Performance Management and Control: A Comprehensive Analysis

VerifiedAdded on 2022/08/25

|13

|1415

|20

Report

AI Summary

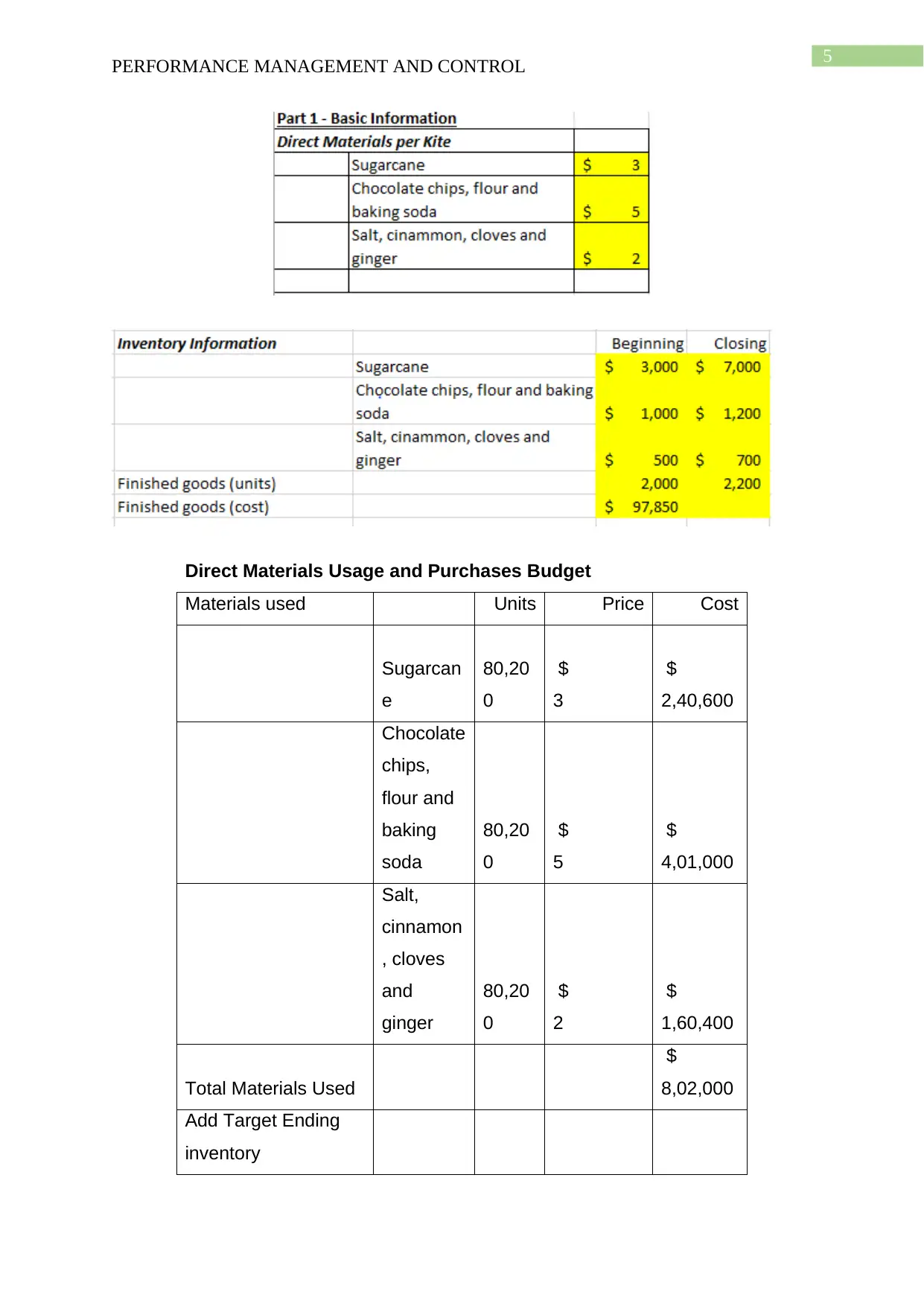

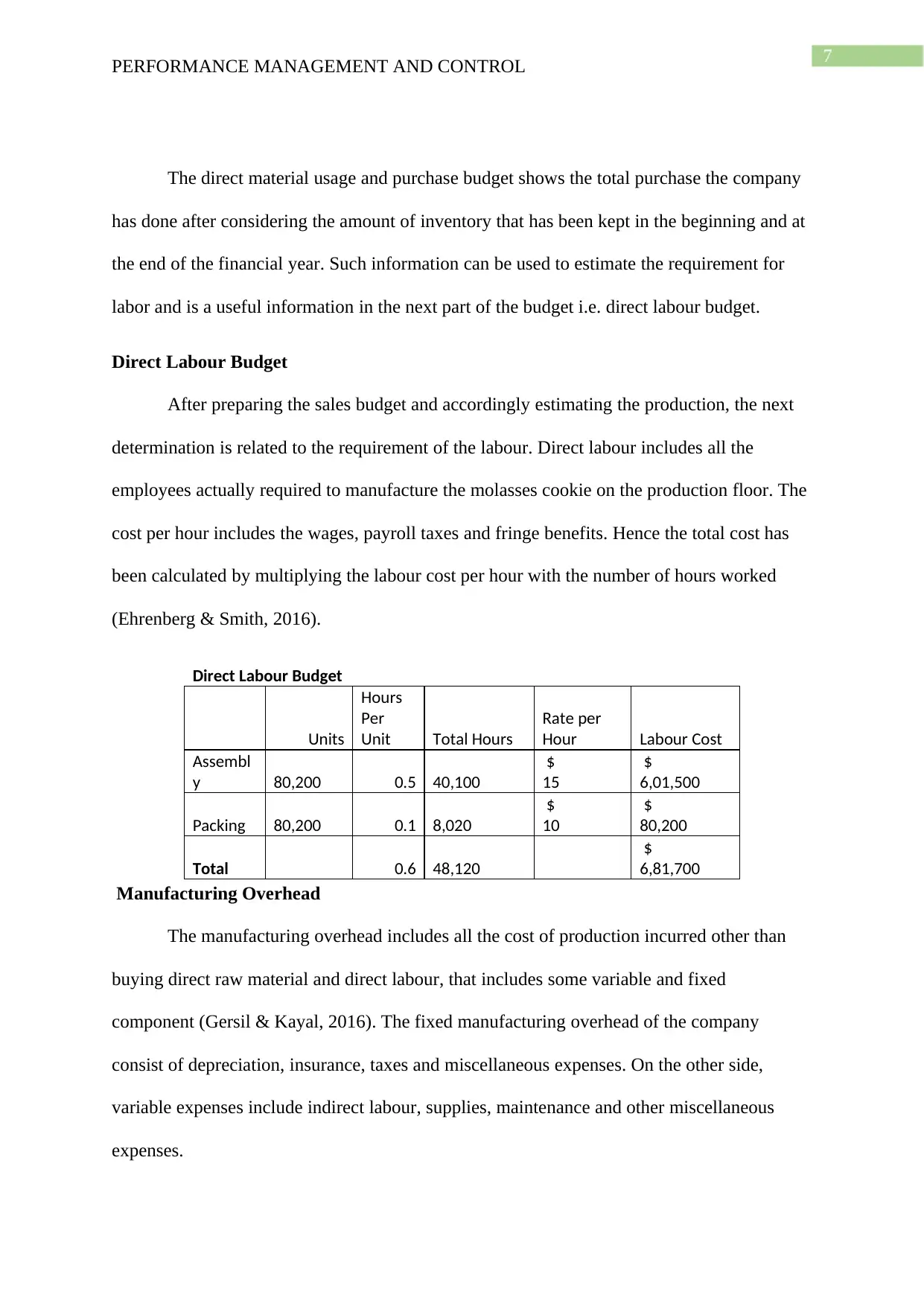

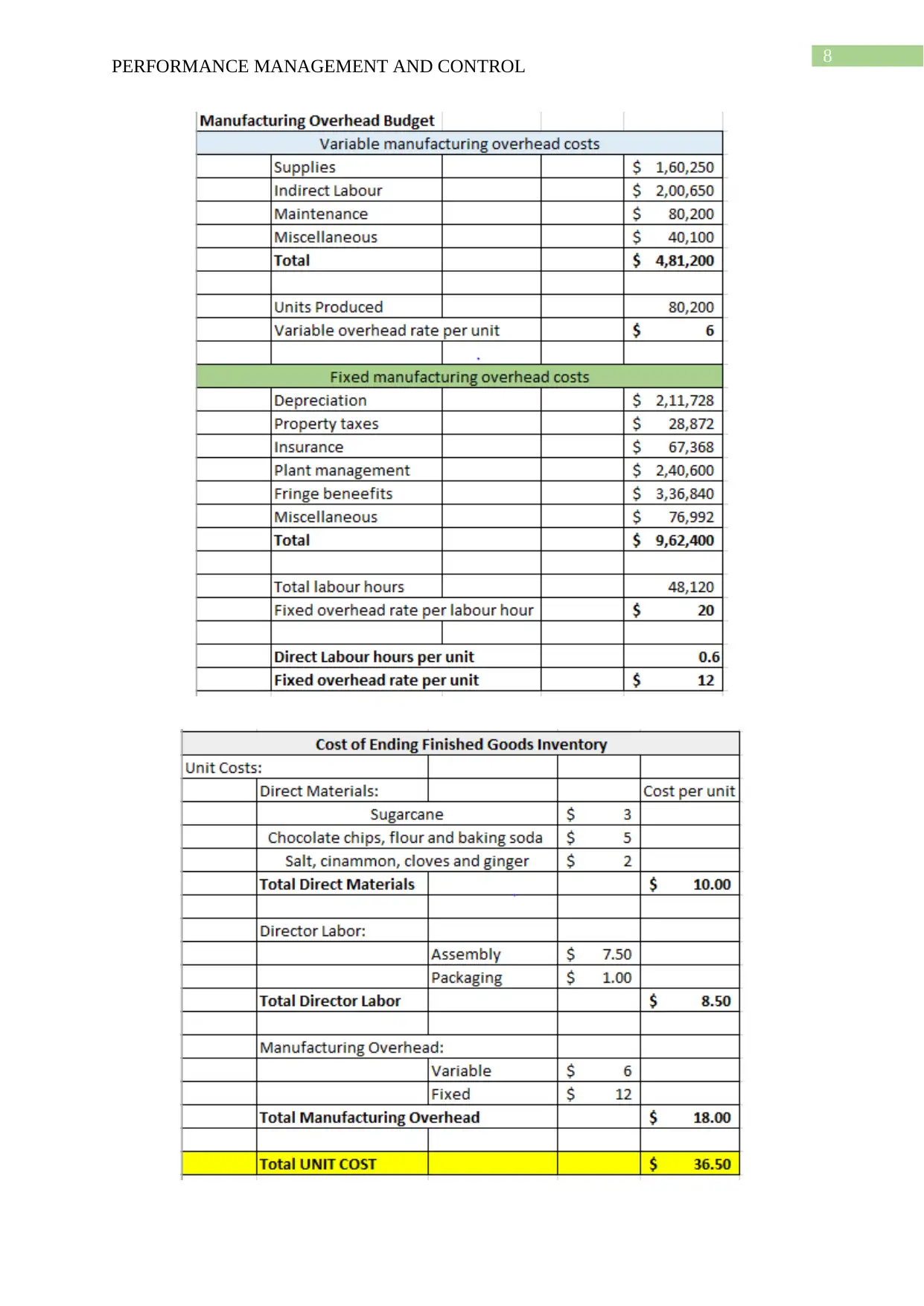

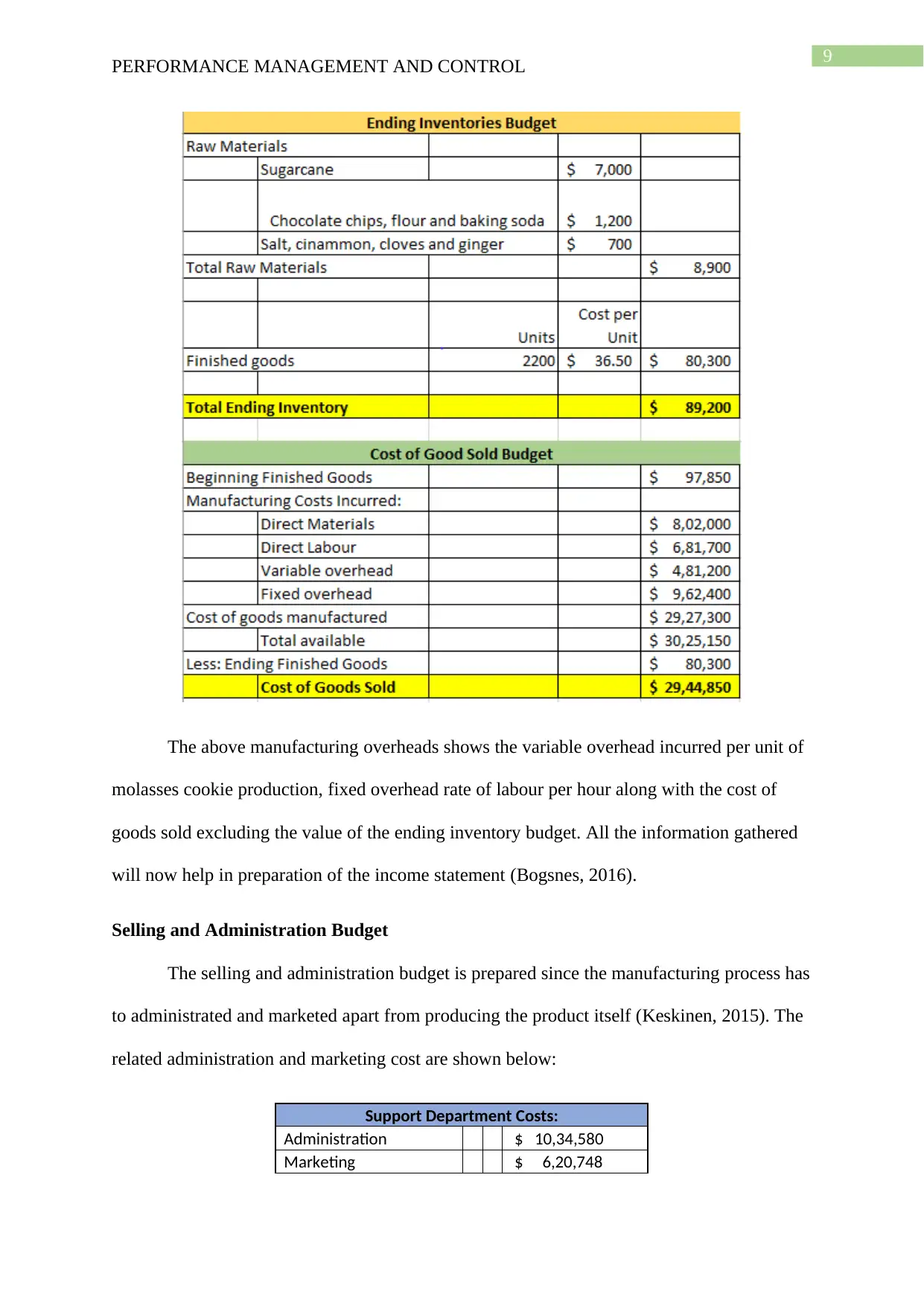

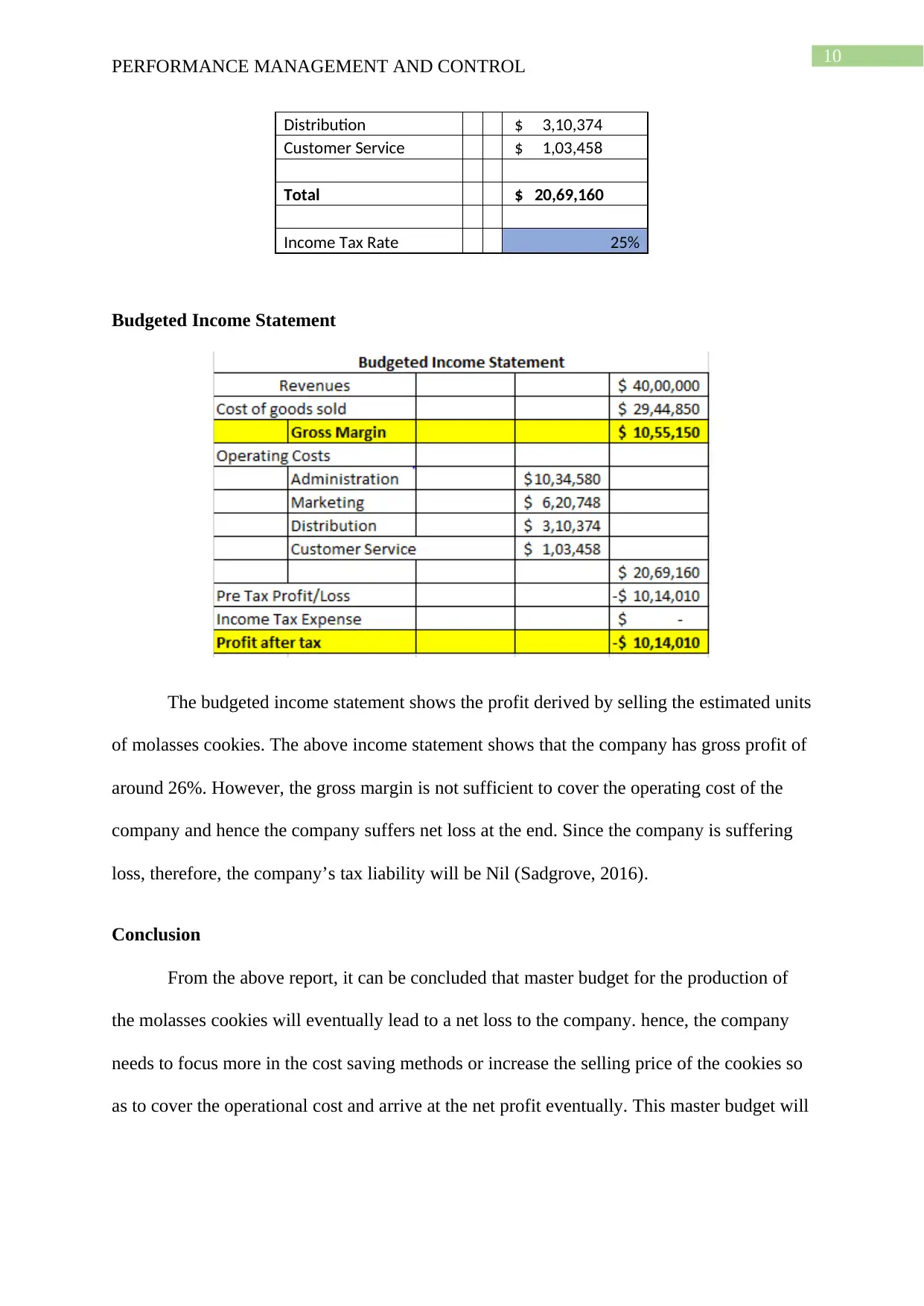

This report presents a comprehensive analysis of performance management and control, focusing on the development of a master budget for molasses cookie production. The report begins with an introduction to master budgeting, outlining its components and importance. It then delves into detailed budget components, including sales forecasts, production budgets, direct material budgets (sugarcane, chocolate chips, flour, etc.), direct labor budgets, manufacturing overhead, and selling and administration budgets. The report calculates key financial metrics, such as total revenue, material costs, labor costs, and overhead expenses. It culminates in a budgeted income statement, revealing a net loss due to operational costs exceeding the gross margin. The conclusion emphasizes the need for cost-saving measures or increased selling prices to achieve profitability, providing a valuable analysis for financial decision-making.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.