In-depth Financial Analysis Report of Moelis Australia Company

VerifiedAdded on 2023/04/21

|3

|1015

|362

Report

AI Summary

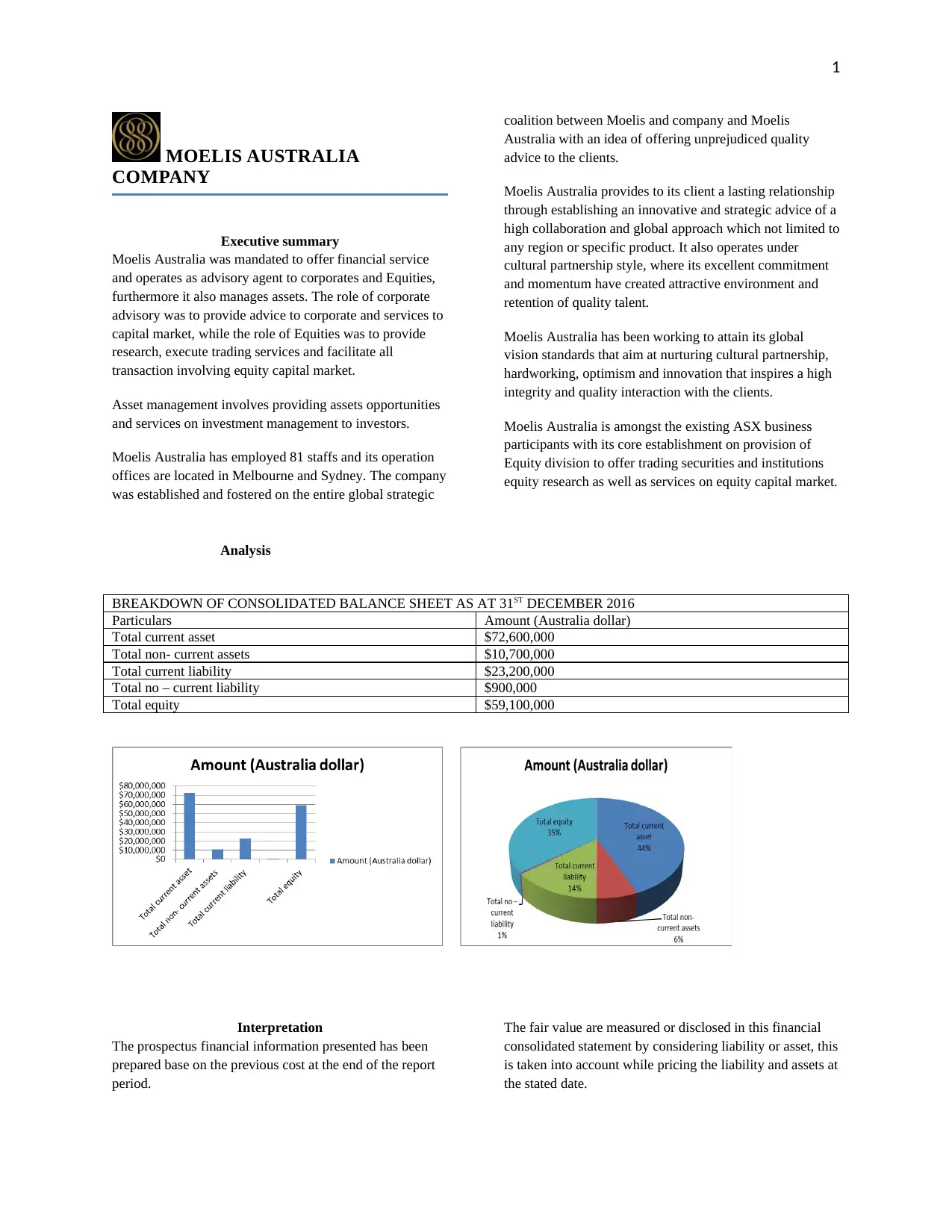

This report provides a financial analysis of Moelis Australia, focusing on their consolidated balance sheet as of December 31, 2016, revenue recognition, lease payments, and taxation. The analysis interprets the financial information based on previous costs and fair value measurements. It covers current and deferred tax implications, plant, property, and equipment considerations, and the recognition of revenue based on transaction completion. The report concludes with an overview of fair value measurement categorization and the computation of gains or losses on asset disposals, referencing key accounting principles and research.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.