University of Sunderland Finance Report: Money, Banking and Finance

VerifiedAdded on 2021/03/25

|18

|4887

|241

Report

AI Summary

This report, submitted by Tran Linh Trang to the Banking Academy of Viet Nam, analyzes the core functions of credit and capital markets in financing companies, households, and governments, differentiating between direct and indirect finance routes, and explaining the flow of funds. It further examines the role of the State Bank of Vietnam in achieving monetary policy goals, including the management of money supply and interest rates to achieve macroeconomic objectives like inflation control and economic growth. The report details the monetary policy framework in Vietnam, including its tools such as reserve requirements, open market operations, and lending facilities. It also discusses the State Bank's independence and its impact on the economy, especially in response to the COVID-19 pandemic, and analyzes the various tools used to maintain monetary stability and stimulate economic growth. The report provides detailed data and analysis on the impact of these policies.

P a g e | 1

Money, Banking and Finance (APC 312)

Tran Linh Trang

Teacher: Tran Huu Tuyen

Student ID: 209233898/1

Word count: 3029

January 8, 2021

Banking Academy of Viet Nam

Money, Banking and Finance (APC 312)

Tran Linh Trang

Teacher: Tran Huu Tuyen

Student ID: 209233898/1

Word count: 3029

January 8, 2021

Banking Academy of Viet Nam

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P a g e | 2

UNIVERSITY OF SU

NDERLAND

BA (HONS) BANKING AND FINANCE or BA (HONS) ACCOUNTING AND FINANCIAL MANAGEMENT

Student ID: 209233898/1

Student Name: Tran Linh Trang

Module Code: APC312

Module Name / Title: Money, Banking and Finance

Due Date: 08th January 2021

Centre / College: Banking Academy of Viet Nam

Hand in Date: 08th January 2021

Assignment Title: Individual assignment

Students Signature: (you must sign this declaring that it is all your own work and all sources of

information have been referenced)

Trang

UNIVERSITY OF SU

NDERLAND

BA (HONS) BANKING AND FINANCE or BA (HONS) ACCOUNTING AND FINANCIAL MANAGEMENT

Student ID: 209233898/1

Student Name: Tran Linh Trang

Module Code: APC312

Module Name / Title: Money, Banking and Finance

Due Date: 08th January 2021

Centre / College: Banking Academy of Viet Nam

Hand in Date: 08th January 2021

Assignment Title: Individual assignment

Students Signature: (you must sign this declaring that it is all your own work and all sources of

information have been referenced)

Trang

P a g e | 3

Table of Content

Table of content 3

Part A. The major objective of credit and capital markets is to finance companies, households and

governments. Critically analyse this statement examining the different routes through which funds can

flow from the surplus to the deficit sector.

1. The different routes through which funds can flow from the surplus to the deficit sector…………….. 4

2. The major objective of credit and capital markets is to finance companies, households and

governments……………………………………………………………………………………………

7

Part B. Critically analyse the State Bank of Vietnam’s role in achieving monetary policy goals and discuss

the merits and limitations of central bank independence.

1. What is monetary policy……………………………………………………………………………… 8

2. Monetary policy in Vietnam ………………………………………………………………………… 8

a. Tools…………………………………………………………………………………………………... 8

b. Intermediate Target……………………………………………………………………………………. 10

c. Final goals ……………………………………………………………………………………………. 12

3. Central bank independence…………………………………………………………………………. 13

Table of Content

Table of content 3

Part A. The major objective of credit and capital markets is to finance companies, households and

governments. Critically analyse this statement examining the different routes through which funds can

flow from the surplus to the deficit sector.

1. The different routes through which funds can flow from the surplus to the deficit sector…………….. 4

2. The major objective of credit and capital markets is to finance companies, households and

governments……………………………………………………………………………………………

7

Part B. Critically analyse the State Bank of Vietnam’s role in achieving monetary policy goals and discuss

the merits and limitations of central bank independence.

1. What is monetary policy……………………………………………………………………………… 8

2. Monetary policy in Vietnam ………………………………………………………………………… 8

a. Tools…………………………………………………………………………………………………... 8

b. Intermediate Target……………………………………………………………………………………. 10

c. Final goals ……………………………………………………………………………………………. 12

3. Central bank independence…………………………………………………………………………. 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P a g e | 4

Part A

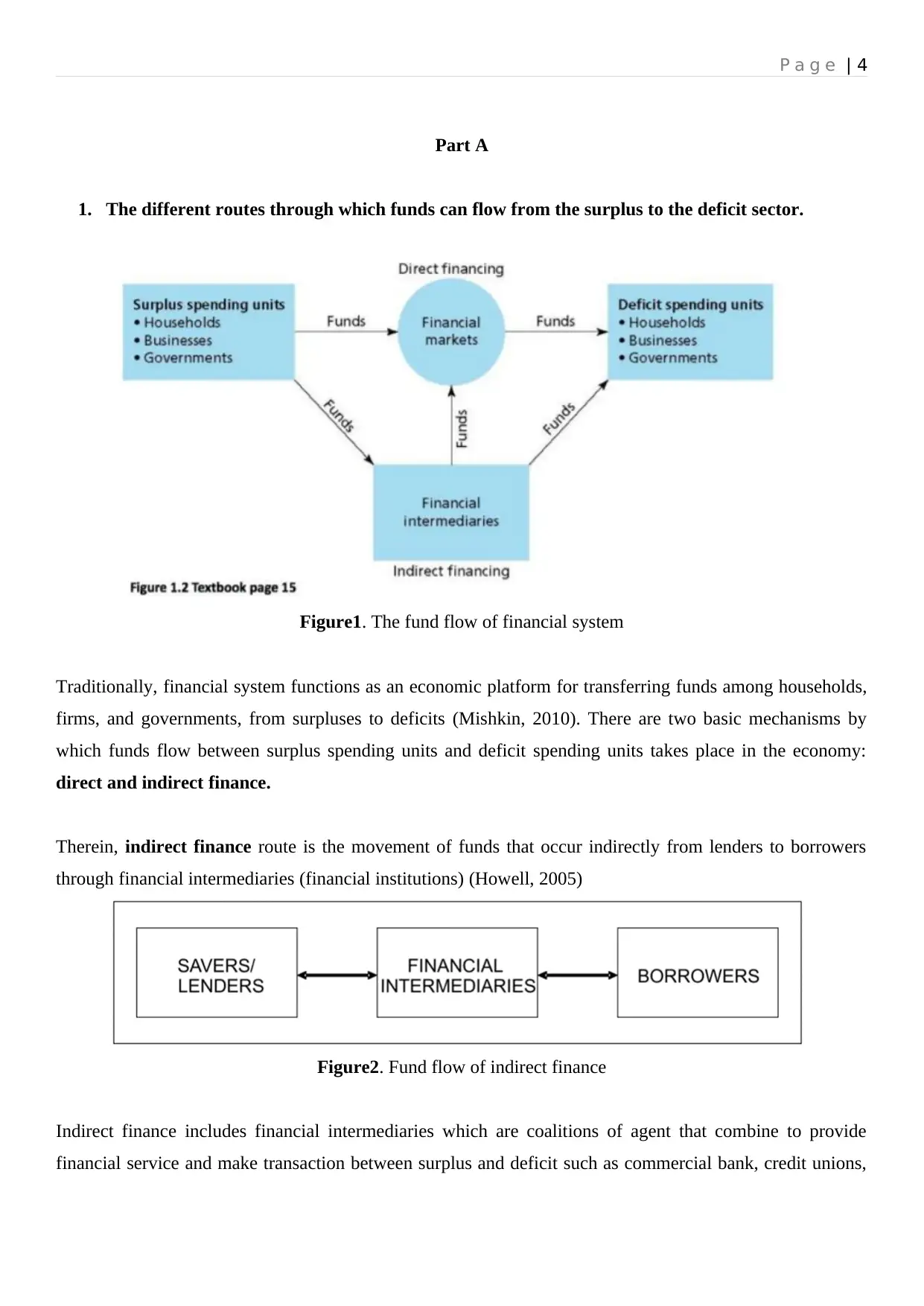

1. The different routes through which funds can flow from the surplus to the deficit sector.

Figure1. The fund flow of financial system

Traditionally, financial system functions as an economic platform for transferring funds among households,

firms, and governments, from surpluses to deficits (Mishkin, 2010). There are two basic mechanisms by

which funds flow between surplus spending units and deficit spending units takes place in the economy:

direct and indirect finance.

Therein, indirect finance route is the movement of funds that occur indirectly from lenders to borrowers

through financial intermediaries (financial institutions) (Howell, 2005)

Figure2. Fund flow of indirect finance

Indirect finance includes financial intermediaries which are coalitions of agent that combine to provide

financial service and make transaction between surplus and deficit such as commercial bank, credit unions,

Part A

1. The different routes through which funds can flow from the surplus to the deficit sector.

Figure1. The fund flow of financial system

Traditionally, financial system functions as an economic platform for transferring funds among households,

firms, and governments, from surpluses to deficits (Mishkin, 2010). There are two basic mechanisms by

which funds flow between surplus spending units and deficit spending units takes place in the economy:

direct and indirect finance.

Therein, indirect finance route is the movement of funds that occur indirectly from lenders to borrowers

through financial intermediaries (financial institutions) (Howell, 2005)

Figure2. Fund flow of indirect finance

Indirect finance includes financial intermediaries which are coalitions of agent that combine to provide

financial service and make transaction between surplus and deficit such as commercial bank, credit unions,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P a g e | 5

financial competitions and micro- finance institutions (Haan and Oosterloo, 2009) and credit markets are a

part of indirect finance. The main and regular activities of credit market are the concentration of idle capital

in the economy, using that capital to supply those in need of capital and the provision of financial services.

Households with wealth are able to receive sustain amounts in bank, then, that money converts into funds

source. New- found companies that want to borrow money are more likely to turn to commercial banks,

where they can better assess this fund to serve their company operation. Therefore, for short-term working

loans such as salary payment, raw material purchase, borrowers look to commercial banks to ensure timely

response to capital for production and business activities.

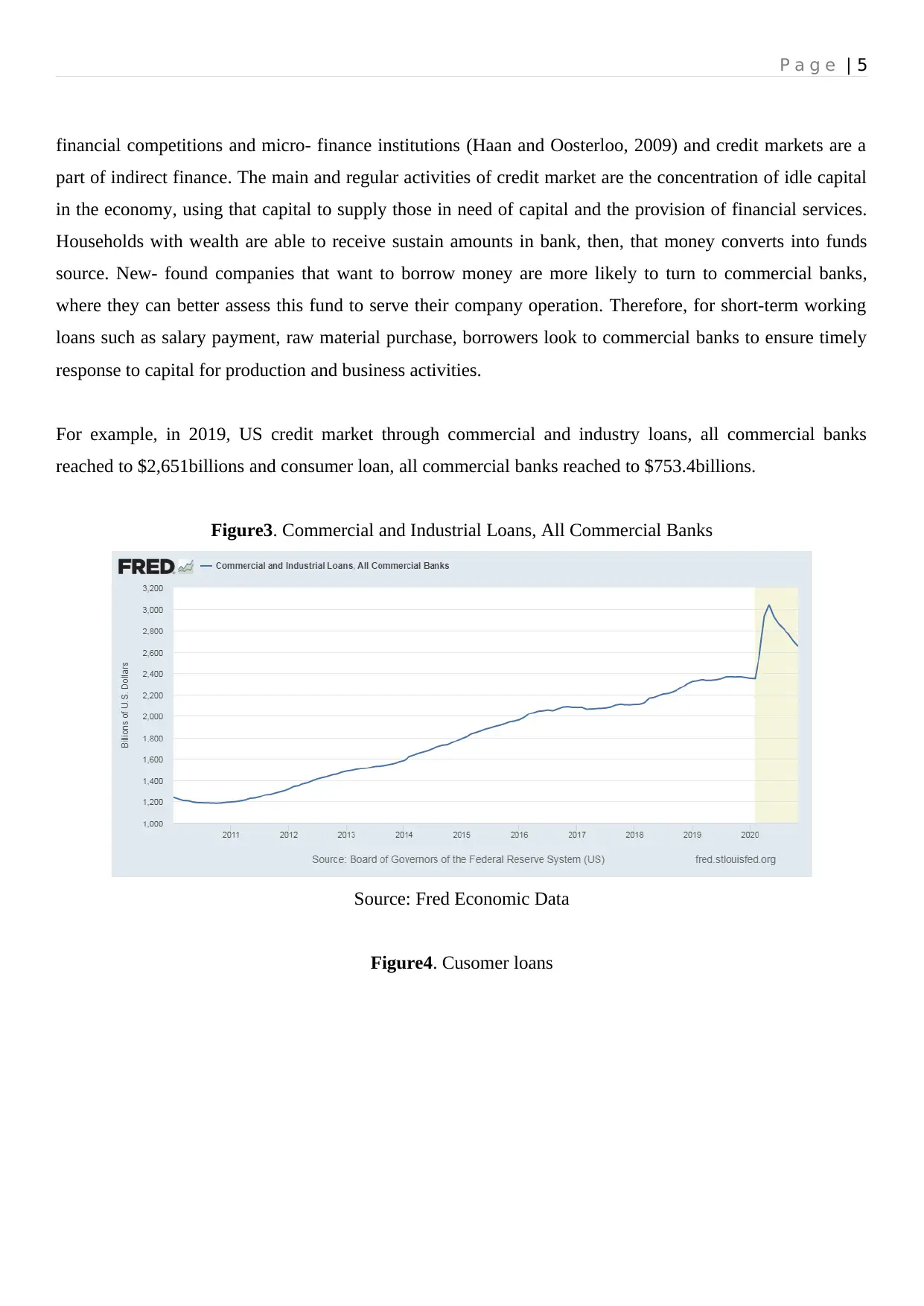

For example, in 2019, US credit market through commercial and industry loans, all commercial banks

reached to $2,651billions and consumer loan, all commercial banks reached to $753.4billions.

Figure3. Commercial and Industrial Loans, All Commercial Banks

Source: Fred Economic Data

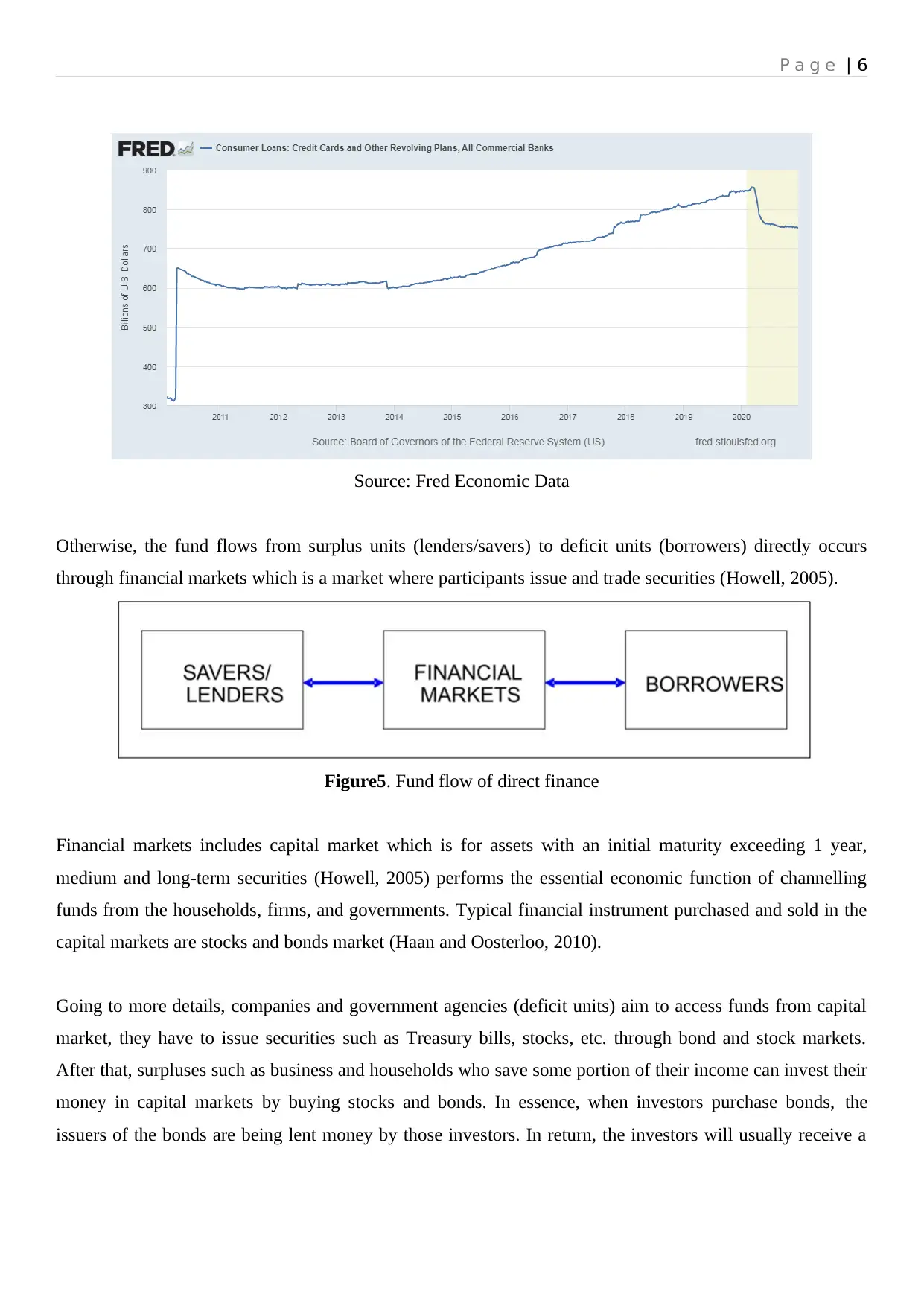

Figure4. Cusomer loans

financial competitions and micro- finance institutions (Haan and Oosterloo, 2009) and credit markets are a

part of indirect finance. The main and regular activities of credit market are the concentration of idle capital

in the economy, using that capital to supply those in need of capital and the provision of financial services.

Households with wealth are able to receive sustain amounts in bank, then, that money converts into funds

source. New- found companies that want to borrow money are more likely to turn to commercial banks,

where they can better assess this fund to serve their company operation. Therefore, for short-term working

loans such as salary payment, raw material purchase, borrowers look to commercial banks to ensure timely

response to capital for production and business activities.

For example, in 2019, US credit market through commercial and industry loans, all commercial banks

reached to $2,651billions and consumer loan, all commercial banks reached to $753.4billions.

Figure3. Commercial and Industrial Loans, All Commercial Banks

Source: Fred Economic Data

Figure4. Cusomer loans

P a g e | 6

Source: Fred Economic Data

Otherwise, the fund flows from surplus units (lenders/savers) to deficit units (borrowers) directly occurs

through financial markets which is a market where participants issue and trade securities (Howell, 2005).

Figure5. Fund flow of direct finance

Financial markets includes capital market which is for assets with an initial maturity exceeding 1 year,

medium and long-term securities (Howell, 2005) performs the essential economic function of channelling

funds from the households, firms, and governments. Typical financial instrument purchased and sold in the

capital markets are stocks and bonds market (Haan and Oosterloo, 2010).

Going to more details, companies and government agencies (deficit units) aim to access funds from capital

market, they have to issue securities such as Treasury bills, stocks, etc. through bond and stock markets.

After that, surpluses such as business and households who save some portion of their income can invest their

money in capital markets by buying stocks and bonds. In essence, when investors purchase bonds, the

issuers of the bonds are being lent money by those investors. In return, the investors will usually receive a

Source: Fred Economic Data

Otherwise, the fund flows from surplus units (lenders/savers) to deficit units (borrowers) directly occurs

through financial markets which is a market where participants issue and trade securities (Howell, 2005).

Figure5. Fund flow of direct finance

Financial markets includes capital market which is for assets with an initial maturity exceeding 1 year,

medium and long-term securities (Howell, 2005) performs the essential economic function of channelling

funds from the households, firms, and governments. Typical financial instrument purchased and sold in the

capital markets are stocks and bonds market (Haan and Oosterloo, 2010).

Going to more details, companies and government agencies (deficit units) aim to access funds from capital

market, they have to issue securities such as Treasury bills, stocks, etc. through bond and stock markets.

After that, surpluses such as business and households who save some portion of their income can invest their

money in capital markets by buying stocks and bonds. In essence, when investors purchase bonds, the

issuers of the bonds are being lent money by those investors. In return, the investors will usually receive a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P a g e | 7

fix rate of interest payments for the lifetime of the bond and receive the principal when the bond expires.

When investors buy stock, they become owners of a share of a company’s assets and earnings. If a company

is successful, the price that is willing to be paid by investors for its stock will often rise. In general, the

issuance of securities of the Government and companies can directly raise fund for them in order to serve

their production and business activities.

For example, in 2019, via debt and equity issuance activity, the US securities industry collected $2.1 trillion

of capital for businesses, a 13.0% decline from the previous year. Equity issuance, including common and

preferred shares, totaled $228.1 billion in 2019, increasing 2.9% year-over year. On the other hand, U.S.

long-term municipal bond issuance reached $426.0 billion in 2019, increasing 22.8% from $346.8 billion in

2018 (SIFMA Research, 2020)

2. The major objective of credit and capital markets is to finance companies, households and

governments.

Credit market and capital market are important instruments in intermediating between the surplus units and

deficit units, in which the surplus units are referred to the parties that excess funds while deficit units are

parties that lack of funds. The key distinction is that capital markets provide direct funding from the

Households when they buy the stocks and bonds to the Government and companies when they issued

securities, while credit markets involves indirect funding with banks as the go-between connecting the saver

and users by receiving deposits from individuals and organizations to form capital sources, to use capital

sources to provide loans in various forms or to invest in securities. End users of a financial system are the

firms, households, individuals, and government that use the services offered by the institutions and markets.

Consequently, in other word, credit and capital market’s main objective is to finance companies, households,

and Government.

Part B

fix rate of interest payments for the lifetime of the bond and receive the principal when the bond expires.

When investors buy stock, they become owners of a share of a company’s assets and earnings. If a company

is successful, the price that is willing to be paid by investors for its stock will often rise. In general, the

issuance of securities of the Government and companies can directly raise fund for them in order to serve

their production and business activities.

For example, in 2019, via debt and equity issuance activity, the US securities industry collected $2.1 trillion

of capital for businesses, a 13.0% decline from the previous year. Equity issuance, including common and

preferred shares, totaled $228.1 billion in 2019, increasing 2.9% year-over year. On the other hand, U.S.

long-term municipal bond issuance reached $426.0 billion in 2019, increasing 22.8% from $346.8 billion in

2018 (SIFMA Research, 2020)

2. The major objective of credit and capital markets is to finance companies, households and

governments.

Credit market and capital market are important instruments in intermediating between the surplus units and

deficit units, in which the surplus units are referred to the parties that excess funds while deficit units are

parties that lack of funds. The key distinction is that capital markets provide direct funding from the

Households when they buy the stocks and bonds to the Government and companies when they issued

securities, while credit markets involves indirect funding with banks as the go-between connecting the saver

and users by receiving deposits from individuals and organizations to form capital sources, to use capital

sources to provide loans in various forms or to invest in securities. End users of a financial system are the

firms, households, individuals, and government that use the services offered by the institutions and markets.

Consequently, in other word, credit and capital market’s main objective is to finance companies, households,

and Government.

Part B

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P a g e | 8

1. What is monetary policy

Monetary policy is the macroeconomic policy implemented by the central bank which involves

management of money supply and interest rate in order to achieve macroeconomic objectives like inflation,

growth and liquidity.

2. Monetary policy framework in Vietnam

According to Law on State Bank of Vietnam 1997, “the State Bank of Vietnam- SBV is a part of

Vietnamese Government (Article 1)”. However, the monetary policy decision and its supervision are largely

the responsibility of the National Assembly and the government. The SBV function includes the preparation

of the monetary policy plan (Article 5) and the implementation of monetary policy is designed by

government. Additionally, the operation of SBV is to stabilize the value of money, contributing to ensuring

the safety of banking operations and the system of credit institutions, and facilitate economic society

development as well as controlling of the inflation rate.

The principal components of the monetary policy goals can be identified as follows: ensuring the goal of

stabilizing the value of money, controlling inflation, contributing to economic growth. In 2020, facing

the Covid- 19 pandemics broke out, to cope with the decline of GDP growth and increase of inflation, the

State bank of Vietnam set the target for monetary policy management was to make a prudent loose monetary

policy to control the stability of money value objectives, inflation control no more than 4%, contributing to

GDP growth target of 2.5%, and carrying out the government’s stimulus policy (Tuan, 2020). In order to

achieve those final goals, the State bank of Vietnam has used flexible and prudent monetary policy

instrument.

a. Tools

Reserve Requirement

Reserve requirements are regulations that require depository institutions to keep a certain fraction of their

deposits in accounts with the central bank (Mishkin, 2016). According to this tool, the State bank of

Vietnam affects the volume and price of credit of commercial bank, thereby affecting the ability to provide

credit and the ability to generate money of the commercial banking system. Under Decision No.1158 / QD-

NHNN 29/05/2018 taking effect from 06/01/2018, the Reserve requirement of Vietnam as following:

1. What is monetary policy

Monetary policy is the macroeconomic policy implemented by the central bank which involves

management of money supply and interest rate in order to achieve macroeconomic objectives like inflation,

growth and liquidity.

2. Monetary policy framework in Vietnam

According to Law on State Bank of Vietnam 1997, “the State Bank of Vietnam- SBV is a part of

Vietnamese Government (Article 1)”. However, the monetary policy decision and its supervision are largely

the responsibility of the National Assembly and the government. The SBV function includes the preparation

of the monetary policy plan (Article 5) and the implementation of monetary policy is designed by

government. Additionally, the operation of SBV is to stabilize the value of money, contributing to ensuring

the safety of banking operations and the system of credit institutions, and facilitate economic society

development as well as controlling of the inflation rate.

The principal components of the monetary policy goals can be identified as follows: ensuring the goal of

stabilizing the value of money, controlling inflation, contributing to economic growth. In 2020, facing

the Covid- 19 pandemics broke out, to cope with the decline of GDP growth and increase of inflation, the

State bank of Vietnam set the target for monetary policy management was to make a prudent loose monetary

policy to control the stability of money value objectives, inflation control no more than 4%, contributing to

GDP growth target of 2.5%, and carrying out the government’s stimulus policy (Tuan, 2020). In order to

achieve those final goals, the State bank of Vietnam has used flexible and prudent monetary policy

instrument.

a. Tools

Reserve Requirement

Reserve requirements are regulations that require depository institutions to keep a certain fraction of their

deposits in accounts with the central bank (Mishkin, 2016). According to this tool, the State bank of

Vietnam affects the volume and price of credit of commercial bank, thereby affecting the ability to provide

credit and the ability to generate money of the commercial banking system. Under Decision No.1158 / QD-

NHNN 29/05/2018 taking effect from 06/01/2018, the Reserve requirement of Vietnam as following:

P a g e | 9

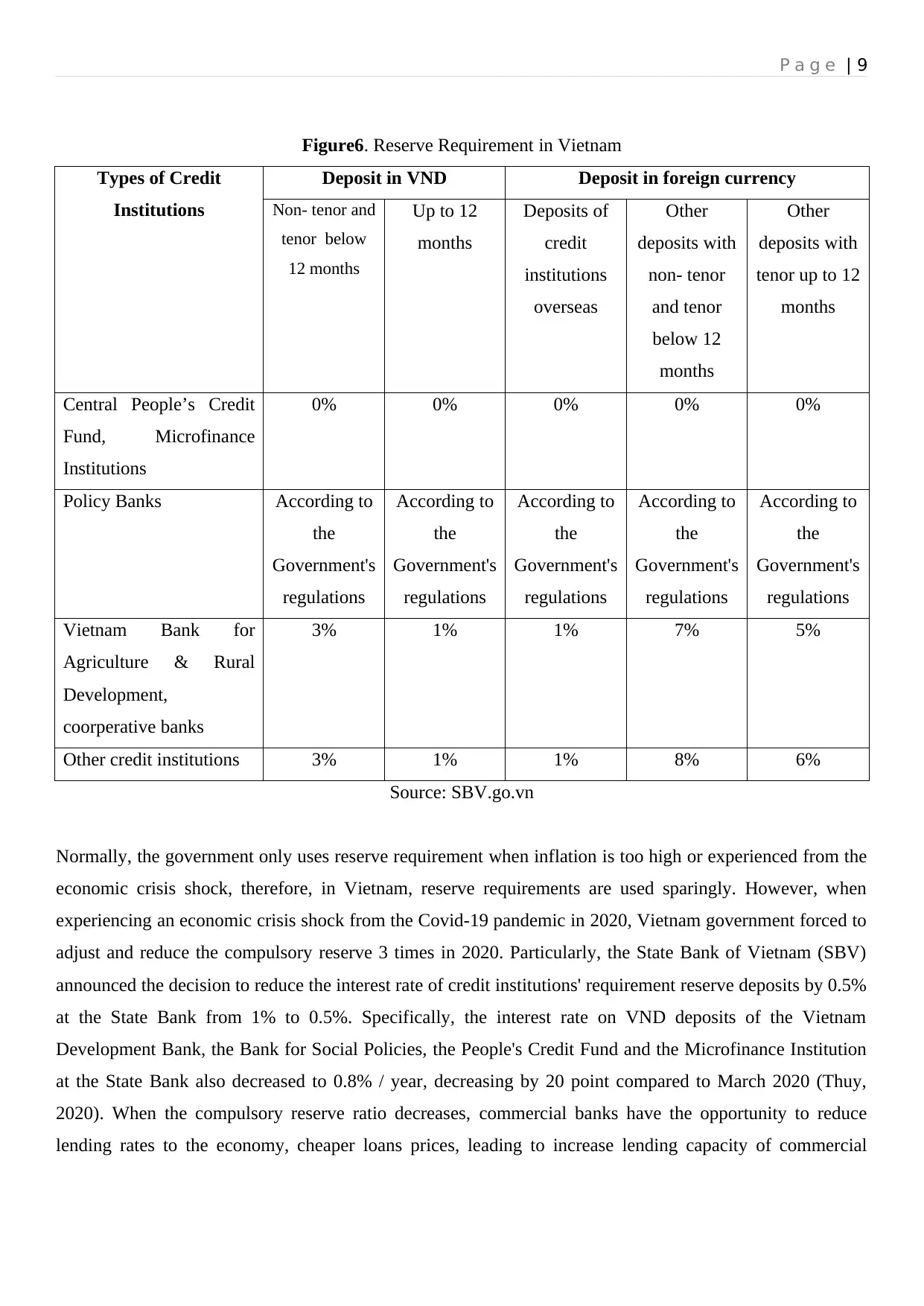

Figure6. Reserve Requirement in Vietnam

Types of Credit

Institutions

Deposit in VND Deposit in foreign currency

Non- tenor and

tenor below

12 months

Up to 12

months

Deposits of

credit

institutions

overseas

Other

deposits with

non- tenor

and tenor

below 12

months

Other

deposits with

tenor up to 12

months

Central People’s Credit

Fund, Microfinance

Institutions

0% 0% 0% 0% 0%

Policy Banks According to

the

Government's

regulations

According to

the

Government's

regulations

According to

the

Government's

regulations

According to

the

Government's

regulations

According to

the

Government's

regulations

Vietnam Bank for

Agriculture & Rural

Development,

coorperative banks

3% 1% 1% 7% 5%

Other credit institutions 3% 1% 1% 8% 6%

Source: SBV.go.vn

Normally, the government only uses reserve requirement when inflation is too high or experienced from the

economic crisis shock, therefore, in Vietnam, reserve requirements are used sparingly. However, when

experiencing an economic crisis shock from the Covid-19 pandemic in 2020, Vietnam government forced to

adjust and reduce the compulsory reserve 3 times in 2020. Particularly, the State Bank of Vietnam (SBV)

announced the decision to reduce the interest rate of credit institutions' requirement reserve deposits by 0.5%

at the State Bank from 1% to 0.5%. Specifically, the interest rate on VND deposits of the Vietnam

Development Bank, the Bank for Social Policies, the People's Credit Fund and the Microfinance Institution

at the State Bank also decreased to 0.8% / year, decreasing by 20 point compared to March 2020 (Thuy,

2020). When the compulsory reserve ratio decreases, commercial banks have the opportunity to reduce

lending rates to the economy, cheaper loans prices, leading to increase lending capacity of commercial

Figure6. Reserve Requirement in Vietnam

Types of Credit

Institutions

Deposit in VND Deposit in foreign currency

Non- tenor and

tenor below

12 months

Up to 12

months

Deposits of

credit

institutions

overseas

Other

deposits with

non- tenor

and tenor

below 12

months

Other

deposits with

tenor up to 12

months

Central People’s Credit

Fund, Microfinance

Institutions

0% 0% 0% 0% 0%

Policy Banks According to

the

Government's

regulations

According to

the

Government's

regulations

According to

the

Government's

regulations

According to

the

Government's

regulations

According to

the

Government's

regulations

Vietnam Bank for

Agriculture & Rural

Development,

coorperative banks

3% 1% 1% 7% 5%

Other credit institutions 3% 1% 1% 8% 6%

Source: SBV.go.vn

Normally, the government only uses reserve requirement when inflation is too high or experienced from the

economic crisis shock, therefore, in Vietnam, reserve requirements are used sparingly. However, when

experiencing an economic crisis shock from the Covid-19 pandemic in 2020, Vietnam government forced to

adjust and reduce the compulsory reserve 3 times in 2020. Particularly, the State Bank of Vietnam (SBV)

announced the decision to reduce the interest rate of credit institutions' requirement reserve deposits by 0.5%

at the State Bank from 1% to 0.5%. Specifically, the interest rate on VND deposits of the Vietnam

Development Bank, the Bank for Social Policies, the People's Credit Fund and the Microfinance Institution

at the State Bank also decreased to 0.8% / year, decreasing by 20 point compared to March 2020 (Thuy,

2020). When the compulsory reserve ratio decreases, commercial banks have the opportunity to reduce

lending rates to the economy, cheaper loans prices, leading to increase lending capacity of commercial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P a g e | 10

banks and accordingly the amount of money supplied increases. The impact of new decision is to limit and

mainly to reduce the pressure on budget spending this year is expected to be high due to the economic

support policies of the under the influence of Covid-19 (including tax reduction packages small and medium

enterprise income, increase public investment spending).

Open Market Operation

Open market operations (OMO) are a central bank’s buying and selling of securities in open market in

order to provide or withdraw reserves becoming the single most important monetary instrument for

controlling liquidity. When the central bank buys securities, it increases the monetary base, thereby

increasing the money supply, and vice versa. In 2020, the interest rate offered to buy valuable papers

through open market operation (OMO) also decreased from 3.0% / year to 2.5% / year in order to attract

money. Meanwhile, according to SSI Securities Company, from the beginning of the year until now the

State Bank has bought a large amount of foreign currency from commercial banks through OMO.

Specifically, the State Bank has bought about $ 2 billion, equivalent to pumping out nearly 50 trillion dong

(Trinh, 2020). Through OMO, the SBV neutralized a large amount of money in circulation, ensured liquidity

for commercial banks and curbed inflation.

Lending facilities

The facility at which banks and other depository institutions can borrow reserves from Central Banks. In

Vietnam, refinancing rate, interest rate and discount rate are the facilities that be used. Recently, the

SBV has actively used both the refinance and discount rates in the process of loosening monetary policy. In

October, the SBV issued Decision No.1728 QD announced that continue reduce the refinancing and

discount interest rate, specifically, the refinancing rate decreased from 4.5% to 4.0%, the rediscount rate

decreased from 3.0% to 2.5% (Son, 2020). This action aims to create rationality among monetary policy

tools, partially reduce operating costs for commercial banks so that commercial banks lower lending interest

rates, support businesses to maintain and expand production, encourage export, stabilize the macro-

economy, and ensure social security.

b. Intermediate Target

In Vietnam, Monetary base is used as Operational objective. The use of monetary base improves the role

of Vietnam Central bank in controlling the supply of money, credit growth thereby helping to stabilize

inflation in the country, and have opportunities to develop the market.

banks and accordingly the amount of money supplied increases. The impact of new decision is to limit and

mainly to reduce the pressure on budget spending this year is expected to be high due to the economic

support policies of the under the influence of Covid-19 (including tax reduction packages small and medium

enterprise income, increase public investment spending).

Open Market Operation

Open market operations (OMO) are a central bank’s buying and selling of securities in open market in

order to provide or withdraw reserves becoming the single most important monetary instrument for

controlling liquidity. When the central bank buys securities, it increases the monetary base, thereby

increasing the money supply, and vice versa. In 2020, the interest rate offered to buy valuable papers

through open market operation (OMO) also decreased from 3.0% / year to 2.5% / year in order to attract

money. Meanwhile, according to SSI Securities Company, from the beginning of the year until now the

State Bank has bought a large amount of foreign currency from commercial banks through OMO.

Specifically, the State Bank has bought about $ 2 billion, equivalent to pumping out nearly 50 trillion dong

(Trinh, 2020). Through OMO, the SBV neutralized a large amount of money in circulation, ensured liquidity

for commercial banks and curbed inflation.

Lending facilities

The facility at which banks and other depository institutions can borrow reserves from Central Banks. In

Vietnam, refinancing rate, interest rate and discount rate are the facilities that be used. Recently, the

SBV has actively used both the refinance and discount rates in the process of loosening monetary policy. In

October, the SBV issued Decision No.1728 QD announced that continue reduce the refinancing and

discount interest rate, specifically, the refinancing rate decreased from 4.5% to 4.0%, the rediscount rate

decreased from 3.0% to 2.5% (Son, 2020). This action aims to create rationality among monetary policy

tools, partially reduce operating costs for commercial banks so that commercial banks lower lending interest

rates, support businesses to maintain and expand production, encourage export, stabilize the macro-

economy, and ensure social security.

b. Intermediate Target

In Vietnam, Monetary base is used as Operational objective. The use of monetary base improves the role

of Vietnam Central bank in controlling the supply of money, credit growth thereby helping to stabilize

inflation in the country, and have opportunities to develop the market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P a g e | 11

Money supply (M2)

Since the Central bank of Vietnam applied monetary base in operation, the money supply is important to

analyse. In order to achieve the monetary policy objective, the State Bank has determined the oriented target

for M2 as well as control credit growth to ensure liquidity for the economy, and control inflation via

management of the monetary policy tools. As said above, in 2020, the Reserve requirement, Discount and

financing rate in Vietnam was reduced, leading to the lowers the amount of cash that banks are required to

hold in reserves, enabling them to make more loans to consumers and businesses. As a results, the money

supply of nation tends to increase and therefore, expanding the economy. Although the increased of money

supply compare to 2019 was lower, however, SBV is still implementing the proposed measures well. The

fact that, in the first ten months of 2020, broad money growth measured by covering covers cash in

circulation and all deposits, reached to 11% and still remained as expected (increase 11%-13%) (Trinh,

2020)

Figure7. Broad money growth (annual %) from 2012 to 2019

Source: Data World Bank

Money supply in 2020

Money supply (M2)

Since the Central bank of Vietnam applied monetary base in operation, the money supply is important to

analyse. In order to achieve the monetary policy objective, the State Bank has determined the oriented target

for M2 as well as control credit growth to ensure liquidity for the economy, and control inflation via

management of the monetary policy tools. As said above, in 2020, the Reserve requirement, Discount and

financing rate in Vietnam was reduced, leading to the lowers the amount of cash that banks are required to

hold in reserves, enabling them to make more loans to consumers and businesses. As a results, the money

supply of nation tends to increase and therefore, expanding the economy. Although the increased of money

supply compare to 2019 was lower, however, SBV is still implementing the proposed measures well. The

fact that, in the first ten months of 2020, broad money growth measured by covering covers cash in

circulation and all deposits, reached to 11% and still remained as expected (increase 11%-13%) (Trinh,

2020)

Figure7. Broad money growth (annual %) from 2012 to 2019

Source: Data World Bank

Money supply in 2020

P a g e | 12

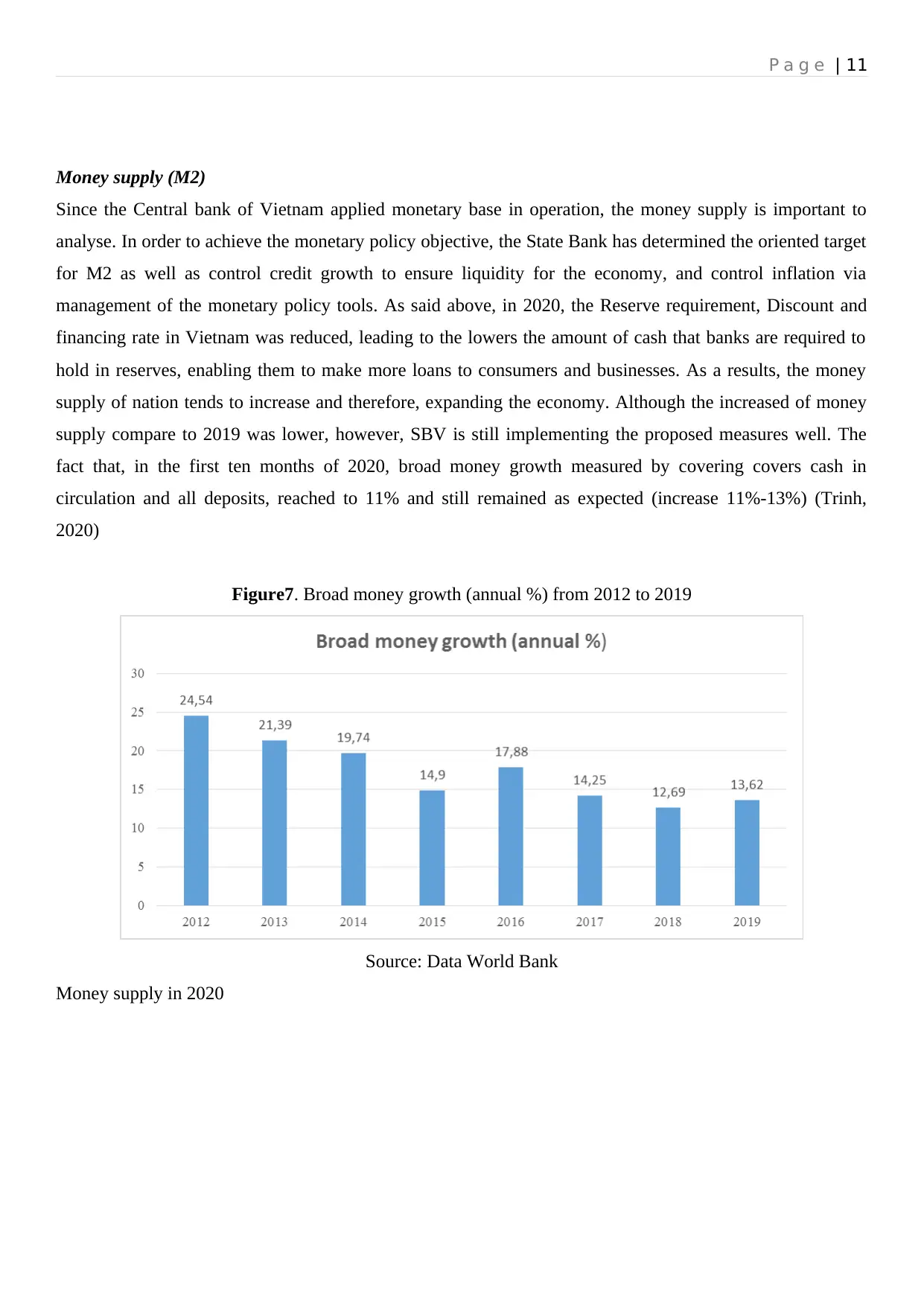

Source: KB Securities Vietnam

c. Final Goals

In general, SBV seem to have succeeded in achieving the economic growth and inflation targets in this

period. In fact, SBV carefully monitored the lending facilities channel in accordance with the key

instruments for the SBV to maintain price stability as well as monitoring the performance of the CPI level.

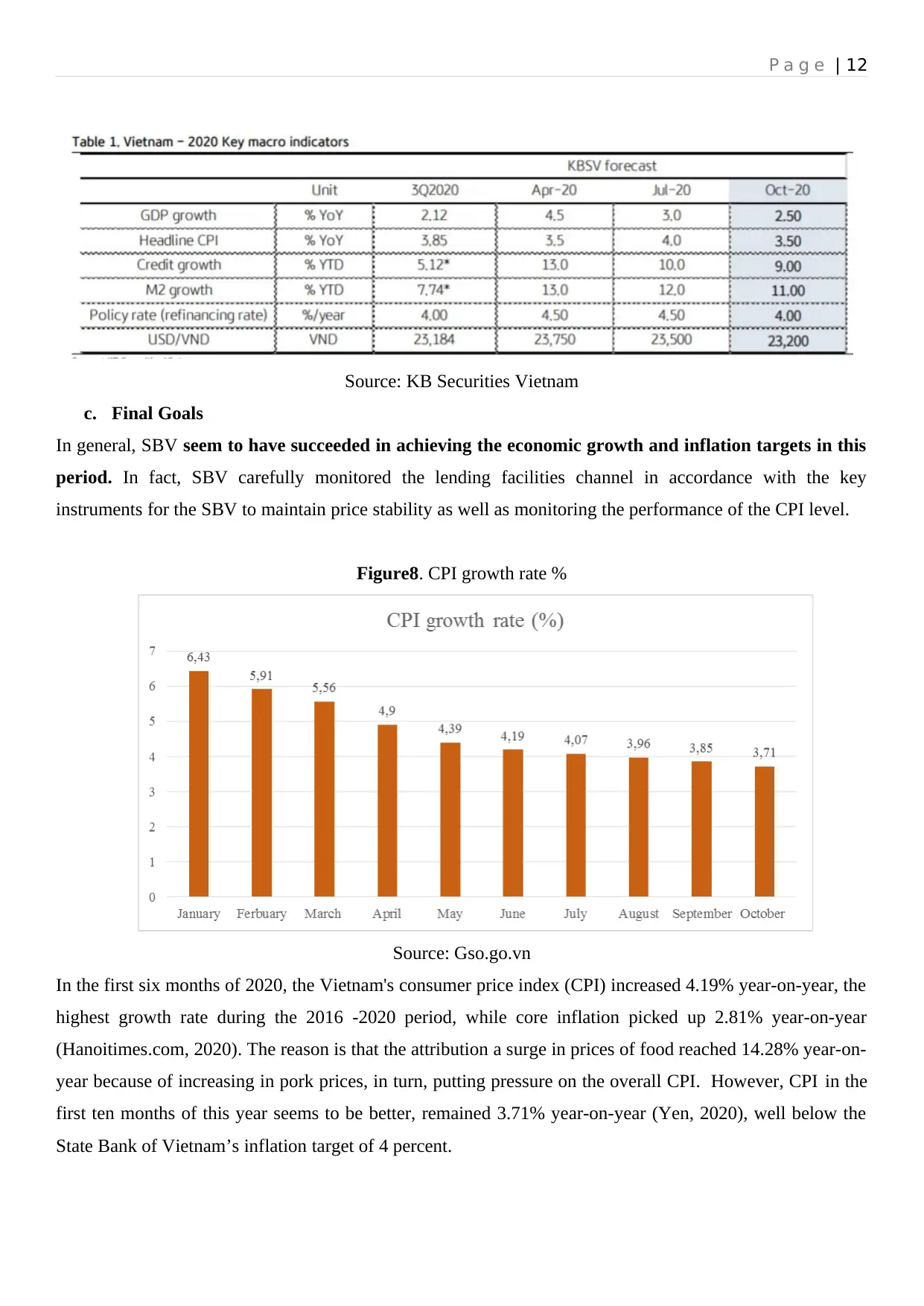

Figure8. CPI growth rate %

Source: Gso.go.vn

In the first six months of 2020, the Vietnam's consumer price index (CPI) increased 4.19% year-on-year, the

highest growth rate during the 2016 -2020 period, while core inflation picked up 2.81% year-on-year

(Hanoitimes.com, 2020). The reason is that the attribution a surge in prices of food reached 14.28% year-on-

year because of increasing in pork prices, in turn, putting pressure on the overall CPI. However, CPI in the

first ten months of this year seems to be better, remained 3.71% year-on-year (Yen, 2020), well below the

State Bank of Vietnam’s inflation target of 4 percent.

Source: KB Securities Vietnam

c. Final Goals

In general, SBV seem to have succeeded in achieving the economic growth and inflation targets in this

period. In fact, SBV carefully monitored the lending facilities channel in accordance with the key

instruments for the SBV to maintain price stability as well as monitoring the performance of the CPI level.

Figure8. CPI growth rate %

Source: Gso.go.vn

In the first six months of 2020, the Vietnam's consumer price index (CPI) increased 4.19% year-on-year, the

highest growth rate during the 2016 -2020 period, while core inflation picked up 2.81% year-on-year

(Hanoitimes.com, 2020). The reason is that the attribution a surge in prices of food reached 14.28% year-on-

year because of increasing in pork prices, in turn, putting pressure on the overall CPI. However, CPI in the

first ten months of this year seems to be better, remained 3.71% year-on-year (Yen, 2020), well below the

State Bank of Vietnam’s inflation target of 4 percent.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.