Applying Modern Portfolio Theory: Investment Strategies and Analysis

VerifiedAdded on 2023/06/11

|13

|3858

|271

Report

AI Summary

This report provides a comprehensive analysis of investment strategies using Modern Portfolio Theory, covering topics such as factors affecting risk tolerance, problems with portfolio allocation, return requirements for retirement, and investment constraints. It includes calculations for forward rates on T-bills, Macaulay duration, and percentage changes in bond prices, along with an industry analysis and computation of a company's intrinsic value for investment advice. The report uses the case of Maggie to discuss investment portfolio management or wealth management. The modern portfolio theory is an emerging concept in the field of investment suggesting a way for investment selection, so that overall returns could be maximized at a level of risk acceptable to investor. The basic idea of modern portfolio theory is to diversify portfolio among different investment options having risk and return either high or low.

MODERN PORTFOLIO

THEORY

THEORY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

QUESTION 1...................................................................................................................................3

a. Identification and explanation of factors affecting Maggie’s ability to take risk...................3

b. Problems identified with respect to current allocation of Maggie’s portfolio........................4

c. Calculation of return requirement for Maggie’s investment portfolio with respect to her

retirement phase..........................................................................................................................4

d. Identification of liquidity requirement, time horizons and unique circumstances for

Maggie’s investment constraint..................................................................................................5

e...................................................................................................................................................6

QUESTION 2...................................................................................................................................6

Calculation of one year forward rate three years from now and two-year forward rate one year

from now for the T-bills..............................................................................................................6

QUESTION 3...................................................................................................................................8

b. Computation of intrinsic value of stock..................................................................................9

c. Weaknesses of P/E ratio........................................................................................................10

REFERENCES..............................................................................................................................12

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

QUESTION 1...................................................................................................................................3

a. Identification and explanation of factors affecting Maggie’s ability to take risk...................3

b. Problems identified with respect to current allocation of Maggie’s portfolio........................4

c. Calculation of return requirement for Maggie’s investment portfolio with respect to her

retirement phase..........................................................................................................................4

d. Identification of liquidity requirement, time horizons and unique circumstances for

Maggie’s investment constraint..................................................................................................5

e...................................................................................................................................................6

QUESTION 2...................................................................................................................................6

Calculation of one year forward rate three years from now and two-year forward rate one year

from now for the T-bills..............................................................................................................6

QUESTION 3...................................................................................................................................8

b. Computation of intrinsic value of stock..................................................................................9

c. Weaknesses of P/E ratio........................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Portfolio Management is an art for making the decision which would help in prosper the

company as well as the individual investor. It helps in managing out the allocation of assets

properly so that the objectives could be met. The individual investment could be made in the

form of bonds, shares, mutual funds, cash or a combination of two or more of these alternative

options to create modern portfolio (Rodríguez, Gómez and Contreras, 2021). The purpose of

creating portfolio while making investment is to maximize total returns. Modern portfolio theory

is an emerging concept in the field of investment suggesting a way for investment selection, so

that overall returns could be maximized at a level of risk acceptable to investor. The basic idea of

modern portfolio theory is to diversify portfolio among different investment options having risk

and return either high or low. The present report consists of three questions where the first

question is about investment portfolio management or wealth management with regards to the

case of Maggie where factors affecting her risk taking ability will be discussed along with

identifying the problems with her current portfolio allocation. Also, the calculation of required

return at retirement phase will be done. In second question, calculations pertaining to forward

rates for T – bills and Macaulay duration & percentage change in bond price will be done with

respect to a corporate bond. In the last question, that is the third one, industry analysis and

computation of company’s intrinsic value will be done for dividend paying stock listed on UK

stock exchange in order to extend investment advice to a client.

MAIN BODY

QUESTION 1

a. Identification and explanation of factors affecting Maggie’s ability to take risk

From the case study provided for Maggie, it has been determined that she is self-sufficient

in terms of meeting her living costs, no one is dependent over her, she is going to retire after 10

years and desire to give an amount of US $ 10 million at the age of 80 years when she will die.

Accordingly, the following factors could affect her risk taking ability:

Independents: Burden of debt can be taken as an independent factor affecting risk taking ability

of an investor. Therefore, as Maggie having no burden of debt and instead of that have constant

income through her employment as well as insurance coverage for the reimbursement of her

Portfolio Management is an art for making the decision which would help in prosper the

company as well as the individual investor. It helps in managing out the allocation of assets

properly so that the objectives could be met. The individual investment could be made in the

form of bonds, shares, mutual funds, cash or a combination of two or more of these alternative

options to create modern portfolio (Rodríguez, Gómez and Contreras, 2021). The purpose of

creating portfolio while making investment is to maximize total returns. Modern portfolio theory

is an emerging concept in the field of investment suggesting a way for investment selection, so

that overall returns could be maximized at a level of risk acceptable to investor. The basic idea of

modern portfolio theory is to diversify portfolio among different investment options having risk

and return either high or low. The present report consists of three questions where the first

question is about investment portfolio management or wealth management with regards to the

case of Maggie where factors affecting her risk taking ability will be discussed along with

identifying the problems with her current portfolio allocation. Also, the calculation of required

return at retirement phase will be done. In second question, calculations pertaining to forward

rates for T – bills and Macaulay duration & percentage change in bond price will be done with

respect to a corporate bond. In the last question, that is the third one, industry analysis and

computation of company’s intrinsic value will be done for dividend paying stock listed on UK

stock exchange in order to extend investment advice to a client.

MAIN BODY

QUESTION 1

a. Identification and explanation of factors affecting Maggie’s ability to take risk

From the case study provided for Maggie, it has been determined that she is self-sufficient

in terms of meeting her living costs, no one is dependent over her, she is going to retire after 10

years and desire to give an amount of US $ 10 million at the age of 80 years when she will die.

Accordingly, the following factors could affect her risk taking ability:

Independents: Burden of debt can be taken as an independent factor affecting risk taking ability

of an investor. Therefore, as Maggie having no burden of debt and instead of that have constant

income through her employment as well as insurance coverage for the reimbursement of her

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

medical expenses must be having greater ability to take risk and accordingly, could invest in

riskier asset such as equities (Hawley, J. P. and Lukomnik, J., 2018).

Dependents: From the case of Maggie, it has been determined that no one is dependent on

Maggie instead her three children are having well-paid jobs. Accordingly, Maggie’s ability to

take risks would be higher on this ground because she is not the sole earning member of the

family instead having several earning sources such as employment income, investment income,

etc. Furthermore, she is not depending on investments for financing her emergency needs such as

for bearing medical expenses because to meet the same she has a separate insurance policy as

well. Therefore, in the absence of dependency, Maggie’s ability to take risks get increases (De

Bortoli and et.al., 2019).

b. Problems identified with respect to current allocation of Maggie’s portfolio

Portfolio allocation related problems with respect to Maggie are as follows:

No element of debt: Maggie has already attended 50 in terms of age and investing majorly that

is, around 70% of the investible fund has been allocated to equities of large and small caps stocks

and stocks of TESLA. However, there is no allocation made towards less risky or safe

investment alternatives such as fixed income securities and other debt instruments (Obeidat and

et.al., 2018). Accordingly, such a higher level of risk taking at the time of retirement planning is

not favourable and not at all recommended.

Huge allocation made to Cash or money market instrument: Maggie’s retirement has 10 years

to go which is quite long duration not demanding for holding large amount in the form of cash or

cash equivalents. However, Maggie has allocated excessively high that is, 30% towards the cash

and as a result of which she is not able to earn either fixed income or gain capital appreciation by

allocating this additional amount towards debt or equity instruments respectively (Malandri and

et.al., 2018).

c. Calculation of return requirement for Maggie’s investment portfolio with respect to her

retirement phase

As Maggie targeted to gift US$10 million to her children at the time of death which is

expected to fall in the age of 80 years giving a time horizon of 30 years. In this duration

of 30 years, she interim focus must be on growing the value of her portfolio partly

through constant income and partly through capital appreciation by investing in stock

riskier asset such as equities (Hawley, J. P. and Lukomnik, J., 2018).

Dependents: From the case of Maggie, it has been determined that no one is dependent on

Maggie instead her three children are having well-paid jobs. Accordingly, Maggie’s ability to

take risks would be higher on this ground because she is not the sole earning member of the

family instead having several earning sources such as employment income, investment income,

etc. Furthermore, she is not depending on investments for financing her emergency needs such as

for bearing medical expenses because to meet the same she has a separate insurance policy as

well. Therefore, in the absence of dependency, Maggie’s ability to take risks get increases (De

Bortoli and et.al., 2019).

b. Problems identified with respect to current allocation of Maggie’s portfolio

Portfolio allocation related problems with respect to Maggie are as follows:

No element of debt: Maggie has already attended 50 in terms of age and investing majorly that

is, around 70% of the investible fund has been allocated to equities of large and small caps stocks

and stocks of TESLA. However, there is no allocation made towards less risky or safe

investment alternatives such as fixed income securities and other debt instruments (Obeidat and

et.al., 2018). Accordingly, such a higher level of risk taking at the time of retirement planning is

not favourable and not at all recommended.

Huge allocation made to Cash or money market instrument: Maggie’s retirement has 10 years

to go which is quite long duration not demanding for holding large amount in the form of cash or

cash equivalents. However, Maggie has allocated excessively high that is, 30% towards the cash

and as a result of which she is not able to earn either fixed income or gain capital appreciation by

allocating this additional amount towards debt or equity instruments respectively (Malandri and

et.al., 2018).

c. Calculation of return requirement for Maggie’s investment portfolio with respect to her

retirement phase

As Maggie targeted to gift US$10 million to her children at the time of death which is

expected to fall in the age of 80 years giving a time horizon of 30 years. In this duration

of 30 years, she interim focus must be on growing the value of her portfolio partly

through constant income and partly through capital appreciation by investing in stock

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which are riskier as well. Maggie having high risk taking ability could go for large cap

stock for growing her portfolio in desired manner.

For the maintenance of current lifestyle, she has to generate amount equivalent to

$370000 ($250000 * (1 + 4%)^10 = $250000 * 1.48) annually, which is an income

adjusted for inflation for the purpose of retirement.

With the expected return on portfolio being 10.8%, Maggie would get nominal after tax

return of 7.56 % (10.8 * 0.7) for each year till the retirement arrives and accordingly, the

portfolio value would be $3000000 * (1 + 7.56%)^10 = $3000000 * 2.072 = $6216000.

For getting $370000 on $6216000, the return equivalent to 5.95% (370000 / 6216000) is

needed.

d. Identification of liquidity requirement, time horizons and unique circumstances for Maggie’s

investment constraint

Liquidity needs: This could be defined as a need either for cash reserved for coping up with the

emergency circumstances. Maggie’s liquidity requirement is lower and also she has an attractive

annual salary of $250000 sufficient for financing her living costs. Furthermore, there is no

concern with respect to medical expenses in the presence of whole-life medical insurance plan

(Periwal, 2018).

Time horizon: There involves multistage time horizon where first stage consists of 10 years to

get retire while the second stage is a long term consists of 30 years or more to die. During the

first stage, the arrangement for the second stage must be done in terms of financial affairs which

is the dominating one out of the two. This is because in this stage, Maggie needs to fulfil her

living costs along with providing for her desire of gifting US$10 million to her three children.

Unique circumstances: There is a need to seek estate planning assistance in a legal manner in

order to implement her gift program for her children at the time of death. Furthermore, the

existing investment portfolio will be held till retirement and as she has secure capital

appreciation on Tesla stock, it is necessary for her to sell the same at a higher value or before the

value begins to fall in order to ensure sustainability of current lifestyle post retirement (Huy,

2018).

e.

i. There are two types of retirement plan, defined benefit and defined contribution plan. In the

former case, the responsibility for benefits in terms of retirement income is held with the plan

stock for growing her portfolio in desired manner.

For the maintenance of current lifestyle, she has to generate amount equivalent to

$370000 ($250000 * (1 + 4%)^10 = $250000 * 1.48) annually, which is an income

adjusted for inflation for the purpose of retirement.

With the expected return on portfolio being 10.8%, Maggie would get nominal after tax

return of 7.56 % (10.8 * 0.7) for each year till the retirement arrives and accordingly, the

portfolio value would be $3000000 * (1 + 7.56%)^10 = $3000000 * 2.072 = $6216000.

For getting $370000 on $6216000, the return equivalent to 5.95% (370000 / 6216000) is

needed.

d. Identification of liquidity requirement, time horizons and unique circumstances for Maggie’s

investment constraint

Liquidity needs: This could be defined as a need either for cash reserved for coping up with the

emergency circumstances. Maggie’s liquidity requirement is lower and also she has an attractive

annual salary of $250000 sufficient for financing her living costs. Furthermore, there is no

concern with respect to medical expenses in the presence of whole-life medical insurance plan

(Periwal, 2018).

Time horizon: There involves multistage time horizon where first stage consists of 10 years to

get retire while the second stage is a long term consists of 30 years or more to die. During the

first stage, the arrangement for the second stage must be done in terms of financial affairs which

is the dominating one out of the two. This is because in this stage, Maggie needs to fulfil her

living costs along with providing for her desire of gifting US$10 million to her three children.

Unique circumstances: There is a need to seek estate planning assistance in a legal manner in

order to implement her gift program for her children at the time of death. Furthermore, the

existing investment portfolio will be held till retirement and as she has secure capital

appreciation on Tesla stock, it is necessary for her to sell the same at a higher value or before the

value begins to fall in order to ensure sustainability of current lifestyle post retirement (Huy,

2018).

e.

i. There are two types of retirement plan, defined benefit and defined contribution plan. In the

former case, the responsibility for benefits in terms of retirement income is held with the plan

sponsor and is inflation adjusted while in the latter case, plan sponsor is responsible for a fixed %

contribution out of the salary of plan participant who is thus responsible for the benefits

accordingly.

In case of DB plan, sponsor bears all the risk while in case of DC plan, participants bear all the

risks and thus provides for greater probability of benefit as compared to DB plan.

Hugo in her young age is capable of taking greater risk and could set his own objectives

pertaining to risk and return. Therefore, DC plan is suitable for Hugo which is having greater

probability of benefits as well.

ii. Two characteristics of Defined Contribution plan

Plan participants has the duty to set the constraints and objectives with respect to risk and

return (Singh and Yadav, 2021).

With the several investment options offered by sponsor, participant could choose most

suitable options on the basis of their risk/return objectives and constraints. However, the

latter remains responsible for benefits from the plan in future.

QUESTION 2

Calculation of one year forward rate three years from now and two-year forward rate one year

from now for the T-bills

One year forward rate three years from now has been calculate with the help of following

formula:

(((1 + Spot rate for time period 1) ^ Time period 1) / ((1 + Spot rate for time period 2) ^ Time

period 2)) ^ (1 / (Time period 1 - Time period 2)) – 1

Spot rate for time period 1 = Spot rate in year 4 = 6.2%

Time period 1 = year 4

Spot rate for time period 2 = Spot rate in year 3 = 6%

Time period 2 = year 3

Accordingly,

(((1 + 0.062) ^ 4) / ((1 + 0.06) ^ 3)) ^ (1 / (4 - 3)) – 1

= (1.2720 / 1.2624) ^1 – 1

= 1.0076 – 1 = 0.0076 = 0.76%

contribution out of the salary of plan participant who is thus responsible for the benefits

accordingly.

In case of DB plan, sponsor bears all the risk while in case of DC plan, participants bear all the

risks and thus provides for greater probability of benefit as compared to DB plan.

Hugo in her young age is capable of taking greater risk and could set his own objectives

pertaining to risk and return. Therefore, DC plan is suitable for Hugo which is having greater

probability of benefits as well.

ii. Two characteristics of Defined Contribution plan

Plan participants has the duty to set the constraints and objectives with respect to risk and

return (Singh and Yadav, 2021).

With the several investment options offered by sponsor, participant could choose most

suitable options on the basis of their risk/return objectives and constraints. However, the

latter remains responsible for benefits from the plan in future.

QUESTION 2

Calculation of one year forward rate three years from now and two-year forward rate one year

from now for the T-bills

One year forward rate three years from now has been calculate with the help of following

formula:

(((1 + Spot rate for time period 1) ^ Time period 1) / ((1 + Spot rate for time period 2) ^ Time

period 2)) ^ (1 / (Time period 1 - Time period 2)) – 1

Spot rate for time period 1 = Spot rate in year 4 = 6.2%

Time period 1 = year 4

Spot rate for time period 2 = Spot rate in year 3 = 6%

Time period 2 = year 3

Accordingly,

(((1 + 0.062) ^ 4) / ((1 + 0.06) ^ 3)) ^ (1 / (4 - 3)) – 1

= (1.2720 / 1.2624) ^1 – 1

= 1.0076 – 1 = 0.0076 = 0.76%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Two year forward rate one year from now has been calculate with the help of following formula:

Spot rate for time period 1 = Spot rate in year 3 = 6%

Time period 1 = year 3

Spot rate for time period 2 = Spot rate in year 1 = 4.5%

Time period 2 = year 1

Accordingly,

(((1 + 0.06) ^ 3) / ((1 + 0.045) ^ 1)) ^ (1 / (3 - 1)) – 1

= (1.191 / 1.045) ^0.5 – 1

= (1.14) ^0.5 – 1 = 1.07 – 1 = 0.07 = 7%

b.

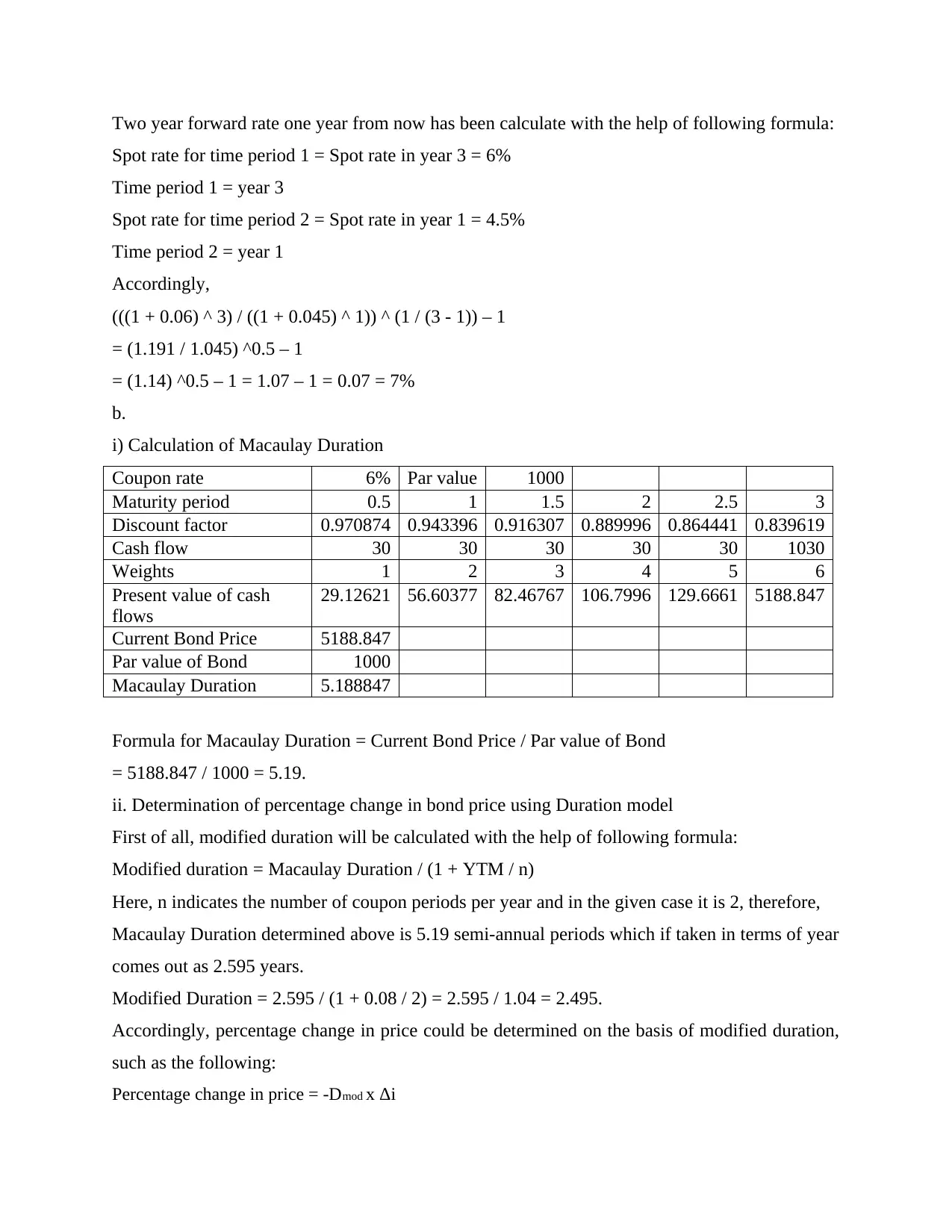

i) Calculation of Macaulay Duration

Coupon rate 6% Par value 1000

Maturity period 0.5 1 1.5 2 2.5 3

Discount factor 0.970874 0.943396 0.916307 0.889996 0.864441 0.839619

Cash flow 30 30 30 30 30 1030

Weights 1 2 3 4 5 6

Present value of cash

flows

29.12621 56.60377 82.46767 106.7996 129.6661 5188.847

Current Bond Price 5188.847

Par value of Bond 1000

Macaulay Duration 5.188847

Formula for Macaulay Duration = Current Bond Price / Par value of Bond

= 5188.847 / 1000 = 5.19.

ii. Determination of percentage change in bond price using Duration model

First of all, modified duration will be calculated with the help of following formula:

Modified duration = Macaulay Duration / (1 + YTM / n)

Here, n indicates the number of coupon periods per year and in the given case it is 2, therefore,

Macaulay Duration determined above is 5.19 semi-annual periods which if taken in terms of year

comes out as 2.595 years.

Modified Duration = 2.595 / (1 + 0.08 / 2) = 2.595 / 1.04 = 2.495.

Accordingly, percentage change in price could be determined on the basis of modified duration,

such as the following:

Percentage change in price = -Dmod x Δi

Spot rate for time period 1 = Spot rate in year 3 = 6%

Time period 1 = year 3

Spot rate for time period 2 = Spot rate in year 1 = 4.5%

Time period 2 = year 1

Accordingly,

(((1 + 0.06) ^ 3) / ((1 + 0.045) ^ 1)) ^ (1 / (3 - 1)) – 1

= (1.191 / 1.045) ^0.5 – 1

= (1.14) ^0.5 – 1 = 1.07 – 1 = 0.07 = 7%

b.

i) Calculation of Macaulay Duration

Coupon rate 6% Par value 1000

Maturity period 0.5 1 1.5 2 2.5 3

Discount factor 0.970874 0.943396 0.916307 0.889996 0.864441 0.839619

Cash flow 30 30 30 30 30 1030

Weights 1 2 3 4 5 6

Present value of cash

flows

29.12621 56.60377 82.46767 106.7996 129.6661 5188.847

Current Bond Price 5188.847

Par value of Bond 1000

Macaulay Duration 5.188847

Formula for Macaulay Duration = Current Bond Price / Par value of Bond

= 5188.847 / 1000 = 5.19.

ii. Determination of percentage change in bond price using Duration model

First of all, modified duration will be calculated with the help of following formula:

Modified duration = Macaulay Duration / (1 + YTM / n)

Here, n indicates the number of coupon periods per year and in the given case it is 2, therefore,

Macaulay Duration determined above is 5.19 semi-annual periods which if taken in terms of year

comes out as 2.595 years.

Modified Duration = 2.595 / (1 + 0.08 / 2) = 2.595 / 1.04 = 2.495.

Accordingly, percentage change in price could be determined on the basis of modified duration,

such as the following:

Percentage change in price = -Dmod x Δi

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Dmod = Modified Duration = 2.495

Δi = Percentage change in YTM

Percentage change in price = - 2.495 * 2%

Percentage change in price = -4.99% or -5%

Thus, with the rise in YTM from 8% to 10%, there will be negative change in the price of bond by

5%, that is, the bond price will fall by 5%.

iii.

Calculation of duration seems to be tricky but the information that an investor gains out of it is

quite straightforward. With the help of duration, the sensitivity of bond price with reference to

the change in YTM could be determined. If the duration is long, there is a probability of greater

changes to be taking place in the bond’s price with respect to changes taking place in YTM or

vice in case of short duration (Rivera-Castro, Pilyugina and Burnaev, 2019). Accordingly, every

small changes that took place in YTM or interest rate is being reflected in the duration. However,

with the large changes taking place in interest rates, there are more chance or underestimating or

overestimating its effect on bond’s price if it is determined through duration model. It is because

of ability of duration to determine the sensitivity of bond to its price which results in linear

relationship between bond price and interest rates.

Therefore, it can be said that duration is not considered to be a good estimator of bond

price as there is large change taking place in YTM of 200 basis points which could lead to either

overestimation or underestimation of bond’s price. Also, duration is not a standalone estimator of

how a bond will react due to not taking into account other factors such as credit quality (Gautam,

Gupta and Awasthi, 2019).

QUESTION 3

The chosen dividend paying stock listed on UK stock exchange is Tesco to provide investment

advice to the client.

a. Industry analysis of Tesco

Tesco is a leading supermarket of UK retail sector by having more than 30% of retail market’s

share. Accordingly, Porter’s five forces analysis have been performed with respect to Tesco as

follows:

Threat of new entrants: There is very low threat from new entrants coming to UK supermarket

industry as it is dominated by few competitors such as ASDA, Sainsbury, ALDI, etc. Tesco is

Δi = Percentage change in YTM

Percentage change in price = - 2.495 * 2%

Percentage change in price = -4.99% or -5%

Thus, with the rise in YTM from 8% to 10%, there will be negative change in the price of bond by

5%, that is, the bond price will fall by 5%.

iii.

Calculation of duration seems to be tricky but the information that an investor gains out of it is

quite straightforward. With the help of duration, the sensitivity of bond price with reference to

the change in YTM could be determined. If the duration is long, there is a probability of greater

changes to be taking place in the bond’s price with respect to changes taking place in YTM or

vice in case of short duration (Rivera-Castro, Pilyugina and Burnaev, 2019). Accordingly, every

small changes that took place in YTM or interest rate is being reflected in the duration. However,

with the large changes taking place in interest rates, there are more chance or underestimating or

overestimating its effect on bond’s price if it is determined through duration model. It is because

of ability of duration to determine the sensitivity of bond to its price which results in linear

relationship between bond price and interest rates.

Therefore, it can be said that duration is not considered to be a good estimator of bond

price as there is large change taking place in YTM of 200 basis points which could lead to either

overestimation or underestimation of bond’s price. Also, duration is not a standalone estimator of

how a bond will react due to not taking into account other factors such as credit quality (Gautam,

Gupta and Awasthi, 2019).

QUESTION 3

The chosen dividend paying stock listed on UK stock exchange is Tesco to provide investment

advice to the client.

a. Industry analysis of Tesco

Tesco is a leading supermarket of UK retail sector by having more than 30% of retail market’s

share. Accordingly, Porter’s five forces analysis have been performed with respect to Tesco as

follows:

Threat of new entrants: There is very low threat from new entrants coming to UK supermarket

industry as it is dominated by few competitors such as ASDA, Sainsbury, ALDI, etc. Tesco is

not required to be worried about new entrants due to having own core competencies and having

economies of scale (Rustagi, 2021).

Bargaining power of buyer: It is low for buyers in UK supermarket industry as the players are

not organised and accordingly, buyers are not deemed to be better off on switching to

competitors such as Sainsbury and ASDA. This makes the industry attractive for Tesco.

Bargaining power of suppliers: Due to having more than 2500 suppliers for Tesco in UK, there

is lower power that these suppliers could exert and accordingly, Tesco is successful in

negotiating hard with suppliers which leads to increased profit margin for it.

Threats of substitutes: It could be said that threat from substitute products is low or in fact

irrelevant in case of Tesco. This is because the company is offering wide range of products along

with their substitutes as well.

Competitive rivalry: There is an intense pressure from close competitors in terms of price wars

affecting Tesco’s profit margins. Also, there are several powerful competitors of Tesco in UK

supermarket industry who are attracting market share through lavishly spending on marketing &

advertisements. Therefore, there is high competition faced by Tesco in UK (Bhatnagar, Arjoon

and Ramlakhan, 2019).

Alongside, Tesco is operating at Growth stage of industry life cycle where company is

expanding its operations in international market, diversifying its product line by focusing on non-

food segment as well as providing customers with more retailing service options. Furthermore,

Tesco belongs to consumer staple industry of UK which is in its late business cycle and thus are

supposed to perform better than other cyclical stocks. This stage shows features such as constant

positive growth where industry has reaches its peak (Agrawal, 2021).

b. Computation of intrinsic value of stock

i. Dividend discount model

With the help of CAPM model, discount rate or required rate of return on stock has been

determined as follows:

r = risk free rate + beta * (Expected market risk premium - rf)

Assumptions:

Risk free rate = 1.53%

Beta of Tesco = 0.57

Expected market risk premium = 5.6%

economies of scale (Rustagi, 2021).

Bargaining power of buyer: It is low for buyers in UK supermarket industry as the players are

not organised and accordingly, buyers are not deemed to be better off on switching to

competitors such as Sainsbury and ASDA. This makes the industry attractive for Tesco.

Bargaining power of suppliers: Due to having more than 2500 suppliers for Tesco in UK, there

is lower power that these suppliers could exert and accordingly, Tesco is successful in

negotiating hard with suppliers which leads to increased profit margin for it.

Threats of substitutes: It could be said that threat from substitute products is low or in fact

irrelevant in case of Tesco. This is because the company is offering wide range of products along

with their substitutes as well.

Competitive rivalry: There is an intense pressure from close competitors in terms of price wars

affecting Tesco’s profit margins. Also, there are several powerful competitors of Tesco in UK

supermarket industry who are attracting market share through lavishly spending on marketing &

advertisements. Therefore, there is high competition faced by Tesco in UK (Bhatnagar, Arjoon

and Ramlakhan, 2019).

Alongside, Tesco is operating at Growth stage of industry life cycle where company is

expanding its operations in international market, diversifying its product line by focusing on non-

food segment as well as providing customers with more retailing service options. Furthermore,

Tesco belongs to consumer staple industry of UK which is in its late business cycle and thus are

supposed to perform better than other cyclical stocks. This stage shows features such as constant

positive growth where industry has reaches its peak (Agrawal, 2021).

b. Computation of intrinsic value of stock

i. Dividend discount model

With the help of CAPM model, discount rate or required rate of return on stock has been

determined as follows:

r = risk free rate + beta * (Expected market risk premium - rf)

Assumptions:

Risk free rate = 1.53%

Beta of Tesco = 0.57

Expected market risk premium = 5.6%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Therefore, r = 1.53% + 0.57 * (5.6 – 1.53) = 1.53% + 2.32% = 3.85%

Now, variable growth version of DDM will be used to determine the value of stock.

Year Period Cash

flows

Discount

factor @

3.85%

Present

value

2022 0 0.109 1 0.109

2023 1 0.108 0.962927 0.104

2024 2 0.112 0.927229 0.104

2025 3 0.123 0.892854 0.110

2026 4 0.124 0.859754 0.107

Stock price in 2026 4 3.22 0.859754 2.77

Stock price in 2026 = 0.124 / 3.85% = 3.22

Intrinsic value of stock = 0.109 + 0.104 + 0.104 + 0.110 + 0.107 + 2.77 = 3.304.

ii. Two ratios under relative valuation technique

Selected comparable is Sainsbury whose P/E and P/B ratio 10.38 and 0.79 respectively.

EPS of Tesco for the next year = 0.215

Therefore, intrinsic value of stock on the basis of P/E = 10.38 * 0.215 = 2.23.

Similarly, book value per share of Tesco for the next year = 1.92

Therefore, intrinsic value of stock on the basis of P/B = 0.79 * 1.92 = 1.52.

c. Weaknesses of P/E ratio

It tells nothing more than the growth in EPS of the company. If a concern is growing,

then EPS of such company would be growing and thus investors are tending to be

comfortable in buying such stock. However, not a perfect base for selecting investment

alternatives (Oloke, Odetunmbi and Akinwumi, 2022).

Also, this technique in determining relative valuation of a company is not appropriate due

to the requirement of choosing comparable which is considered to be quite difficult task.

Also, incorrect selection of comparable leads to misleading results and invalidate the

entire analysis.

Now, variable growth version of DDM will be used to determine the value of stock.

Year Period Cash

flows

Discount

factor @

3.85%

Present

value

2022 0 0.109 1 0.109

2023 1 0.108 0.962927 0.104

2024 2 0.112 0.927229 0.104

2025 3 0.123 0.892854 0.110

2026 4 0.124 0.859754 0.107

Stock price in 2026 4 3.22 0.859754 2.77

Stock price in 2026 = 0.124 / 3.85% = 3.22

Intrinsic value of stock = 0.109 + 0.104 + 0.104 + 0.110 + 0.107 + 2.77 = 3.304.

ii. Two ratios under relative valuation technique

Selected comparable is Sainsbury whose P/E and P/B ratio 10.38 and 0.79 respectively.

EPS of Tesco for the next year = 0.215

Therefore, intrinsic value of stock on the basis of P/E = 10.38 * 0.215 = 2.23.

Similarly, book value per share of Tesco for the next year = 1.92

Therefore, intrinsic value of stock on the basis of P/B = 0.79 * 1.92 = 1.52.

c. Weaknesses of P/E ratio

It tells nothing more than the growth in EPS of the company. If a concern is growing,

then EPS of such company would be growing and thus investors are tending to be

comfortable in buying such stock. However, not a perfect base for selecting investment

alternatives (Oloke, Odetunmbi and Akinwumi, 2022).

Also, this technique in determining relative valuation of a company is not appropriate due

to the requirement of choosing comparable which is considered to be quite difficult task.

Also, incorrect selection of comparable leads to misleading results and invalidate the

entire analysis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

De Bortoli, D., and et.al., 2019. Personality traits and investor profile analysis: A behavioral

finance study. PloS one. 14(3). p.e0214062.

Hawley, J. P. and Lukomnik, J., 2018. The third, system stage of corporate governance: Why

institutional investors need to move beyond modern portfolio theory. System Stage of

Corporate Governance: Why Institutional Investors Need to Move Beyond Modern

Portfolio Theory (February 21, 2018).

Malandri, L., and et.al., 2018. Public mood–driven asset allocation: The importance of financial

sentiment in portfolio management. Cognitive Computation. 10(6). pp.1167-1176.

Obeidat, S., and et.al., 2018. Adaptive portfolio asset allocation optimization with deep

learning. International Journal on Advances in Intelligent Systems. 11(1). pp.25-34.

Rodríguez, Y. E., Gómez, J. M. and Contreras, J., 2021. Diversified behavioral portfolio as an

alternative to Modern Portfolio Theory. The North American Journal of Economics and

Finance. 58. p.101508.

Oloke, O. C., Odetunmbi, O. A. and Akinwumi, S. A., 2022, March. An examination of the level

of engagement of modern portfolio techniques for portfolio management by real estate

firms in Lagos State, Nigeria. In IOP Conference Series: Earth and Environmental

Science (Vol. 993, No. 1, p. 012005). IOP Publishing.

Bhatnagar, C. S., Arjoon, V. and Ramlakhan, P., 2019. The Diversified Economy: Possibilities

from Modern Portfolio Management. In Development, Political, and Economic

Difficulties in the Caribbean (pp. 13-36). Palgrave Macmillan, Cham.

Rustagi, R. P., 2021. Investment Analysis & Portfolio Management. Sultan Chand & Sons.

Rivera-Castro, R., Pilyugina, P. and Burnaev, E., 2019, November. Topological data analysis for

portfolio management of cryptocurrencies. In 2019 International Conference on Data

Mining Workshops (ICDMW) (pp. 238-243). IEEE.

Singh, S. and Yadav, S. S., 2021. Security Analysis and Portfolio Management: A Primer.

Springer Nature.

Huy, L. P., 2018. Applying principal component analysis to cryptocurrency portfolio

management (Doctoral dissertation, International University-HCMC).

Periwal, D., 2018. TLP for Security Analysis and Portfolio Management 2017-2018.

Books and Journals

De Bortoli, D., and et.al., 2019. Personality traits and investor profile analysis: A behavioral

finance study. PloS one. 14(3). p.e0214062.

Hawley, J. P. and Lukomnik, J., 2018. The third, system stage of corporate governance: Why

institutional investors need to move beyond modern portfolio theory. System Stage of

Corporate Governance: Why Institutional Investors Need to Move Beyond Modern

Portfolio Theory (February 21, 2018).

Malandri, L., and et.al., 2018. Public mood–driven asset allocation: The importance of financial

sentiment in portfolio management. Cognitive Computation. 10(6). pp.1167-1176.

Obeidat, S., and et.al., 2018. Adaptive portfolio asset allocation optimization with deep

learning. International Journal on Advances in Intelligent Systems. 11(1). pp.25-34.

Rodríguez, Y. E., Gómez, J. M. and Contreras, J., 2021. Diversified behavioral portfolio as an

alternative to Modern Portfolio Theory. The North American Journal of Economics and

Finance. 58. p.101508.

Oloke, O. C., Odetunmbi, O. A. and Akinwumi, S. A., 2022, March. An examination of the level

of engagement of modern portfolio techniques for portfolio management by real estate

firms in Lagos State, Nigeria. In IOP Conference Series: Earth and Environmental

Science (Vol. 993, No. 1, p. 012005). IOP Publishing.

Bhatnagar, C. S., Arjoon, V. and Ramlakhan, P., 2019. The Diversified Economy: Possibilities

from Modern Portfolio Management. In Development, Political, and Economic

Difficulties in the Caribbean (pp. 13-36). Palgrave Macmillan, Cham.

Rustagi, R. P., 2021. Investment Analysis & Portfolio Management. Sultan Chand & Sons.

Rivera-Castro, R., Pilyugina, P. and Burnaev, E., 2019, November. Topological data analysis for

portfolio management of cryptocurrencies. In 2019 International Conference on Data

Mining Workshops (ICDMW) (pp. 238-243). IEEE.

Singh, S. and Yadav, S. S., 2021. Security Analysis and Portfolio Management: A Primer.

Springer Nature.

Huy, L. P., 2018. Applying principal component analysis to cryptocurrency portfolio

management (Doctoral dissertation, International University-HCMC).

Periwal, D., 2018. TLP for Security Analysis and Portfolio Management 2017-2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.