Strategic Revenue Generation in MNCs: Analyzing General Productions

VerifiedAdded on 2023/06/13

|11

|3189

|488

Case Study

AI Summary

This assignment provides a comprehensive case study analysis of General Productions (GP), an electronics manufacturing specialist, as it plans to enter the mobile phone market. The study examines various senior management perspectives on revenue generation, including marketing strategies, R&D investments, and financial considerations. It discusses the implementation of social media marketing, celebrity endorsements, and product differentiation to maximize revenue. The assignment also addresses the challenges and utilities of budget systems in companies, highlighting issues like bureaucratic control and unrealistic assumptions. Furthermore, it explores the advantages and disadvantages of activity-based costing (ABC) for accurate product costing and decision-making. The analysis integrates different managerial viewpoints to develop a strategic approach for GP's mobile phone launch, emphasizing risk management and continuous product development. The document is available on Desklib, a platform offering a range of study tools and resources for students.

Running head: REVENUE GENERATION IN MNCS

Revenue Generation in MNCs

Name of the Student:

Name of the University:

Author Note:

Revenue Generation in MNCs

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

REVENUE GENERATION IN MNCS

Answer 1:

The members of the senior management of General Productions (GP) who presented their

at the management meeting were the chief marketing officer, head of research and development,

the vice president, finance and production director. General Production was a mobile phone

component manufacturing company which supplied parts to small and medium scale companies

and multinational companies. One can infer from its range of customers that the firm was

financially stable. The meeting revolved around the new business decision of the apex

management which was entry of the company into mobile phone manufacturing market, though

it had little knowledge in the area. Moreover, the sales managers often distorted their business

generation figures to earn more incentives which only added to the salary expenditure of GP

(Vahlne & Johanson, 2017).

The chief marketing officer put forward the view that the General Productions should

promote its new product, mobile phones using social media. He also put the second idea that the

company must tie up with local celebrities as brand ambassadors to endorse the product of the

company, mobile phones. It is clear from his views that these strategies were aimed at early

market penetration by employing aggressive promotional tactics to acquire customer base to buy

mobile phones (Conrado et al., 2016).

The head of research and development opined that GP should invest in incorporating

attractive features in the mobile handset models. He had the opinion that the mobile phone

models with new features would enable the company to create more demand. This demand

would enable the company use premium pricing to enter the market and generate huge revenue

(Rao & Tilt, 2016).

The vice president of finance contradicted with of research and development on the

heavy investments to develop attractive features in the mobile phones. He regarded this

investments as risks which would not contribute towards increasing the revenue generation of the

company. He instead predicted that the investment would be unprofitable because new

technological investments would render the existing technology redundant. He further added that

this investment would only result in unprofitable cash flow (Teubner, 2017).

REVENUE GENERATION IN MNCS

Answer 1:

The members of the senior management of General Productions (GP) who presented their

at the management meeting were the chief marketing officer, head of research and development,

the vice president, finance and production director. General Production was a mobile phone

component manufacturing company which supplied parts to small and medium scale companies

and multinational companies. One can infer from its range of customers that the firm was

financially stable. The meeting revolved around the new business decision of the apex

management which was entry of the company into mobile phone manufacturing market, though

it had little knowledge in the area. Moreover, the sales managers often distorted their business

generation figures to earn more incentives which only added to the salary expenditure of GP

(Vahlne & Johanson, 2017).

The chief marketing officer put forward the view that the General Productions should

promote its new product, mobile phones using social media. He also put the second idea that the

company must tie up with local celebrities as brand ambassadors to endorse the product of the

company, mobile phones. It is clear from his views that these strategies were aimed at early

market penetration by employing aggressive promotional tactics to acquire customer base to buy

mobile phones (Conrado et al., 2016).

The head of research and development opined that GP should invest in incorporating

attractive features in the mobile handset models. He had the opinion that the mobile phone

models with new features would enable the company to create more demand. This demand

would enable the company use premium pricing to enter the market and generate huge revenue

(Rao & Tilt, 2016).

The vice president of finance contradicted with of research and development on the

heavy investments to develop attractive features in the mobile phones. He regarded this

investments as risks which would not contribute towards increasing the revenue generation of the

company. He instead predicted that the investment would be unprofitable because new

technological investments would render the existing technology redundant. He further added that

this investment would only result in unprofitable cash flow (Teubner, 2017).

2

REVENUE GENERATION IN MNCS

The production director agreed with the vice of president of finance on the unprofitable

outcomes of product line extension and investments towards adding new features to the mobile

phones. He put forward the suggestion that the company should consider future business moves

like product line extensions strategically since they attract expenditure towards research.

General Product’s apex management should incorporate the opinion of the chief

marketing officer, the head of R&D, vice president, finance and production director to achieve

growth in revenue and profits. The opinion of the vice president finance and production director

may seem to be contradictory but the company can incorporate them in its new production plan

revolving around mobile phone launch. The chief marketing officer was of the opinion that

General Productions should use social media to promote its new products, the line of mobile

phones. He also proposed that the company should sign in local celebrities to endorse the mobile

phones. The company should use this promotional strategy because the strategy would enable it

to create huge demand in the market. Endorsement of the mobile phones by celebrities would

allow the company to position the phones as premium products (Petkova et al., 2014). This

would enable the mobile phones attract upper and middle class customers which would generate

huge revenue right after launch. Continuous celebrity endorsements would enable the mobile

phones attract more customers to generate more revenue. The company as a result be able to use

premium pricing strategy to generate maximum revenue in its initial stage during there would no

close competitor, since it is a new product. The company would channelize a portion of this

immense revenue to continue celebrity promotions of its mobile phones, thus gaining product

differentiation. This product differentiation would set the mobile phones of GP apart from their

emerging competing mobile phone models with more advanced technology. The company can

channelize another portion of its revenue towards bringing about more advanced versions of its

mobile phones. This would enable the company to counteract the threats from newer

technological advancements and prevent its technology from, becoming redundant

(Romiszowski, 2016). Thus this revenue would enable the company to manage the risks or

threats new technological advancements, the concern expressed by the vice president, finance.

The above analysis shows that strong promotion at through the launch and growth stages would

enable the mobile phone business earn immense revenue. This immense revenue would enable

the company to diversify its risk management and new product development research, the

REVENUE GENERATION IN MNCS

The production director agreed with the vice of president of finance on the unprofitable

outcomes of product line extension and investments towards adding new features to the mobile

phones. He put forward the suggestion that the company should consider future business moves

like product line extensions strategically since they attract expenditure towards research.

General Product’s apex management should incorporate the opinion of the chief

marketing officer, the head of R&D, vice president, finance and production director to achieve

growth in revenue and profits. The opinion of the vice president finance and production director

may seem to be contradictory but the company can incorporate them in its new production plan

revolving around mobile phone launch. The chief marketing officer was of the opinion that

General Productions should use social media to promote its new products, the line of mobile

phones. He also proposed that the company should sign in local celebrities to endorse the mobile

phones. The company should use this promotional strategy because the strategy would enable it

to create huge demand in the market. Endorsement of the mobile phones by celebrities would

allow the company to position the phones as premium products (Petkova et al., 2014). This

would enable the mobile phones attract upper and middle class customers which would generate

huge revenue right after launch. Continuous celebrity endorsements would enable the mobile

phones attract more customers to generate more revenue. The company as a result be able to use

premium pricing strategy to generate maximum revenue in its initial stage during there would no

close competitor, since it is a new product. The company would channelize a portion of this

immense revenue to continue celebrity promotions of its mobile phones, thus gaining product

differentiation. This product differentiation would set the mobile phones of GP apart from their

emerging competing mobile phone models with more advanced technology. The company can

channelize another portion of its revenue towards bringing about more advanced versions of its

mobile phones. This would enable the company to counteract the threats from newer

technological advancements and prevent its technology from, becoming redundant

(Romiszowski, 2016). Thus this revenue would enable the company to manage the risks or

threats new technological advancements, the concern expressed by the vice president, finance.

The above analysis shows that strong promotion at through the launch and growth stages would

enable the mobile phone business earn immense revenue. This immense revenue would enable

the company to diversify its risk management and new product development research, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

REVENUE GENERATION IN MNCS

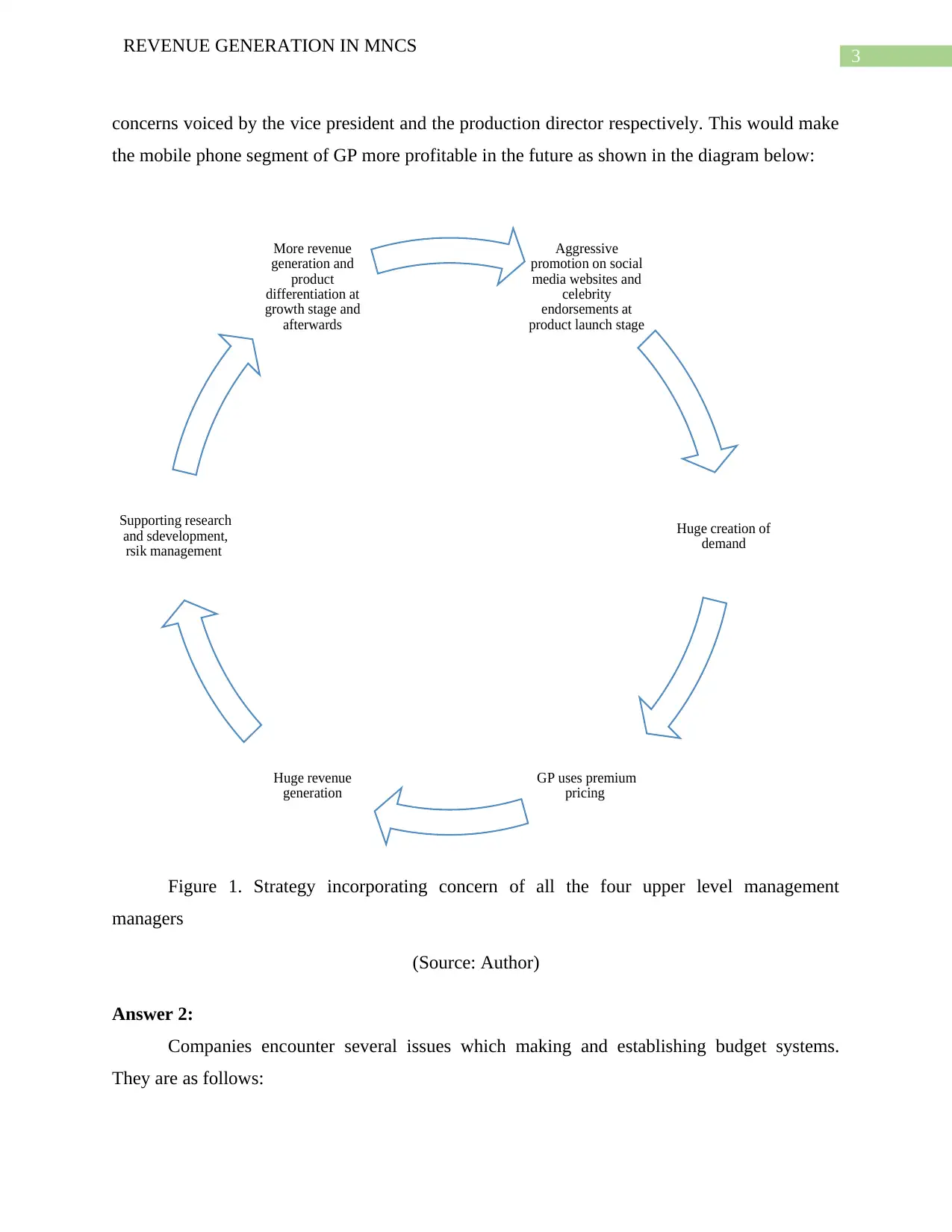

concerns voiced by the vice president and the production director respectively. This would make

the mobile phone segment of GP more profitable in the future as shown in the diagram below:

Figure 1. Strategy incorporating concern of all the four upper level management

managers

(Source: Author)

Answer 2:

Companies encounter several issues which making and establishing budget systems.

They are as follows:

Aggressive

promotion on social

media websites and

celebrity

endorsements at

product launch stage

Huge creation of

demand

GP uses premium

pricing

Huge revenue

generation

Supporting research

and sdevelopment,

rsik management

More revenue

generation and

product

differentiation at

growth stage and

afterwards

REVENUE GENERATION IN MNCS

concerns voiced by the vice president and the production director respectively. This would make

the mobile phone segment of GP more profitable in the future as shown in the diagram below:

Figure 1. Strategy incorporating concern of all the four upper level management

managers

(Source: Author)

Answer 2:

Companies encounter several issues which making and establishing budget systems.

They are as follows:

Aggressive

promotion on social

media websites and

celebrity

endorsements at

product launch stage

Huge creation of

demand

GP uses premium

pricing

Huge revenue

generation

Supporting research

and sdevelopment,

rsik management

More revenue

generation and

product

differentiation at

growth stage and

afterwards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

REVENUE GENERATION IN MNCS

Issue 1: Bureaucratic control:

Bureaucratic control poses a great issue when it comes to making and implementation of

budgets. The upper level executives often suffer from ego problems which prevents smooth

preparation of the budget. For example, it is evident from the case study that chief marketing

officer and the R&D head are in favour of launching mobile phone using advanced technological

features. The vice president, finance and the production director were not in favour of such

investments. It is evident from the discussion that VP and the production director would oppose

the acceptance of the budget towards manufacture of mobile phones. Thus, bureaucratic control

poses a serious issue in financial budget establishment (Ferry & Ahrens, 2017).

Issue 2: Unrealistic assumptions:

The budgets are based on forecasts and assumptions which may not materialize, thus only

resulting in wastage of time and money spent to make them. The apex management of companies

have to invest funds and resources towards making of the budget. For example, as per the case

study, the chief marketing officer emphasized on promotion of upcoming mobile phones on

social networking websites and use of celebrity endorsements, both of which are expensive and

require immense allocation of funds. Now, if an established mobile company introduces a new

and more innovative model of mobile phone, the entire expenditure towards R&D becomes

useless and the company suffers a great loss. Hence, the unrealistic assumption on which budgets

stand often prove faulty and lead to immense losses to companies (Rajput, 2015).

Issue 3: Negative impact on the actual operations of the business organizations:

The formation of budget often requires allocation of funds and human resources. The

companies make budgets to forecast future businesses which means that those business at the

time of making the budget have no actual revenue income. This means that the companies

actually have to allocate funds from present sources, thus depriving a part of the present

operations. For example, as per the case study, the CMO has suggested online promotions and

celebrity promotions of the mobile phones. General Productions has to allocate funds towards

these new areas without any actual income. The company in order to bear the increased

marketing expenditure may have to render some sales staffs redundant to reduce salary

expenditure (Wanyama, Burton & Helliar, 2017).

REVENUE GENERATION IN MNCS

Issue 1: Bureaucratic control:

Bureaucratic control poses a great issue when it comes to making and implementation of

budgets. The upper level executives often suffer from ego problems which prevents smooth

preparation of the budget. For example, it is evident from the case study that chief marketing

officer and the R&D head are in favour of launching mobile phone using advanced technological

features. The vice president, finance and the production director were not in favour of such

investments. It is evident from the discussion that VP and the production director would oppose

the acceptance of the budget towards manufacture of mobile phones. Thus, bureaucratic control

poses a serious issue in financial budget establishment (Ferry & Ahrens, 2017).

Issue 2: Unrealistic assumptions:

The budgets are based on forecasts and assumptions which may not materialize, thus only

resulting in wastage of time and money spent to make them. The apex management of companies

have to invest funds and resources towards making of the budget. For example, as per the case

study, the chief marketing officer emphasized on promotion of upcoming mobile phones on

social networking websites and use of celebrity endorsements, both of which are expensive and

require immense allocation of funds. Now, if an established mobile company introduces a new

and more innovative model of mobile phone, the entire expenditure towards R&D becomes

useless and the company suffers a great loss. Hence, the unrealistic assumption on which budgets

stand often prove faulty and lead to immense losses to companies (Rajput, 2015).

Issue 3: Negative impact on the actual operations of the business organizations:

The formation of budget often requires allocation of funds and human resources. The

companies make budgets to forecast future businesses which means that those business at the

time of making the budget have no actual revenue income. This means that the companies

actually have to allocate funds from present sources, thus depriving a part of the present

operations. For example, as per the case study, the CMO has suggested online promotions and

celebrity promotions of the mobile phones. General Productions has to allocate funds towards

these new areas without any actual income. The company in order to bear the increased

marketing expenditure may have to render some sales staffs redundant to reduce salary

expenditure (Wanyama, Burton & Helliar, 2017).

5

REVENUE GENERATION IN MNCS

Utility 1: Helps in launching of new products:

GP can use the budget despite these issues the company can use the budget towards the

new mobile phone launch. The company must take into account the different expenditure like

resources and employees to the extent possible for making more accurate budget and control its

new business venture of mobile phone launching (Kearney & Morris, 2015).

Utility 2: Helps in administration of costs:

New product launches require management bodies to monitor the costs on regular basis.

The budget formation as pointed out in the issues can time consuming and expensive. However,

there is no doubt that budget enable the management bodies of companies like GP form

estimates of the costs like the expenditures and losses they are like to face. They can also make

an estimate about the sources of revenue which they can earn from different sources. Thus,

though budget cannot give accurate figures, they can to a certain enable the management of the

costs in organizations (Rajput, 2015).

Utility 3: Setting of business targets:

The management can use to budget to take rough business targets like the sales figures

they want to achieve to cover the estimated costs. The CMOs of the companies like GP can set

targets and form strategies which they would tale to achieve the target sales. One can point out

without, this target would not be possible to take. Thus, budget helps companies to form sales

targets to generate revenue to support initial costs of the new businesses (Romiszowski, 2016).

Answer 3:

The first advantage of activity based costing which GP can enjoy is accuracy in setting

product cost. The system recognizes the activities which contribute to the costs which help in

more accurate cost calculation. For example, the marketing activity proposed by the chief

marketing activities are categorized under two broad heads, online marketing and celebrity

endorsements. The expenditure required for the can be considered as follows:

1. Marketing staffs to design the ways the mobile phones are to be promoted online.

2. Technical who would design and maintain the software of the company.

3. Hiring of services of social networking sites like Youtube.

REVENUE GENERATION IN MNCS

Utility 1: Helps in launching of new products:

GP can use the budget despite these issues the company can use the budget towards the

new mobile phone launch. The company must take into account the different expenditure like

resources and employees to the extent possible for making more accurate budget and control its

new business venture of mobile phone launching (Kearney & Morris, 2015).

Utility 2: Helps in administration of costs:

New product launches require management bodies to monitor the costs on regular basis.

The budget formation as pointed out in the issues can time consuming and expensive. However,

there is no doubt that budget enable the management bodies of companies like GP form

estimates of the costs like the expenditures and losses they are like to face. They can also make

an estimate about the sources of revenue which they can earn from different sources. Thus,

though budget cannot give accurate figures, they can to a certain enable the management of the

costs in organizations (Rajput, 2015).

Utility 3: Setting of business targets:

The management can use to budget to take rough business targets like the sales figures

they want to achieve to cover the estimated costs. The CMOs of the companies like GP can set

targets and form strategies which they would tale to achieve the target sales. One can point out

without, this target would not be possible to take. Thus, budget helps companies to form sales

targets to generate revenue to support initial costs of the new businesses (Romiszowski, 2016).

Answer 3:

The first advantage of activity based costing which GP can enjoy is accuracy in setting

product cost. The system recognizes the activities which contribute to the costs which help in

more accurate cost calculation. For example, the marketing activity proposed by the chief

marketing activities are categorized under two broad heads, online marketing and celebrity

endorsements. The expenditure required for the can be considered as follows:

1. Marketing staffs to design the ways the mobile phones are to be promoted online.

2. Technical who would design and maintain the software of the company.

3. Hiring of services of social networking sites like Youtube.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

REVENUE GENERATION IN MNCS

4. The company can also approach third party technology consultants to maintain and

update software.

5. Cost of acquiring software to advertise products on social networking sites

6. Interest to be paid on loans taken from banks for the new promotional tactics.

7. Advertisement expenditures on these websites based slots.

This means the apex management of GP can monitor the expenses related to their promotion

more effectively. This would also enable them to supervise the quotation of costs by the

marketing managers.

The second advantage of ABC method is that it makes costing easier because it tracks each

item to arrive at the final costs. ABC or activity based costing is a costing method which breaks

down the activities of a company into several parts and allocates costs to each parts. The parts

are broken down into resources like human resources and material resources. Now if cost is

allocated to these activities, they can be divided into fixed, variable and semi variable. The salary

of the marketing staff would include basic salary and incentives. Hence, it is semi-variable in

nature. The salary of the technical staff does not include incentives and hence is fixed in nature,

if one assumes that the number of staff remains the same.

The third advantage of the ABC costing is better decision making the apex management. The

apex management of GP would be able to break down the cost associated with the launching of

mobile phones would be able to break down the expenditure, thus able to take more accurate

decision regarding the launch.

The three disadvantages of ABC which GP should consider are:

The ABC system is very expensive because it requires the accounts department to break the

entire expenditure into cost centers. For example, GP needs to break down the cost of promoting

the new mobile phone into cost centers would require the company allocate human resources and

material resources like computers and software towards the process. This shows that ABC is

expensive.

The second disadvantage of ABC model is that it is very difficult to measure to exact

cost of the different cost centers. As far as GP is concerned, the company is about to enter the

REVENUE GENERATION IN MNCS

4. The company can also approach third party technology consultants to maintain and

update software.

5. Cost of acquiring software to advertise products on social networking sites

6. Interest to be paid on loans taken from banks for the new promotional tactics.

7. Advertisement expenditures on these websites based slots.

This means the apex management of GP can monitor the expenses related to their promotion

more effectively. This would also enable them to supervise the quotation of costs by the

marketing managers.

The second advantage of ABC method is that it makes costing easier because it tracks each

item to arrive at the final costs. ABC or activity based costing is a costing method which breaks

down the activities of a company into several parts and allocates costs to each parts. The parts

are broken down into resources like human resources and material resources. Now if cost is

allocated to these activities, they can be divided into fixed, variable and semi variable. The salary

of the marketing staff would include basic salary and incentives. Hence, it is semi-variable in

nature. The salary of the technical staff does not include incentives and hence is fixed in nature,

if one assumes that the number of staff remains the same.

The third advantage of the ABC costing is better decision making the apex management. The

apex management of GP would be able to break down the cost associated with the launching of

mobile phones would be able to break down the expenditure, thus able to take more accurate

decision regarding the launch.

The three disadvantages of ABC which GP should consider are:

The ABC system is very expensive because it requires the accounts department to break the

entire expenditure into cost centers. For example, GP needs to break down the cost of promoting

the new mobile phone into cost centers would require the company allocate human resources and

material resources like computers and software towards the process. This shows that ABC is

expensive.

The second disadvantage of ABC model is that it is very difficult to measure to exact

cost of the different cost centers. As far as GP is concerned, the company is about to enter the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

REVENUE GENERATION IN MNCS

mobile phone market. The company require to measure the cost of each component but due to its

lack of actual knowledge about the product, it would be difficult for it to judge the actual costs.

The third disadvantage of ABC system is that it is time consuming besides being

expensive. The above explanation clearly shows that companies like GP have to allocate funds

and resources to break down the entire expenditure into units. Though it is not always possible

practically to break dowm all expenditure, following this system takes a lot of time. Thus, ABC

system of accounting is extremely time consuming and may not prove profitable for companies.

This shows that ABC method would enable the company to monitor its marketing costs by

breaking them entire activities into variable, fixed and semi-variable costs. This control would

enable the apex management make better estimates and make more accurate budget. Moreover, it

would also prevent unethical marketing managers present distorted sales figure before the

management to earn undeserved incentives. This also enable the company quote accurately to its

clients and earn more revenue.

Answer 4:

Change of inventory accounting method would be adverse impact on the gross profit.

This is because change in inventory accounting method would impact the budget. For example,

the If the inventory accounting method is shifted from FIFO to weighted average method, the

value of the closing stock would change, thus changing the gross profits. Again fall in sales

prices would result result in fall in gross profit on account of increasing prime costs. Failure to

introduce a market centric product mix results in decrease in sales and increase in cost, thus

shooting up the budget. GP must consider these facts while launching the mobile phone and

promote them before finally launching them in the market. The company must ensure that the

sale price it fixes for mobile phones are able to meet the expenditure like tax and complicated

cost structure. The company before forming the budget must conduct extensive market research

to gain information like recent trends in the mobile phone market, tentative technological trends

in the market which leading companies are likely to introduce and probable ranges of the mobile

phones. General Productions can use the social media as per the recommendations of the CMO

to gain knowledge and then form strategies on research and development. The company while

ordering parts of mobile phones from suppliers must consider the same. This would enable it to

minimize or at least control the prime costs to maximize its gross profits. It would also be able to

REVENUE GENERATION IN MNCS

mobile phone market. The company require to measure the cost of each component but due to its

lack of actual knowledge about the product, it would be difficult for it to judge the actual costs.

The third disadvantage of ABC system is that it is time consuming besides being

expensive. The above explanation clearly shows that companies like GP have to allocate funds

and resources to break down the entire expenditure into units. Though it is not always possible

practically to break dowm all expenditure, following this system takes a lot of time. Thus, ABC

system of accounting is extremely time consuming and may not prove profitable for companies.

This shows that ABC method would enable the company to monitor its marketing costs by

breaking them entire activities into variable, fixed and semi-variable costs. This control would

enable the apex management make better estimates and make more accurate budget. Moreover, it

would also prevent unethical marketing managers present distorted sales figure before the

management to earn undeserved incentives. This also enable the company quote accurately to its

clients and earn more revenue.

Answer 4:

Change of inventory accounting method would be adverse impact on the gross profit.

This is because change in inventory accounting method would impact the budget. For example,

the If the inventory accounting method is shifted from FIFO to weighted average method, the

value of the closing stock would change, thus changing the gross profits. Again fall in sales

prices would result result in fall in gross profit on account of increasing prime costs. Failure to

introduce a market centric product mix results in decrease in sales and increase in cost, thus

shooting up the budget. GP must consider these facts while launching the mobile phone and

promote them before finally launching them in the market. The company must ensure that the

sale price it fixes for mobile phones are able to meet the expenditure like tax and complicated

cost structure. The company before forming the budget must conduct extensive market research

to gain information like recent trends in the mobile phone market, tentative technological trends

in the market which leading companies are likely to introduce and probable ranges of the mobile

phones. General Productions can use the social media as per the recommendations of the CMO

to gain knowledge and then form strategies on research and development. The company while

ordering parts of mobile phones from suppliers must consider the same. This would enable it to

minimize or at least control the prime costs to maximize its gross profits. It would also be able to

8

REVENUE GENERATION IN MNCS

minimize closing stock and consequent opening stock, thus maximizing gross profits. The

companies should also use software to manage their stocks of inventory more accurately. This

shows that adopting appropriate inventory accounting methods and maintaining inventory

efficiently would enabling in boosting gross profits. The companies should incorporate market

information to achieve these two targets.

REVENUE GENERATION IN MNCS

minimize closing stock and consequent opening stock, thus maximizing gross profits. The

companies should also use software to manage their stocks of inventory more accurately. This

shows that adopting appropriate inventory accounting methods and maintaining inventory

efficiently would enabling in boosting gross profits. The companies should incorporate market

information to achieve these two targets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

REVENUE GENERATION IN MNCS

References:

Conrado, S. P., Neville, K., Woodworth, S., & O’Riordan, S. (2016). Managing social media

uncertainty to support the decision making process during emergencies. Journal of

Decision Systems, 25(sup1), 171-181.

Ferry, L., & Ahrens, T. (2017). Using management control to understand public sector corporate

governance changes: Localism, public interest, and enabling control in an English local

authority. Journal of Accounting & Organizational Change, 13(4), 548-567.

Kearney, C., & Morris, M. H. (2015). Strategic renewal as a mediator of environmental effects

on public sector performance. Small Business Economics, 45(2), 425-445.

Petkova, A. P., Wadhwa, A., Yao, X., & Jain, S. (2014). Reputation and decision making under

ambiguity: a study of US venture capital firms' investments in the emerging clean energy

sector. Academy of Management Journal, 57(2), 422-448.

Rajput, N. (2015). Shareholder types, corporate governance and firm performance: An anecdote

from Indian corporate sector. Asian Journal of Finance & Accounting, 7(1), 45.

Rao, K., & Tilt, C. (2016). Board composition and corporate social responsibility: The role of

diversity, gender, strategy and decision making. Journal of Business Ethics, 138(2), 327-

347.

Romiszowski, A. J. (2016). Designing instructional systems: Decision making in course

planning and curriculum design. Routledge.

Teubner, G. (2017). Global private regimes: Neo-spontaneous law and dual constitution of

autonomous sectors?. In Public Governance in the age of globalization (pp. 71-87).

Routledge.

Vahlne, J. E., & Johanson, J. (2017). The internationalization process of the firm—a model of

knowledge development and increasing foreign market commitments. In International

Business (pp. 145-154). Routledge.

REVENUE GENERATION IN MNCS

References:

Conrado, S. P., Neville, K., Woodworth, S., & O’Riordan, S. (2016). Managing social media

uncertainty to support the decision making process during emergencies. Journal of

Decision Systems, 25(sup1), 171-181.

Ferry, L., & Ahrens, T. (2017). Using management control to understand public sector corporate

governance changes: Localism, public interest, and enabling control in an English local

authority. Journal of Accounting & Organizational Change, 13(4), 548-567.

Kearney, C., & Morris, M. H. (2015). Strategic renewal as a mediator of environmental effects

on public sector performance. Small Business Economics, 45(2), 425-445.

Petkova, A. P., Wadhwa, A., Yao, X., & Jain, S. (2014). Reputation and decision making under

ambiguity: a study of US venture capital firms' investments in the emerging clean energy

sector. Academy of Management Journal, 57(2), 422-448.

Rajput, N. (2015). Shareholder types, corporate governance and firm performance: An anecdote

from Indian corporate sector. Asian Journal of Finance & Accounting, 7(1), 45.

Rao, K., & Tilt, C. (2016). Board composition and corporate social responsibility: The role of

diversity, gender, strategy and decision making. Journal of Business Ethics, 138(2), 327-

347.

Romiszowski, A. J. (2016). Designing instructional systems: Decision making in course

planning and curriculum design. Routledge.

Teubner, G. (2017). Global private regimes: Neo-spontaneous law and dual constitution of

autonomous sectors?. In Public Governance in the age of globalization (pp. 71-87).

Routledge.

Vahlne, J. E., & Johanson, J. (2017). The internationalization process of the firm—a model of

knowledge development and increasing foreign market commitments. In International

Business (pp. 145-154). Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

REVENUE GENERATION IN MNCS

Wanyama, S., Burton, B. M., & Helliar, C. V. (2017). Corporate governance and accountability

in Uganda. Corporate Citizenship in Africa: Lessons from the Past; Paths to the Future,

54.

REVENUE GENERATION IN MNCS

Wanyama, S., Burton, B. M., & Helliar, C. V. (2017). Corporate governance and accountability

in Uganda. Corporate Citizenship in Africa: Lessons from the Past; Paths to the Future,

54.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.