An Investigation into Factors Influencing Mobile Banking Usage

VerifiedAdded on 2023/01/17

|65

|20694

|38

Report

AI Summary

This research dissertation abstract explores the factors influencing mobile banking usage, particularly within the Malaysian context. The study investigates the evolution of banking services through mobile banking, highlighting its convenience and ease of use. It examines the impact of mobile banking features like fund transfers and balance inquiries, and analyzes the shift towards digital channels. The research focuses on the Technology Acceptance Model (TAM) to understand the behavioral intentions of individuals, considering perceived ease of use, perceived usefulness, and perceived risk. The literature review provides a comprehensive analysis of these factors, supported by relevant studies and data. The research methodology is outlined, and the data analysis is presented. The study aims to identify key factors influencing mobile banking adoption, offering insights into how banks can enhance services and meet customer needs. The study also includes a self-reflection and recommendations for future research in this area.

Research Dissertation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

Mobile phones have become the tool for everyday life and therefore it develops an

opportunity for the evolution of banking services through mobile banking. By the assistance of

this, an individual can make use of various such as fund transfer, balance enquiry, transaction

alert and many more. The mobile banking brings a lot changes in banking services such as ease

of communication, quickly deposits and decline use of employees. The increasing development

in the number of mobile banking users has assist the banking sector to be focus towards

executing and adopting advance mobile banking features for providing easy facilities to their

customers and shows that mobiles phones are not any-more only used for entertainment or their

any typical reasons. Banking sector has mainly converted internet, mobile applications and apps

into the most appropriate channel for offering banking products and services to their significant

clients. It is important for Banks now to make use of advanced technology, which help in

providing quick and on time service to customers. Thus, banks are very much focuses over

developing easy technology, which are based on perceived ease of use for the purpose of

affecting an individual intention to adopt and use mobile banking. The main innovation in

banking services includes the mobile banking, digital wallet, aggregators, big data analytics and

so on. Nowadays, every person has smart phone, which help them to easily access their bank

accounts without going to the banks and also help in transferring amount quickly. The banks has

developed their own applications in order to provide better services and to increase the usage of

mobile banking. The increasing use of mobile application and services has made easy for buyers

to access through everywhere and at any time.

Mobile phones have become the tool for everyday life and therefore it develops an

opportunity for the evolution of banking services through mobile banking. By the assistance of

this, an individual can make use of various such as fund transfer, balance enquiry, transaction

alert and many more. The mobile banking brings a lot changes in banking services such as ease

of communication, quickly deposits and decline use of employees. The increasing development

in the number of mobile banking users has assist the banking sector to be focus towards

executing and adopting advance mobile banking features for providing easy facilities to their

customers and shows that mobiles phones are not any-more only used for entertainment or their

any typical reasons. Banking sector has mainly converted internet, mobile applications and apps

into the most appropriate channel for offering banking products and services to their significant

clients. It is important for Banks now to make use of advanced technology, which help in

providing quick and on time service to customers. Thus, banks are very much focuses over

developing easy technology, which are based on perceived ease of use for the purpose of

affecting an individual intention to adopt and use mobile banking. The main innovation in

banking services includes the mobile banking, digital wallet, aggregators, big data analytics and

so on. Nowadays, every person has smart phone, which help them to easily access their bank

accounts without going to the banks and also help in transferring amount quickly. The banks has

developed their own applications in order to provide better services and to increase the usage of

mobile banking. The increasing use of mobile application and services has made easy for buyers

to access through everywhere and at any time.

Table of Contents

Abstract............................................................................................................................................2

Title..................................................................................................................................................1

Chapter 1: Introduction....................................................................................................................1

Chapter 2: Literature Review...........................................................................................................3

An understanding regarding the behavioural intention of people to use mobile banking with

the support of Technology Acceptance Model.......................................................................3

The impact of Perceived Ease of Use (PEOU) and its significant impact towards intention to

adapt mobile banking.............................................................................................................7

The significant impact of Perceived Usefulness (PU) towards adaptation to mobile banking.

................................................................................................................................................9

The impact of Perceived Risk (PR) towards adaptation to mobile banking.........................12

Chapter 3: Research Methodology.................................................................................................21

Chapter 4: Data Analysis...............................................................................................................29

Chapter 5: Conclusion....................................................................................................................51

Chapter 6: Recommendation..........................................................................................................53

Chapter 7: Self-Reflection.............................................................................................................54

References......................................................................................................................................57

Abstract............................................................................................................................................2

Title..................................................................................................................................................1

Chapter 1: Introduction....................................................................................................................1

Chapter 2: Literature Review...........................................................................................................3

An understanding regarding the behavioural intention of people to use mobile banking with

the support of Technology Acceptance Model.......................................................................3

The impact of Perceived Ease of Use (PEOU) and its significant impact towards intention to

adapt mobile banking.............................................................................................................7

The significant impact of Perceived Usefulness (PU) towards adaptation to mobile banking.

................................................................................................................................................9

The impact of Perceived Risk (PR) towards adaptation to mobile banking.........................12

Chapter 3: Research Methodology.................................................................................................21

Chapter 4: Data Analysis...............................................................................................................29

Chapter 5: Conclusion....................................................................................................................51

Chapter 6: Recommendation..........................................................................................................53

Chapter 7: Self-Reflection.............................................................................................................54

References......................................................................................................................................57

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Title

Factors Influencing the Usage of Mobile Banking

Chapter 1: Introduction

Overview of the Research

This study aim to analysing the potential factors that influences the usage of mobile

banking, therefore, Mobile phones have become the tool for every day life, thus it creates an

opportunity for the evolution of banking service to reach the previously banked population by

mobile banking (Zhou, 2011). In addition to this, banking is one of the most regulated industry in

the globe, thus the banks in both private and public sector, reached a remarkable position due to

its high level of technology. Therefore, mobile banking is an innovative technology which has

attained popularity in the globe. Mobile banking services consist of things likewise balance

enquiry, fund transfer in between of other facilities. The adoption of mobile banking has brought

about changes in banking operations that are following the advancement of mobile

communication techniques and the collaboration with mobile service providers as a result, the

mobile banking technology has become more conductive to individuals and banking sector.

Mobile banking is recognised as a channel whereby the buyers interacts with a bank through

mobile devices like as mobile phone and personal digital assistance (Alalwan, Dwivedi and

Rana, 2017). In the present investigation work, the study is focuses over Malaysia, thus the

financial industry in Malaysia plays an effective role in not only as a service provided but also as

a strong banking industry which supports economic growth to deliver efficient services, that are

significant for the benefits of customers and banks.

Rationale of the Research

The investigation into consideration is based on the factors that influencing the usage of

Mobile Banking. The scope of study is wide as, this investigation is effective in exploring the

idea and knowledge in regarding to the chosen area of investigation (Lee and et. al., 2012). This

study is mainly significant in developing the knowledge of individual in regards to the area of the

factors that are affecting the usage of mobile banking. The key purpose of conducting the

research is the personal interest of the researcher, therefore, this study will be effective for an

individual, learner or researcher in conducting their future project in more effective manner.

Research Aim

1

Factors Influencing the Usage of Mobile Banking

Chapter 1: Introduction

Overview of the Research

This study aim to analysing the potential factors that influences the usage of mobile

banking, therefore, Mobile phones have become the tool for every day life, thus it creates an

opportunity for the evolution of banking service to reach the previously banked population by

mobile banking (Zhou, 2011). In addition to this, banking is one of the most regulated industry in

the globe, thus the banks in both private and public sector, reached a remarkable position due to

its high level of technology. Therefore, mobile banking is an innovative technology which has

attained popularity in the globe. Mobile banking services consist of things likewise balance

enquiry, fund transfer in between of other facilities. The adoption of mobile banking has brought

about changes in banking operations that are following the advancement of mobile

communication techniques and the collaboration with mobile service providers as a result, the

mobile banking technology has become more conductive to individuals and banking sector.

Mobile banking is recognised as a channel whereby the buyers interacts with a bank through

mobile devices like as mobile phone and personal digital assistance (Alalwan, Dwivedi and

Rana, 2017). In the present investigation work, the study is focuses over Malaysia, thus the

financial industry in Malaysia plays an effective role in not only as a service provided but also as

a strong banking industry which supports economic growth to deliver efficient services, that are

significant for the benefits of customers and banks.

Rationale of the Research

The investigation into consideration is based on the factors that influencing the usage of

Mobile Banking. The scope of study is wide as, this investigation is effective in exploring the

idea and knowledge in regarding to the chosen area of investigation (Lee and et. al., 2012). This

study is mainly significant in developing the knowledge of individual in regards to the area of the

factors that are affecting the usage of mobile banking. The key purpose of conducting the

research is the personal interest of the researcher, therefore, this study will be effective for an

individual, learner or researcher in conducting their future project in more effective manner.

Research Aim

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is the most imperative part of an investigation as it is effective in assisting the

overall work in right manner to reaching at the potential outcome (Al-Jabri and Sohail, 2012).

The key aim of this investigation is "To investigate the factors that are influencing the use of

Mobile banking". A study on Malaysia.

Research Objectives

To understand the behavioural intention of people to use mobile banking with the support

of Technology Acceptance Model.

To determine the impact of Perceived Ease of Use (PEOU) and its significant impact

towards intention to adapt mobile banking

To explore the significant impact of Perceived Usefulness (PU) towards adaptation to

mobile banking To investigate the impact of Perceived Risk (PR) towards adaptation to mobile banking

Research Questions

What is behavioural intention of people to use mobile banking with the support of

Technology Acceptance Model?

What is the impact of Perceived Ease of Use (PEOU) and its significant impact towards

intention to adapt mobile banking?

What is the significant impact of Perceived Usefulness (PU) towards adaptation to mobile

banking?

What is the impact of Perceived Risk (PR) towards adaptation to mobile banking?

2

overall work in right manner to reaching at the potential outcome (Al-Jabri and Sohail, 2012).

The key aim of this investigation is "To investigate the factors that are influencing the use of

Mobile banking". A study on Malaysia.

Research Objectives

To understand the behavioural intention of people to use mobile banking with the support

of Technology Acceptance Model.

To determine the impact of Perceived Ease of Use (PEOU) and its significant impact

towards intention to adapt mobile banking

To explore the significant impact of Perceived Usefulness (PU) towards adaptation to

mobile banking To investigate the impact of Perceived Risk (PR) towards adaptation to mobile banking

Research Questions

What is behavioural intention of people to use mobile banking with the support of

Technology Acceptance Model?

What is the impact of Perceived Ease of Use (PEOU) and its significant impact towards

intention to adapt mobile banking?

What is the significant impact of Perceived Usefulness (PU) towards adaptation to mobile

banking?

What is the impact of Perceived Risk (PR) towards adaptation to mobile banking?

2

Chapter 2: Literature Review

This refers as the most imperative part of an investigation, therefore, this is effective in

providing significant analysis over the area of the factors that are influencing the use of Mobile

banking. This section of research is effective in developing a detailed analysis over the chosen

subject area, for the purpose of developing understanding of the researcher and learner towards

the specific area. This section of investigation is mainly replay upon secondary source of

information accumulation (Akturan and Tezcan, 2012). Therefore, in this information is

accumulated through books, journals, published research articles and so on. This section of

imperative in developing an in-depth analysis which is supportive in creating theoretical

perspective over the chosen study area and enhance the understanding of an individual with the

development of theoretical base.

An understanding regarding the behavioural intention of people to use mobile banking with the

support of Technology Acceptance Model.

As per the opinion stated by Darmesh Krishanan, Aye Aye Khin and Kevin Teng, 2015,

The advancement and emergence of technology mainly the wireless tools has transformed the

way in which banks operates their transactions and that are been done now a day's far from the

traditional method of banking system where an individual has to visit a bank to making their

transaction success or making any kind of deposit etc. and so as to now individual carry out their

banking transaction to the use of advance technologies like intent banking, Automatic teller

machine, e-banking, mobile banking or m-Banking etc. (Hanafizadeh and et. al., 2014). As per

the opinion stated by Muazu Muazu, 2020, The continuous development of the Mobile and

wireless market during the past few decades has it to the leading growing market at global level

with a wider number of mobile subscriber that would be around 5.9 billion subscriber globally

(Zhou, 2012). According to the opinion stated by Shuhaida Mohamed Shuhidan, Saidtul Rahah

Hamidi and Intan Syazwani Saleh, 2017, mobile banking is recognised as the most appropriate

source of providing convenience to the banks and their customers as an individual and bank both

are able to perform their banking transactions outside offices and off the working hours as it can

be accessed through anywhere at any time for that it might indeed become a preference to the

buyers. In the context of Malaysia, mobile banking was embraced few decades age through the

banking sector and a enhance banking sector is of the potential importance to a country through

3

This refers as the most imperative part of an investigation, therefore, this is effective in

providing significant analysis over the area of the factors that are influencing the use of Mobile

banking. This section of research is effective in developing a detailed analysis over the chosen

subject area, for the purpose of developing understanding of the researcher and learner towards

the specific area. This section of investigation is mainly replay upon secondary source of

information accumulation (Akturan and Tezcan, 2012). Therefore, in this information is

accumulated through books, journals, published research articles and so on. This section of

imperative in developing an in-depth analysis which is supportive in creating theoretical

perspective over the chosen study area and enhance the understanding of an individual with the

development of theoretical base.

An understanding regarding the behavioural intention of people to use mobile banking with the

support of Technology Acceptance Model.

As per the opinion stated by Darmesh Krishanan, Aye Aye Khin and Kevin Teng, 2015,

The advancement and emergence of technology mainly the wireless tools has transformed the

way in which banks operates their transactions and that are been done now a day's far from the

traditional method of banking system where an individual has to visit a bank to making their

transaction success or making any kind of deposit etc. and so as to now individual carry out their

banking transaction to the use of advance technologies like intent banking, Automatic teller

machine, e-banking, mobile banking or m-Banking etc. (Hanafizadeh and et. al., 2014). As per

the opinion stated by Muazu Muazu, 2020, The continuous development of the Mobile and

wireless market during the past few decades has it to the leading growing market at global level

with a wider number of mobile subscriber that would be around 5.9 billion subscriber globally

(Zhou, 2012). According to the opinion stated by Shuhaida Mohamed Shuhidan, Saidtul Rahah

Hamidi and Intan Syazwani Saleh, 2017, mobile banking is recognised as the most appropriate

source of providing convenience to the banks and their customers as an individual and bank both

are able to perform their banking transactions outside offices and off the working hours as it can

be accessed through anywhere at any time for that it might indeed become a preference to the

buyers. In the context of Malaysia, mobile banking was embraced few decades age through the

banking sector and a enhance banking sector is of the potential importance to a country through

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

supporting the economic development by its efficient services. In the modern scenario,

individual are living in a busy schedule and they are mainly seeking for comfortable facilities, so

in the terms of conducting banking transaction, people are from past few decades are concern

over using mobile banking as to making easy transaction without making any extra efforts.

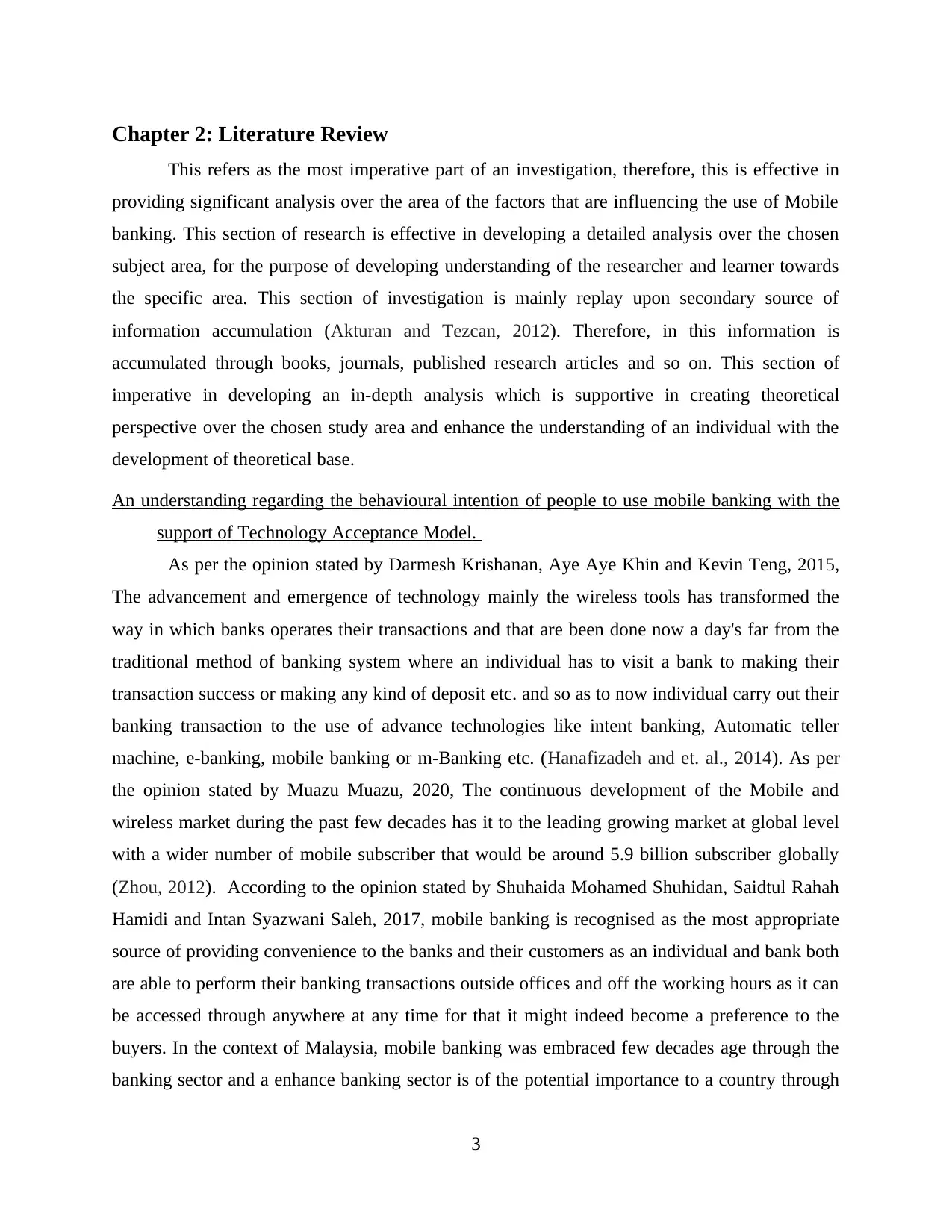

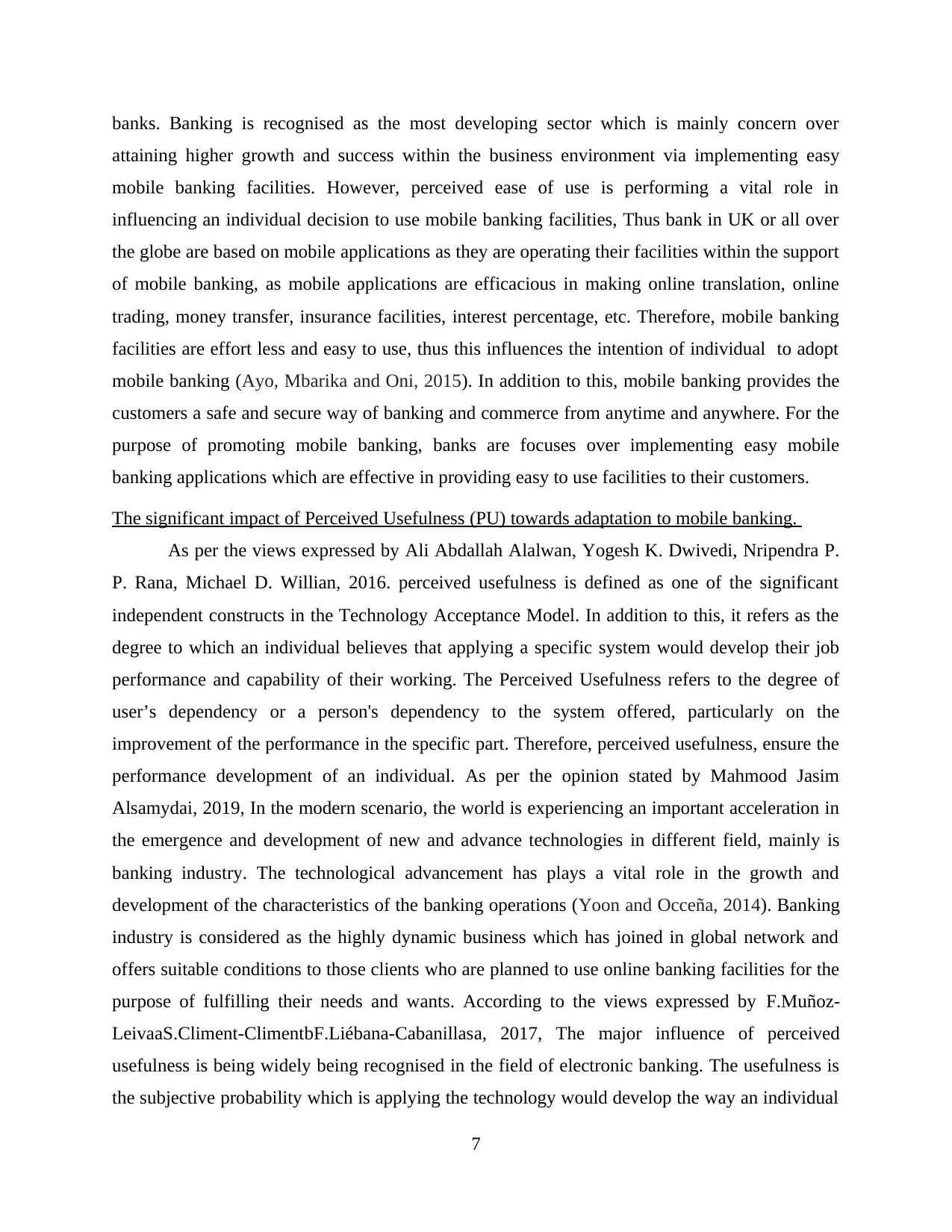

(Source: Percentage of Smartphone Users by Age Category, 2020)

The above mentioned graph stated that, Malaysian Communications or Multimedia

commission in survey hand phone user survey 2014, stated that 52.4 percentage of respondent

applying smartphone. As per the analysis it has been determined that young adulthood in the age

group of 20 to 39 have the highest smartphone user in Malaysia. Therefore, young adulthood are

recognised as the most appropriate age group who are concerning over using smartphones,

therefore people from this age group are doing any job and persuading education, or conducting

any personal business and for which they are frequently using mobile banking facilities to fulfil

their needs of banking operations (Lin, 2011). The emergence of advance technology especially

internet or mobile banking is easy in Malaysia, as individual's are using mobiles for their

personal needs and wants, therefore, the high usage in the young adult hood from the age of 24 to

39 has leads the execution of mobile banking in the Malaysia. However, people are very much

attracted by the easy and free from efforts facilities. Mobile banking is still in its conception step

in Malaysia. Therefore, Mobile banking is obfuscate as the ability to execute bank transactions

with the help of mobile device, or more broadly to conduct financial transactions through a

mobile terminal. In addition to this, mobile banking is defined as “a channel whereby the clients

4

Illustration 1: Percentage of Smartphone Users by Age Category, 2020.

individual are living in a busy schedule and they are mainly seeking for comfortable facilities, so

in the terms of conducting banking transaction, people are from past few decades are concern

over using mobile banking as to making easy transaction without making any extra efforts.

(Source: Percentage of Smartphone Users by Age Category, 2020)

The above mentioned graph stated that, Malaysian Communications or Multimedia

commission in survey hand phone user survey 2014, stated that 52.4 percentage of respondent

applying smartphone. As per the analysis it has been determined that young adulthood in the age

group of 20 to 39 have the highest smartphone user in Malaysia. Therefore, young adulthood are

recognised as the most appropriate age group who are concerning over using smartphones,

therefore people from this age group are doing any job and persuading education, or conducting

any personal business and for which they are frequently using mobile banking facilities to fulfil

their needs of banking operations (Lin, 2011). The emergence of advance technology especially

internet or mobile banking is easy in Malaysia, as individual's are using mobiles for their

personal needs and wants, therefore, the high usage in the young adult hood from the age of 24 to

39 has leads the execution of mobile banking in the Malaysia. However, people are very much

attracted by the easy and free from efforts facilities. Mobile banking is still in its conception step

in Malaysia. Therefore, Mobile banking is obfuscate as the ability to execute bank transactions

with the help of mobile device, or more broadly to conduct financial transactions through a

mobile terminal. In addition to this, mobile banking is defined as “a channel whereby the clients

4

Illustration 1: Percentage of Smartphone Users by Age Category, 2020.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interacts with a bank via mobile device, such as a mobile phone or personal digital assistant.

Therefore, these are effective in making banking transaction more easy and reliable which are

efficacious in satisfying the needs and wants of people at market place. In today's modern era,

individual are living in a busy schedule and this is the major reason of adopting advance

technologies for fulfilling their needs without making any kind of extra efforts.

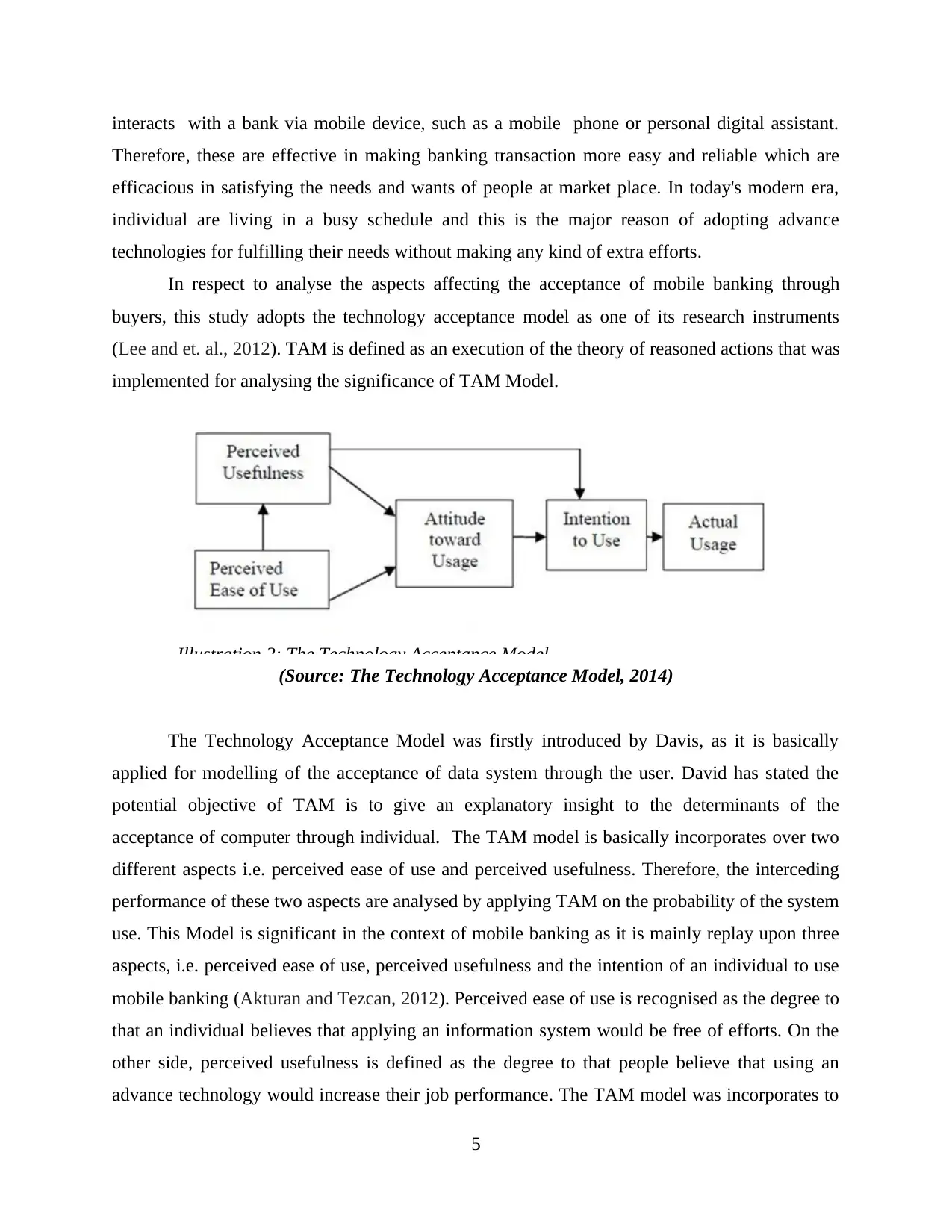

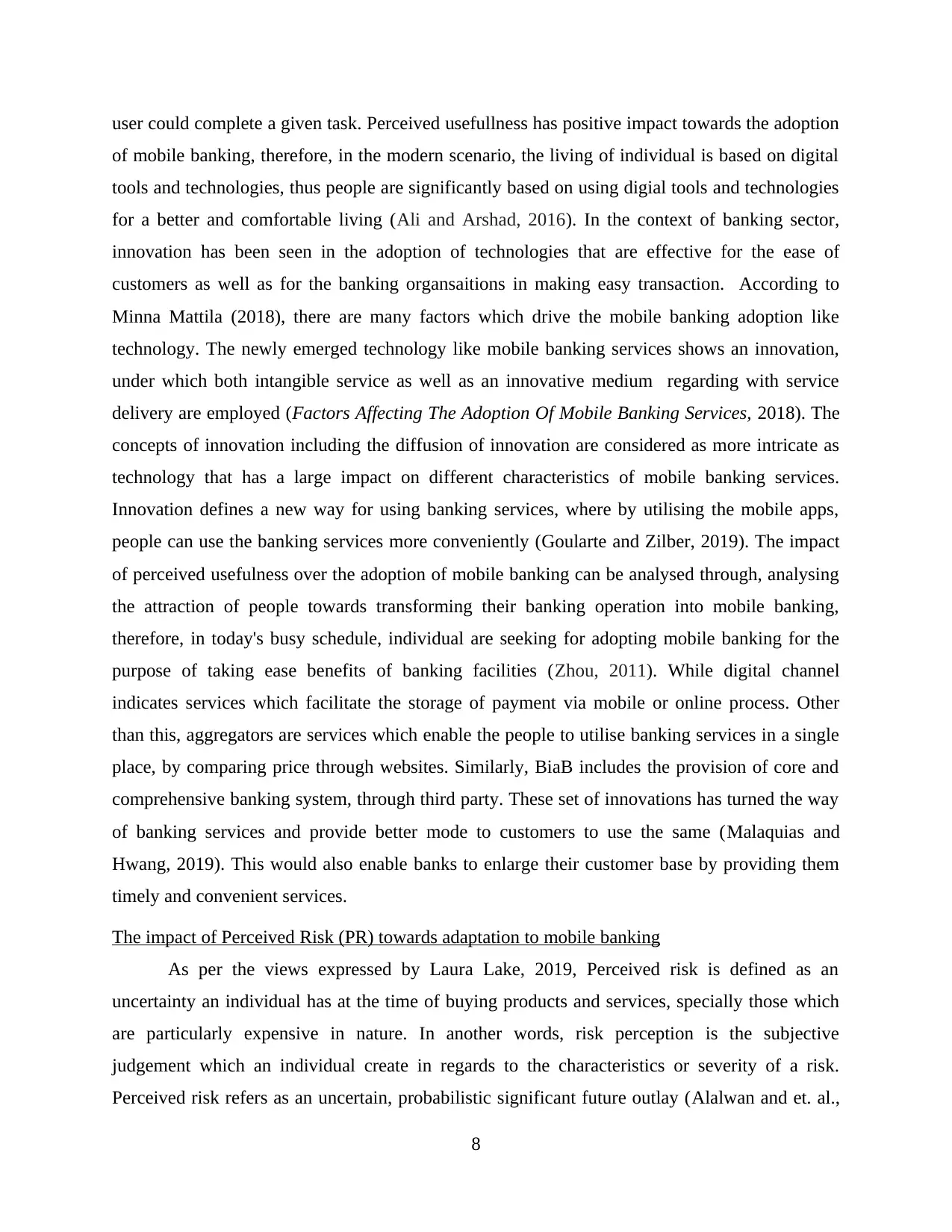

In respect to analyse the aspects affecting the acceptance of mobile banking through

buyers, this study adopts the technology acceptance model as one of its research instruments

(Lee and et. al., 2012). TAM is defined as an execution of the theory of reasoned actions that was

implemented for analysing the significance of TAM Model.

(Source: The Technology Acceptance Model, 2014)

The Technology Acceptance Model was firstly introduced by Davis, as it is basically

applied for modelling of the acceptance of data system through the user. David has stated the

potential objective of TAM is to give an explanatory insight to the determinants of the

acceptance of computer through individual. The TAM model is basically incorporates over two

different aspects i.e. perceived ease of use and perceived usefulness. Therefore, the interceding

performance of these two aspects are analysed by applying TAM on the probability of the system

use. This Model is significant in the context of mobile banking as it is mainly replay upon three

aspects, i.e. perceived ease of use, perceived usefulness and the intention of an individual to use

mobile banking (Akturan and Tezcan, 2012). Perceived ease of use is recognised as the degree to

that an individual believes that applying an information system would be free of efforts. On the

other side, perceived usefulness is defined as the degree to that people believe that using an

advance technology would increase their job performance. The TAM model was incorporates to

5

Illustration 2: The Technology Acceptance Model.

Therefore, these are effective in making banking transaction more easy and reliable which are

efficacious in satisfying the needs and wants of people at market place. In today's modern era,

individual are living in a busy schedule and this is the major reason of adopting advance

technologies for fulfilling their needs without making any kind of extra efforts.

In respect to analyse the aspects affecting the acceptance of mobile banking through

buyers, this study adopts the technology acceptance model as one of its research instruments

(Lee and et. al., 2012). TAM is defined as an execution of the theory of reasoned actions that was

implemented for analysing the significance of TAM Model.

(Source: The Technology Acceptance Model, 2014)

The Technology Acceptance Model was firstly introduced by Davis, as it is basically

applied for modelling of the acceptance of data system through the user. David has stated the

potential objective of TAM is to give an explanatory insight to the determinants of the

acceptance of computer through individual. The TAM model is basically incorporates over two

different aspects i.e. perceived ease of use and perceived usefulness. Therefore, the interceding

performance of these two aspects are analysed by applying TAM on the probability of the system

use. This Model is significant in the context of mobile banking as it is mainly replay upon three

aspects, i.e. perceived ease of use, perceived usefulness and the intention of an individual to use

mobile banking (Akturan and Tezcan, 2012). Perceived ease of use is recognised as the degree to

that an individual believes that applying an information system would be free of efforts. On the

other side, perceived usefulness is defined as the degree to that people believe that using an

advance technology would increase their job performance. The TAM model was incorporates to

5

Illustration 2: The Technology Acceptance Model.

predict an individual interest to adopt new and advance technology in IS and mobile banking

through tyhe public in developed and developing countries. The impact of Perceived Ease of Use

(PEOU) and its significant impact towards intention to adapt mobile banking.

As per the views expressed by Yoon Jin Ma, Hae Jin Gam and Jennifer Banning, 2017,

Perceived ease of use is recognised as the key aspect of Technology acceptance model, therefore

it is widely used in determining the level of acceptance of individual in relation to dealing with

the technology mainly in the field of information system. Technology Acceptance model is

mainly consist over the social psychology theory, where acceptance regarding technology is

analysed through the perception and reason of users which has direct influence over the

behaviour, action, intention and their internal belief. This model is mainly relay upon three

aspects i.e. perceived usefulness, perceived ease of use and behavioural intention. These three

aspects are based on each other and provide a significant support to the digital advancement and

develops the belief of individual in relation to using digital tools and technologies for the sack of

reducing their efforts (Ali and Arshad, 2016). Perceived usefulness is recognised as a term where

an individual believes that applying a particular system would improvise their working

performance. On the contrast, perceived ease of use is defined when an individual believes that

using a specific system would be free from efforts. Furthermore, the third aspect, behavioural

intention is evaluated as the potential use of given a particular IT system and therefore, analyse

the acceptance regarding technology. This model is significantly based over the acceptance of an

individual bin relation to a specific technology in their daily life. Perceived ease of use has

positive impact over influencing an individual's intention to adopt banking, therefore, from the

past few decade, banking sector is concern over transforming their operations into digital

technologies for the purpose of providing easy facilities to their potential users. As per the

opinion analysis of James Chen, 2019, mobile banking refers as the act of making financial

transaction on a mobile device which involves tablet, mobile phone, etc. In addition to this,

mobile banking is defied as the progression of electronic banking that authorises users to

complete financial transaction through applying mobile or its handheld gadgets (Alavi and

Ahuja, 2016). As per the opinion stated by Syed Ali Raza, Amna Umer and Nida Shah, 2017,

The positive impact of Perceived ease of use is significant in influencing the intention of an

individual to adapt mobile banking, therefore, this is more easy than the traditional method as it

is effectual in making banking transaction more easy and reliable and also reduces the rush in

6

through tyhe public in developed and developing countries. The impact of Perceived Ease of Use

(PEOU) and its significant impact towards intention to adapt mobile banking.

As per the views expressed by Yoon Jin Ma, Hae Jin Gam and Jennifer Banning, 2017,

Perceived ease of use is recognised as the key aspect of Technology acceptance model, therefore

it is widely used in determining the level of acceptance of individual in relation to dealing with

the technology mainly in the field of information system. Technology Acceptance model is

mainly consist over the social psychology theory, where acceptance regarding technology is

analysed through the perception and reason of users which has direct influence over the

behaviour, action, intention and their internal belief. This model is mainly relay upon three

aspects i.e. perceived usefulness, perceived ease of use and behavioural intention. These three

aspects are based on each other and provide a significant support to the digital advancement and

develops the belief of individual in relation to using digital tools and technologies for the sack of

reducing their efforts (Ali and Arshad, 2016). Perceived usefulness is recognised as a term where

an individual believes that applying a particular system would improvise their working

performance. On the contrast, perceived ease of use is defined when an individual believes that

using a specific system would be free from efforts. Furthermore, the third aspect, behavioural

intention is evaluated as the potential use of given a particular IT system and therefore, analyse

the acceptance regarding technology. This model is significantly based over the acceptance of an

individual bin relation to a specific technology in their daily life. Perceived ease of use has

positive impact over influencing an individual's intention to adopt banking, therefore, from the

past few decade, banking sector is concern over transforming their operations into digital

technologies for the purpose of providing easy facilities to their potential users. As per the

opinion analysis of James Chen, 2019, mobile banking refers as the act of making financial

transaction on a mobile device which involves tablet, mobile phone, etc. In addition to this,

mobile banking is defied as the progression of electronic banking that authorises users to

complete financial transaction through applying mobile or its handheld gadgets (Alavi and

Ahuja, 2016). As per the opinion stated by Syed Ali Raza, Amna Umer and Nida Shah, 2017,

The positive impact of Perceived ease of use is significant in influencing the intention of an

individual to adapt mobile banking, therefore, this is more easy than the traditional method as it

is effectual in making banking transaction more easy and reliable and also reduces the rush in

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

banks. Banking is recognised as the most developing sector which is mainly concern over

attaining higher growth and success within the business environment via implementing easy

mobile banking facilities. However, perceived ease of use is performing a vital role in

influencing an individual decision to use mobile banking facilities, Thus bank in UK or all over

the globe are based on mobile applications as they are operating their facilities within the support

of mobile banking, as mobile applications are efficacious in making online translation, online

trading, money transfer, insurance facilities, interest percentage, etc. Therefore, mobile banking

facilities are effort less and easy to use, thus this influences the intention of individual to adopt

mobile banking (Ayo, Mbarika and Oni, 2015). In addition to this, mobile banking provides the

customers a safe and secure way of banking and commerce from anytime and anywhere. For the

purpose of promoting mobile banking, banks are focuses over implementing easy mobile

banking applications which are effective in providing easy to use facilities to their customers.

The significant impact of Perceived Usefulness (PU) towards adaptation to mobile banking.

As per the views expressed by Ali Abdallah Alalwan, Yogesh K. Dwivedi, Nripendra P.

P. Rana, Michael D. Willian, 2016. perceived usefulness is defined as one of the significant

independent constructs in the Technology Acceptance Model. In addition to this, it refers as the

degree to which an individual believes that applying a specific system would develop their job

performance and capability of their working. The Perceived Usefulness refers to the degree of

user’s dependency or a person's dependency to the system offered, particularly on the

improvement of the performance in the specific part. Therefore, perceived usefulness, ensure the

performance development of an individual. As per the opinion stated by Mahmood Jasim

Alsamydai, 2019, In the modern scenario, the world is experiencing an important acceleration in

the emergence and development of new and advance technologies in different field, mainly is

banking industry. The technological advancement has plays a vital role in the growth and

development of the characteristics of the banking operations (Yoon and Occeña, 2014). Banking

industry is considered as the highly dynamic business which has joined in global network and

offers suitable conditions to those clients who are planned to use online banking facilities for the

purpose of fulfilling their needs and wants. According to the views expressed by F.Muñoz-

LeivaaS.Climent-ClimentbF.Liébana-Cabanillasa, 2017, The major influence of perceived

usefulness is being widely being recognised in the field of electronic banking. The usefulness is

the subjective probability which is applying the technology would develop the way an individual

7

attaining higher growth and success within the business environment via implementing easy

mobile banking facilities. However, perceived ease of use is performing a vital role in

influencing an individual decision to use mobile banking facilities, Thus bank in UK or all over

the globe are based on mobile applications as they are operating their facilities within the support

of mobile banking, as mobile applications are efficacious in making online translation, online

trading, money transfer, insurance facilities, interest percentage, etc. Therefore, mobile banking

facilities are effort less and easy to use, thus this influences the intention of individual to adopt

mobile banking (Ayo, Mbarika and Oni, 2015). In addition to this, mobile banking provides the

customers a safe and secure way of banking and commerce from anytime and anywhere. For the

purpose of promoting mobile banking, banks are focuses over implementing easy mobile

banking applications which are effective in providing easy to use facilities to their customers.

The significant impact of Perceived Usefulness (PU) towards adaptation to mobile banking.

As per the views expressed by Ali Abdallah Alalwan, Yogesh K. Dwivedi, Nripendra P.

P. Rana, Michael D. Willian, 2016. perceived usefulness is defined as one of the significant

independent constructs in the Technology Acceptance Model. In addition to this, it refers as the

degree to which an individual believes that applying a specific system would develop their job

performance and capability of their working. The Perceived Usefulness refers to the degree of

user’s dependency or a person's dependency to the system offered, particularly on the

improvement of the performance in the specific part. Therefore, perceived usefulness, ensure the

performance development of an individual. As per the opinion stated by Mahmood Jasim

Alsamydai, 2019, In the modern scenario, the world is experiencing an important acceleration in

the emergence and development of new and advance technologies in different field, mainly is

banking industry. The technological advancement has plays a vital role in the growth and

development of the characteristics of the banking operations (Yoon and Occeña, 2014). Banking

industry is considered as the highly dynamic business which has joined in global network and

offers suitable conditions to those clients who are planned to use online banking facilities for the

purpose of fulfilling their needs and wants. According to the views expressed by F.Muñoz-

LeivaaS.Climent-ClimentbF.Liébana-Cabanillasa, 2017, The major influence of perceived

usefulness is being widely being recognised in the field of electronic banking. The usefulness is

the subjective probability which is applying the technology would develop the way an individual

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

user could complete a given task. Perceived usefullness has positive impact towards the adoption

of mobile banking, therefore, in the modern scenario, the living of individual is based on digital

tools and technologies, thus people are significantly based on using digial tools and technologies

for a better and comfortable living (Ali and Arshad, 2016). In the context of banking sector,

innovation has been seen in the adoption of technologies that are effective for the ease of

customers as well as for the banking organsaitions in making easy transaction. According to

Minna Mattila (2018), there are many factors which drive the mobile banking adoption like

technology. The newly emerged technology like mobile banking services shows an innovation,

under which both intangible service as well as an innovative medium regarding with service

delivery are employed (Factors Affecting The Adoption Of Mobile Banking Services, 2018). The

concepts of innovation including the diffusion of innovation are considered as more intricate as

technology that has a large impact on different characteristics of mobile banking services.

Innovation defines a new way for using banking services, where by utilising the mobile apps,

people can use the banking services more conveniently (Goularte and Zilber, 2019). The impact

of perceived usefulness over the adoption of mobile banking can be analysed through, analysing

the attraction of people towards transforming their banking operation into mobile banking,

therefore, in today's busy schedule, individual are seeking for adopting mobile banking for the

purpose of taking ease benefits of banking facilities (Zhou, 2011). While digital channel

indicates services which facilitate the storage of payment via mobile or online process. Other

than this, aggregators are services which enable the people to utilise banking services in a single

place, by comparing price through websites. Similarly, BiaB includes the provision of core and

comprehensive banking system, through third party. These set of innovations has turned the way

of banking services and provide better mode to customers to use the same (Malaquias and

Hwang, 2019). This would also enable banks to enlarge their customer base by providing them

timely and convenient services.

The impact of Perceived Risk (PR) towards adaptation to mobile banking

As per the views expressed by Laura Lake, 2019, Perceived risk is defined as an

uncertainty an individual has at the time of buying products and services, specially those which

are particularly expensive in nature. In another words, risk perception is the subjective

judgement which an individual create in regards to the characteristics or severity of a risk.

Perceived risk refers as an uncertain, probabilistic significant future outlay (Alalwan and et. al.,

8

of mobile banking, therefore, in the modern scenario, the living of individual is based on digital

tools and technologies, thus people are significantly based on using digial tools and technologies

for a better and comfortable living (Ali and Arshad, 2016). In the context of banking sector,

innovation has been seen in the adoption of technologies that are effective for the ease of

customers as well as for the banking organsaitions in making easy transaction. According to

Minna Mattila (2018), there are many factors which drive the mobile banking adoption like

technology. The newly emerged technology like mobile banking services shows an innovation,

under which both intangible service as well as an innovative medium regarding with service

delivery are employed (Factors Affecting The Adoption Of Mobile Banking Services, 2018). The

concepts of innovation including the diffusion of innovation are considered as more intricate as

technology that has a large impact on different characteristics of mobile banking services.

Innovation defines a new way for using banking services, where by utilising the mobile apps,

people can use the banking services more conveniently (Goularte and Zilber, 2019). The impact

of perceived usefulness over the adoption of mobile banking can be analysed through, analysing

the attraction of people towards transforming their banking operation into mobile banking,

therefore, in today's busy schedule, individual are seeking for adopting mobile banking for the

purpose of taking ease benefits of banking facilities (Zhou, 2011). While digital channel

indicates services which facilitate the storage of payment via mobile or online process. Other

than this, aggregators are services which enable the people to utilise banking services in a single

place, by comparing price through websites. Similarly, BiaB includes the provision of core and

comprehensive banking system, through third party. These set of innovations has turned the way

of banking services and provide better mode to customers to use the same (Malaquias and

Hwang, 2019). This would also enable banks to enlarge their customer base by providing them

timely and convenient services.

The impact of Perceived Risk (PR) towards adaptation to mobile banking

As per the views expressed by Laura Lake, 2019, Perceived risk is defined as an

uncertainty an individual has at the time of buying products and services, specially those which

are particularly expensive in nature. In another words, risk perception is the subjective

judgement which an individual create in regards to the characteristics or severity of a risk.

Perceived risk refers as an uncertain, probabilistic significant future outlay (Alalwan and et. al.,

8

2016). In addition to this, perceived risk is the ambiguity which buyers have before making a

purchase decision in regards to a product or services. Perceived risk is an effective term of

marketing which is associated with products which are expensive like wise house or cars or

products which are complex and have many features like computer or laptops. In the context of

banking, perceived risk has wider influence over adoption of mobile banking, therefore, in the

sector of banking individual are having the risk of security and safety of their personal data and

information. According to the opinion stated by Shuhaida Mohamed Shuhidan, Saidatul Rahah

Hamidi, Intan Syazwani Saleh, 2017, banking system adopts technology to support bank services

effectively. Therefore, mobile banking is defined as an effective platform of performing financial

activities through portable devices likewise mobile phones, computer systems, tablets which are

connected to telecommunication network. According to the opinion stated by ChauShen Chen,

2013, Perceived risk has a direct influence over the operations and progression of internet

banking in Malaysia. The perceived risk has categorised among different facts i.e. performance

risk, social risk, financial risk, time risk, security risk that are provided more in detailed

understanding of characteristics of risks in regards internet banking (Martins, Oliveira and

Popovič, 2014). Performance risk is mainly defined to the losses incurred through lack or

malfunctions of mobile banking. In the modern scenario, the living of individual is very much

based on digital technologies, therefore, people are preferring internet banking facilities for the

purpose of fulfilling their banking needs instantly. Therefore, there are multiple perceived risk

are arises in the adoption of internet banking, thus, mobile phones has limited battery power and

wireless networks may break the connection as these are not applicable for wider uses, thus these

are limiting the use of mobile services.

Security and privacy is recognised as the significant loss for the reason of hackers and

fraud that compromising the security of a mobile banking user. Security is the major perceived

risk which has wider influence over using mobile banking facilities, therefore, individual's are

mainly having the issue of hacking of their mobile passwords and use them in wrong manner.

This element has caused major security and privacy errors, which affects the adoption of mobile

banking. However, Phishing is the new way of hacking an individual data, thus phishers are

considering buyers information like wide their user ID, password, debit or credit card

information through masquerading as a trust worthy entity in an electronic telecommunication

way (Mathew, Sulphey and Prabhakaran, 2014).

9

purchase decision in regards to a product or services. Perceived risk is an effective term of

marketing which is associated with products which are expensive like wise house or cars or

products which are complex and have many features like computer or laptops. In the context of

banking, perceived risk has wider influence over adoption of mobile banking, therefore, in the

sector of banking individual are having the risk of security and safety of their personal data and

information. According to the opinion stated by Shuhaida Mohamed Shuhidan, Saidatul Rahah

Hamidi, Intan Syazwani Saleh, 2017, banking system adopts technology to support bank services

effectively. Therefore, mobile banking is defined as an effective platform of performing financial

activities through portable devices likewise mobile phones, computer systems, tablets which are

connected to telecommunication network. According to the opinion stated by ChauShen Chen,

2013, Perceived risk has a direct influence over the operations and progression of internet

banking in Malaysia. The perceived risk has categorised among different facts i.e. performance

risk, social risk, financial risk, time risk, security risk that are provided more in detailed

understanding of characteristics of risks in regards internet banking (Martins, Oliveira and

Popovič, 2014). Performance risk is mainly defined to the losses incurred through lack or

malfunctions of mobile banking. In the modern scenario, the living of individual is very much

based on digital technologies, therefore, people are preferring internet banking facilities for the

purpose of fulfilling their banking needs instantly. Therefore, there are multiple perceived risk

are arises in the adoption of internet banking, thus, mobile phones has limited battery power and

wireless networks may break the connection as these are not applicable for wider uses, thus these

are limiting the use of mobile services.

Security and privacy is recognised as the significant loss for the reason of hackers and

fraud that compromising the security of a mobile banking user. Security is the major perceived

risk which has wider influence over using mobile banking facilities, therefore, individual's are

mainly having the issue of hacking of their mobile passwords and use them in wrong manner.

This element has caused major security and privacy errors, which affects the adoption of mobile

banking. However, Phishing is the new way of hacking an individual data, thus phishers are

considering buyers information like wide their user ID, password, debit or credit card

information through masquerading as a trust worthy entity in an electronic telecommunication

way (Mathew, Sulphey and Prabhakaran, 2014).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 65

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.