Risk and Return Analysis: A Study of GM and Ford Stocks

VerifiedAdded on 2022/08/16

|7

|1378

|26

Report

AI Summary

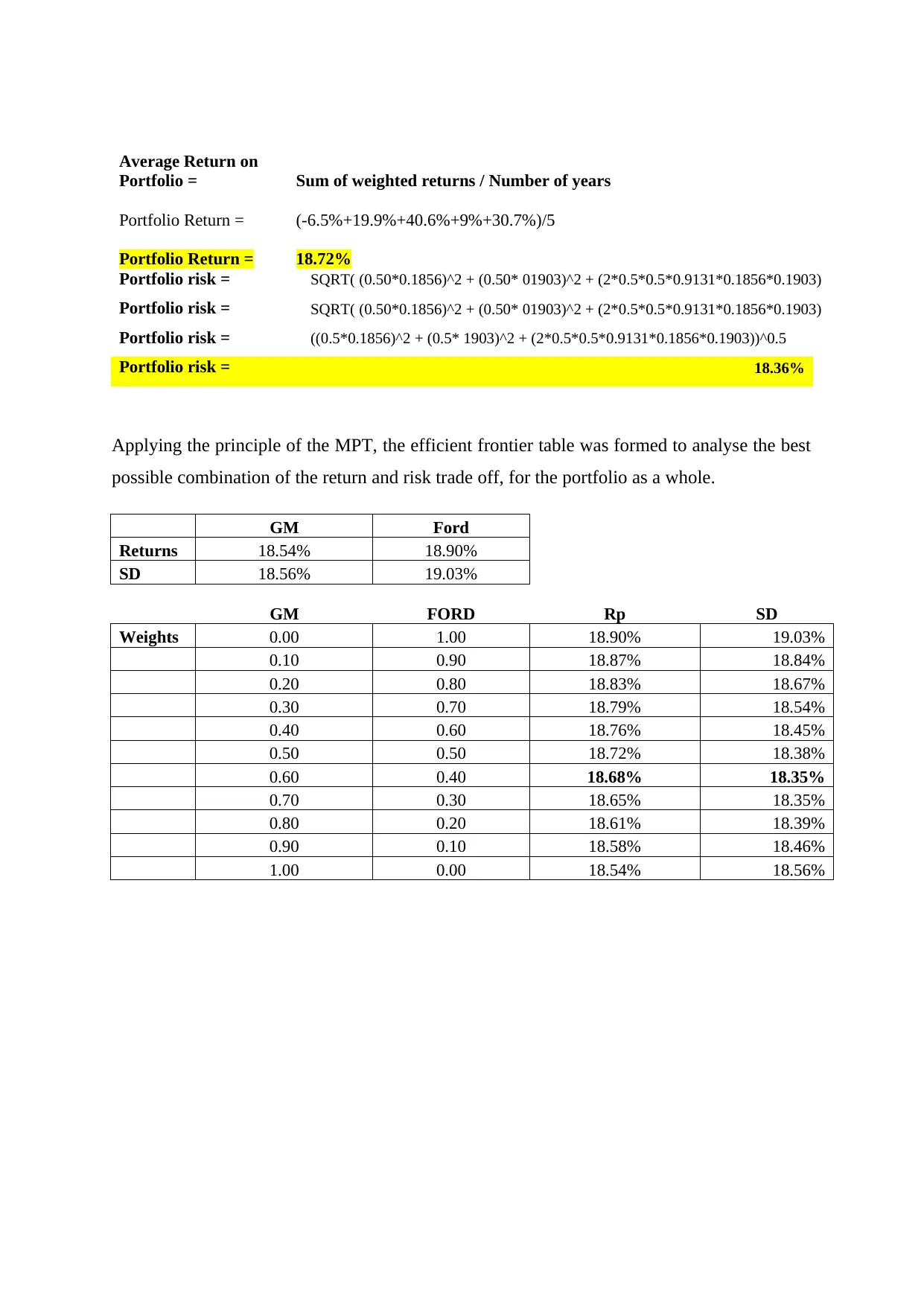

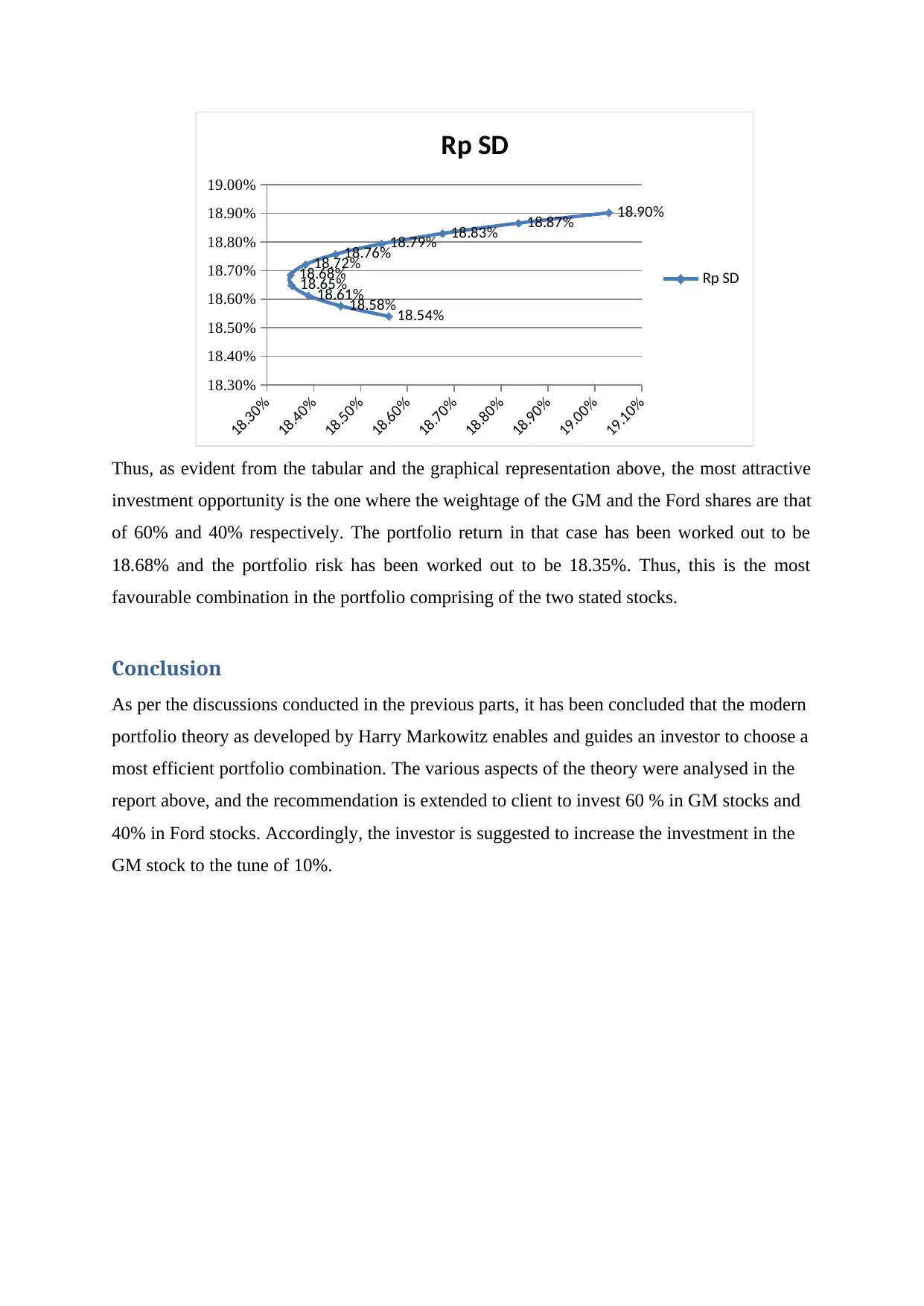

This report analyzes the risk and return of General Motors (GM) and Ford (Ford) stocks using Modern Portfolio Theory (MPT). The analysis includes calculating individual average returns, portfolio returns with equal weights, and individual stock risks (standard deviation). The report also calculates portfolio risk and explores the efficient frontier to identify the optimal stock combination for maximizing returns while minimizing risk. The findings suggest an investment strategy where 60% of the portfolio is allocated to GM stocks and 40% to Ford stocks. The report concludes that MPT provides a framework for efficient portfolio construction, guiding investors in selecting optimal asset allocations to achieve their financial goals. The report uses data from the New York Stock Exchange (NYSE) to calculate the rate of return on the asset portfolio each year. It also estimates the average return on the portfolio during the period from 2003 to 2007 and calculates the coefficient correlation between the returns of the two common stocks.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.