Modern Auditing and Assurance Service Audit Procedure Report

VerifiedAdded on 2020/05/16

|13

|2476

|40

Report

AI Summary

This report delves into the realm of modern auditing and assurance services, focusing on the audit procedures for various financial accounts. The report begins with an introduction to audit planning, emphasizing its significance in ensuring the accuracy and reliability of financial statements. It then explores analytical review techniques, particularly horizontal trend analysis, to identify potential misstatements. The concept of preliminary judgment of materiality is discussed, highlighting its role in setting acceptable limits for misstatements. The report then proceeds to examine specific accounts, including accounts receivable, inventory, cost of sales, service fees (revenue), wages, and other income. For each account, the report provides a rationale for selection, an explanation of relevant assertions, and recommended audit procedures. The analysis includes trend analysis of key financial statement items, providing insights into potential areas of concern. The report aims to provide a comprehensive overview of the audit process, offering valuable insights for finance students and professionals alike. The report highlights the importance of audit procedures in evaluating the accuracy and reliability of financial statements. The report provides a detailed analysis of the accounts and suggests effective audit procedures.

Running head: MODERN AUDITING AND ASSURANCE SERVICE

Modern Auditing and Assurance Service

Name of the Student:

Name of the University:

Author Note

Modern Auditing and Assurance Service

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MODERN AUDITING AND ASSURANCE SERVICE

Table of Contents

Introduction......................................................................................................................................3

Audit Planning............................................................................................................................3

Analytical Review.......................................................................................................................3

Preliminary judgment of materiality...........................................................................................4

Accounts Receivable.......................................................................................................................4

Rationale for Selection................................................................................................................4

Assertion and Explanation..........................................................................................................5

Recommended Audit Procedure.................................................................................................5

Inventory..........................................................................................................................................5

Rationale for Selection................................................................................................................5

Assertion and Explanation..........................................................................................................6

Recommended Audit Procedure.................................................................................................6

Cost of Sales....................................................................................................................................6

Rationale for Selection................................................................................................................6

Assertion and Explanation..........................................................................................................7

Recommended Audit Procedure.................................................................................................7

Service Fees (Revenue)...................................................................................................................7

Rationale for Selection................................................................................................................7

Assertion and Explanation..........................................................................................................7

Recommended Audit Procedure.................................................................................................8

Wages Account................................................................................................................................8

Rationale for Selection................................................................................................................8

Assertion and Explanation..........................................................................................................8

Table of Contents

Introduction......................................................................................................................................3

Audit Planning............................................................................................................................3

Analytical Review.......................................................................................................................3

Preliminary judgment of materiality...........................................................................................4

Accounts Receivable.......................................................................................................................4

Rationale for Selection................................................................................................................4

Assertion and Explanation..........................................................................................................5

Recommended Audit Procedure.................................................................................................5

Inventory..........................................................................................................................................5

Rationale for Selection................................................................................................................5

Assertion and Explanation..........................................................................................................6

Recommended Audit Procedure.................................................................................................6

Cost of Sales....................................................................................................................................6

Rationale for Selection................................................................................................................6

Assertion and Explanation..........................................................................................................7

Recommended Audit Procedure.................................................................................................7

Service Fees (Revenue)...................................................................................................................7

Rationale for Selection................................................................................................................7

Assertion and Explanation..........................................................................................................7

Recommended Audit Procedure.................................................................................................8

Wages Account................................................................................................................................8

Rationale for Selection................................................................................................................8

Assertion and Explanation..........................................................................................................8

2MODERN AUDITING AND ASSURANCE SERVICE

Recommended Audit Procedure.................................................................................................8

Other Income...................................................................................................................................9

Rationale for Selection................................................................................................................9

Assertion and Explanation..........................................................................................................9

Recommended Audit Procedure.................................................................................................9

References......................................................................................................................................10

Recommended Audit Procedure.................................................................................................8

Other Income...................................................................................................................................9

Rationale for Selection................................................................................................................9

Assertion and Explanation..........................................................................................................9

Recommended Audit Procedure.................................................................................................9

References......................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MODERN AUDITING AND ASSURANCE SERVICE

Introduction

Audit Planning

Audit planning essentially refers to the planning by an auditor in regards to the systematic

audit process that is carried out for the evaluation of the financial statements in order to ensure

that the accounting statements reflect the true and fair view of the financial condition of the

company. The audit of the accounting statements of a corporate entity is carried out in each

financial year. A quality audit plan reflects the particular regulations and policies that should be

strictly followed by an auditor for the successful execution of the auditing procedures. The major

benefit that can be facilitated by the providence of an audit plan is that, by the following of the

audit plan, an auditor can obtain enough evidence for the required examination and evaluation of

the financial and non-financial proceedings of the company. The auditing procedure or plan

effectively includes the testing of the various account balances for the identification of the

material misstatements in the books of accounts. Thus, the audit testing of accounts forms a

crucial part of audit planning van (Buuren caes et al., 2014).

Analytical Review

The analytical review of the trial balance has been asked in the question can be

effectively carried out by the horizontal trend analysis of the account balances of the financial

statements of the company. The advantages that can be accrued from the analytical review of the

trial balance is that the auditor can identify the material misstatements in the different account

balances. The misstatements may have occurred either due to the fraud carried out by the

concerned employee of the organization willingly or on the account of carelessness. The

analytical review of the chosen accounts that have been carried out in this particular report has

been effectively carried out by the horizontal trend analysis of the account balances.

Preliminary judgment of materiality

The preliminary judgment of materiality refers to the particular amount of materiality that

is effectively carried out by the auditor in order to ascertain the maximum permissible amount

that can be allowed in case the financial accounts are misstated. This particular amount of

materiality that is fixed by the auditor, is the maximum amount by which the accounts if

misstated, will not hamper the quality of the financial statements and they will continue

Introduction

Audit Planning

Audit planning essentially refers to the planning by an auditor in regards to the systematic

audit process that is carried out for the evaluation of the financial statements in order to ensure

that the accounting statements reflect the true and fair view of the financial condition of the

company. The audit of the accounting statements of a corporate entity is carried out in each

financial year. A quality audit plan reflects the particular regulations and policies that should be

strictly followed by an auditor for the successful execution of the auditing procedures. The major

benefit that can be facilitated by the providence of an audit plan is that, by the following of the

audit plan, an auditor can obtain enough evidence for the required examination and evaluation of

the financial and non-financial proceedings of the company. The auditing procedure or plan

effectively includes the testing of the various account balances for the identification of the

material misstatements in the books of accounts. Thus, the audit testing of accounts forms a

crucial part of audit planning van (Buuren caes et al., 2014).

Analytical Review

The analytical review of the trial balance has been asked in the question can be

effectively carried out by the horizontal trend analysis of the account balances of the financial

statements of the company. The advantages that can be accrued from the analytical review of the

trial balance is that the auditor can identify the material misstatements in the different account

balances. The misstatements may have occurred either due to the fraud carried out by the

concerned employee of the organization willingly or on the account of carelessness. The

analytical review of the chosen accounts that have been carried out in this particular report has

been effectively carried out by the horizontal trend analysis of the account balances.

Preliminary judgment of materiality

The preliminary judgment of materiality refers to the particular amount of materiality that

is effectively carried out by the auditor in order to ascertain the maximum permissible amount

that can be allowed in case the financial accounts are misstated. This particular amount of

materiality that is fixed by the auditor, is the maximum amount by which the accounts if

misstated, will not hamper the quality of the financial statements and they will continue

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MODERN AUDITING AND ASSURANCE SERVICE

representing the true and fair view of the liquidity position of the concerned company. It should

be noted here that the materiality misstatements in the account balances might have occurred due

to the double entry book-keeping system in accordance to which the trial balance has been

prepared (Malaescu and Sutton 2014).

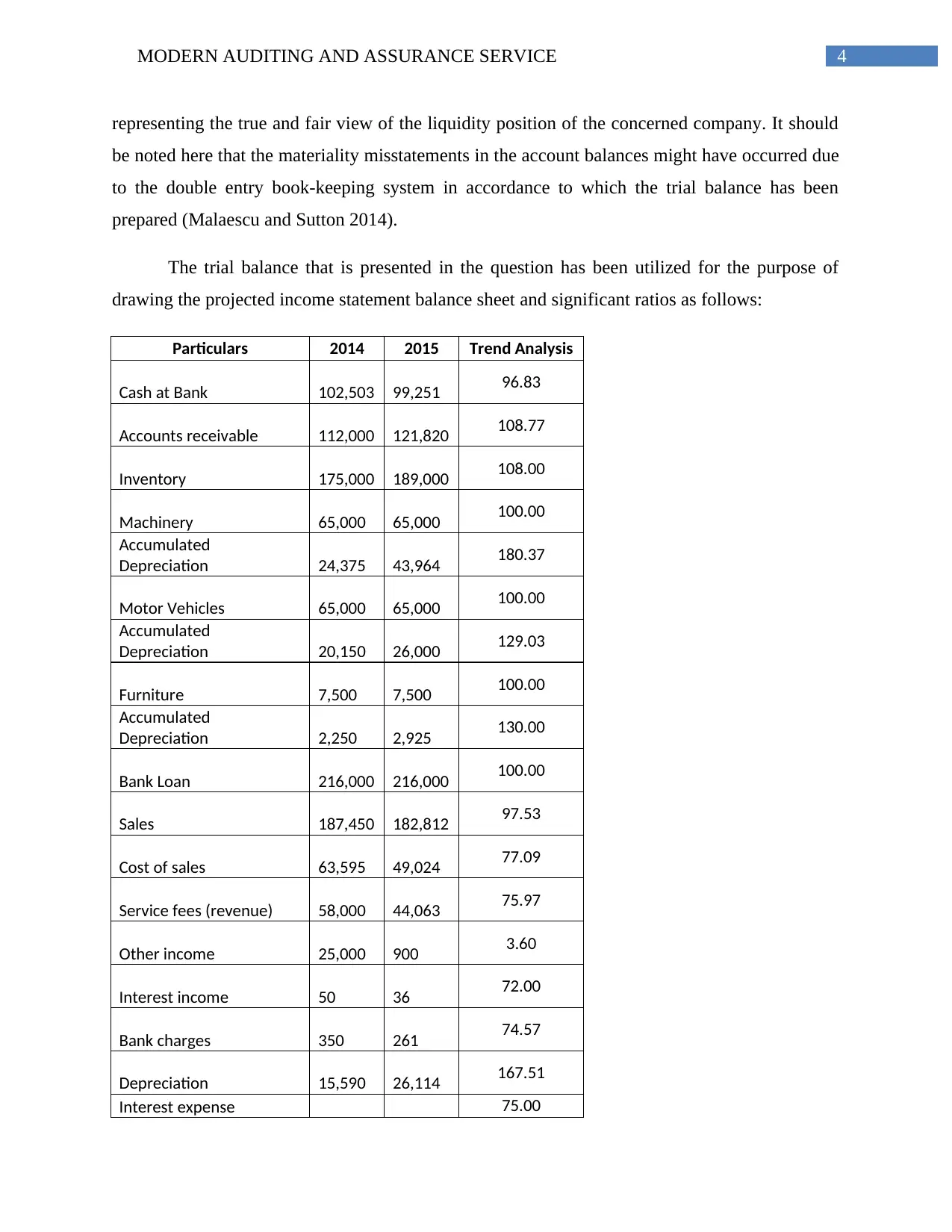

The trial balance that is presented in the question has been utilized for the purpose of

drawing the projected income statement balance sheet and significant ratios as follows:

Particulars 2014 2015 Trend Analysis

Cash at Bank 102,503 99,251 96.83

Accounts receivable 112,000 121,820 108.77

Inventory 175,000 189,000 108.00

Machinery 65,000 65,000 100.00

Accumulated

Depreciation 24,375 43,964 180.37

Motor Vehicles 65,000 65,000 100.00

Accumulated

Depreciation 20,150 26,000 129.03

Furniture 7,500 7,500 100.00

Accumulated

Depreciation 2,250 2,925 130.00

Bank Loan 216,000 216,000 100.00

Sales 187,450 182,812 97.53

Cost of sales 63,595 49,024 77.09

Service fees (revenue) 58,000 44,063 75.97

Other income 25,000 900 3.60

Interest income 50 36 72.00

Bank charges 350 261 74.57

Depreciation 15,590 26,114 167.51

Interest expense 75.00

representing the true and fair view of the liquidity position of the concerned company. It should

be noted here that the materiality misstatements in the account balances might have occurred due

to the double entry book-keeping system in accordance to which the trial balance has been

prepared (Malaescu and Sutton 2014).

The trial balance that is presented in the question has been utilized for the purpose of

drawing the projected income statement balance sheet and significant ratios as follows:

Particulars 2014 2015 Trend Analysis

Cash at Bank 102,503 99,251 96.83

Accounts receivable 112,000 121,820 108.77

Inventory 175,000 189,000 108.00

Machinery 65,000 65,000 100.00

Accumulated

Depreciation 24,375 43,964 180.37

Motor Vehicles 65,000 65,000 100.00

Accumulated

Depreciation 20,150 26,000 129.03

Furniture 7,500 7,500 100.00

Accumulated

Depreciation 2,250 2,925 130.00

Bank Loan 216,000 216,000 100.00

Sales 187,450 182,812 97.53

Cost of sales 63,595 49,024 77.09

Service fees (revenue) 58,000 44,063 75.97

Other income 25,000 900 3.60

Interest income 50 36 72.00

Bank charges 350 261 74.57

Depreciation 15,590 26,114 167.51

Interest expense 75.00

5MODERN AUDITING AND ASSURANCE SERVICE

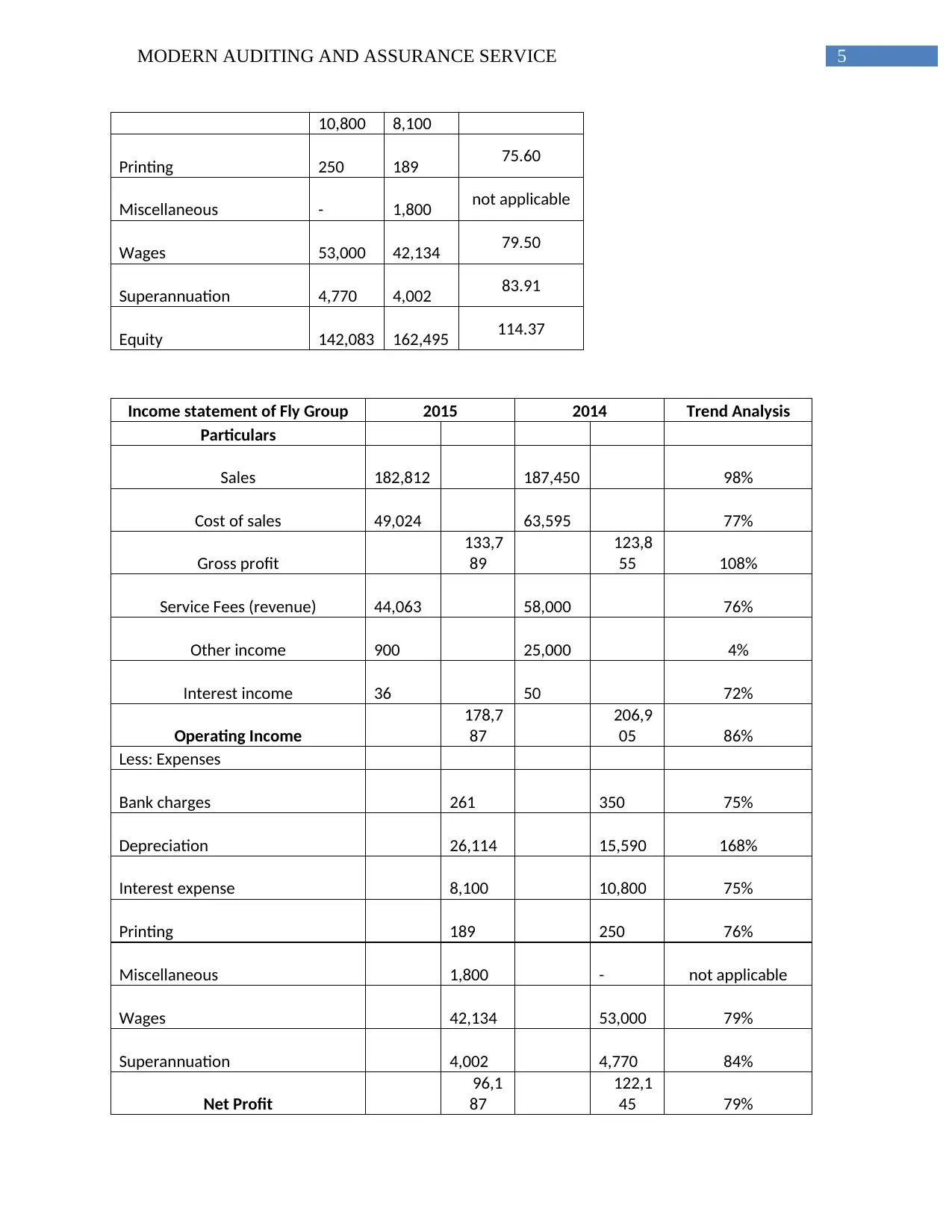

10,800 8,100

Printing 250 189 75.60

Miscellaneous - 1,800 not applicable

Wages 53,000 42,134 79.50

Superannuation 4,770 4,002 83.91

Equity 142,083 162,495 114.37

Income statement of Fly Group 2015 2014 Trend Analysis

Particulars

Sales 182,812 187,450 98%

Cost of sales 49,024 63,595 77%

Gross profit

133,7

89

123,8

55 108%

Service Fees (revenue) 44,063 58,000 76%

Other income 900 25,000 4%

Interest income 36 50 72%

Operating Income

178,7

87

206,9

05 86%

Less: Expenses

Bank charges 261 350 75%

Depreciation 26,114 15,590 168%

Interest expense 8,100 10,800 75%

Printing 189 250 76%

Miscellaneous 1,800 - not applicable

Wages 42,134 53,000 79%

Superannuation 4,002 4,770 84%

Net Profit

96,1

87

122,1

45 79%

10,800 8,100

Printing 250 189 75.60

Miscellaneous - 1,800 not applicable

Wages 53,000 42,134 79.50

Superannuation 4,770 4,002 83.91

Equity 142,083 162,495 114.37

Income statement of Fly Group 2015 2014 Trend Analysis

Particulars

Sales 182,812 187,450 98%

Cost of sales 49,024 63,595 77%

Gross profit

133,7

89

123,8

55 108%

Service Fees (revenue) 44,063 58,000 76%

Other income 900 25,000 4%

Interest income 36 50 72%

Operating Income

178,7

87

206,9

05 86%

Less: Expenses

Bank charges 261 350 75%

Depreciation 26,114 15,590 168%

Interest expense 8,100 10,800 75%

Printing 189 250 76%

Miscellaneous 1,800 - not applicable

Wages 42,134 53,000 79%

Superannuation 4,002 4,770 84%

Net Profit

96,1

87

122,1

45 79%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MODERN AUDITING AND ASSURANCE SERVICE

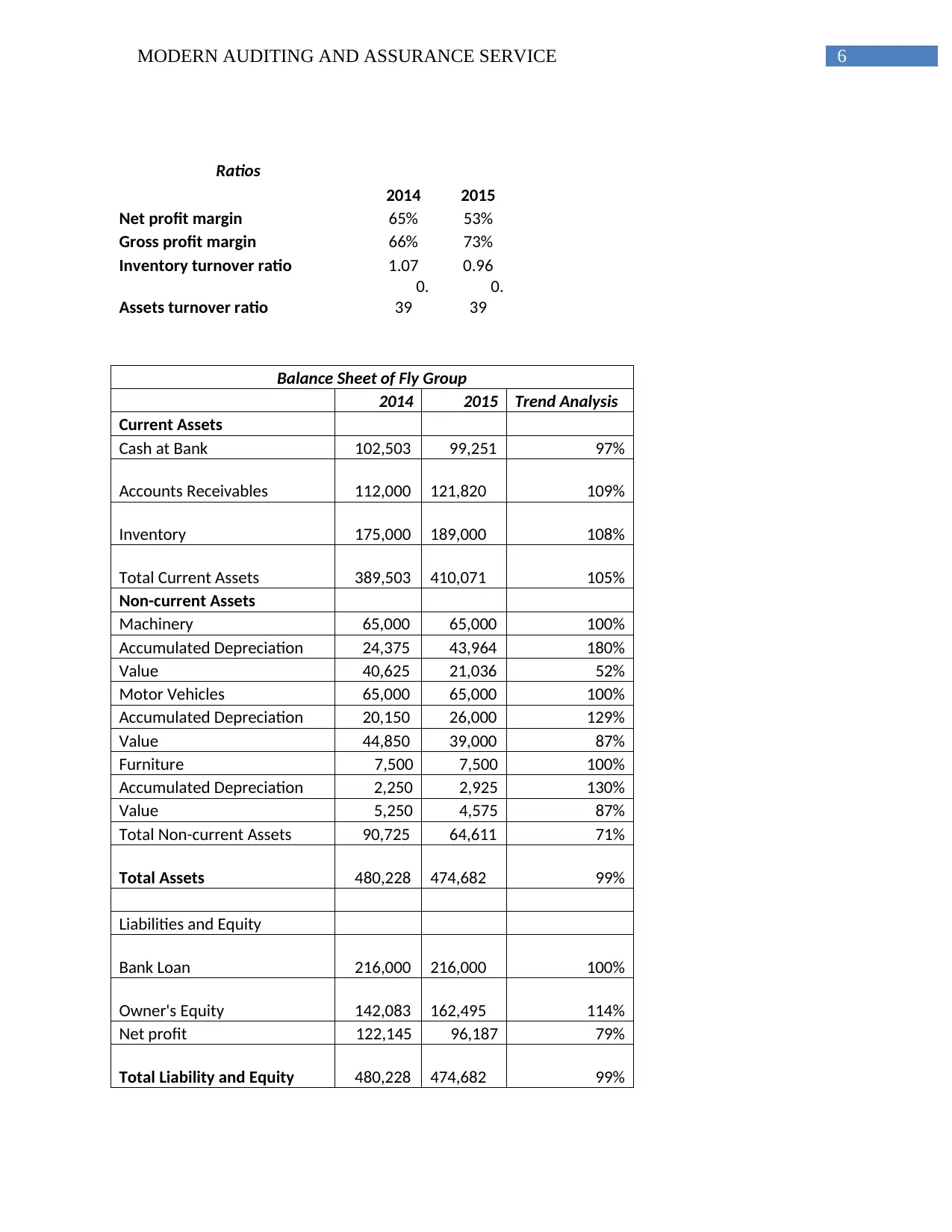

Ratios

2014 2015

Net profit margin 65% 53%

Gross profit margin 66% 73%

Inventory turnover ratio 1.07 0.96

Assets turnover ratio

0.

39

0.

39

Balance Sheet of Fly Group

2014 2015 Trend Analysis

Current Assets

Cash at Bank 102,503 99,251 97%

Accounts Receivables 112,000 121,820 109%

Inventory 175,000 189,000 108%

Total Current Assets 389,503 410,071 105%

Non-current Assets

Machinery 65,000 65,000 100%

Accumulated Depreciation 24,375 43,964 180%

Value 40,625 21,036 52%

Motor Vehicles 65,000 65,000 100%

Accumulated Depreciation 20,150 26,000 129%

Value 44,850 39,000 87%

Furniture 7,500 7,500 100%

Accumulated Depreciation 2,250 2,925 130%

Value 5,250 4,575 87%

Total Non-current Assets 90,725 64,611 71%

Total Assets 480,228 474,682 99%

Liabilities and Equity

Bank Loan 216,000 216,000 100%

Owner's Equity 142,083 162,495 114%

Net profit 122,145 96,187 79%

Total Liability and Equity 480,228 474,682 99%

Ratios

2014 2015

Net profit margin 65% 53%

Gross profit margin 66% 73%

Inventory turnover ratio 1.07 0.96

Assets turnover ratio

0.

39

0.

39

Balance Sheet of Fly Group

2014 2015 Trend Analysis

Current Assets

Cash at Bank 102,503 99,251 97%

Accounts Receivables 112,000 121,820 109%

Inventory 175,000 189,000 108%

Total Current Assets 389,503 410,071 105%

Non-current Assets

Machinery 65,000 65,000 100%

Accumulated Depreciation 24,375 43,964 180%

Value 40,625 21,036 52%

Motor Vehicles 65,000 65,000 100%

Accumulated Depreciation 20,150 26,000 129%

Value 44,850 39,000 87%

Furniture 7,500 7,500 100%

Accumulated Depreciation 2,250 2,925 130%

Value 5,250 4,575 87%

Total Non-current Assets 90,725 64,611 71%

Total Assets 480,228 474,682 99%

Liabilities and Equity

Bank Loan 216,000 216,000 100%

Owner's Equity 142,083 162,495 114%

Net profit 122,145 96,187 79%

Total Liability and Equity 480,228 474,682 99%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MODERN AUDITING AND ASSURANCE SERVICE

The accounts that have been selected have been listed down as follows:

Account Receivable

Inventory

Cost of Sales

Service Fees (revenue)

Wages

Other Income

Accounts Receivable

The accounts receivable has been selected for the purpose of audit testing in order to

identify the materiality in the accounts

Rationale for Selection

The Accounts Receivable account has been selected due to the fact that this particular

account has increased by 108.77%. This means that the auditor should look into such a rising

trend as because materiality may have occurred in the selected account. This is also a crucial

financial component because it is directly linked with the total sales revenue incurred by the

firm.

Assertion and Explanation

The accounts receivable represents that part of the total sales that has been incurred on

credit. This means that the revenue that the business has generated has not yet been received. The

chances of the accounts receivable balance being understated or overstated is high as this

particular balance does not impact the cash generated by the firm. Therefore, a particular

employee carrying out fraudulent activities may understate or overstate this account for

increasing or decreasing the profitability of the firm. The accounts receivable is treated as an

asset in the balance sheet of a particular company.

Recommended Audit Procedure

The recommended audit procedure for the auditor is that the auditor should look into each

credit sales of the organization. The credit transaction should be checked with the respective

customers and the other stakeholders of business. Moreover, the accounts receivable balance in

The accounts that have been selected have been listed down as follows:

Account Receivable

Inventory

Cost of Sales

Service Fees (revenue)

Wages

Other Income

Accounts Receivable

The accounts receivable has been selected for the purpose of audit testing in order to

identify the materiality in the accounts

Rationale for Selection

The Accounts Receivable account has been selected due to the fact that this particular

account has increased by 108.77%. This means that the auditor should look into such a rising

trend as because materiality may have occurred in the selected account. This is also a crucial

financial component because it is directly linked with the total sales revenue incurred by the

firm.

Assertion and Explanation

The accounts receivable represents that part of the total sales that has been incurred on

credit. This means that the revenue that the business has generated has not yet been received. The

chances of the accounts receivable balance being understated or overstated is high as this

particular balance does not impact the cash generated by the firm. Therefore, a particular

employee carrying out fraudulent activities may understate or overstate this account for

increasing or decreasing the profitability of the firm. The accounts receivable is treated as an

asset in the balance sheet of a particular company.

Recommended Audit Procedure

The recommended audit procedure for the auditor is that the auditor should look into each

credit sales of the organization. The credit transaction should be checked with the respective

customers and the other stakeholders of business. Moreover, the accounts receivable balance in

8MODERN AUDITING AND ASSURANCE SERVICE

the subsidiary ledger should be matched with the general ledger in terms of each credit

transaction (Earley 2015).

Inventory

The inventory has been selected for the purpose of audit testing in order to identify the

materiality in the accounts

Rationale for Selection

The inventory account has been selected because this particular account displays an

increase by 108%.

Assertion and Explanation

The inventory account that has been selected might be subjected to materiality. This is

due to the fact that often the inventory of a particular organization is maintained by different

techniques like the perpetual inventory system and the periodic inventory system. This increases

the chances of misstatement in the inventory account. It should be noted here that the inventory

account has a direct link with the liquidity position of the company. This means that the

overstatement or the understatement of the inventory account will affect the financial position of

the company.

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

identify the particular process that is adopted by the corporate entity for treating the inventory of

the organization. Moreover, the accounting records that have been maintained in regards to the

purchase and sale of the inventory should be checked in order to filter out the instances of

materiality in the books of accounts (Earley 2015).

Cost of Sales

The cost of sales account has been selected for the purpose of audit testing in order to

identify the materiality in the accounts

the subsidiary ledger should be matched with the general ledger in terms of each credit

transaction (Earley 2015).

Inventory

The inventory has been selected for the purpose of audit testing in order to identify the

materiality in the accounts

Rationale for Selection

The inventory account has been selected because this particular account displays an

increase by 108%.

Assertion and Explanation

The inventory account that has been selected might be subjected to materiality. This is

due to the fact that often the inventory of a particular organization is maintained by different

techniques like the perpetual inventory system and the periodic inventory system. This increases

the chances of misstatement in the inventory account. It should be noted here that the inventory

account has a direct link with the liquidity position of the company. This means that the

overstatement or the understatement of the inventory account will affect the financial position of

the company.

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

identify the particular process that is adopted by the corporate entity for treating the inventory of

the organization. Moreover, the accounting records that have been maintained in regards to the

purchase and sale of the inventory should be checked in order to filter out the instances of

materiality in the books of accounts (Earley 2015).

Cost of Sales

The cost of sales account has been selected for the purpose of audit testing in order to

identify the materiality in the accounts

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MODERN AUDITING AND ASSURANCE SERVICE

Rationale for Selection

The cost of sales account has been selected because this particular account has decreased

to 77.09%.

Assertion and Explanation

The cost of sales account refers to the different costs that are incurred by the firms and

constitutes of the direct costs like the direct labor cost. The cost of sales account is directly

related to the sales revenue that is, if the cost of sales has been understated or overstated the

profitability of the firm will directly increase or decrease. Therefore, the cost of sales also

signifies the fact that whether the profitability strategies that are incorporated by the firm are

working out or not.

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

check whether all the purchase or sales in regards to the cost of sales has been properly recorded

and authorized. He should also monitor the results of the different inventory tests (Earley 2015).

Service Fees (Revenue)

The service fees (revenue) account has been selected for the purpose of audit testing in

order to identify the materiality in the accounts.

Rationale for Selection

The service fees account has been selected due to the fact that the account has decreased

to 75.97%

Assertion and Explanation

The service fees account has been selected due to the fact that the account displays an

abnormal decrease in the account balance. It might be the case, that the account balance

decreases due to a genuine reason. However, it is the primary duty of the auditor to look into the

reason, as to why the service fees have decreased.

Rationale for Selection

The cost of sales account has been selected because this particular account has decreased

to 77.09%.

Assertion and Explanation

The cost of sales account refers to the different costs that are incurred by the firms and

constitutes of the direct costs like the direct labor cost. The cost of sales account is directly

related to the sales revenue that is, if the cost of sales has been understated or overstated the

profitability of the firm will directly increase or decrease. Therefore, the cost of sales also

signifies the fact that whether the profitability strategies that are incorporated by the firm are

working out or not.

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

check whether all the purchase or sales in regards to the cost of sales has been properly recorded

and authorized. He should also monitor the results of the different inventory tests (Earley 2015).

Service Fees (Revenue)

The service fees (revenue) account has been selected for the purpose of audit testing in

order to identify the materiality in the accounts.

Rationale for Selection

The service fees account has been selected due to the fact that the account has decreased

to 75.97%

Assertion and Explanation

The service fees account has been selected due to the fact that the account displays an

abnormal decrease in the account balance. It might be the case, that the account balance

decreases due to a genuine reason. However, it is the primary duty of the auditor to look into the

reason, as to why the service fees have decreased.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MODERN AUDITING AND ASSURANCE SERVICE

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

look into the factors that led to the decrease in the service fees and determine whether there has

been any genuine reason for such materiality (Graham 2015).

Wages Account

The wages account has been selected for the purpose of audit testing in order to identify

the materiality in the accounts

Rationale for Selection

The wages has been selected because this particular account has increased by 125.7%.

Assertion and Explanation

The wages account shows an unprecedented rise in the current year. This might be due to

the fact that there has been a huge recruitment drive for workers in the organization. However, it

is the primary duty of the auditor to look into the fact as to why the wages account has increased.

The wages account if subjected to materiality will directly be reflected in the profitability of the

organization.

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

check the total number of workers recruited or the workers who have been promoted and the

particular wages offered to them. This will help the auditor to ascertain the fact whether there has

been any materiality issue in the account (Graham 2015).

Other Income

The other income account has been selected for the purpose of audit testing in order to

identify the materiality in the accounts

Rationale for Selection

The other income account has been selected because this particular account decreases to

3.60%.

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

look into the factors that led to the decrease in the service fees and determine whether there has

been any genuine reason for such materiality (Graham 2015).

Wages Account

The wages account has been selected for the purpose of audit testing in order to identify

the materiality in the accounts

Rationale for Selection

The wages has been selected because this particular account has increased by 125.7%.

Assertion and Explanation

The wages account shows an unprecedented rise in the current year. This might be due to

the fact that there has been a huge recruitment drive for workers in the organization. However, it

is the primary duty of the auditor to look into the fact as to why the wages account has increased.

The wages account if subjected to materiality will directly be reflected in the profitability of the

organization.

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

check the total number of workers recruited or the workers who have been promoted and the

particular wages offered to them. This will help the auditor to ascertain the fact whether there has

been any materiality issue in the account (Graham 2015).

Other Income

The other income account has been selected for the purpose of audit testing in order to

identify the materiality in the accounts

Rationale for Selection

The other income account has been selected because this particular account decreases to

3.60%.

11MODERN AUDITING AND ASSURANCE SERVICE

Assertion and Explanation

The other income has been selected because this particular account displays an abnormal

decrease in the account balance. The auditor should review this highly abnormal phenomenon.

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

monitor and check all the components of the other income account and trace back the

transactions to their point of generation (Graham 2015).

Assertion and Explanation

The other income has been selected because this particular account displays an abnormal

decrease in the account balance. The auditor should review this highly abnormal phenomenon.

Recommended Audit Procedure

The recommended audit procedure that should be applied by the auditor is that he should

monitor and check all the components of the other income account and trace back the

transactions to their point of generation (Graham 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.