Evaluating Management Accounting Innovations and Practices

VerifiedAdded on 2020/06/04

|16

|4725

|1002

Essay

AI Summary

This essay provides a detailed examination of contemporary management accounting innovations. Key areas covered include the evolution from traditional costing methods to advanced approaches like Activity-Based Costing (ABC) and Absorption Costing. The essay evaluates budgeting techniques, contrasting Zero-Based Budgeting with Activity-Based Budgeting, and discusses their impacts on financial resource allocation. Additionally, it analyzes performance evaluation systems with an emphasis on the Balanced Scorecard, assessing its effectiveness in strategic management. Through comparisons of modern practices against traditional methods, the essay highlights benefits such as enhanced accuracy and strategic alignment while acknowledging challenges like implementation complexity. Real-world applications are explored to demonstrate these concepts' practical relevance.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

P1 Management accounting and essential requirements of management accounting...........3

P2 Discussing three management accounting reporting method that can be used by Tata

motors.....................................................................................................................................6

TASK 2......................................................................................................................................7

P3 Producing income statement as per marginal and absorption costing system..................7

TASK 3......................................................................................................................................7

P4 Discussing tools which are used by Tata Motors for budgetary and financial control.....7

P5 Comparing two business units in relation to the manner in which they have used

management accounting systems for responding financial problems..................................11

CONCLUSION........................................................................................................................12

REFERENCES.........................................................................................................................13

INTRODUCTION......................................................................................................................3

P1 Management accounting and essential requirements of management accounting...........3

P2 Discussing three management accounting reporting method that can be used by Tata

motors.....................................................................................................................................6

TASK 2......................................................................................................................................7

P3 Producing income statement as per marginal and absorption costing system..................7

TASK 3......................................................................................................................................7

P4 Discussing tools which are used by Tata Motors for budgetary and financial control.....7

P5 Comparing two business units in relation to the manner in which they have used

management accounting systems for responding financial problems..................................11

CONCLUSION........................................................................................................................12

REFERENCES.........................................................................................................................13

INTRODUCTION

Management accounting plays crucial role in the business to resolve complex

problems by taking effective decisions. Present report deals with importance of management

accounting to Tata Motors which is engaged in automotive industry and satisfying customers.

Various systems and reports of management accounting are discussed in the report.

Furthermore, marginal and absorption costing techniques are also assessed. Moreover,

functions of management accounting and requirements in the organisation are also listed.

Various planning tools are provided with advantages and disadvantages and also how

management accounting can be used to respond to financial problems are discussed in this

report. Thus, management accounting has immense importance in the corporate world to

assess performance, improvise over the same, and take enhanced decisions.

P1 Management accounting and essential requirements of management accounting

Management accounting is quite useful as it provides valuable advice to management

in taking effective decisions for the betterment of the company. This type of accounting

draws results from the financial accounting and provides clarity to management to make

enhanced decisions. Tata Motors, which is an automobile giant,also takes into account this

information so that it may be able to make improvement in the operational tasks with much

ease. This means that management accounting information assists managerial personnel’s in

taking enhanced decisions (Cooper, Ezzamel and Qu, 2017). Internal operations can be

improved with the help of this information and as such, company is able to perform well and

as such, management accounting information is quite useful for Tata Motors to improve its

performance in effectual way.

Moreover, costs are controlled in Tata Motors so that revenue may be maximised by

reducing the expenses and as such, cost accounting is major type of management accounting.

If expenditures exceed revenue, firm incurs losses and to overcome the same, cost related

reports are prepared which help company to cut down expenses in the best possible manner.

Thus, internal operations can be controlled and strengthened in effectual way. In relation to

this, functions of management accounting can be enumerated as follows-

1. Planning-

Management accounting plays crucial role in the business to resolve complex

problems by taking effective decisions. Present report deals with importance of management

accounting to Tata Motors which is engaged in automotive industry and satisfying customers.

Various systems and reports of management accounting are discussed in the report.

Furthermore, marginal and absorption costing techniques are also assessed. Moreover,

functions of management accounting and requirements in the organisation are also listed.

Various planning tools are provided with advantages and disadvantages and also how

management accounting can be used to respond to financial problems are discussed in this

report. Thus, management accounting has immense importance in the corporate world to

assess performance, improvise over the same, and take enhanced decisions.

P1 Management accounting and essential requirements of management accounting

Management accounting is quite useful as it provides valuable advice to management

in taking effective decisions for the betterment of the company. This type of accounting

draws results from the financial accounting and provides clarity to management to make

enhanced decisions. Tata Motors, which is an automobile giant,also takes into account this

information so that it may be able to make improvement in the operational tasks with much

ease. This means that management accounting information assists managerial personnel’s in

taking enhanced decisions (Cooper, Ezzamel and Qu, 2017). Internal operations can be

improved with the help of this information and as such, company is able to perform well and

as such, management accounting information is quite useful for Tata Motors to improve its

performance in effectual way.

Moreover, costs are controlled in Tata Motors so that revenue may be maximised by

reducing the expenses and as such, cost accounting is major type of management accounting.

If expenditures exceed revenue, firm incurs losses and to overcome the same, cost related

reports are prepared which help company to cut down expenses in the best possible manner.

Thus, internal operations can be controlled and strengthened in effectual way. In relation to

this, functions of management accounting can be enumerated as follows-

1. Planning-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Planning is essential for the business and as such, budget is prepared. Management

accounting help to take decision and budget can be prepared as whole process of budgeting is

based on the accounting reports. For instance, if Tata Motors assess target profit for coming

period and should also assess what are the plans for successful achieving objectives.

2. Organising –

This is another useful function to organise framework within which employees will

carry out tasks in a better way. This means that allocation of responsibilities and duties are

imparted to each and every employees si that objectives can be easily met by the company.

Thus, divisions of the organisation carry out their functions quite easily as they all become

interlinked with one another (Sharma. 2018).

3. Controlling-

This is another major function of management accounting as control and performance

reports are provided to the management. The reports are then matched with budgeted results

so that actual output may be assessed. If deviations are found, then corrective actions are

taken to remove the same and improvement is done. Thus, variances are eradicated and

improvement can be made for achieving desired goals.

4. Decision-making –

Decision-making is the essence of management accounting as by using this

information, top managerial personnel’s are able to take enhanced decision for the betterment

of the company. Without performing above three functions, manager cannot plan and chose

for the best alternatives, which would help company to prosper with much ease.

Difference between management accounting and financial accounting is described below-

Management accounting Financial accounting

1. Information is provided to managerial personnel’s

for taking effective decisions (Jermias, 2017).

1. Information is imparted to users who have stake in

the business.

2. Management accounting has its focus on making

company internally strong and achieve goals.

2. While, financial statements are provided to

stakeholders to analyse and take decisions.

3. Management accounting is not mandatory to be

accomplished by the firm.

3. Financial 4accounting is mandatory so that financial

statements may be provided to users of accounting

information.

4. Detailed information regarding costs and expenses 4. Overview of various aspects are listed in the

accounting help to take decision and budget can be prepared as whole process of budgeting is

based on the accounting reports. For instance, if Tata Motors assess target profit for coming

period and should also assess what are the plans for successful achieving objectives.

2. Organising –

This is another useful function to organise framework within which employees will

carry out tasks in a better way. This means that allocation of responsibilities and duties are

imparted to each and every employees si that objectives can be easily met by the company.

Thus, divisions of the organisation carry out their functions quite easily as they all become

interlinked with one another (Sharma. 2018).

3. Controlling-

This is another major function of management accounting as control and performance

reports are provided to the management. The reports are then matched with budgeted results

so that actual output may be assessed. If deviations are found, then corrective actions are

taken to remove the same and improvement is done. Thus, variances are eradicated and

improvement can be made for achieving desired goals.

4. Decision-making –

Decision-making is the essence of management accounting as by using this

information, top managerial personnel’s are able to take enhanced decision for the betterment

of the company. Without performing above three functions, manager cannot plan and chose

for the best alternatives, which would help company to prosper with much ease.

Difference between management accounting and financial accounting is described below-

Management accounting Financial accounting

1. Information is provided to managerial personnel’s

for taking effective decisions (Jermias, 2017).

1. Information is imparted to users who have stake in

the business.

2. Management accounting has its focus on making

company internally strong and achieve goals.

2. While, financial statements are provided to

stakeholders to analyse and take decisions.

3. Management accounting is not mandatory to be

accomplished by the firm.

3. Financial 4accounting is mandatory so that financial

statements may be provided to users of accounting

information.

4. Detailed information regarding costs and expenses 4. Overview of various aspects are listed in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are imparted by this type of accounting which aids in

decision-making.

financials of the company and no detail information is

present.

Essentials types of management accounting systems are as follows-

1. Cost accounting-

It is one of the main type of management accounting as it aims to control costs in the

best possible manner (Nitzl, 2018). Cost accounting help to initiate control over expenses and

as such, Tata Motors can easily cut down its expenditures in order to have maximum level of

production. There are various types of costs such as direct, indirect, fixed, variable and semi-

variable, which are to be effectively controlled so that expenses may not exceed revenue.

Cost accounting help to inject profits by reducing expenses in effective manner.

2. Inventory management system-

Tata Motors is a manufacturing company and as such, production department needs

adequate level of stock to be maintained. This is required so that orders received from the

customers may be fulfilled in timely manner. Thus, inventory is managed by the organisation

so that desired production may be achieved and no wastage may occur (Cooper, Ezzamel and

Qu, 2017). If inventory is ordered in more than required quantum, it unnecessary increases

cost of handling in the warehouse. Thus, inventory should be managed in adequate level to

accomplish production.

3. Price optimisation-

Price optimisation technique is a mathematical model, which is used to assess

customer demand in relation to change in the price of particular product. This means that

price is quoted in relevance to market and competition (Ax and Greve, 2017). If price is

charged low, Tata Motors would be unable to recover its costs and low profits will be made

and on the other hand, if price is high, customers will switch to rivals. Thus, price

optimisation system provides clarity to business that how much price should be quoted to

attract customers in effective way. Thus, it is quite useful system of management accounting.

decision-making.

financials of the company and no detail information is

present.

Essentials types of management accounting systems are as follows-

1. Cost accounting-

It is one of the main type of management accounting as it aims to control costs in the

best possible manner (Nitzl, 2018). Cost accounting help to initiate control over expenses and

as such, Tata Motors can easily cut down its expenditures in order to have maximum level of

production. There are various types of costs such as direct, indirect, fixed, variable and semi-

variable, which are to be effectively controlled so that expenses may not exceed revenue.

Cost accounting help to inject profits by reducing expenses in effective manner.

2. Inventory management system-

Tata Motors is a manufacturing company and as such, production department needs

adequate level of stock to be maintained. This is required so that orders received from the

customers may be fulfilled in timely manner. Thus, inventory is managed by the organisation

so that desired production may be achieved and no wastage may occur (Cooper, Ezzamel and

Qu, 2017). If inventory is ordered in more than required quantum, it unnecessary increases

cost of handling in the warehouse. Thus, inventory should be managed in adequate level to

accomplish production.

3. Price optimisation-

Price optimisation technique is a mathematical model, which is used to assess

customer demand in relation to change in the price of particular product. This means that

price is quoted in relevance to market and competition (Ax and Greve, 2017). If price is

charged low, Tata Motors would be unable to recover its costs and low profits will be made

and on the other hand, if price is high, customers will switch to rivals. Thus, price

optimisation system provides clarity to business that how much price should be quoted to

attract customers in effective way. Thus, it is quite useful system of management accounting.

P2 Discussing three management accounting reporting method that can be used by Tata

motors

Management reporting may be served as a control system which in turn furnishes

adequate information at various level of management. In the case of managerial reporting

system, concerned managers present and gives report at regular intervals. Tata Motors

undertake such formal system that provides management team with suitable information for

decision making. Prominent reporting system includes several characteristics such as

promptness, accuracy, comparability and consistency (Jermias, 2017). In accordance with

such aspect, managerial reports should be designed in such a manner which in turn helps in

comparing current performance with the past. Along with this, future business decisions are

highly based on managerial reports. Thus, manager of Tata Motors should ensure that all the

information contains in managerial reports must be accurate.

Effective management reporting offers high level of benefit to Tata Motors by giving

input for decision making purpose. Further, it also helps in enhancing the effectiveness of

management and aid in organizational growth. Managerial reports give clear indication to the

manager about actions that need to be undertaken for quality and cost control or management.

Along with this, reporting system also enhances the level of responsiveness towards the issue

arises.

There are several types of reports which can be used by Tata Motors for improving

operational aspects and performance such as:

Cost reports: It presents the cost of material, labour and overhead that is highly

associated with the item produced. This report enables firm to do comparison of cost

of goods sold with selling price. Management of Tata Motors can set suitable prices

by undertaking such report (Nitzl, 2018). Hence, cost report helps manager in

planning and controlling profit margin to a great extent.

Budget reports: Such managerial report includes income and expenses pertaining to

the future time period. With the help of such report management team of Tata Motors

can assess whether they should stay with budgeted amounts for the attainment of

goals or not. The rationale behind this, managers always look for the vendor or

supplier which offers raw material at fewer prices (Ax and Greve, 2017). Hence,

through evaluating such report, manager of such automobile company can find out

suitable ways for increasing revenue and decreasing expenses.

motors

Management reporting may be served as a control system which in turn furnishes

adequate information at various level of management. In the case of managerial reporting

system, concerned managers present and gives report at regular intervals. Tata Motors

undertake such formal system that provides management team with suitable information for

decision making. Prominent reporting system includes several characteristics such as

promptness, accuracy, comparability and consistency (Jermias, 2017). In accordance with

such aspect, managerial reports should be designed in such a manner which in turn helps in

comparing current performance with the past. Along with this, future business decisions are

highly based on managerial reports. Thus, manager of Tata Motors should ensure that all the

information contains in managerial reports must be accurate.

Effective management reporting offers high level of benefit to Tata Motors by giving

input for decision making purpose. Further, it also helps in enhancing the effectiveness of

management and aid in organizational growth. Managerial reports give clear indication to the

manager about actions that need to be undertaken for quality and cost control or management.

Along with this, reporting system also enhances the level of responsiveness towards the issue

arises.

There are several types of reports which can be used by Tata Motors for improving

operational aspects and performance such as:

Cost reports: It presents the cost of material, labour and overhead that is highly

associated with the item produced. This report enables firm to do comparison of cost

of goods sold with selling price. Management of Tata Motors can set suitable prices

by undertaking such report (Nitzl, 2018). Hence, cost report helps manager in

planning and controlling profit margin to a great extent.

Budget reports: Such managerial report includes income and expenses pertaining to

the future time period. With the help of such report management team of Tata Motors

can assess whether they should stay with budgeted amounts for the attainment of

goals or not. The rationale behind this, managers always look for the vendor or

supplier which offers raw material at fewer prices (Ax and Greve, 2017). Hence,

through evaluating such report, manager of such automobile company can find out

suitable ways for increasing revenue and decreasing expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance reports: This report contains information regarding budgeted and actual

monetary performance. Company prepares such report with the motive to evaluate

and assess departmental performance. By using this report, manager of Tata Motors

can do comparison of actual revenue and expenses with budgeted figures (Nuhu,

Baird and Bala Appuhamilage, 2017). This in turn helps them in assessing deviations

and reasons take place behind the same. Hence, referring the results of performance

report manager of the firm can make proper budgeting plan or framework for the

upcoming time period.

TASK 2

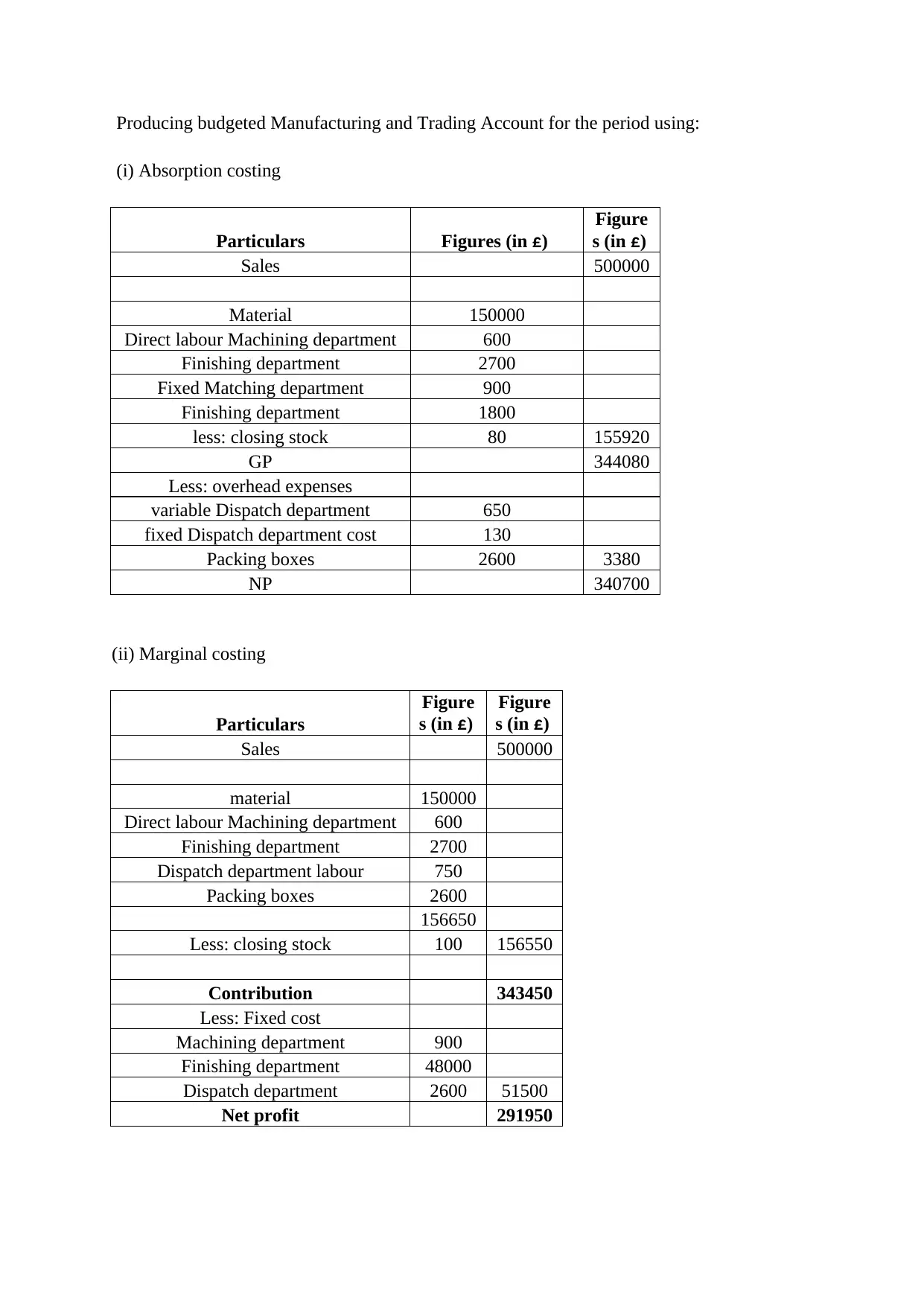

P3 Producing income statement as per marginal and absorption costing system

Marginal costing implies for the accounting system where variable costs are charged

in against to the unit cost. This management accounting system focuses on writing off fixed

cost in against to the aggregate contribution. It may be served as a principle costing technique

which is used by the majority of organizations for decision making purpose (MITCHELL and

NØRREKLIT, 2017). On the other side, absorption is known as full costing method under

which apportionment of total costs to the center is done with the motive to assess production

cost.

In marginal costing method, variable cost is considered as product, whereas fixed

expenses come under the category of periodical. On the other side, in the case of absorption

costing method, both fixed and variable expenses are directly attributable to the product.

Marginal costing method classifies overhead expenses in terms of fixed and variable. In

contrast to this, AC method presents overhead expenses as production, administration, selling

& distribution (Zimmerman and Yahya-Zadeh, 2011). MC presents and measures

profitability in terms of PV ratio. Further, in this, variances which take place in the opening

and closing inventory does not have high level of influence on cost per unit of output. Apart

from this, in AC, inclusion of fixed cost in manufacturing closely influences profitability

aspect (Difference between Marginal Costing and Absorption Costing, 2018).

Calculating number of units completed and packed in the period

On the basis of cited case situation, out of 3000 units, 2600 completed and packed in

the concerned period.

monetary performance. Company prepares such report with the motive to evaluate

and assess departmental performance. By using this report, manager of Tata Motors

can do comparison of actual revenue and expenses with budgeted figures (Nuhu,

Baird and Bala Appuhamilage, 2017). This in turn helps them in assessing deviations

and reasons take place behind the same. Hence, referring the results of performance

report manager of the firm can make proper budgeting plan or framework for the

upcoming time period.

TASK 2

P3 Producing income statement as per marginal and absorption costing system

Marginal costing implies for the accounting system where variable costs are charged

in against to the unit cost. This management accounting system focuses on writing off fixed

cost in against to the aggregate contribution. It may be served as a principle costing technique

which is used by the majority of organizations for decision making purpose (MITCHELL and

NØRREKLIT, 2017). On the other side, absorption is known as full costing method under

which apportionment of total costs to the center is done with the motive to assess production

cost.

In marginal costing method, variable cost is considered as product, whereas fixed

expenses come under the category of periodical. On the other side, in the case of absorption

costing method, both fixed and variable expenses are directly attributable to the product.

Marginal costing method classifies overhead expenses in terms of fixed and variable. In

contrast to this, AC method presents overhead expenses as production, administration, selling

& distribution (Zimmerman and Yahya-Zadeh, 2011). MC presents and measures

profitability in terms of PV ratio. Further, in this, variances which take place in the opening

and closing inventory does not have high level of influence on cost per unit of output. Apart

from this, in AC, inclusion of fixed cost in manufacturing closely influences profitability

aspect (Difference between Marginal Costing and Absorption Costing, 2018).

Calculating number of units completed and packed in the period

On the basis of cited case situation, out of 3000 units, 2600 completed and packed in

the concerned period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Producing budgeted Manufacturing and Trading Account for the period using:

(i) Absorption costing

Particulars Figures (in £)

Figure

s (in £)

Sales 500000

Material 150000

Direct labour Machining department 600

Finishing department 2700

Fixed Matching department 900

Finishing department 1800

less: closing stock 80 155920

GP 344080

Less: overhead expenses

variable Dispatch department 650

fixed Dispatch department cost 130

Packing boxes 2600 3380

NP 340700

(ii) Marginal costing

Particulars

Figure

s (in £)

Figure

s (in £)

Sales 500000

material 150000

Direct labour Machining department 600

Finishing department 2700

Dispatch department labour 750

Packing boxes 2600

156650

Less: closing stock 100 156550

Contribution 343450

Less: Fixed cost

Machining department 900

Finishing department 48000

Dispatch department 2600 51500

Net profit 291950

(i) Absorption costing

Particulars Figures (in £)

Figure

s (in £)

Sales 500000

Material 150000

Direct labour Machining department 600

Finishing department 2700

Fixed Matching department 900

Finishing department 1800

less: closing stock 80 155920

GP 344080

Less: overhead expenses

variable Dispatch department 650

fixed Dispatch department cost 130

Packing boxes 2600 3380

NP 340700

(ii) Marginal costing

Particulars

Figure

s (in £)

Figure

s (in £)

Sales 500000

material 150000

Direct labour Machining department 600

Finishing department 2700

Dispatch department labour 750

Packing boxes 2600

156650

Less: closing stock 100 156550

Contribution 343450

Less: Fixed cost

Machining department 900

Finishing department 48000

Dispatch department 2600 51500

Net profit 291950

Suggest whether company should go ahead with this product

Considering outcome of absorption and marginal costing technique it can be

presented that Tata Motors should manufacture. This in turn offers positive as well as high

net profit to the firm and thereby contributes in the organizational growth.

TASK 3

P4 Discussing tools which are used by Tata Motors for budgetary and financial control

Effective planning is the key for organizational growth and success so business unit

requires making proper estimation or forecasting about internal & external aspects.

Attainment of high profit margin by making optimum use of financial resources is the main

objective of Tata Motors. Planning tools provide high level of assistance to the management

team in making forecast about the future aspects (Macintosh and Quattrone, 2010). It may be

served as an attempt that is made by the business unit for coping up with the situation of

uncertainties. For competent planning, appropriate forecast about the future aspect is highly

required. Forecasting usually starts with certain assumptions, management knowledge,

experience and judgment. Hence, there are several budgeting tools that can be used by Tata

Motors for planning purpose such as:

Budgeting: Budget includes expenditure that firm will incur for attaining the desired

level of profit margin. In the context of business unit, budgeting is highly significant which in

turn persuade personnel working at different level about the manner expenses need to be

incurred.

Zero base budgeting: In accordance with zero base budgeting tool manager of Tata

Motors should not consider past framework. In other words, as per ZBB manager needs to

start budget with zero base and make focus on assessing alternative ways of performing

activities. In this, every item of cash flow statement is re-evaluated by the manager for the

development of competent financial framework. Along with this, it also lays emphasis on

justifying expenses that needs to be incurred by the department. This budgeting method

assumes that no balances need to be carried forward in the upcoming time period. Moreover,

changes take place in market trend etc has significant impact on business activities and

financial aspects.

Advantages:

Considering outcome of absorption and marginal costing technique it can be

presented that Tata Motors should manufacture. This in turn offers positive as well as high

net profit to the firm and thereby contributes in the organizational growth.

TASK 3

P4 Discussing tools which are used by Tata Motors for budgetary and financial control

Effective planning is the key for organizational growth and success so business unit

requires making proper estimation or forecasting about internal & external aspects.

Attainment of high profit margin by making optimum use of financial resources is the main

objective of Tata Motors. Planning tools provide high level of assistance to the management

team in making forecast about the future aspects (Macintosh and Quattrone, 2010). It may be

served as an attempt that is made by the business unit for coping up with the situation of

uncertainties. For competent planning, appropriate forecast about the future aspect is highly

required. Forecasting usually starts with certain assumptions, management knowledge,

experience and judgment. Hence, there are several budgeting tools that can be used by Tata

Motors for planning purpose such as:

Budgeting: Budget includes expenditure that firm will incur for attaining the desired

level of profit margin. In the context of business unit, budgeting is highly significant which in

turn persuade personnel working at different level about the manner expenses need to be

incurred.

Zero base budgeting: In accordance with zero base budgeting tool manager of Tata

Motors should not consider past framework. In other words, as per ZBB manager needs to

start budget with zero base and make focus on assessing alternative ways of performing

activities. In this, every item of cash flow statement is re-evaluated by the manager for the

development of competent financial framework. Along with this, it also lays emphasis on

justifying expenses that needs to be incurred by the department. This budgeting method

assumes that no balances need to be carried forward in the upcoming time period. Moreover,

changes take place in market trend etc has significant impact on business activities and

financial aspects.

Advantages:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ZBB facilitates efficient allocation of financial resources as it does not consider past

values. Thus, using ZBB tool Tata Motors can develop highly financial plan.

Using ZBB technique redundant activities can be reduced to a great extent. Moreover,

it helps in identifying opportunities and cost effectual ways of performing activities.

In this way, ZBB assists in removing all unproductive activities and thereby helps in

making effectual use of monetary resources.

It provides business unit or concerned departments with highly accurate plan.

Moreover, for computing operational cost every department relooks each and every

item of cash flow (Zero Based Budgeting v/s Activity-Based Budgeting, 2018). Hence,

ZBB presents clear view of cost in against to the desired goals.

Disadvantages:

Preparation of budget as per ZBB is considered as highly time consuming process.

Moreover, in this, no past details pertaining to the financial aspects are considered by

the firm.

ZBB demands for high manpower requirement because in this entire budget starts

from scratch. Hence, involvement of large number of personnel in budget preparation

closely impacts other business activities and performance.

Further, to prepare budget as per ZBB, company requires highly talented personnel.

Justification of every line of item is highly difficult so business unit has to organize

training for the managers.

Activity based budgeting technique: This modern budgeting technique focuses on budget

preparation by taking into account overhead cost. Such management accounting tool does not

consider previous year’s budget for arriving at new one. In this, activities that incur cost are

deeply analyzed and evaluated. Hence, on the basis of outcome or results resources are

allocated to each activity. Tata Motors can bring efficiency in the activities by taking into

account ABB. Moreover, in this, by justifying cost drivers budgets are drafted by the

managers.

Advantages:

ABB enables manager to eliminate all unnecessary activities and maintain appropriate

cost level. In this way, by reducing the level of expense and providing customers with

values. Thus, using ZBB tool Tata Motors can develop highly financial plan.

Using ZBB technique redundant activities can be reduced to a great extent. Moreover,

it helps in identifying opportunities and cost effectual ways of performing activities.

In this way, ZBB assists in removing all unproductive activities and thereby helps in

making effectual use of monetary resources.

It provides business unit or concerned departments with highly accurate plan.

Moreover, for computing operational cost every department relooks each and every

item of cash flow (Zero Based Budgeting v/s Activity-Based Budgeting, 2018). Hence,

ZBB presents clear view of cost in against to the desired goals.

Disadvantages:

Preparation of budget as per ZBB is considered as highly time consuming process.

Moreover, in this, no past details pertaining to the financial aspects are considered by

the firm.

ZBB demands for high manpower requirement because in this entire budget starts

from scratch. Hence, involvement of large number of personnel in budget preparation

closely impacts other business activities and performance.

Further, to prepare budget as per ZBB, company requires highly talented personnel.

Justification of every line of item is highly difficult so business unit has to organize

training for the managers.

Activity based budgeting technique: This modern budgeting technique focuses on budget

preparation by taking into account overhead cost. Such management accounting tool does not

consider previous year’s budget for arriving at new one. In this, activities that incur cost are

deeply analyzed and evaluated. Hence, on the basis of outcome or results resources are

allocated to each activity. Tata Motors can bring efficiency in the activities by taking into

account ABB. Moreover, in this, by justifying cost drivers budgets are drafted by the

managers.

Advantages:

ABB enables manager to eliminate all unnecessary activities and maintain appropriate

cost level. In this way, by reducing the level of expense and providing customers with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

products or services at suitable price Tata Motors can gain competitive edge over

others.

Activity based budgeting technique eliminates bottlenecks and thereby ensures

smooth functioning of the operations (Advantages, Disadvantages and Limitations of

Activity Based Costing (ABC) System, 2018).

In ABB, emphasis is placed on evaluating each and every cost driver. Thus, by

avoiding all the irrelevant activities manager of Tata Motors can develop highly

effectual plan.

Disadvantage:

Budget preparation according to ABB is highly complex and time consuming in

nature. Moreover, financial planning on the basis of ABB includes research and

analysis of various factors.

In addition to this, to prepare budget on the basis of ABB manager of Tata Motors

requires in-depth understanding about the various functional area of business.

In this, company has to employ top officials for conducting numerous analysis.

Hence, high resource consumption closely influences functioning and performance of

business unit.

Budgetary control: This is another most effectual technique that can be undertaken by

Tata Motors for planning purpose. On the basis of such technique, manager makes

comparison of actual figures with the budgeted aspects. In this, on the identification of

deviation managers make effort to assess the reasons associated with the same. Hence, using

the tool of budgetary control and taking into account the reasons for deviations management

team of Tata Motors can set specific, measurable, achievable, realistic as well as time bound

financial goals.

Advantages

Tool of variance analysis helps in setting suitable standards for the upcoming time

period. This in turn enhances employee motivation and thereby makes contribution in

the attainment of organizational goals.

Gives clear indication regarding the training need of personnel

Provides assistance in recognizing and monitoring departmental performance on

periodic basis.

others.

Activity based budgeting technique eliminates bottlenecks and thereby ensures

smooth functioning of the operations (Advantages, Disadvantages and Limitations of

Activity Based Costing (ABC) System, 2018).

In ABB, emphasis is placed on evaluating each and every cost driver. Thus, by

avoiding all the irrelevant activities manager of Tata Motors can develop highly

effectual plan.

Disadvantage:

Budget preparation according to ABB is highly complex and time consuming in

nature. Moreover, financial planning on the basis of ABB includes research and

analysis of various factors.

In addition to this, to prepare budget on the basis of ABB manager of Tata Motors

requires in-depth understanding about the various functional area of business.

In this, company has to employ top officials for conducting numerous analysis.

Hence, high resource consumption closely influences functioning and performance of

business unit.

Budgetary control: This is another most effectual technique that can be undertaken by

Tata Motors for planning purpose. On the basis of such technique, manager makes

comparison of actual figures with the budgeted aspects. In this, on the identification of

deviation managers make effort to assess the reasons associated with the same. Hence, using

the tool of budgetary control and taking into account the reasons for deviations management

team of Tata Motors can set specific, measurable, achievable, realistic as well as time bound

financial goals.

Advantages

Tool of variance analysis helps in setting suitable standards for the upcoming time

period. This in turn enhances employee motivation and thereby makes contribution in

the attainment of organizational goals.

Gives clear indication regarding the training need of personnel

Provides assistance in recognizing and monitoring departmental performance on

periodic basis.

Helps in developing suitable incentive plans for the personnel

It helps in reducing production cost by eliminating wasteful expenses.

Disadvantages

Sometimes high deviations occur in the financial aspects when manager fails to set

competent monetary plan. Hence, high deviations or unrealistic goals negatively

impact employee motivation and performance (Disadvantages or Limitations of

Budgetary Control, 2018). Success of budgetary control tool is highly depends on the support of top

management. In the case of failure pertaining to support from the side of top

management may result into inappropriate evaluation.

P5 Comparing two business units in relation to the manner in which they have used

management accounting systems for responding financial problems

Financial problems are the main parts of business unit which in turn has direct impact

on its growth and success. In this, tools and techniques of management accounting are highly

prominent that can be used by business unit for responding monetary problems. Jaguar is also

one of the leading automobile companies which provide customers with high-tech vehicles.

Similarly Tata Motors, Jaguar also undertakes management accounting tools for dealing with

monetary issues. However, tools which are employed by Tata Motors and Jaguar highly

differ to the significant level.

Tata Motors undertake benchmarking technique with the motive to measure and

evaluate financial performance. On the basis of such technique, manager of such automotive

firm does comparison of performance on periodical basis. This in turn clearly presents

deviations take place in financial performance in against to the budgeted figures

(Wickramasinghe and Alawattage, 2012). By taking into account such information manager

would become able to make modifications in financial framework within the suitable time

frame. Hence, benchmarking technique gives input for decision making and thereby helps in

improving performance (Garrison and et.al., 2010). On the other side, Jaguar undertakes key

performance indicator tool of management accounting for solving financial issues. Jaguar sets

several indicators regarding sales, profit, market share etc. Hence, by comparing current

performance in against to the set KPI’s Jaguar assesses the extent to which goals are met.

This technique of management accounting helps business unit in undertaking strategic action

for improvement (Baldvinsdottir, Mitchell and Nørreklit, 2010). However, if business unit

It helps in reducing production cost by eliminating wasteful expenses.

Disadvantages

Sometimes high deviations occur in the financial aspects when manager fails to set

competent monetary plan. Hence, high deviations or unrealistic goals negatively

impact employee motivation and performance (Disadvantages or Limitations of

Budgetary Control, 2018). Success of budgetary control tool is highly depends on the support of top

management. In the case of failure pertaining to support from the side of top

management may result into inappropriate evaluation.

P5 Comparing two business units in relation to the manner in which they have used

management accounting systems for responding financial problems

Financial problems are the main parts of business unit which in turn has direct impact

on its growth and success. In this, tools and techniques of management accounting are highly

prominent that can be used by business unit for responding monetary problems. Jaguar is also

one of the leading automobile companies which provide customers with high-tech vehicles.

Similarly Tata Motors, Jaguar also undertakes management accounting tools for dealing with

monetary issues. However, tools which are employed by Tata Motors and Jaguar highly

differ to the significant level.

Tata Motors undertake benchmarking technique with the motive to measure and

evaluate financial performance. On the basis of such technique, manager of such automotive

firm does comparison of performance on periodical basis. This in turn clearly presents

deviations take place in financial performance in against to the budgeted figures

(Wickramasinghe and Alawattage, 2012). By taking into account such information manager

would become able to make modifications in financial framework within the suitable time

frame. Hence, benchmarking technique gives input for decision making and thereby helps in

improving performance (Garrison and et.al., 2010). On the other side, Jaguar undertakes key

performance indicator tool of management accounting for solving financial issues. Jaguar sets

several indicators regarding sales, profit, market share etc. Hence, by comparing current

performance in against to the set KPI’s Jaguar assesses the extent to which goals are met.

This technique of management accounting helps business unit in undertaking strategic action

for improvement (Baldvinsdottir, Mitchell and Nørreklit, 2010). However, if business unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.