ECOM058 Applied Econometrics Assignment: UK Money Demand Analysis

VerifiedAdded on 2023/02/01

|34

|7312

|97

Homework Assignment

AI Summary

This assignment analyzes the money demand function in the UK, examining both short-run and long-run dynamics. The solution begins with estimating a static money demand function using inflation rate, real GDP, and interest rate as independent variables. Autocorrelation tests are performed to assess model robustness. The analysis then shifts to the long run, acknowledging the challenges of directly observing the money demand function and employing instrumental variables to address potential endogeneity issues. The solution includes unit root tests using the Augmented Dickey-Fuller test and cointegration analysis using the Engel-Granger test. The document provides detailed regression results, interpretations of coefficients, and statistical tests, including F-tests and LM tests for autocorrelation. The assignment also discusses the impact of autocorrelation on OLS estimators and the implications for policy formulation.

Running head: APPLIED ECONOMETRICS

Applied Econometrics

Name of the Student

Name of the University

Course ID

Applied Econometrics

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1APPLIED ECONOMETRICS

Executive Summary

The paper aims to analyze the money demand function both in the short run and in the long run.

The static money demand function has been estimated taking inflation rate, real GDP and interest

rate. In order to analyze robustness of the model autocorrelation test has been performed for

examining presence of serial correlation in the model. Condition in the short run however is

different from that in the long run. In the long run, it is assumed that money demand function is

not directly observable and difference between observed money supply tends to adjust towards

the expected difference in money supply having certain speed of adjustment. In the long run

inclusion of lagged dependent variables may result in the problem of endogeneity where

independent variables are found to be related with the error term. In order to eliminate the

problem of endogeneity the technique of instrumental variables is used through the estimation

method of two stage least square. Each of the series has been tested for unit root by employing

the Augmenyed Dicky Fuller test. Finally, Engel Granger test has been performed to examine co-

integration among the variables. The money demand function and its associate determinants

provide useful implication for policy formulation.

Executive Summary

The paper aims to analyze the money demand function both in the short run and in the long run.

The static money demand function has been estimated taking inflation rate, real GDP and interest

rate. In order to analyze robustness of the model autocorrelation test has been performed for

examining presence of serial correlation in the model. Condition in the short run however is

different from that in the long run. In the long run, it is assumed that money demand function is

not directly observable and difference between observed money supply tends to adjust towards

the expected difference in money supply having certain speed of adjustment. In the long run

inclusion of lagged dependent variables may result in the problem of endogeneity where

independent variables are found to be related with the error term. In order to eliminate the

problem of endogeneity the technique of instrumental variables is used through the estimation

method of two stage least square. Each of the series has been tested for unit root by employing

the Augmenyed Dicky Fuller test. Finally, Engel Granger test has been performed to examine co-

integration among the variables. The money demand function and its associate determinants

provide useful implication for policy formulation.

2APPLIED ECONOMETRICS

Table of Contents

Question 1........................................................................................................................................4

Question 2........................................................................................................................................6

Question a....................................................................................................................................6

Question b....................................................................................................................................7

Question c....................................................................................................................................8

Question 3........................................................................................................................................8

Question a....................................................................................................................................8

Question b....................................................................................................................................9

Question 4......................................................................................................................................10

Question a..................................................................................................................................10

Question b..................................................................................................................................12

Question c..................................................................................................................................12

Question 5......................................................................................................................................13

Question a..................................................................................................................................13

Question b..................................................................................................................................13

Question c..................................................................................................................................13

Question d..................................................................................................................................13

Question 6......................................................................................................................................14

Question 7......................................................................................................................................15

Table of Contents

Question 1........................................................................................................................................4

Question 2........................................................................................................................................6

Question a....................................................................................................................................6

Question b....................................................................................................................................7

Question c....................................................................................................................................8

Question 3........................................................................................................................................8

Question a....................................................................................................................................8

Question b....................................................................................................................................9

Question 4......................................................................................................................................10

Question a..................................................................................................................................10

Question b..................................................................................................................................12

Question c..................................................................................................................................12

Question 5......................................................................................................................................13

Question a..................................................................................................................................13

Question b..................................................................................................................................13

Question c..................................................................................................................................13

Question d..................................................................................................................................13

Question 6......................................................................................................................................14

Question 7......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3APPLIED ECONOMETRICS

Question a..................................................................................................................................15

Question b..................................................................................................................................15

Question c..................................................................................................................................15

Question 8......................................................................................................................................15

Question a..................................................................................................................................15

Question b..................................................................................................................................16

Question c..................................................................................................................................16

Question 9......................................................................................................................................16

Question a..................................................................................................................................16

Question b..................................................................................................................................18

Question c..................................................................................................................................18

Question 10....................................................................................................................................18

References and Bibliography.........................................................................................................20

Appendix........................................................................................................................................22

Question a..................................................................................................................................15

Question b..................................................................................................................................15

Question c..................................................................................................................................15

Question 8......................................................................................................................................15

Question a..................................................................................................................................15

Question b..................................................................................................................................16

Question c..................................................................................................................................16

Question 9......................................................................................................................................16

Question a..................................................................................................................................16

Question b..................................................................................................................................18

Question c..................................................................................................................................18

Question 10....................................................................................................................................18

References and Bibliography.........................................................................................................20

Appendix........................................................................................................................................22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4APPLIED ECONOMETRICS

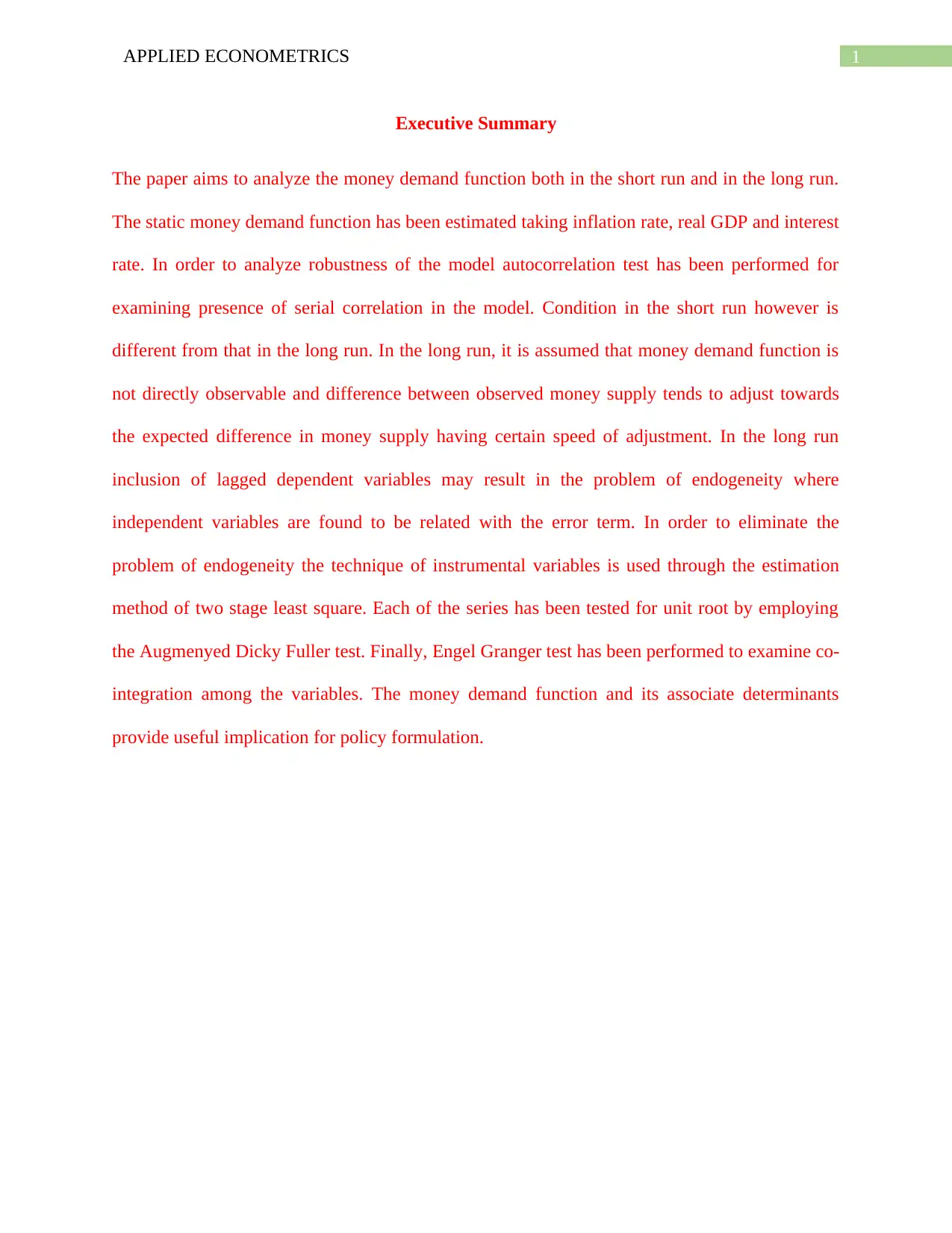

Question 1

Figure 1: Dynamic trend of inflation rate

The inflation series is highly volatile. The series initially increases, reaches peak and then

again declines. Most of the times, inflation rate varies between 0.01 to 0.02 percent.

Question 1

Figure 1: Dynamic trend of inflation rate

The inflation series is highly volatile. The series initially increases, reaches peak and then

again declines. Most of the times, inflation rate varies between 0.01 to 0.02 percent.

5APPLIED ECONOMETRICS

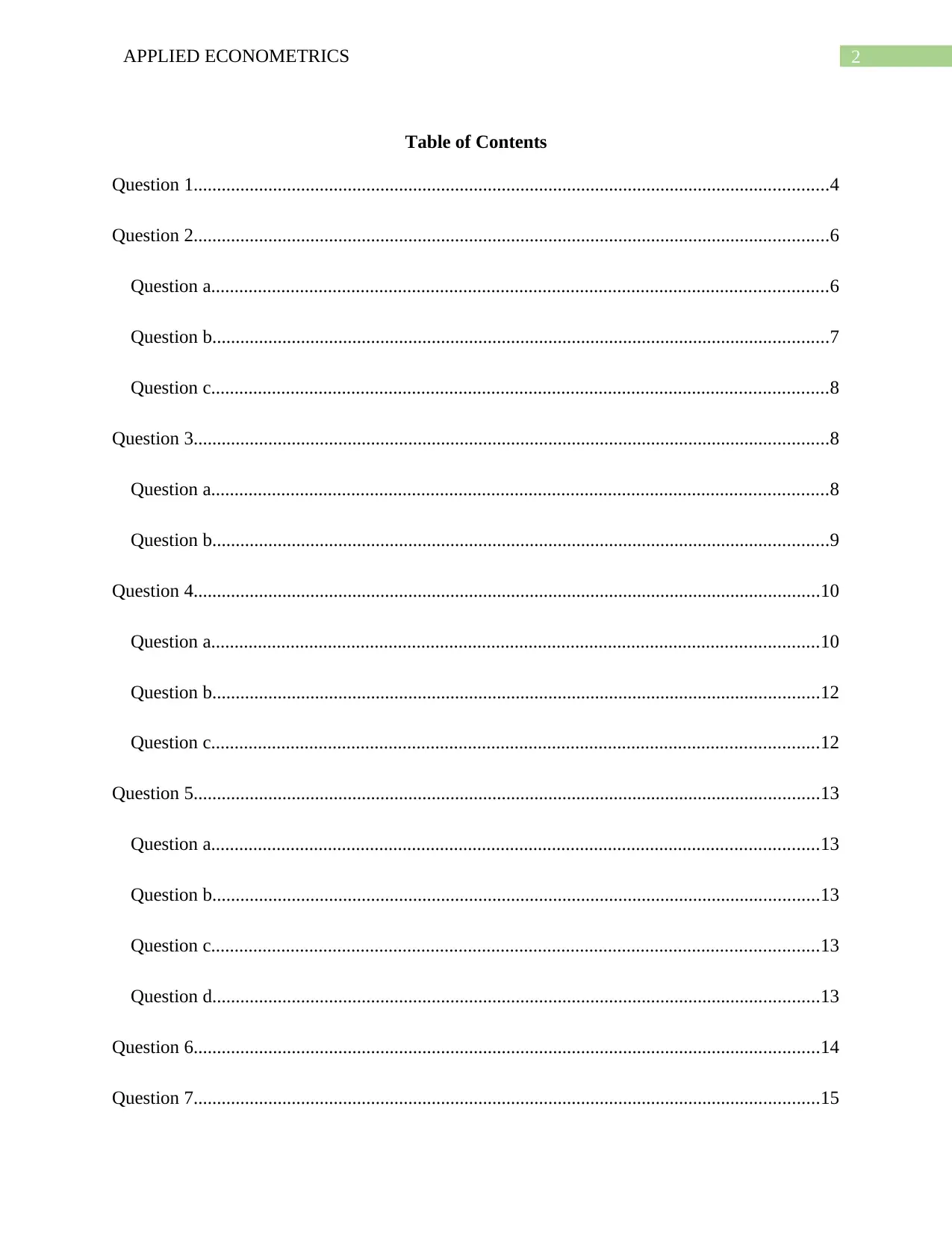

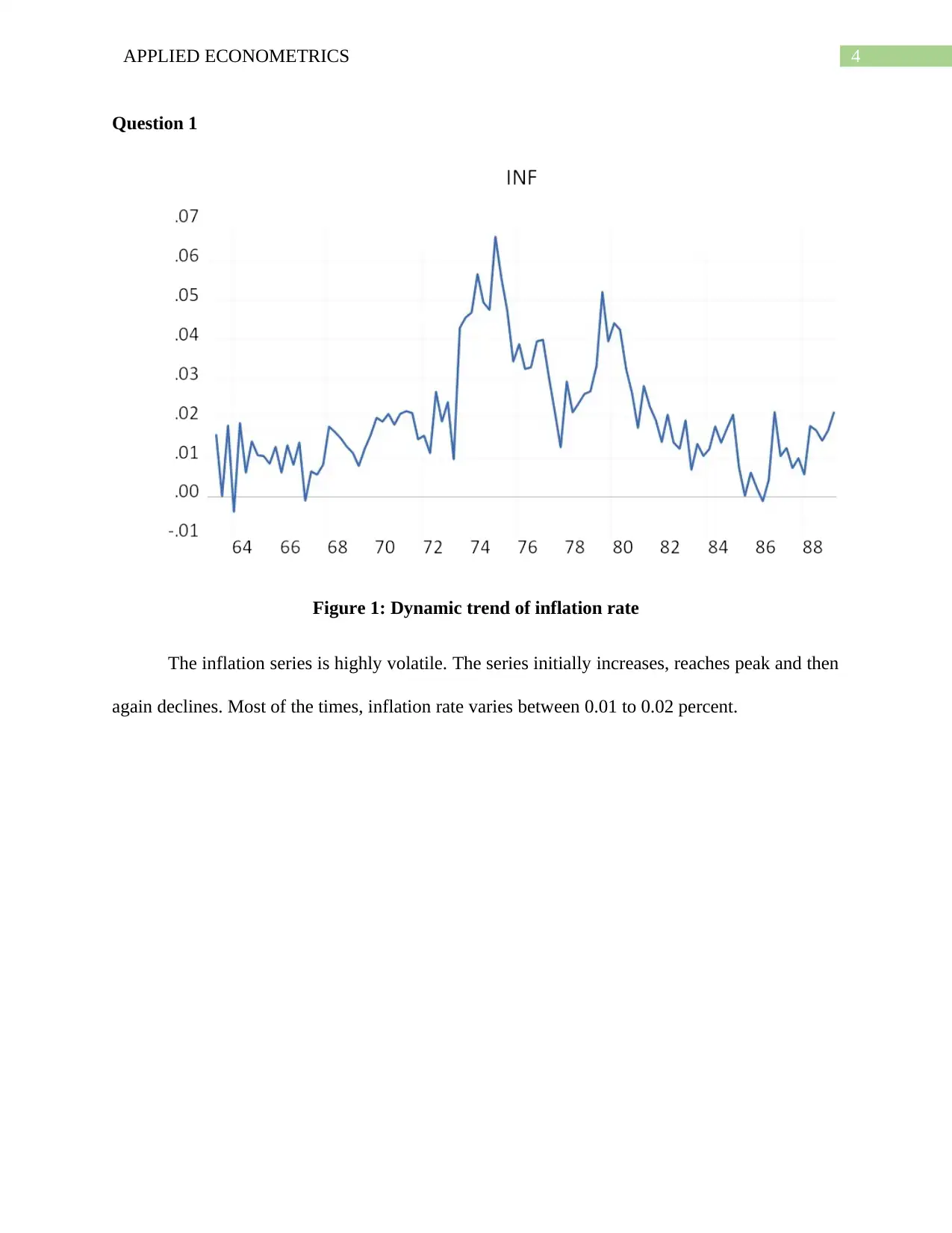

Figure 2: Dynamic trend in interest rate

Like inflation series, the series of interest rate also shows dynamic fluctuating trend.

Figure 3: Dynamic trend in real GDP

Figure 2: Dynamic trend in interest rate

Like inflation series, the series of interest rate also shows dynamic fluctuating trend.

Figure 3: Dynamic trend in real GDP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6APPLIED ECONOMETRICS

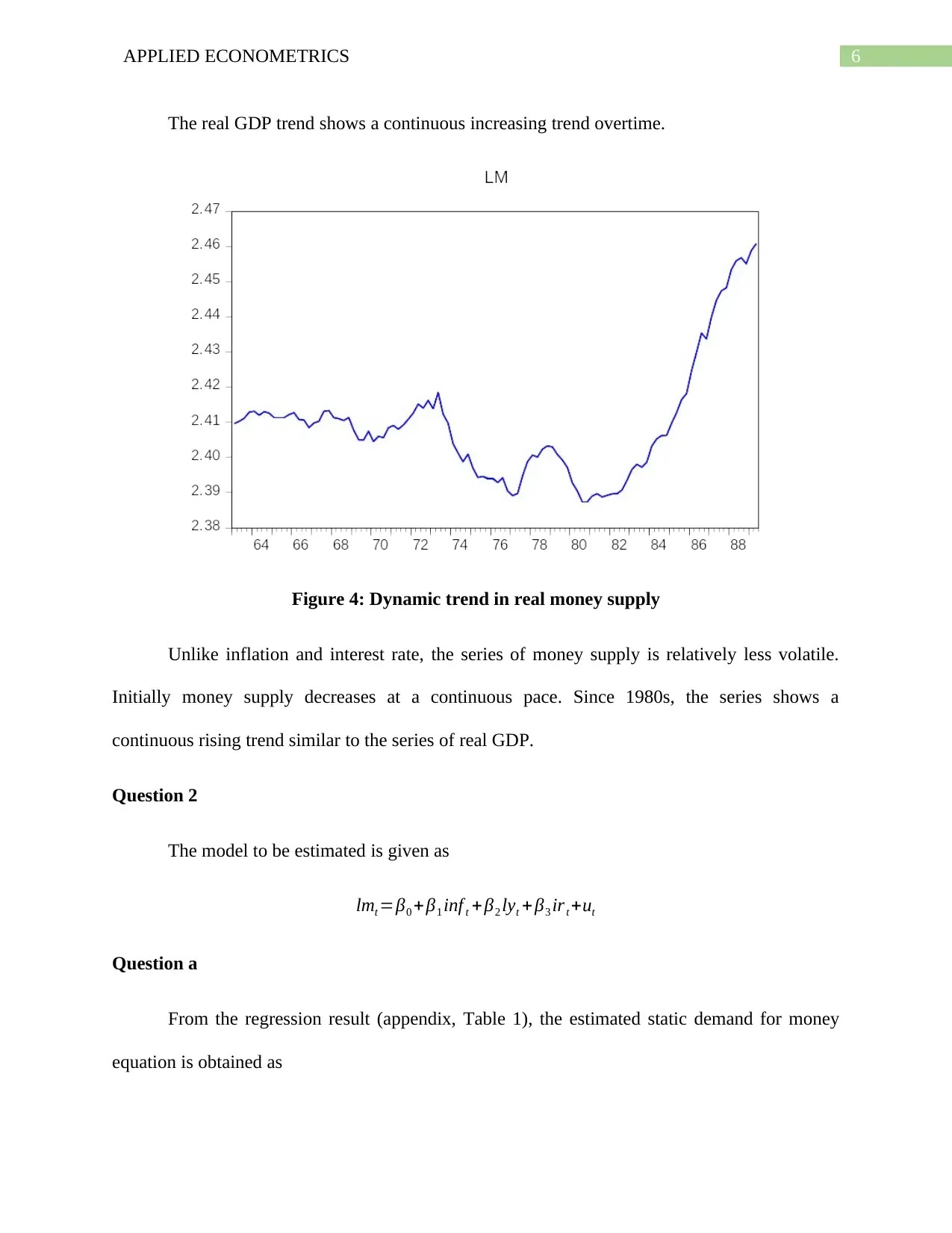

The real GDP trend shows a continuous increasing trend overtime.

Figure 4: Dynamic trend in real money supply

Unlike inflation and interest rate, the series of money supply is relatively less volatile.

Initially money supply decreases at a continuous pace. Since 1980s, the series shows a

continuous rising trend similar to the series of real GDP.

Question 2

The model to be estimated is given as

lmt =β0 +β1 inf t +β2 lyt +β3 irt +ut

Question a

From the regression result (appendix, Table 1), the estimated static demand for money

equation is obtained as

The real GDP trend shows a continuous increasing trend overtime.

Figure 4: Dynamic trend in real money supply

Unlike inflation and interest rate, the series of money supply is relatively less volatile.

Initially money supply decreases at a continuous pace. Since 1980s, the series shows a

continuous rising trend similar to the series of real GDP.

Question 2

The model to be estimated is given as

lmt =β0 +β1 inf t +β2 lyt +β3 irt +ut

Question a

From the regression result (appendix, Table 1), the estimated static demand for money

equation is obtained as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7APPLIED ECONOMETRICS

lmt =1.423214+0.079303inf t +0.0413525 lyt −0.361611 irt

Question b

From the estimated static demand equation, the constant is obtained as 1.423214. The

constant implies slope of the money demand curve. That is all other variables influencing money

demand and such as inflation, real GDP and interest rate are zero, then money demand in the

economy is 1.423214. The coefficient associated with inflation rate is 0.0799303. The positive

value of inflation coefficient means that inflation has a positive relation with money demand

(Johnson 2017, pp. 121-128). That is higher the inflation, higher is the money demand and vice-

versa. More precisely, for 10 percent increase in inflation rate, log of real money balance

increases by 0.7 percent. This is consistent with expectation because during high inflation people

require more money to purchase goods and services increasing demand for money. For real

GDP, the estimated coefficient is 0.0413525. This implies real GDP is again positively

associated with money supply. From the coefficient estimate, it can be said that 10 percent

increase in log real GDP increases money demand by 0.04 percent. Increase in GDP thus

increase money supply and vice versa. A higher GDP implies a higher average income for

people. With increases in income people demand more money. The finding thus is consistent

with expectation. In case of interest rate, the associated coefficient is - -0.361611. The negative

coefficient suggests an inverse association with money demand and interest rate. That is money

demand increase with a decrease in interest rate. This is expected as interest rate is the cost of

holding money and hence is inversely associated with demand for money (Gan 2019).

lmt =1.423214+0.079303inf t +0.0413525 lyt −0.361611 irt

Question b

From the estimated static demand equation, the constant is obtained as 1.423214. The

constant implies slope of the money demand curve. That is all other variables influencing money

demand and such as inflation, real GDP and interest rate are zero, then money demand in the

economy is 1.423214. The coefficient associated with inflation rate is 0.0799303. The positive

value of inflation coefficient means that inflation has a positive relation with money demand

(Johnson 2017, pp. 121-128). That is higher the inflation, higher is the money demand and vice-

versa. More precisely, for 10 percent increase in inflation rate, log of real money balance

increases by 0.7 percent. This is consistent with expectation because during high inflation people

require more money to purchase goods and services increasing demand for money. For real

GDP, the estimated coefficient is 0.0413525. This implies real GDP is again positively

associated with money supply. From the coefficient estimate, it can be said that 10 percent

increase in log real GDP increases money demand by 0.04 percent. Increase in GDP thus

increase money supply and vice versa. A higher GDP implies a higher average income for

people. With increases in income people demand more money. The finding thus is consistent

with expectation. In case of interest rate, the associated coefficient is - -0.361611. The negative

coefficient suggests an inverse association with money demand and interest rate. That is money

demand increase with a decrease in interest rate. This is expected as interest rate is the cost of

holding money and hence is inversely associated with demand for money (Gan 2019).

8APPLIED ECONOMETRICS

Question c

Computed ‘t’ value for inflation rate 0.8764. The critical t value at 5% level of

significance and 101 degrees of freedom is 1.9837. As the absolute value of computed t is less

than the critical t, null hypothesis for no significant relation between inflation and money

demand is accepted. The independent variable, inflation thus is not statistically significant.

Associated p value for the coefficient is 0.3829. The p value exceeds the value of 5%

significance level again implying acceptance of null hypothesis of no significant relation

between dependent and independent variable. The proposed association between inflation and

money demand thus is not statistically significant. The proposed association between real GDP

and money demand thus is statistically significant as the computed t exceeds the critical t and p

value is smaller than the significance level. In case of interest rate a statistically significant but

negative association is obtained between money demand and interest rate.

Question 3

Question a

The joint significance test for the regression model can be performed using the F test. The

null and alternative hypotheses for the test are given as follows.

Null hypothesis: β1 = β2= β3 = 0

Alternative hypothesis: At least any of the β’s is not equal to zero.

The computed F value of the model is 75.07595. The critical F value at 5 percent level of

significance and (3, 101) degrees of freedom is 2.6946. The computed F value exceeds the

critical F value at 5 percent level of significance implying rejection of null hypothesis stating all

Question c

Computed ‘t’ value for inflation rate 0.8764. The critical t value at 5% level of

significance and 101 degrees of freedom is 1.9837. As the absolute value of computed t is less

than the critical t, null hypothesis for no significant relation between inflation and money

demand is accepted. The independent variable, inflation thus is not statistically significant.

Associated p value for the coefficient is 0.3829. The p value exceeds the value of 5%

significance level again implying acceptance of null hypothesis of no significant relation

between dependent and independent variable. The proposed association between inflation and

money demand thus is not statistically significant. The proposed association between real GDP

and money demand thus is statistically significant as the computed t exceeds the critical t and p

value is smaller than the significance level. In case of interest rate a statistically significant but

negative association is obtained between money demand and interest rate.

Question 3

Question a

The joint significance test for the regression model can be performed using the F test. The

null and alternative hypotheses for the test are given as follows.

Null hypothesis: β1 = β2= β3 = 0

Alternative hypothesis: At least any of the β’s is not equal to zero.

The computed F value of the model is 75.07595. The critical F value at 5 percent level of

significance and (3, 101) degrees of freedom is 2.6946. The computed F value exceeds the

critical F value at 5 percent level of significance implying rejection of null hypothesis stating all

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9APPLIED ECONOMETRICS

coefficients are zero. This can therefore be said that at least one of the coefficient is significantly

different from zero and hence, the model is jointly significant. The result is again supported by

the p value test. Associated p value for the F statistics is 0.0000. As the p value is less than

significance value of 0.05, the null hypothesis stating that the overall model is insignificant is

rejected. The independent variables in the model thus are jointly significant.

Question b

In multiple regression model adjusted R square is used as a measure of goodness of fit.

The obtained value of adjusted R square is 0.6812. The value indicates that inflation, real GDP

and interest rate can together explain 68 percent variation of the dependent variables. As the

independent variables account a considerably higher variability of the dependent variable, the

model is a good fit model.

coefficients are zero. This can therefore be said that at least one of the coefficient is significantly

different from zero and hence, the model is jointly significant. The result is again supported by

the p value test. Associated p value for the F statistics is 0.0000. As the p value is less than

significance value of 0.05, the null hypothesis stating that the overall model is insignificant is

rejected. The independent variables in the model thus are jointly significant.

Question b

In multiple regression model adjusted R square is used as a measure of goodness of fit.

The obtained value of adjusted R square is 0.6812. The value indicates that inflation, real GDP

and interest rate can together explain 68 percent variation of the dependent variables. As the

independent variables account a considerably higher variability of the dependent variable, the

model is a good fit model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10APPLIED ECONOMETRICS

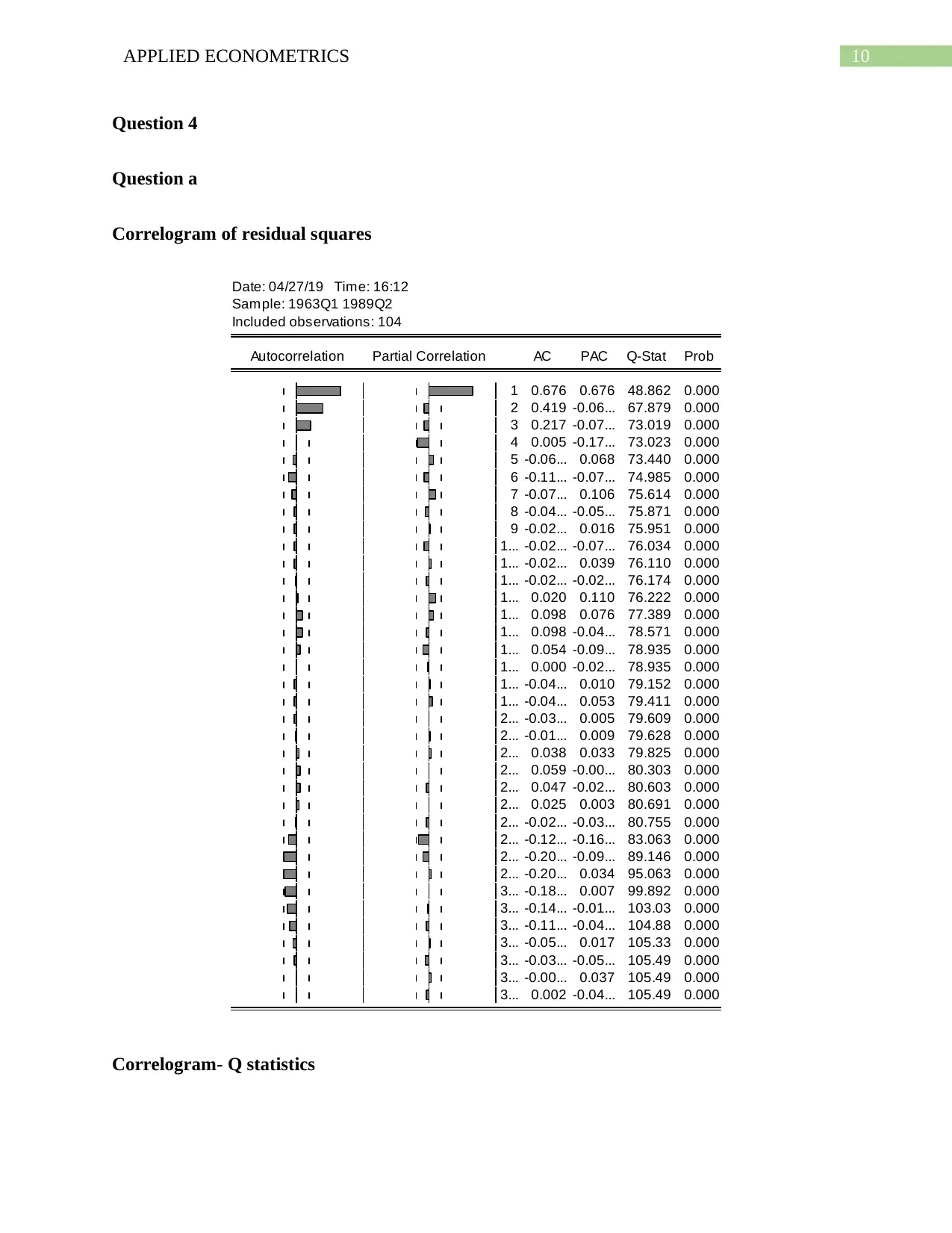

Question 4

Question a

Correlogram of residual squares

Date: 04/27/19 Time: 16:12

Sample: 1963Q1 1989Q2

Included observations: 104

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

1 0.676 0.676 48.862 0.000

2 0.419 -0.06... 67.879 0.000

3 0.217 -0.07... 73.019 0.000

4 0.005 -0.17... 73.023 0.000

5 -0.06... 0.068 73.440 0.000

6 -0.11... -0.07... 74.985 0.000

7 -0.07... 0.106 75.614 0.000

8 -0.04... -0.05... 75.871 0.000

9 -0.02... 0.016 75.951 0.000

1... -0.02... -0.07... 76.034 0.000

1... -0.02... 0.039 76.110 0.000

1... -0.02... -0.02... 76.174 0.000

1... 0.020 0.110 76.222 0.000

1... 0.098 0.076 77.389 0.000

1... 0.098 -0.04... 78.571 0.000

1... 0.054 -0.09... 78.935 0.000

1... 0.000 -0.02... 78.935 0.000

1... -0.04... 0.010 79.152 0.000

1... -0.04... 0.053 79.411 0.000

2... -0.03... 0.005 79.609 0.000

2... -0.01... 0.009 79.628 0.000

2... 0.038 0.033 79.825 0.000

2... 0.059 -0.00... 80.303 0.000

2... 0.047 -0.02... 80.603 0.000

2... 0.025 0.003 80.691 0.000

2... -0.02... -0.03... 80.755 0.000

2... -0.12... -0.16... 83.063 0.000

2... -0.20... -0.09... 89.146 0.000

2... -0.20... 0.034 95.063 0.000

3... -0.18... 0.007 99.892 0.000

3... -0.14... -0.01... 103.03 0.000

3... -0.11... -0.04... 104.88 0.000

3... -0.05... 0.017 105.33 0.000

3... -0.03... -0.05... 105.49 0.000

3... -0.00... 0.037 105.49 0.000

3... 0.002 -0.04... 105.49 0.000

Correlogram- Q statistics

Question 4

Question a

Correlogram of residual squares

Date: 04/27/19 Time: 16:12

Sample: 1963Q1 1989Q2

Included observations: 104

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

1 0.676 0.676 48.862 0.000

2 0.419 -0.06... 67.879 0.000

3 0.217 -0.07... 73.019 0.000

4 0.005 -0.17... 73.023 0.000

5 -0.06... 0.068 73.440 0.000

6 -0.11... -0.07... 74.985 0.000

7 -0.07... 0.106 75.614 0.000

8 -0.04... -0.05... 75.871 0.000

9 -0.02... 0.016 75.951 0.000

1... -0.02... -0.07... 76.034 0.000

1... -0.02... 0.039 76.110 0.000

1... -0.02... -0.02... 76.174 0.000

1... 0.020 0.110 76.222 0.000

1... 0.098 0.076 77.389 0.000

1... 0.098 -0.04... 78.571 0.000

1... 0.054 -0.09... 78.935 0.000

1... 0.000 -0.02... 78.935 0.000

1... -0.04... 0.010 79.152 0.000

1... -0.04... 0.053 79.411 0.000

2... -0.03... 0.005 79.609 0.000

2... -0.01... 0.009 79.628 0.000

2... 0.038 0.033 79.825 0.000

2... 0.059 -0.00... 80.303 0.000

2... 0.047 -0.02... 80.603 0.000

2... 0.025 0.003 80.691 0.000

2... -0.02... -0.03... 80.755 0.000

2... -0.12... -0.16... 83.063 0.000

2... -0.20... -0.09... 89.146 0.000

2... -0.20... 0.034 95.063 0.000

3... -0.18... 0.007 99.892 0.000

3... -0.14... -0.01... 103.03 0.000

3... -0.11... -0.04... 104.88 0.000

3... -0.05... 0.017 105.33 0.000

3... -0.03... -0.05... 105.49 0.000

3... -0.00... 0.037 105.49 0.000

3... 0.002 -0.04... 105.49 0.000

Correlogram- Q statistics

11APPLIED ECONOMETRICS

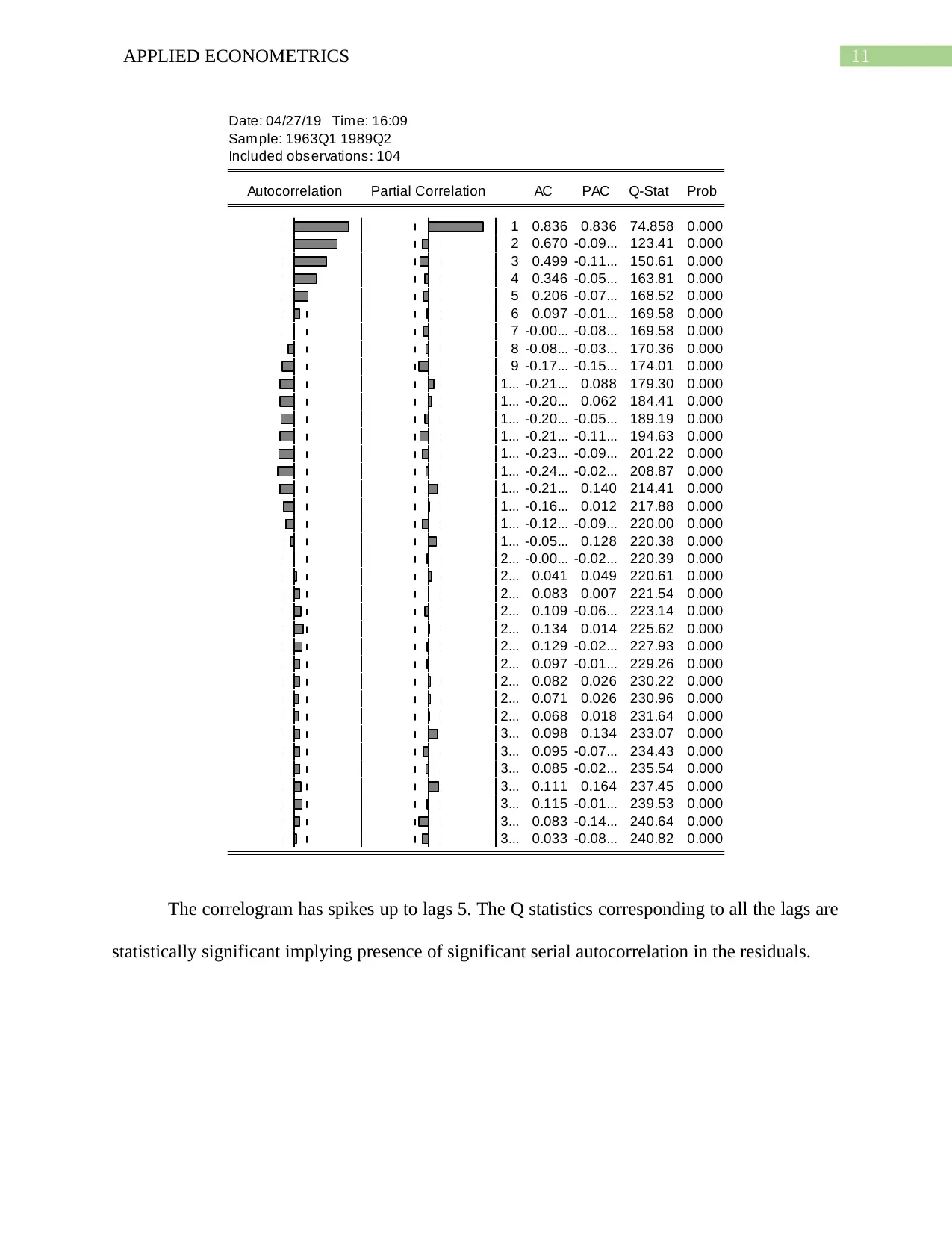

Date: 04/27/19 Time: 16:09

Sample: 1963Q1 1989Q2

Included observations: 104

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

1 0.836 0.836 74.858 0.000

2 0.670 -0.09... 123.41 0.000

3 0.499 -0.11... 150.61 0.000

4 0.346 -0.05... 163.81 0.000

5 0.206 -0.07... 168.52 0.000

6 0.097 -0.01... 169.58 0.000

7 -0.00... -0.08... 169.58 0.000

8 -0.08... -0.03... 170.36 0.000

9 -0.17... -0.15... 174.01 0.000

1... -0.21... 0.088 179.30 0.000

1... -0.20... 0.062 184.41 0.000

1... -0.20... -0.05... 189.19 0.000

1... -0.21... -0.11... 194.63 0.000

1... -0.23... -0.09... 201.22 0.000

1... -0.24... -0.02... 208.87 0.000

1... -0.21... 0.140 214.41 0.000

1... -0.16... 0.012 217.88 0.000

1... -0.12... -0.09... 220.00 0.000

1... -0.05... 0.128 220.38 0.000

2... -0.00... -0.02... 220.39 0.000

2... 0.041 0.049 220.61 0.000

2... 0.083 0.007 221.54 0.000

2... 0.109 -0.06... 223.14 0.000

2... 0.134 0.014 225.62 0.000

2... 0.129 -0.02... 227.93 0.000

2... 0.097 -0.01... 229.26 0.000

2... 0.082 0.026 230.22 0.000

2... 0.071 0.026 230.96 0.000

2... 0.068 0.018 231.64 0.000

3... 0.098 0.134 233.07 0.000

3... 0.095 -0.07... 234.43 0.000

3... 0.085 -0.02... 235.54 0.000

3... 0.111 0.164 237.45 0.000

3... 0.115 -0.01... 239.53 0.000

3... 0.083 -0.14... 240.64 0.000

3... 0.033 -0.08... 240.82 0.000

The correlogram has spikes up to lags 5. The Q statistics corresponding to all the lags are

statistically significant implying presence of significant serial autocorrelation in the residuals.

Date: 04/27/19 Time: 16:09

Sample: 1963Q1 1989Q2

Included observations: 104

Autocorrelation Partial Correlation AC PAC Q-Stat Prob

1 0.836 0.836 74.858 0.000

2 0.670 -0.09... 123.41 0.000

3 0.499 -0.11... 150.61 0.000

4 0.346 -0.05... 163.81 0.000

5 0.206 -0.07... 168.52 0.000

6 0.097 -0.01... 169.58 0.000

7 -0.00... -0.08... 169.58 0.000

8 -0.08... -0.03... 170.36 0.000

9 -0.17... -0.15... 174.01 0.000

1... -0.21... 0.088 179.30 0.000

1... -0.20... 0.062 184.41 0.000

1... -0.20... -0.05... 189.19 0.000

1... -0.21... -0.11... 194.63 0.000

1... -0.23... -0.09... 201.22 0.000

1... -0.24... -0.02... 208.87 0.000

1... -0.21... 0.140 214.41 0.000

1... -0.16... 0.012 217.88 0.000

1... -0.12... -0.09... 220.00 0.000

1... -0.05... 0.128 220.38 0.000

2... -0.00... -0.02... 220.39 0.000

2... 0.041 0.049 220.61 0.000

2... 0.083 0.007 221.54 0.000

2... 0.109 -0.06... 223.14 0.000

2... 0.134 0.014 225.62 0.000

2... 0.129 -0.02... 227.93 0.000

2... 0.097 -0.01... 229.26 0.000

2... 0.082 0.026 230.22 0.000

2... 0.071 0.026 230.96 0.000

2... 0.068 0.018 231.64 0.000

3... 0.098 0.134 233.07 0.000

3... 0.095 -0.07... 234.43 0.000

3... 0.085 -0.02... 235.54 0.000

3... 0.111 0.164 237.45 0.000

3... 0.115 -0.01... 239.53 0.000

3... 0.083 -0.14... 240.64 0.000

3... 0.033 -0.08... 240.82 0.000

The correlogram has spikes up to lags 5. The Q statistics corresponding to all the lags are

statistically significant implying presence of significant serial autocorrelation in the residuals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.