Financial Analysis and Loan Recommendation for Mirvac Group Expansion

VerifiedAdded on 2020/07/23

|14

|3154

|279

Report

AI Summary

This report provides a comprehensive financial analysis of Mirvac Group's loan proposal to Westpac for a $250 million expansion project. It begins with an overview of Mirvac Group, an Australian publicly listed real estate company, and its integrated property business model. The analysis delves into profitability, liquidity, and solvency, comparing Mirvac's performance to competitors like Finbar Group and Lendlease Group. The report assesses Mirvac's financial health, including debt-to-equity ratio, borrowing costs, and cash flow management. It then examines Westpac's loan policy, pricing model, and security requirements, emphasizing the need for collateral. The report concludes with recommendations for Mirvac to secure the loan, focusing on improving its interest burden capacity, providing collateral, and implementing sound cash flow management strategies. The report highlights key financial metrics, lending policies, and potential risks associated with the loan.

Assessment Task

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Overview of the borrower............................................................................................................3

Financial analysis.........................................................................................................................3

Security........................................................................................................................................7

Loan Policy..................................................................................................................................7

Pricing Model...............................................................................................................................8

Recommendations........................................................................................................................8

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................12

Appendix: 1 Security analysis....................................................................................................12

Appendix: 2: Financial analysis.................................................................................................12

Appendix: 3: Projected statements.............................................................................................13

Overview of the borrower............................................................................................................3

Financial analysis.........................................................................................................................3

Security........................................................................................................................................7

Loan Policy..................................................................................................................................7

Pricing Model...............................................................................................................................8

Recommendations........................................................................................................................8

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................12

Appendix: 1 Security analysis....................................................................................................12

Appendix: 2: Financial analysis.................................................................................................12

Appendix: 3: Projected statements.............................................................................................13

Overview of the borrower

Mirvac Group is Australian leading publicly listed company on ASX headquartered in

Sydney NSW, Australia. It was established in the year 1972 and operates in real estate industry.

It is an integrated property group which owns and manages number of assets across industrial,

retail and office sectors. Its key mission is to invest in vibrant cities considering well-connected

places for work, live and play. Along with the property development operations, it also invest in

hi-quality commercial assets and residential projects for their consumers so as to maximize long-

term value for security holders. Such integrated business approach of Mirvac provide it’s a

competitive benefit in creating and developing world class assets across project lifecycle from

planning to construction, leasing, development and property management (Mirvac Group Annual

report, 2017). Its integrated business model assures growth in its income through having a

balance of active & passive capital. with having an experience of 45 years, Mirvac is redefining

its presence in Australia through developing highly sustainable, well-connected and vibrant

urban environment for the society whether they can play, live, shop and work. It is extremely

committed towards innovation, sustainability, technological advancements and safety. In the year

2016, its urban strategy and well managed capital delivered successful results with $482m

operating profit (+6%, $455m in 2015) which got increased to $750m EBIT in FY 2017. Its

statutory profit increased from 1.03 bn to $1.16 bn and operating cash flow from $509m to

$513m. Currently, it employed more than 1,470 employees spreaded all around the world at a

sex ratio of 59:41. As per FY 2017, it has effectively managed its capital through lowering its

gearing (Pan, Wang and Weisbac, 2014). With the reduction in debt composition which will be

due in one year, its weight average debt maturity increased by 6.2 years, whilst, average

borrowing cost came down to 4.8% from 5%. Its 2017 year annual report presented revenue of

$2,275m at a total long-term borrowing of $2,765m. Currently, it is looking for expansion for

which it requires loan borrowing of AUD 250m.

Financial analysis

Profitability analysis

Mirvac Group is Australian leading publicly listed company on ASX headquartered in

Sydney NSW, Australia. It was established in the year 1972 and operates in real estate industry.

It is an integrated property group which owns and manages number of assets across industrial,

retail and office sectors. Its key mission is to invest in vibrant cities considering well-connected

places for work, live and play. Along with the property development operations, it also invest in

hi-quality commercial assets and residential projects for their consumers so as to maximize long-

term value for security holders. Such integrated business approach of Mirvac provide it’s a

competitive benefit in creating and developing world class assets across project lifecycle from

planning to construction, leasing, development and property management (Mirvac Group Annual

report, 2017). Its integrated business model assures growth in its income through having a

balance of active & passive capital. with having an experience of 45 years, Mirvac is redefining

its presence in Australia through developing highly sustainable, well-connected and vibrant

urban environment for the society whether they can play, live, shop and work. It is extremely

committed towards innovation, sustainability, technological advancements and safety. In the year

2016, its urban strategy and well managed capital delivered successful results with $482m

operating profit (+6%, $455m in 2015) which got increased to $750m EBIT in FY 2017. Its

statutory profit increased from 1.03 bn to $1.16 bn and operating cash flow from $509m to

$513m. Currently, it employed more than 1,470 employees spreaded all around the world at a

sex ratio of 59:41. As per FY 2017, it has effectively managed its capital through lowering its

gearing (Pan, Wang and Weisbac, 2014). With the reduction in debt composition which will be

due in one year, its weight average debt maturity increased by 6.2 years, whilst, average

borrowing cost came down to 4.8% from 5%. Its 2017 year annual report presented revenue of

$2,275m at a total long-term borrowing of $2,765m. Currently, it is looking for expansion for

which it requires loan borrowing of AUD 250m.

Financial analysis

Profitability analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2013 2014 2015 2016 2017

9.49%

24.37%

32.59% 35.53%

49.87%

22.46%

13.00%

27.66%

8.49%

4.03%4.45% 5.85% 4.58% 4.55% 4.51%

Net profit ratio

Mirvac Group Finbar Group LendLease Group

2013 2014 2015 2016 2017

14.33%

37.95% 41.35%

49.33%

44.34%

30.43%

20.94%

31.91%

9.43% 8.06%8.06% 5.08% 7.41% 6.41% 6.26%

Operating profit ratio

Mirvac Group Finbar Group LendLease Group

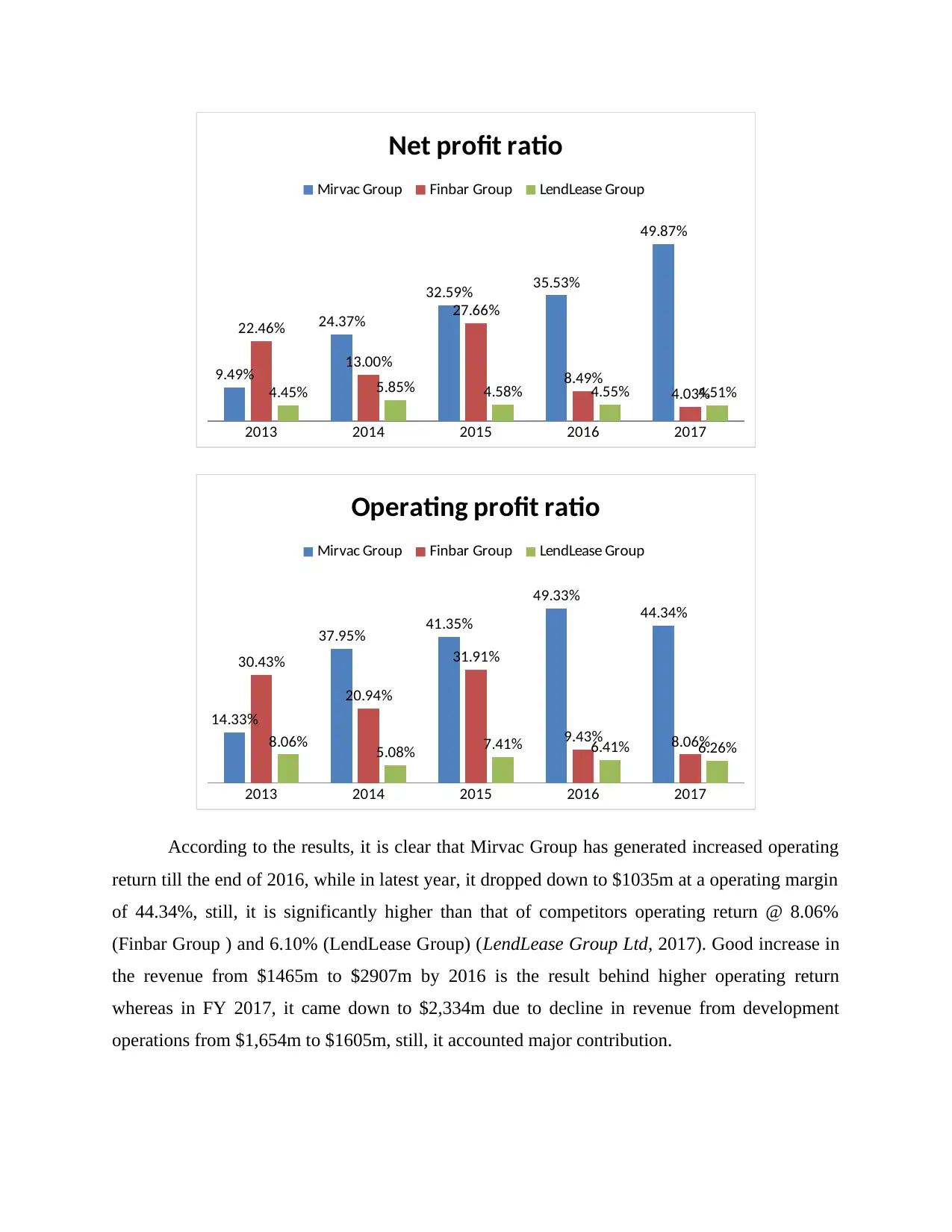

According to the results, it is clear that Mirvac Group has generated increased operating

return till the end of 2016, while in latest year, it dropped down to $1035m at a operating margin

of 44.34%, still, it is significantly higher than that of competitors operating return @ 8.06%

(Finbar Group ) and 6.10% (LendLease Group) (LendLease Group Ltd, 2017). Good increase in

the revenue from $1465m to $2907m by 2016 is the result behind higher operating return

whereas in FY 2017, it came down to $2,334m due to decline in revenue from development

operations from $1,654m to $1605m, still, it accounted major contribution.

9.49%

24.37%

32.59% 35.53%

49.87%

22.46%

13.00%

27.66%

8.49%

4.03%4.45% 5.85% 4.58% 4.55% 4.51%

Net profit ratio

Mirvac Group Finbar Group LendLease Group

2013 2014 2015 2016 2017

14.33%

37.95% 41.35%

49.33%

44.34%

30.43%

20.94%

31.91%

9.43% 8.06%8.06% 5.08% 7.41% 6.41% 6.26%

Operating profit ratio

Mirvac Group Finbar Group LendLease Group

According to the results, it is clear that Mirvac Group has generated increased operating

return till the end of 2016, while in latest year, it dropped down to $1035m at a operating margin

of 44.34%, still, it is significantly higher than that of competitors operating return @ 8.06%

(Finbar Group ) and 6.10% (LendLease Group) (LendLease Group Ltd, 2017). Good increase in

the revenue from $1465m to $2907m by 2016 is the result behind higher operating return

whereas in FY 2017, it came down to $2,334m due to decline in revenue from development

operations from $1,654m to $1605m, still, it accounted major contribution.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Although decline in sales lower down its operational return, still, good control of the

mangers over their indirect overheads resultant good net return worth $1,164m at a net margin of

49.87% which was 35.53% in FY 2016. The result of net profit shows a sudden increase from

9.49% to 49.87% in FY 2017 and also it is extremely higher in comparison to the rivalry

organizations, Finbar and LendLease Group who are earning a net return of 4.03% and 4.51%.

Firm has maintained strong control over its variable costs i.e. through using direct seeding

planting technique rather than tube stock planting; firm became able to manage cost efficiency

and generated greater return. As per FY 2017, it had achieved saving worth $2.8m and thereby

meet budgetary targets to 85%. It reduced its borrowing costs to 4.8% and minimized occupancy

cost from 15.3% to 15% (Tumwine and et.al., 2015). Besides this, recycling strategy for waste

management and efficient use of resources with optimum allocation helped it to maximize its net

return. However, increasing cost of house and living created pressure upon firm.

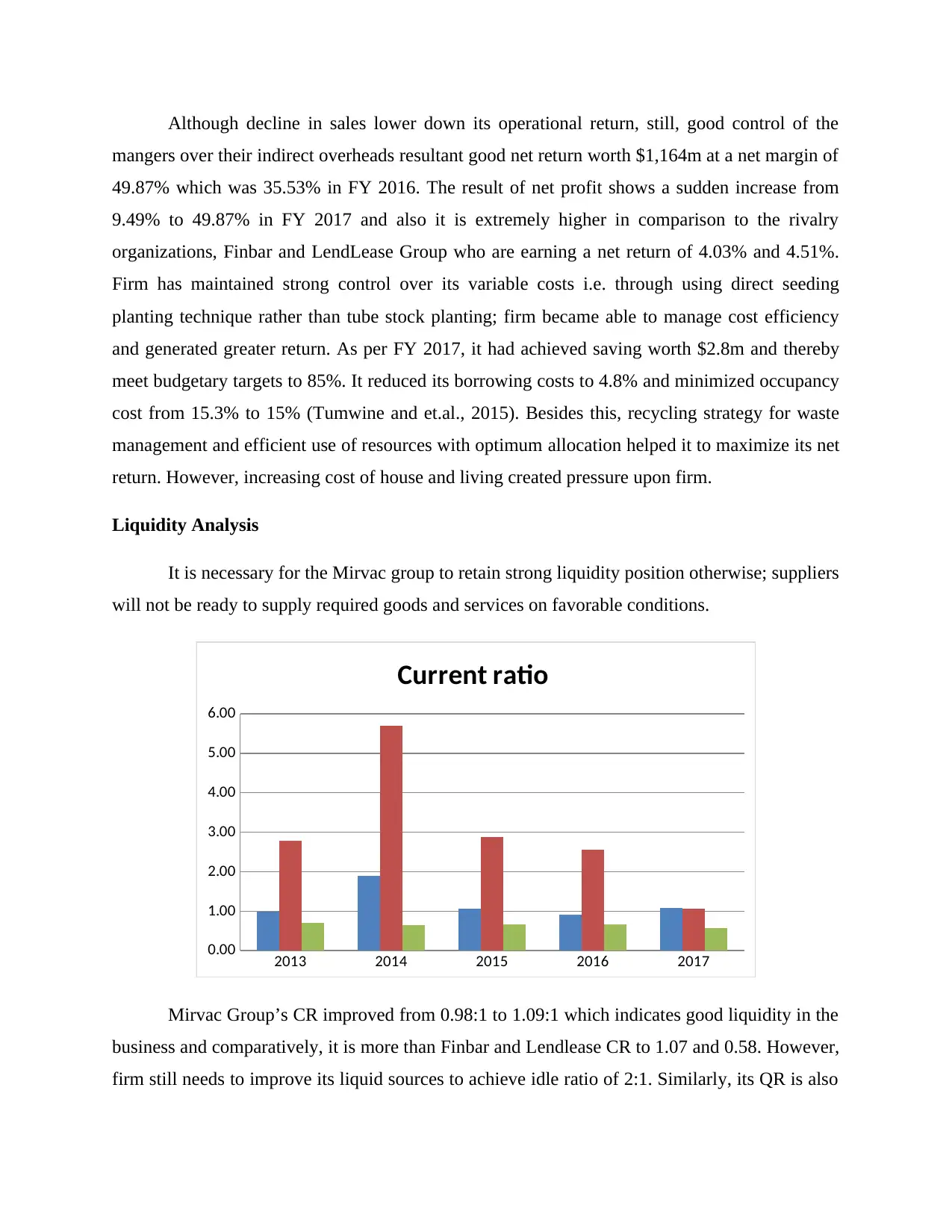

Liquidity Analysis

It is necessary for the Mirvac group to retain strong liquidity position otherwise; suppliers

will not be ready to supply required goods and services on favorable conditions.

2013 2014 2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Current ratio

Mirvac Group’s CR improved from 0.98:1 to 1.09:1 which indicates good liquidity in the

business and comparatively, it is more than Finbar and Lendlease CR to 1.07 and 0.58. However,

firm still needs to improve its liquid sources to achieve idle ratio of 2:1. Similarly, its QR is also

mangers over their indirect overheads resultant good net return worth $1,164m at a net margin of

49.87% which was 35.53% in FY 2016. The result of net profit shows a sudden increase from

9.49% to 49.87% in FY 2017 and also it is extremely higher in comparison to the rivalry

organizations, Finbar and LendLease Group who are earning a net return of 4.03% and 4.51%.

Firm has maintained strong control over its variable costs i.e. through using direct seeding

planting technique rather than tube stock planting; firm became able to manage cost efficiency

and generated greater return. As per FY 2017, it had achieved saving worth $2.8m and thereby

meet budgetary targets to 85%. It reduced its borrowing costs to 4.8% and minimized occupancy

cost from 15.3% to 15% (Tumwine and et.al., 2015). Besides this, recycling strategy for waste

management and efficient use of resources with optimum allocation helped it to maximize its net

return. However, increasing cost of house and living created pressure upon firm.

Liquidity Analysis

It is necessary for the Mirvac group to retain strong liquidity position otherwise; suppliers

will not be ready to supply required goods and services on favorable conditions.

2013 2014 2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Current ratio

Mirvac Group’s CR improved from 0.98:1 to 1.09:1 which indicates good liquidity in the

business and comparatively, it is more than Finbar and Lendlease CR to 1.07 and 0.58. However,

firm still needs to improve its liquid sources to achieve idle ratio of 2:1. Similarly, its QR is also

0.39:1 very less than standard ratio of 1:1 indicates ineffective liquidity management. In FY

2017, in order to minimize credit risk, it uses credit limit policy, obtain collateral from customers

and regularly monitor counterparty credit rating and payments (Mirvac Group Annual report,

2017). It regularly examine its cash availability, marketable securities and its ability to raise

funds through issuance of new securities.

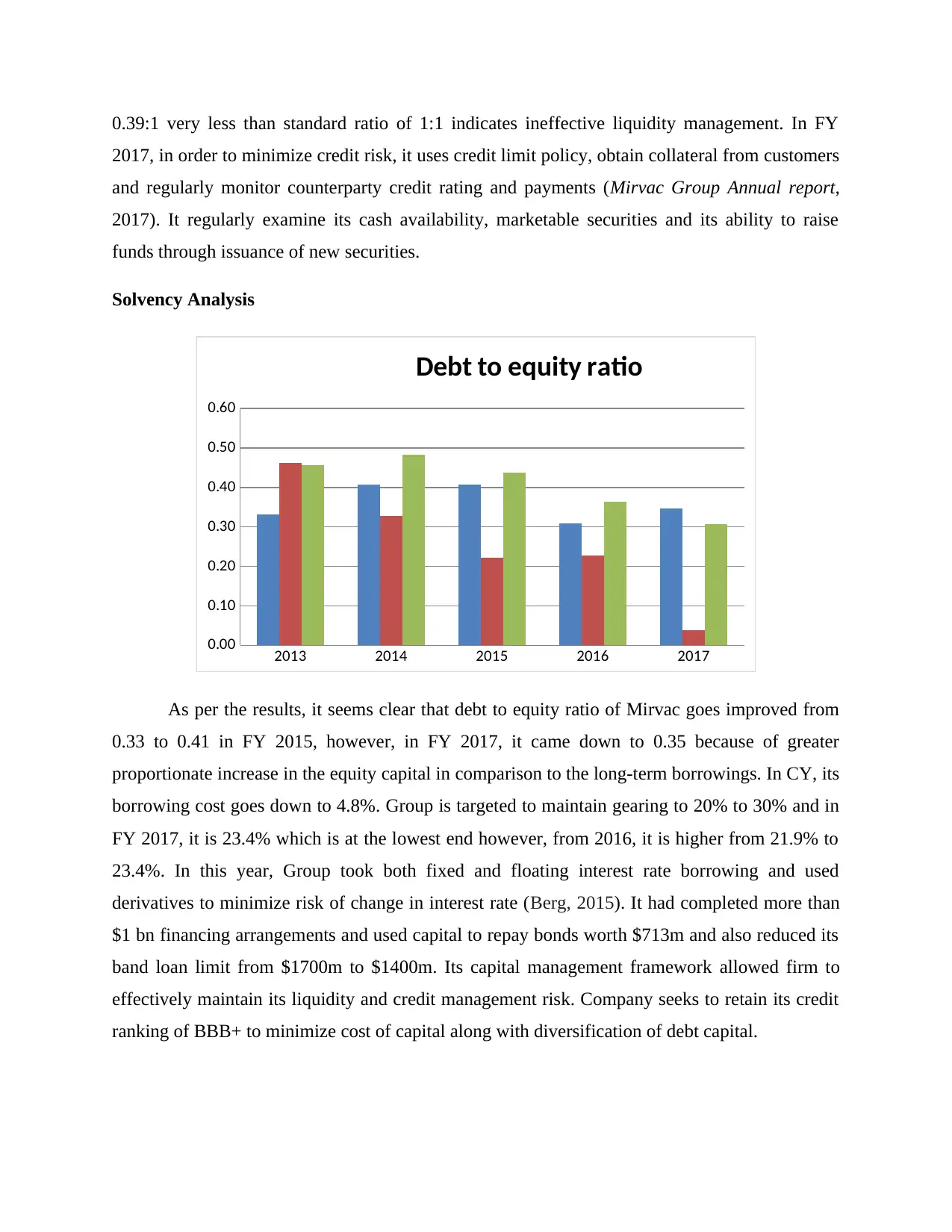

Solvency Analysis

2013 2014 2015 2016 2017

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Debt to equity ratio

As per the results, it seems clear that debt to equity ratio of Mirvac goes improved from

0.33 to 0.41 in FY 2015, however, in FY 2017, it came down to 0.35 because of greater

proportionate increase in the equity capital in comparison to the long-term borrowings. In CY, its

borrowing cost goes down to 4.8%. Group is targeted to maintain gearing to 20% to 30% and in

FY 2017, it is 23.4% which is at the lowest end however, from 2016, it is higher from 21.9% to

23.4%. In this year, Group took both fixed and floating interest rate borrowing and used

derivatives to minimize risk of change in interest rate (Berg, 2015). It had completed more than

$1 bn financing arrangements and used capital to repay bonds worth $713m and also reduced its

band loan limit from $1700m to $1400m. Its capital management framework allowed firm to

effectively maintain its liquidity and credit management risk. Company seeks to retain its credit

ranking of BBB+ to minimize cost of capital along with diversification of debt capital.

2017, in order to minimize credit risk, it uses credit limit policy, obtain collateral from customers

and regularly monitor counterparty credit rating and payments (Mirvac Group Annual report,

2017). It regularly examine its cash availability, marketable securities and its ability to raise

funds through issuance of new securities.

Solvency Analysis

2013 2014 2015 2016 2017

0.00

0.10

0.20

0.30

0.40

0.50

0.60

Debt to equity ratio

As per the results, it seems clear that debt to equity ratio of Mirvac goes improved from

0.33 to 0.41 in FY 2015, however, in FY 2017, it came down to 0.35 because of greater

proportionate increase in the equity capital in comparison to the long-term borrowings. In CY, its

borrowing cost goes down to 4.8%. Group is targeted to maintain gearing to 20% to 30% and in

FY 2017, it is 23.4% which is at the lowest end however, from 2016, it is higher from 21.9% to

23.4%. In this year, Group took both fixed and floating interest rate borrowing and used

derivatives to minimize risk of change in interest rate (Berg, 2015). It had completed more than

$1 bn financing arrangements and used capital to repay bonds worth $713m and also reduced its

band loan limit from $1700m to $1400m. Its capital management framework allowed firm to

effectively maintain its liquidity and credit management risk. Company seeks to retain its credit

ranking of BBB+ to minimize cost of capital along with diversification of debt capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In contrast to this, Finbar’s debt to equity ratio shows a consistent decline from 0.46 to

0.04 times due to regular decline in debt capital and use of owners equity in the capital

composition (Finbar group Ltd, 2017). Although, it shows less financial burden, but, firm has no

tax benefits and also diluted control to the shareholders (Butler, Cornaggia and Gurun, 2016).

Similarly, Lendlease ratio decreased from 0.46 to 0.31 due to minimal debt use and higher equity

capital. Although in comparison to the rival firms, Mirvac’s Debt to equity ratio is more closer to

idle ratio of 0.50:1, still, decreased interest burden ratio from 5.23 to 3.19 resulted stated that

firm should not use more borrowing otherwise, it might face financial burden. In this year,

Mirbac complied all debt covenants requirement and committed to sell property or issue more

equity shares in order to repay its long-term borrowings.

Security

Mirvac Group reports its borrowing initially at fair value while subsequent reporting is

made using effective interest rate method and the difference between initial amount and

redemption is reported in SOCI. In FY 2017, firm’s balance sheet reported non-current

borrowing worth $2965m at a fair value of $2939m which all are unsecured (Halldórsson, Hsuan

and Kotzab, 2015). Thus, as per current security structure, none of the loan borrowing has been

secured by collateral. However, as company is looking for expanding its business and need to

borrow loan of $250m from Westapc, it will definitely need collateral security that needs to be

provided to the bank (Mirvac Group Ltd, 2017). Thus, it will be a main issue that firm needs to

arrange collateral. Besides this, more use of debt will help it to reach idle, still, declined interest

bearing ratio may have an adverse impact on receiving loan facilities from Westpac.

Loan Policy

Westpac Banking Corporation is an Australian Financial institution that is one of leading

commercial bank in Australia and engaged in financial, consumer banking, investment banking,

wealth management, mortgage, private equity and credit card operations. It imposed tougher

lending rules for the property developers to raise required capital through borrowings. In this

regards, initially, Westpac examine borrower’s payment ability, credit rating and others aspect to

assure that whether he or she is able or not to cope up with the high interest rate (Yeates, 2015).

It takes all the necessary actions and put regulatory efforts to prevent against possible risk of

overheating housing market. Before just two years, it had made changes in its lending policy and

maximize standard of 180 basis points to 210 basis points in order to respond Australian

0.04 times due to regular decline in debt capital and use of owners equity in the capital

composition (Finbar group Ltd, 2017). Although, it shows less financial burden, but, firm has no

tax benefits and also diluted control to the shareholders (Butler, Cornaggia and Gurun, 2016).

Similarly, Lendlease ratio decreased from 0.46 to 0.31 due to minimal debt use and higher equity

capital. Although in comparison to the rival firms, Mirvac’s Debt to equity ratio is more closer to

idle ratio of 0.50:1, still, decreased interest burden ratio from 5.23 to 3.19 resulted stated that

firm should not use more borrowing otherwise, it might face financial burden. In this year,

Mirbac complied all debt covenants requirement and committed to sell property or issue more

equity shares in order to repay its long-term borrowings.

Security

Mirvac Group reports its borrowing initially at fair value while subsequent reporting is

made using effective interest rate method and the difference between initial amount and

redemption is reported in SOCI. In FY 2017, firm’s balance sheet reported non-current

borrowing worth $2965m at a fair value of $2939m which all are unsecured (Halldórsson, Hsuan

and Kotzab, 2015). Thus, as per current security structure, none of the loan borrowing has been

secured by collateral. However, as company is looking for expanding its business and need to

borrow loan of $250m from Westapc, it will definitely need collateral security that needs to be

provided to the bank (Mirvac Group Ltd, 2017). Thus, it will be a main issue that firm needs to

arrange collateral. Besides this, more use of debt will help it to reach idle, still, declined interest

bearing ratio may have an adverse impact on receiving loan facilities from Westpac.

Loan Policy

Westpac Banking Corporation is an Australian Financial institution that is one of leading

commercial bank in Australia and engaged in financial, consumer banking, investment banking,

wealth management, mortgage, private equity and credit card operations. It imposed tougher

lending rules for the property developers to raise required capital through borrowings. In this

regards, initially, Westpac examine borrower’s payment ability, credit rating and others aspect to

assure that whether he or she is able or not to cope up with the high interest rate (Yeates, 2015).

It takes all the necessary actions and put regulatory efforts to prevent against possible risk of

overheating housing market. Before just two years, it had made changes in its lending policy and

maximize standard of 180 basis points to 210 basis points in order to respond Australian

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Prudential Regulation Authority’s warning (Yeates, 2015). As per the policy, it is essential for

Mirvac Group to convince Westpac that it is able to pay loan at an interest rate floor of 7.1%

(earlier 5%), even if Reserve Bank of Australia cuts their official rate. Moreover, slow rate of

growth in credit rating also influence its lending decisions. Currently, its lending policy does not

grant any loan to the foreigners who are interesting in applying loan for purchase of residential

properties. Westpac take into account loan to value ratio as an indicator of financial risk while

granting loan. After a sharp slowdown in bank lending to the property investors, Westpac

maximized LVRs (Loan-to-valuation-ratio) from 80% to 90%. It clearly means that property

borrowers need to deposit 10% of property’s value which was earlier 20% indicates some

relaxation in lending decisions which assists borrowers to lend more money. However, at the

same time, in order to mitigate the risk of borrowers default in loan payment, it had tightened its

loan granting criteria. In March, its interest rate on loans has been grew to 7.2% (Yeates, 2016).

Under the lending policy, bank examine security, verification of income, borrowing history and

credit check to ensure that loan is granted to the party who is able to make payment on time.

As per the case study, Mirvac need $250m for prospective expansion project. According

to current lending rules, Westpac grant flexible loans to the businesses that are looking for

expansion and growth. Under this, minimum loan amount is $250,000 and grant loan facilities at

flexible conditions at loan amount above $1m (Westpac Commercial loans. n.d.). Considering

the lending policy, it becomes clear that Mirvac’s must follow such requirements and debt

covenant conditions to obtain loan worth $250m.

Pricing Model

Mirvac require borrowing of $250m for investing, thus, it will need to take loan for

longer-period above 5 year on which, WestPac charges fixed interest rate (base rate) @ 5.74%

and variable rate (base rate) of 6.43% per annum (WestPac Busines Loans Rates, 2017). In order

to manage risk due to floating interest rate, Mirvac must use interest rate derivatives which

protect the firm against sudden increase in the loan interest. Besides this, firm needs to put

tighten control over the expenditures that will derive maximum yield so that it will have

sufficient liquid in the form of cash available to meet its debt covenant obligations. In addition,

cash flow management strategies need to be prepared for having enough cash to meet out debt

interest obligation as per scheduled requirement and on time.

Mirvac Group to convince Westpac that it is able to pay loan at an interest rate floor of 7.1%

(earlier 5%), even if Reserve Bank of Australia cuts their official rate. Moreover, slow rate of

growth in credit rating also influence its lending decisions. Currently, its lending policy does not

grant any loan to the foreigners who are interesting in applying loan for purchase of residential

properties. Westpac take into account loan to value ratio as an indicator of financial risk while

granting loan. After a sharp slowdown in bank lending to the property investors, Westpac

maximized LVRs (Loan-to-valuation-ratio) from 80% to 90%. It clearly means that property

borrowers need to deposit 10% of property’s value which was earlier 20% indicates some

relaxation in lending decisions which assists borrowers to lend more money. However, at the

same time, in order to mitigate the risk of borrowers default in loan payment, it had tightened its

loan granting criteria. In March, its interest rate on loans has been grew to 7.2% (Yeates, 2016).

Under the lending policy, bank examine security, verification of income, borrowing history and

credit check to ensure that loan is granted to the party who is able to make payment on time.

As per the case study, Mirvac need $250m for prospective expansion project. According

to current lending rules, Westpac grant flexible loans to the businesses that are looking for

expansion and growth. Under this, minimum loan amount is $250,000 and grant loan facilities at

flexible conditions at loan amount above $1m (Westpac Commercial loans. n.d.). Considering

the lending policy, it becomes clear that Mirvac’s must follow such requirements and debt

covenant conditions to obtain loan worth $250m.

Pricing Model

Mirvac require borrowing of $250m for investing, thus, it will need to take loan for

longer-period above 5 year on which, WestPac charges fixed interest rate (base rate) @ 5.74%

and variable rate (base rate) of 6.43% per annum (WestPac Busines Loans Rates, 2017). In order

to manage risk due to floating interest rate, Mirvac must use interest rate derivatives which

protect the firm against sudden increase in the loan interest. Besides this, firm needs to put

tighten control over the expenditures that will derive maximum yield so that it will have

sufficient liquid in the form of cash available to meet its debt covenant obligations. In addition,

cash flow management strategies need to be prepared for having enough cash to meet out debt

interest obligation as per scheduled requirement and on time.

Recommendations

On the basis of the discussion, it becomes clear that in order to take more borrowing from

the loan, company is advised to maximize its interest burden capacity by maximizing its

revenues and control direct cost so that it will have higher operational profit. By providing

collateral and improving its interest bearing ratio, it will be able to satisfy Westpac lending

conditions and could borrow the capital. In addition to that, sound cash flow management plan

through strict monitoring and control will maintain higher cash resources and manage solvency

position.

On the basis of the discussion, it becomes clear that in order to take more borrowing from

the loan, company is advised to maximize its interest burden capacity by maximizing its

revenues and control direct cost so that it will have higher operational profit. By providing

collateral and improving its interest bearing ratio, it will be able to satisfy Westpac lending

conditions and could borrow the capital. In addition to that, sound cash flow management plan

through strict monitoring and control will maintain higher cash resources and manage solvency

position.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Berg, T., 2015. Playing the devil's advocate: The causal effect of risk management on loan

quality. The Review of Financial Studies.28(12). pp.3367-3406.

Butler, A. W., Cornaggia, J. and Gurun, U. G., 2016. Do Local Capital Market Conditions Affect

Consumers’ Borrowing Decisions?. Management Science.

Halldórsson, Á., Hsuan, J. and Kotzab, H., 2015. Complementary theories to supply chain

management revisited–from borrowing theories to theorizing. Supply Chain

Management: An International Journal. 20(6). pp.574-586.

Pan, Y., Wang, T. Y. and Weisbach, M. S., 2014. Does Uncertainty about Management Affect

Firms’ Costs of Borrowing? (No. w20674). National Bureau of Economic Research.

Tumwine, S. and et.al., 2015. A borrowing cost model for effective performance of SMEs in

Uganda. World Journal of Entrepreneurship, Management and Sustainable Development.

11(2). pp.74-89.

Online

Finbar group Ltd. 2017. [Online]. Available through:

https://markets.ft.com/data/equities/tearsheet/financials?

s=FRI:ASX&subview=BalanceSheet. [Accessed on 2nd October 2017].

LendLease Group Ltd. 2017. [Online]. Available through:

https://markets.ft.com/data/equities/tearsheet/financials?

s=LLC:ASX&subview=BalanceSheet>. [Accessed on 2nd October 2017].

Mirvac Group Annual report. 2017. [PDF]. Available through: <

http://groupir.mirvac.com/icms_docs/272505_MGR_-_FY17_Annual_Report.pdf>.

[Accessed on 2nd October 2017].

Mirvac Group Ltd. 2017. [Online]. Available through:

https://markets.ft.com/data/equities/tearsheet/financials?

s=MGR:ASX&subview=BalanceSheet. [Accessed on 2nd October 2017].

Books and Journals

Berg, T., 2015. Playing the devil's advocate: The causal effect of risk management on loan

quality. The Review of Financial Studies.28(12). pp.3367-3406.

Butler, A. W., Cornaggia, J. and Gurun, U. G., 2016. Do Local Capital Market Conditions Affect

Consumers’ Borrowing Decisions?. Management Science.

Halldórsson, Á., Hsuan, J. and Kotzab, H., 2015. Complementary theories to supply chain

management revisited–from borrowing theories to theorizing. Supply Chain

Management: An International Journal. 20(6). pp.574-586.

Pan, Y., Wang, T. Y. and Weisbach, M. S., 2014. Does Uncertainty about Management Affect

Firms’ Costs of Borrowing? (No. w20674). National Bureau of Economic Research.

Tumwine, S. and et.al., 2015. A borrowing cost model for effective performance of SMEs in

Uganda. World Journal of Entrepreneurship, Management and Sustainable Development.

11(2). pp.74-89.

Online

Finbar group Ltd. 2017. [Online]. Available through:

https://markets.ft.com/data/equities/tearsheet/financials?

s=FRI:ASX&subview=BalanceSheet. [Accessed on 2nd October 2017].

LendLease Group Ltd. 2017. [Online]. Available through:

https://markets.ft.com/data/equities/tearsheet/financials?

s=LLC:ASX&subview=BalanceSheet>. [Accessed on 2nd October 2017].

Mirvac Group Annual report. 2017. [PDF]. Available through: <

http://groupir.mirvac.com/icms_docs/272505_MGR_-_FY17_Annual_Report.pdf>.

[Accessed on 2nd October 2017].

Mirvac Group Ltd. 2017. [Online]. Available through:

https://markets.ft.com/data/equities/tearsheet/financials?

s=MGR:ASX&subview=BalanceSheet. [Accessed on 2nd October 2017].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

WestPac Busines Loans Rates. 2017. [Online]. Available through:

https://www.westpac.com.au/business-banking/business-loans/business-loans-interest-

rate/. [Accessed on 2nd October 2017].

Westpac Commercial loans. n.d. [Online]. Available through:

https://www.westpac.com.au/business-banking/business-loans/commercial-loans/.

[Accessed on 3rd October 2017].

Yeates, C., 2015. Westpac imposes tougher borrowing rules on property investors.

[Online]. Available through: < http://www.smh.com.au/business/banking-and-

finance/westpac-imposes-tougher-borrowing-rules-on-property-investors-

20150504-ggtq3e.html>. [Accessed on 2nd October 2017].

Yeates, C., 2016. WestPac Lower hurdle for property investors. [Online]. Available

through: <http://www.smh.com.au/business/banking-and-finance/westpac-lowers-

deposit-hurdle-for-property-investors-20160523-gp1i2c.html>. [Accessed on 3rd

October 2017].

https://www.westpac.com.au/business-banking/business-loans/business-loans-interest-

rate/. [Accessed on 2nd October 2017].

Westpac Commercial loans. n.d. [Online]. Available through:

https://www.westpac.com.au/business-banking/business-loans/commercial-loans/.

[Accessed on 3rd October 2017].

Yeates, C., 2015. Westpac imposes tougher borrowing rules on property investors.

[Online]. Available through: < http://www.smh.com.au/business/banking-and-

finance/westpac-imposes-tougher-borrowing-rules-on-property-investors-

20150504-ggtq3e.html>. [Accessed on 2nd October 2017].

Yeates, C., 2016. WestPac Lower hurdle for property investors. [Online]. Available

through: <http://www.smh.com.au/business/banking-and-finance/westpac-lowers-

deposit-hurdle-for-property-investors-20160523-gp1i2c.html>. [Accessed on 3rd

October 2017].

APPENDIX

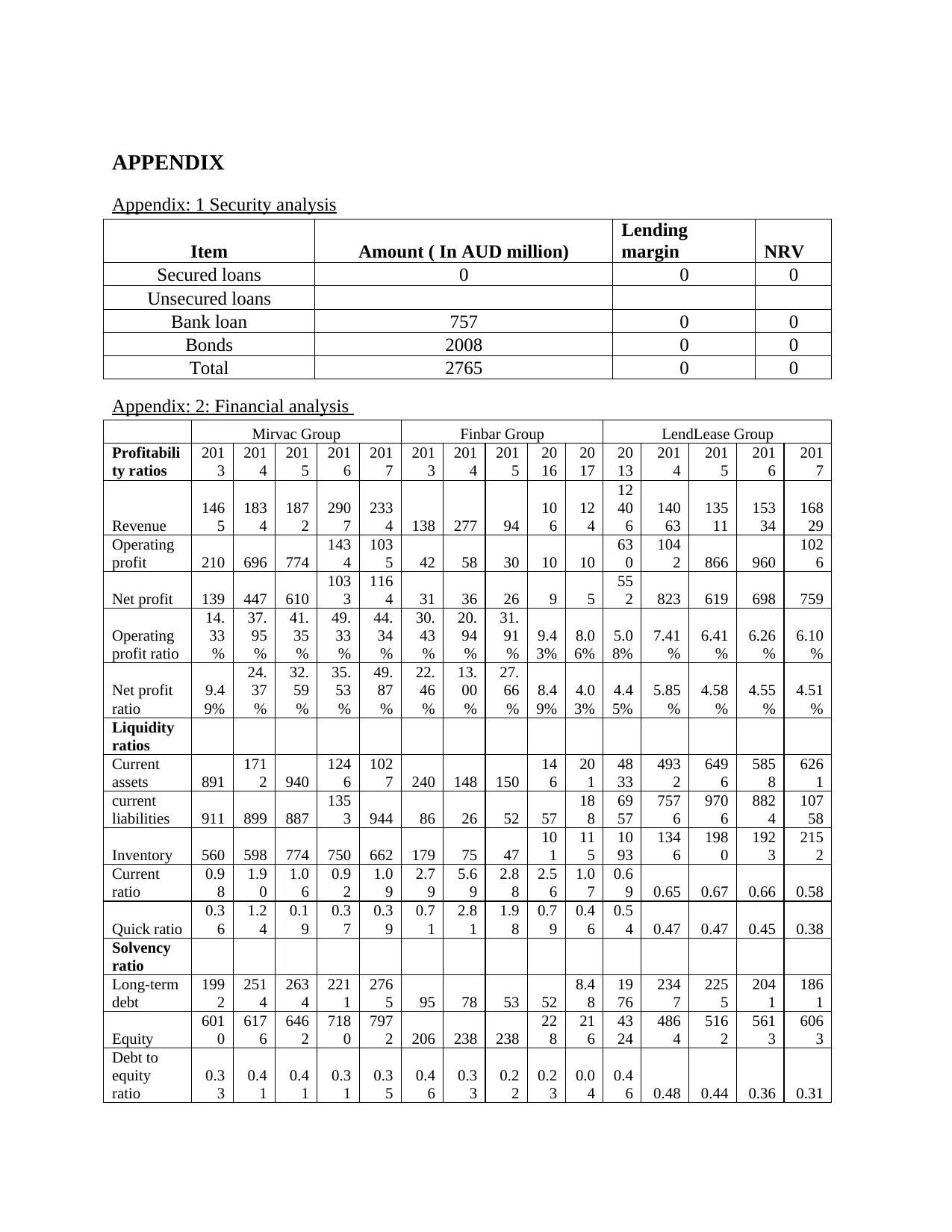

Appendix: 1 Security analysis

Item Amount ( In AUD million)

Lending

margin NRV

Secured loans 0 0 0

Unsecured loans

Bank loan 757 0 0

Bonds 2008 0 0

Total 2765 0 0

Appendix: 2: Financial analysis

Mirvac Group Finbar Group LendLease Group

Profitabili

ty ratios

201

3

201

4

201

5

201

6

201

7

201

3

201

4

201

5

20

16

20

17

20

13

201

4

201

5

201

6

201

7

Revenue

146

5

183

4

187

2

290

7

233

4 138 277 94

10

6

12

4

12

40

6

140

63

135

11

153

34

168

29

Operating

profit 210 696 774

143

4

103

5 42 58 30 10 10

63

0

104

2 866 960

102

6

Net profit 139 447 610

103

3

116

4 31 36 26 9 5

55

2 823 619 698 759

Operating

profit ratio

14.

33

%

37.

95

%

41.

35

%

49.

33

%

44.

34

%

30.

43

%

20.

94

%

31.

91

%

9.4

3%

8.0

6%

5.0

8%

7.41

%

6.41

%

6.26

%

6.10

%

Net profit

ratio

9.4

9%

24.

37

%

32.

59

%

35.

53

%

49.

87

%

22.

46

%

13.

00

%

27.

66

%

8.4

9%

4.0

3%

4.4

5%

5.85

%

4.58

%

4.55

%

4.51

%

Liquidity

ratios

Current

assets 891

171

2 940

124

6

102

7 240 148 150

14

6

20

1

48

33

493

2

649

6

585

8

626

1

current

liabilities 911 899 887

135

3 944 86 26 52 57

18

8

69

57

757

6

970

6

882

4

107

58

Inventory 560 598 774 750 662 179 75 47

10

1

11

5

10

93

134

6

198

0

192

3

215

2

Current

ratio

0.9

8

1.9

0

1.0

6

0.9

2

1.0

9

2.7

9

5.6

9

2.8

8

2.5

6

1.0

7

0.6

9 0.65 0.67 0.66 0.58

Quick ratio

0.3

6

1.2

4

0.1

9

0.3

7

0.3

9

0.7

1

2.8

1

1.9

8

0.7

9

0.4

6

0.5

4 0.47 0.47 0.45 0.38

Solvency

ratio

Long-term

debt

199

2

251

4

263

4

221

1

276

5 95 78 53 52

8.4

8

19

76

234

7

225

5

204

1

186

1

Equity

601

0

617

6

646

2

718

0

797

2 206 238 238

22

8

21

6

43

24

486

4

516

2

561

3

606

3

Debt to

equity

ratio

0.3

3

0.4

1

0.4

1

0.3

1

0.3

5

0.4

6

0.3

3

0.2

2

0.2

3

0.0

4

0.4

6 0.48 0.44 0.36 0.31

Appendix: 1 Security analysis

Item Amount ( In AUD million)

Lending

margin NRV

Secured loans 0 0 0

Unsecured loans

Bank loan 757 0 0

Bonds 2008 0 0

Total 2765 0 0

Appendix: 2: Financial analysis

Mirvac Group Finbar Group LendLease Group

Profitabili

ty ratios

201

3

201

4

201

5

201

6

201

7

201

3

201

4

201

5

20

16

20

17

20

13

201

4

201

5

201

6

201

7

Revenue

146

5

183

4

187

2

290

7

233

4 138 277 94

10

6

12

4

12

40

6

140

63

135

11

153

34

168

29

Operating

profit 210 696 774

143

4

103

5 42 58 30 10 10

63

0

104

2 866 960

102

6

Net profit 139 447 610

103

3

116

4 31 36 26 9 5

55

2 823 619 698 759

Operating

profit ratio

14.

33

%

37.

95

%

41.

35

%

49.

33

%

44.

34

%

30.

43

%

20.

94

%

31.

91

%

9.4

3%

8.0

6%

5.0

8%

7.41

%

6.41

%

6.26

%

6.10

%

Net profit

ratio

9.4

9%

24.

37

%

32.

59

%

35.

53

%

49.

87

%

22.

46

%

13.

00

%

27.

66

%

8.4

9%

4.0

3%

4.4

5%

5.85

%

4.58

%

4.55

%

4.51

%

Liquidity

ratios

Current

assets 891

171

2 940

124

6

102

7 240 148 150

14

6

20

1

48

33

493

2

649

6

585

8

626

1

current

liabilities 911 899 887

135

3 944 86 26 52 57

18

8

69

57

757

6

970

6

882

4

107

58

Inventory 560 598 774 750 662 179 75 47

10

1

11

5

10

93

134

6

198

0

192

3

215

2

Current

ratio

0.9

8

1.9

0

1.0

6

0.9

2

1.0

9

2.7

9

5.6

9

2.8

8

2.5

6

1.0

7

0.6

9 0.65 0.67 0.66 0.58

Quick ratio

0.3

6

1.2

4

0.1

9

0.3

7

0.3

9

0.7

1

2.8

1

1.9

8

0.7

9

0.4

6

0.5

4 0.47 0.47 0.45 0.38

Solvency

ratio

Long-term

debt

199

2

251

4

263

4

221

1

276

5 95 78 53 52

8.4

8

19

76

234

7

225

5

204

1

186

1

Equity

601

0

617

6

646

2

718

0

797

2 206 238 238

22

8

21

6

43

24

486

4

516

2

561

3

606

3

Debt to

equity

ratio

0.3

3

0.4

1

0.4

1

0.3

1

0.3

5

0.4

6

0.3

3

0.2

2

0.2

3

0.0

4

0.4

6 0.48 0.44 0.36 0.31

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.