Mobile Banking and Financial Innovation: Analysis and Report

VerifiedAdded on 2022/08/15

|14

|2311

|19

Report

AI Summary

This report provides a comprehensive analysis of mobile banking and financial innovation. It begins by examining the mobile banking ecosystem, including its strategy, key stakeholders (users, banks, government, etc.), and the business processes involved. The report then delves into system design, focusing on prototyping methodologies and wireframe interface design. Section C analyzes the impact of mobile banking, covering social, financial, organizational, and technical aspects, as well as highlighting key innovations. The report addresses the challenges associated with mobile banking, such as connectivity, awareness, illiteracy, and lack of trust. Furthermore, it emphasizes the benefits of mobile banking, including cost reduction, increased security, and improved customer experience. Overall, the report offers a detailed overview of the current state and future potential of mobile banking.

Running head: MOBILE BANKING AND FINANCIAL INNOVATION

MOBILE BANKING AND FINANCIAL INNOVATION

Name of the Student

Name of the University

Author Note

MOBILE BANKING AND FINANCIAL INNOVATION

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MOBILE BANKING AND FINANCIAL INNOVATION

Table of Contents

Section A – Mobile Banking Ecosystem.........................................................................................2

Strategy........................................................................................................................................2

Stakeholders.................................................................................................................................2

Business Processes.......................................................................................................................4

Benefits........................................................................................................................................5

Challenges....................................................................................................................................6

Section B - System Design..............................................................................................................7

Prototyping..................................................................................................................................7

Services........................................................................................................................................7

Wireframe Interface.....................................................................................................................7

Section C – System Impact............................................................................................................11

Social Impact.............................................................................................................................11

Financial impact.........................................................................................................................11

Organizational Impact...............................................................................................................11

Technical Impact.......................................................................................................................11

Innovations................................................................................................................................11

Table of Contents

Section A – Mobile Banking Ecosystem.........................................................................................2

Strategy........................................................................................................................................2

Stakeholders.................................................................................................................................2

Business Processes.......................................................................................................................4

Benefits........................................................................................................................................5

Challenges....................................................................................................................................6

Section B - System Design..............................................................................................................7

Prototyping..................................................................................................................................7

Services........................................................................................................................................7

Wireframe Interface.....................................................................................................................7

Section C – System Impact............................................................................................................11

Social Impact.............................................................................................................................11

Financial impact.........................................................................................................................11

Organizational Impact...............................................................................................................11

Technical Impact.......................................................................................................................11

Innovations................................................................................................................................11

2MOBILE BANKING AND FINANCIAL INNOVATION

Section A – Mobile Banking Ecosystem

Strategy

Mobile banking is a key aspect of the competitive advantage strategy in an enterprise

system. The devices are used by almost all the people around the world. It has a positive

significance for the customer satisfaction and overall usability. In the recent few years, it has

successfully enhanced the convenience, efficiency, security and accessibility for the users. Apart

from the functional efficiency, it has been seen that the mobile banking has an opposite impact

over the operational efficiency as the operational costs have been reduced dramatically in this

industry. The costs are mainly the customer service, employee and admin expenses along with

the branch expenditures. On another hand, the use of the mobile banking increases the

organizational performance significantly.

Stakeholders

The development of the mobile banking app also requires the development and

management of its stakeholders. Stakeholders are an individual or group which an affect or

affected by the development of this mobile banking app. They are categorized as the internal or

external stakeholders where the internal ones are the directly affected parties. Externals are the

parties which are affected indirectly by the actions of the internal stakeholders. In this scenario

the main important stakeholders of the mobile banking app development will be the banks, users,

network operators, government of the Netherlands, technology provider and the merchants. The

recent advancements in the mobile technology has promoted the bank users to take part in the

internet banking sector and banks to provide those services. It allows the user to do basic

Section A – Mobile Banking Ecosystem

Strategy

Mobile banking is a key aspect of the competitive advantage strategy in an enterprise

system. The devices are used by almost all the people around the world. It has a positive

significance for the customer satisfaction and overall usability. In the recent few years, it has

successfully enhanced the convenience, efficiency, security and accessibility for the users. Apart

from the functional efficiency, it has been seen that the mobile banking has an opposite impact

over the operational efficiency as the operational costs have been reduced dramatically in this

industry. The costs are mainly the customer service, employee and admin expenses along with

the branch expenditures. On another hand, the use of the mobile banking increases the

organizational performance significantly.

Stakeholders

The development of the mobile banking app also requires the development and

management of its stakeholders. Stakeholders are an individual or group which an affect or

affected by the development of this mobile banking app. They are categorized as the internal or

external stakeholders where the internal ones are the directly affected parties. Externals are the

parties which are affected indirectly by the actions of the internal stakeholders. In this scenario

the main important stakeholders of the mobile banking app development will be the banks, users,

network operators, government of the Netherlands, technology provider and the merchants. The

recent advancements in the mobile technology has promoted the bank users to take part in the

internet banking sector and banks to provide those services. It allows the user to do basic

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MOBILE BANKING AND FINANCIAL INNOVATION

functionalities without reaching to the bank by themselves. The key stakeholders of this

development are discussed below:

a. Users: Users are the fundamental reasons to develop the mobile banking app. It saves

times and money for the users of the banks. The usability requirements and satisfaction

level of the users gives an idea about the development and its success as well as.

b. Banks: Banks are the internal and main stakeholder of the mobile app. The services

provided by them will define the functionality and future of the software. Also the fee

structure of the internet and mobile banking sector are usually lower than the

conventional methods of the banking.

c. Government: Government is the external stakeholder where tax is charged by them on

the mobile payments which gives a standard to each user and banking industry. The tax

on the transaction differs for each government and country by country. Government also

plays major role in deciding that what all the user are allowed for or not as per standard.

d. Smartphone manufacturers: Recently the mobile industry has seen many

advancements and huge hike on their sales and manufacturing. Smartphone has become

an important aspect all around the world. The device in which the application will run can

have also some capabilities according to the different activities. The manufacturers have

also adopted to develop better devices which can perform all the basic standard

operations required for the banking applications.

e. Network operators: It is a separate industry from the mobile manufacturers. It main

involvement of this industry to generate income and get traffic of the network. They

expect standard income flows and loyalty of the customers which are connected by their

network to perform any internet related operations.

functionalities without reaching to the bank by themselves. The key stakeholders of this

development are discussed below:

a. Users: Users are the fundamental reasons to develop the mobile banking app. It saves

times and money for the users of the banks. The usability requirements and satisfaction

level of the users gives an idea about the development and its success as well as.

b. Banks: Banks are the internal and main stakeholder of the mobile app. The services

provided by them will define the functionality and future of the software. Also the fee

structure of the internet and mobile banking sector are usually lower than the

conventional methods of the banking.

c. Government: Government is the external stakeholder where tax is charged by them on

the mobile payments which gives a standard to each user and banking industry. The tax

on the transaction differs for each government and country by country. Government also

plays major role in deciding that what all the user are allowed for or not as per standard.

d. Smartphone manufacturers: Recently the mobile industry has seen many

advancements and huge hike on their sales and manufacturing. Smartphone has become

an important aspect all around the world. The device in which the application will run can

have also some capabilities according to the different activities. The manufacturers have

also adopted to develop better devices which can perform all the basic standard

operations required for the banking applications.

e. Network operators: It is a separate industry from the mobile manufacturers. It main

involvement of this industry to generate income and get traffic of the network. They

expect standard income flows and loyalty of the customers which are connected by their

network to perform any internet related operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MOBILE BANKING AND FINANCIAL INNOVATION

f. Merchants: The merchant are needed to be accept and promote the mobile banking

methods for betterment of the business. They expect that the transactions should be

secure, fast and zero costing.

Business Processes

The business process are the collection of the functions of a business to operate. The

functions help in fulfilling to achieve their aims. It is consisting of clearly defined inputs and

outputs of the system. The inputs are the factors ad contributes in the business and the outputs

are the objectives. The main business process for the mobile development can be directly

associated with the bank and its processes. The service provided in the application can have

some limitations, however; it includes all the basic processes which the banks have. The

processes can be altered or their approach may get change for the automating the services

through mobile banking. The different potential changes for the banking business processes can

be made for implementing the mobile banking:

i. Automation: The processes for the mobile banking are mostly more automated than the

conventional methods of visiting banks. The transfer, account statements, fund

management etc. are the most basic functions of a standard bank. These all functions will

become automated and no human authorization will require except than the user itself.

ii. Accessibility: The Accessibility of the functions will also get change for the mobile

banking as the user can access all the basic sections of their accounts using only the apps.

iii. Security: The security aspect of the user gets a new definition in mobile banking. In

conventional banking system, the common way of authorization may be the account

details and the signature of the user. On other hand, in mobile banking, there will be

different layer of authorizations to perform a single transaction securely.

f. Merchants: The merchant are needed to be accept and promote the mobile banking

methods for betterment of the business. They expect that the transactions should be

secure, fast and zero costing.

Business Processes

The business process are the collection of the functions of a business to operate. The

functions help in fulfilling to achieve their aims. It is consisting of clearly defined inputs and

outputs of the system. The inputs are the factors ad contributes in the business and the outputs

are the objectives. The main business process for the mobile development can be directly

associated with the bank and its processes. The service provided in the application can have

some limitations, however; it includes all the basic processes which the banks have. The

processes can be altered or their approach may get change for the automating the services

through mobile banking. The different potential changes for the banking business processes can

be made for implementing the mobile banking:

i. Automation: The processes for the mobile banking are mostly more automated than the

conventional methods of visiting banks. The transfer, account statements, fund

management etc. are the most basic functions of a standard bank. These all functions will

become automated and no human authorization will require except than the user itself.

ii. Accessibility: The Accessibility of the functions will also get change for the mobile

banking as the user can access all the basic sections of their accounts using only the apps.

iii. Security: The security aspect of the user gets a new definition in mobile banking. In

conventional banking system, the common way of authorization may be the account

details and the signature of the user. On other hand, in mobile banking, there will be

different layer of authorizations to perform a single transaction securely.

5MOBILE BANKING AND FINANCIAL INNOVATION

iv. Analytics: The power of the mobile analytics is more powerful than the people think of

it. The data collection by the banks will be analyzed and can be viewed by the users. The

analytics helps in decision making and predicting the direction of the business using the

customer feedbacks.

Benefits

After the technological advancements and innovations in the mobile industry, the banks

and other financial organizations have become more eager to improve their business through this.

It has been seen that using of mobile banking has increased the banking practices more frequent

than what it was earlier in the past. The benefits of the mobile banking cover the both bank and

user domains which are discussed below:

I. Most importantly the usage of the mobile banking cut down the operating costs of the

bank which can be seen in the form of the lower bank charges for their services.

II. It has been seen that the mobile banking is also cheaper than visiting ATMs or Branches

for both the user and banks.

III. It provides higher return on investments where the options for the returns are higher than

the normal methods.

IV. The more the user will get engaged to the banks, the more services will get introduced by

the banks.

V. It provides higher security than the conventional banking practices.

VI. It has a better customer experience as there are few limitations for the customers.

VII. In case of retaining the old users, the mobile banking comes to the rescue using the push

and in-app notifications.

iv. Analytics: The power of the mobile analytics is more powerful than the people think of

it. The data collection by the banks will be analyzed and can be viewed by the users. The

analytics helps in decision making and predicting the direction of the business using the

customer feedbacks.

Benefits

After the technological advancements and innovations in the mobile industry, the banks

and other financial organizations have become more eager to improve their business through this.

It has been seen that using of mobile banking has increased the banking practices more frequent

than what it was earlier in the past. The benefits of the mobile banking cover the both bank and

user domains which are discussed below:

I. Most importantly the usage of the mobile banking cut down the operating costs of the

bank which can be seen in the form of the lower bank charges for their services.

II. It has been seen that the mobile banking is also cheaper than visiting ATMs or Branches

for both the user and banks.

III. It provides higher return on investments where the options for the returns are higher than

the normal methods.

IV. The more the user will get engaged to the banks, the more services will get introduced by

the banks.

V. It provides higher security than the conventional banking practices.

VI. It has a better customer experience as there are few limitations for the customers.

VII. In case of retaining the old users, the mobile banking comes to the rescue using the push

and in-app notifications.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MOBILE BANKING AND FINANCIAL INNOVATION

Challenges

The challenges in adapting the mobile banking can depend on the different fields

of the operation. Some existing challenges in adapting the mobile banking are listed ad discuused

below:

a. Connectivity: The usage of the Mobile banking depends of the strength of the

connectivity over the particular areas. Poor mobile connectivity are the main challenges

for the banking sectors in the under development countries.

b. Awareness: Lack in awareness of the available mobile banking services are the major

challenges for the banks. Mostly in the rural areas, people do not even have the bank

accounts. This is second most large barrier for the banks.

c. Illiteracy: Illiteracy can affect the usage of a person. If people cannot understand the

application and banking procedures, it will be impossible to become a regular mobile

banking practitioner.

d. Lack of trust: Apart from all the difficulties, some people have lack of trust in the online

or mobile banking. They rather prefer the conventional methods over the mobile. The

major cause of the lack of trusts are the security threats of hacking, frauds etc.

Section B - System Design

The development of the mobile banking application is more centric around the users of

the banks. The best software development Life cycle approach will be the prototyping where the

feedback of the users can be used or the further improvements of the mobile banking

applications. The detail analysis of the prototyping methods for the mobile banking app is

discussed below:

Challenges

The challenges in adapting the mobile banking can depend on the different fields

of the operation. Some existing challenges in adapting the mobile banking are listed ad discuused

below:

a. Connectivity: The usage of the Mobile banking depends of the strength of the

connectivity over the particular areas. Poor mobile connectivity are the main challenges

for the banking sectors in the under development countries.

b. Awareness: Lack in awareness of the available mobile banking services are the major

challenges for the banks. Mostly in the rural areas, people do not even have the bank

accounts. This is second most large barrier for the banks.

c. Illiteracy: Illiteracy can affect the usage of a person. If people cannot understand the

application and banking procedures, it will be impossible to become a regular mobile

banking practitioner.

d. Lack of trust: Apart from all the difficulties, some people have lack of trust in the online

or mobile banking. They rather prefer the conventional methods over the mobile. The

major cause of the lack of trusts are the security threats of hacking, frauds etc.

Section B - System Design

The development of the mobile banking application is more centric around the users of

the banks. The best software development Life cycle approach will be the prototyping where the

feedback of the users can be used or the further improvements of the mobile banking

applications. The detail analysis of the prototyping methods for the mobile banking app is

discussed below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MOBILE BANKING AND FINANCIAL INNOVATION

Prototyping

Prototyping is rapid methodology to develop software in less time. The main idea of the

prototyping follows the launch of an early version of the software products with some basic and

standard functionalities. The prototype the gathers the important user feedbacks and relate to the

business ideas to improve the processes and the prototype both. Ultimately the prototypes are

tested in the real life environment by the potential users of the business. It allows the

development team to gather extra time for updating and maintenance of the applications. In

mobile banking industry it seems to be a form of the user centric method to gets the validation

from the user to the strategic design. A prototype can also be an initial design nor visualization of

the working application. User experiences and satisfaction can be tested in the early stages of the

mobile app development. The main stages of the prototyping for the mobile banking application

development are the requirements analysis, system design, implementation, user evaluation,

validation and maintenance.

However, the stages of the development do not define the standards of the mobile

banking application. Using a prototype will allows the bank to improve their service over time.

The stakeholders should present important information during the development too be clear

about the direction and main goal of the system. Regular meetings and conferences should be

held to be focused on the development. For example, the user will get the information about the

development from the prototype, developers will use the requirement analysis and design

information and organizational/managerial stakeholders will follow the development reports over

the time. The main criteria for developing the application in a more user centric way are listed

below:

Prototyping

Prototyping is rapid methodology to develop software in less time. The main idea of the

prototyping follows the launch of an early version of the software products with some basic and

standard functionalities. The prototype the gathers the important user feedbacks and relate to the

business ideas to improve the processes and the prototype both. Ultimately the prototypes are

tested in the real life environment by the potential users of the business. It allows the

development team to gather extra time for updating and maintenance of the applications. In

mobile banking industry it seems to be a form of the user centric method to gets the validation

from the user to the strategic design. A prototype can also be an initial design nor visualization of

the working application. User experiences and satisfaction can be tested in the early stages of the

mobile app development. The main stages of the prototyping for the mobile banking application

development are the requirements analysis, system design, implementation, user evaluation,

validation and maintenance.

However, the stages of the development do not define the standards of the mobile

banking application. Using a prototype will allows the bank to improve their service over time.

The stakeholders should present important information during the development too be clear

about the direction and main goal of the system. Regular meetings and conferences should be

held to be focused on the development. For example, the user will get the information about the

development from the prototype, developers will use the requirement analysis and design

information and organizational/managerial stakeholders will follow the development reports over

the time. The main criteria for developing the application in a more user centric way are listed

below:

8MOBILE BANKING AND FINANCIAL INNOVATION

Stability & Performance: The application should attain high stability and convenient

performance irrespective of the device performance. The system should able to take all the load,

stress and soak testing. The stable performance will keep the users engaged and they will prefer

the application over any other method or application.

Personalized design: Personalization is the most require aspect of a user centric development. It

should allow the user to personalize the design or features by setting or analyzing consumer

behaviors. The Authentication of the application using the usernames and passwords also comes

under the personalization where the user should be able to create their own user name and

password within the criteria of the creation.

High-end Security: Users data and transaction data is the most confidential information type of

information in any banking system. The data privacy and security should be the first priority of

the system. Potential loopholes in the system can attract the hackers who can damage the user

and bank system both. Using encryption, different layers of authorization and QR codes for

transaction should provide better security.

Verification: Before releasing the system, testing and verification should be important aspect for

any developed application or system. It should have basic standard functionalities which is

performed in bank system. The One-time-password verification should also be present to support

the security parameters of the application.

Feedback: Even after the development, the feedback of the users is important as it will help in

the further devolvement in the application. It also keeps the user engaged while introducing

better features and fixing errors. The feedback can be in terms of the ratings, messages or

Stability & Performance: The application should attain high stability and convenient

performance irrespective of the device performance. The system should able to take all the load,

stress and soak testing. The stable performance will keep the users engaged and they will prefer

the application over any other method or application.

Personalized design: Personalization is the most require aspect of a user centric development. It

should allow the user to personalize the design or features by setting or analyzing consumer

behaviors. The Authentication of the application using the usernames and passwords also comes

under the personalization where the user should be able to create their own user name and

password within the criteria of the creation.

High-end Security: Users data and transaction data is the most confidential information type of

information in any banking system. The data privacy and security should be the first priority of

the system. Potential loopholes in the system can attract the hackers who can damage the user

and bank system both. Using encryption, different layers of authorization and QR codes for

transaction should provide better security.

Verification: Before releasing the system, testing and verification should be important aspect for

any developed application or system. It should have basic standard functionalities which is

performed in bank system. The One-time-password verification should also be present to support

the security parameters of the application.

Feedback: Even after the development, the feedback of the users is important as it will help in

the further devolvement in the application. It also keeps the user engaged while introducing

better features and fixing errors. The feedback can be in terms of the ratings, messages or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MOBILE BANKING AND FINANCIAL INNOVATION

complains about the application. The developers can also measure the feedback of the users

through the application responses and success rate of the functionalities.

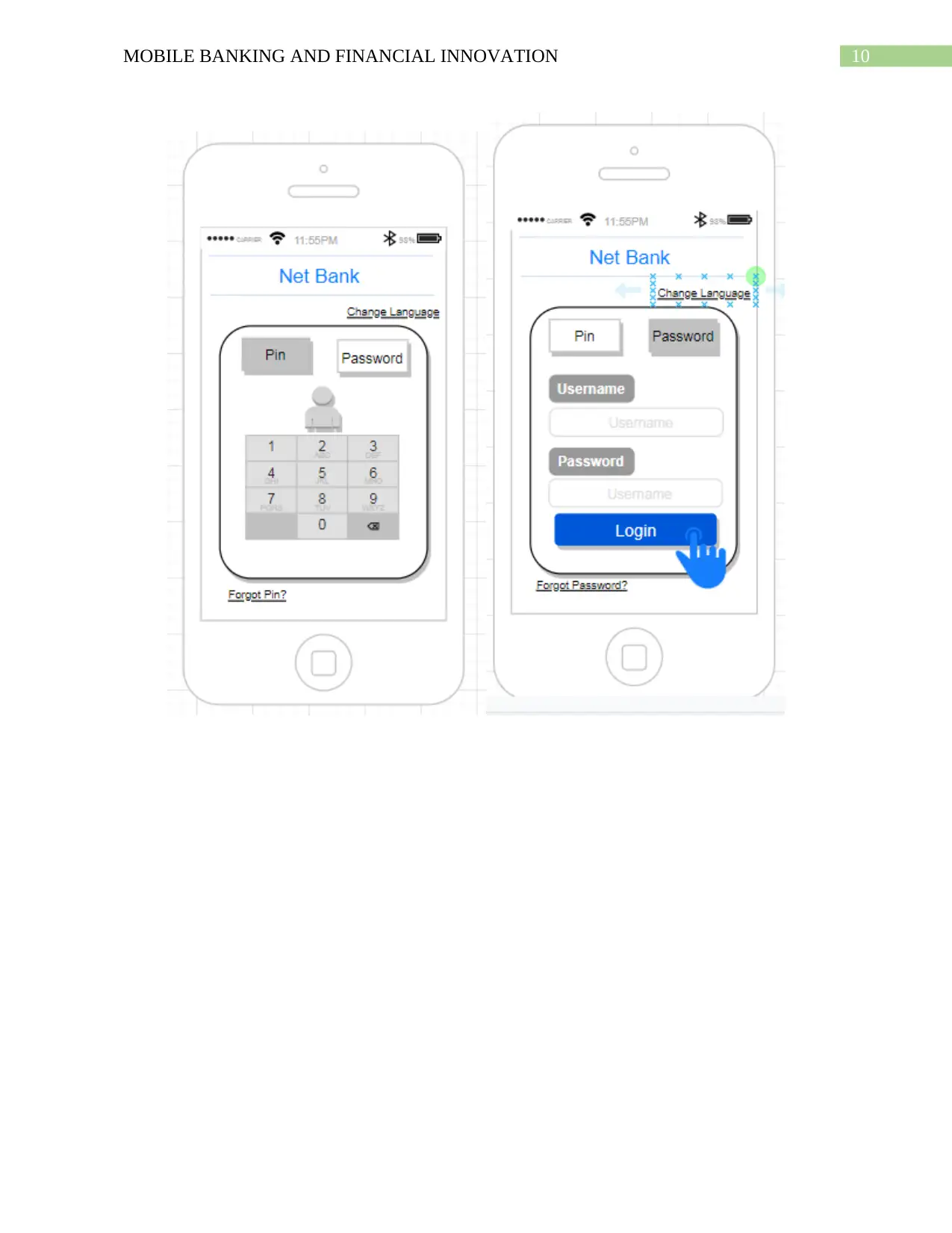

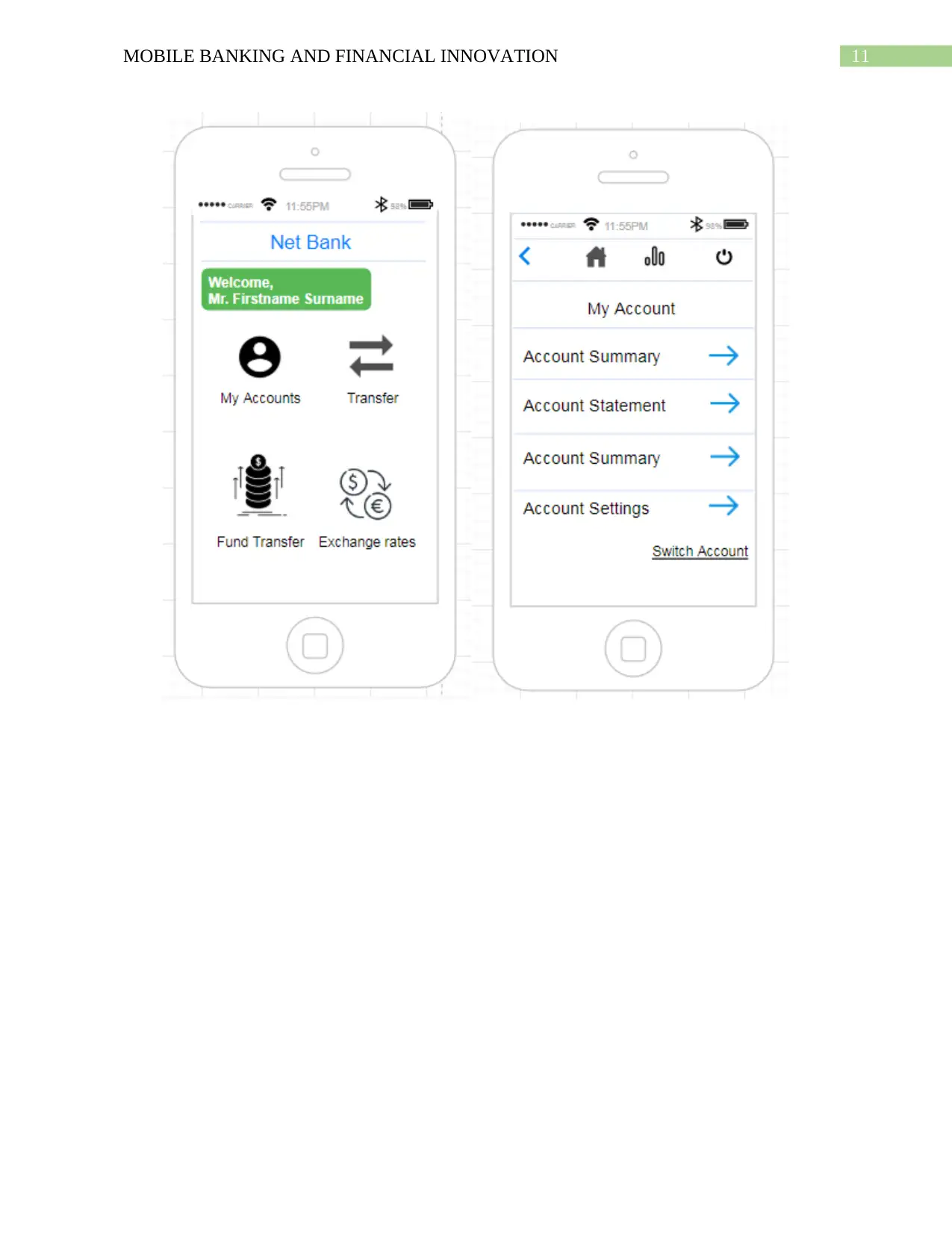

Wireframe Interface Design

Wireframe is a part of user interface design where the design is explained on a structured

level. It commonly focuses the contents and functionality of the UI which is the different than

the visual design of the page. The main of the wireframe to show the layout of the page, and

explain the elements of the interface. It is designed in order to meet the user expectations from

the application. It is very easy and cheap way to represent the structure of the key pages for the

system. It can be hand drawn or developed using software tools which are available for free on

different online platforms. Below the wireframe design for the mobile banking application has

been show which is developed on the “draw.io” platform.

complains about the application. The developers can also measure the feedback of the users

through the application responses and success rate of the functionalities.

Wireframe Interface Design

Wireframe is a part of user interface design where the design is explained on a structured

level. It commonly focuses the contents and functionality of the UI which is the different than

the visual design of the page. The main of the wireframe to show the layout of the page, and

explain the elements of the interface. It is designed in order to meet the user expectations from

the application. It is very easy and cheap way to represent the structure of the key pages for the

system. It can be hand drawn or developed using software tools which are available for free on

different online platforms. Below the wireframe design for the mobile banking application has

been show which is developed on the “draw.io” platform.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MOBILE BANKING AND FINANCIAL INNOVATION

11MOBILE BANKING AND FINANCIAL INNOVATION

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.