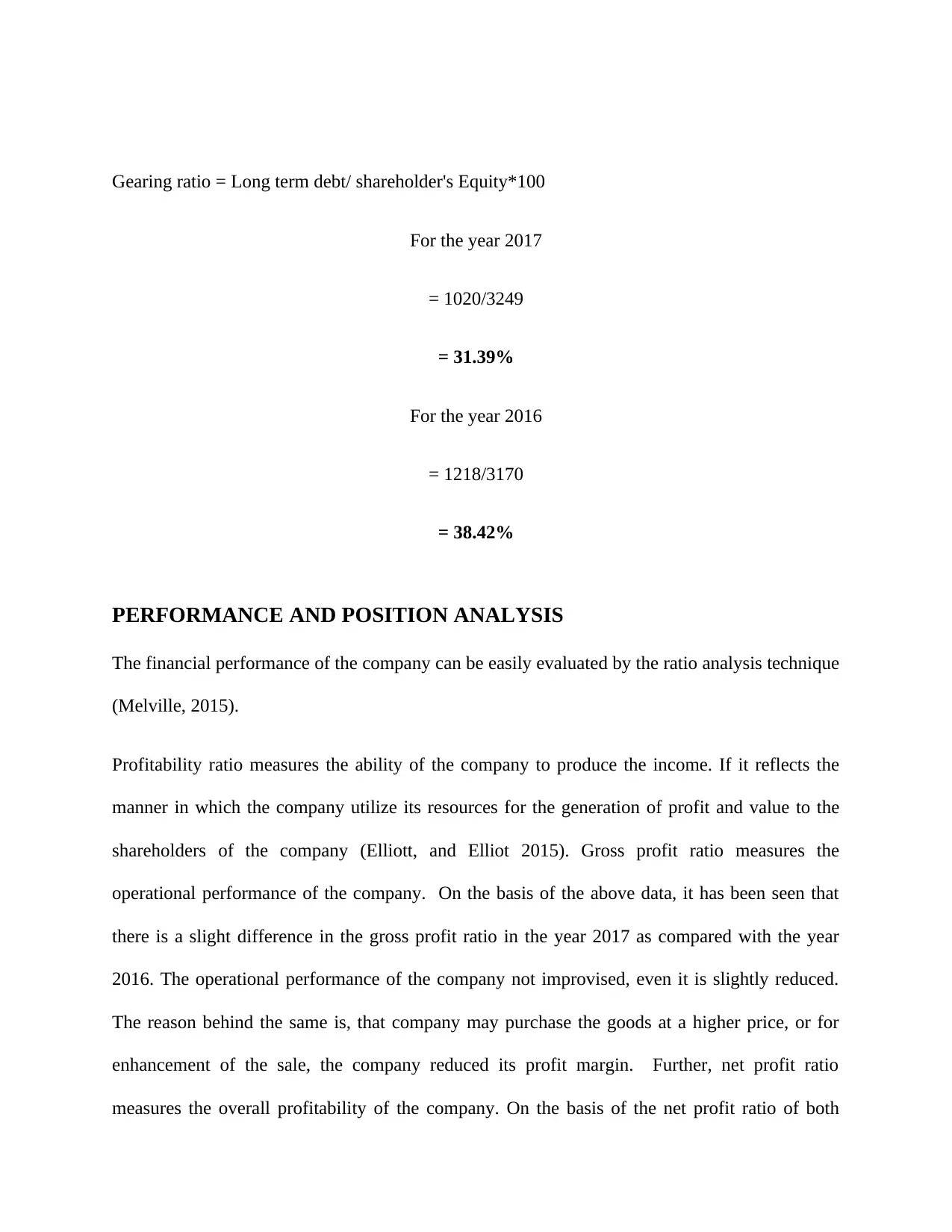

This report offers a comprehensive financial analysis of Millennium and Copthorne Hotels plc, focusing on the company's performance through ratio analysis and addressing the reporting requirements of IAS 19 Employee Benefits, specifically concerning pension schemes. The analysis includes the calculation of profitability, liquidity, efficiency, and gearing ratios for 2017 and 2016, providing insights into the company's operational and financial positions. The report evaluates the company's gross profit, net profit, return on capital employed, return on equity, operating profit margin, asset turnover, and liquidity, including current and quick ratios. It further examines efficiency ratios like inventory and receivable turnover, along with payable turnover and gearing ratios. The study then delves into the application of IAS 19, analyzing the requirements for reporting pension schemes and employee benefits within the context of the company's financial statements. The report concludes with an assessment of the company's financial health and compliance with accounting standards.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.