Money Laundering in Malaysia's Financial Institutions: A Review

VerifiedAdded on 2021/04/24

|34

|10583

|38

Report

AI Summary

This report provides a comprehensive literature review on money laundering within Malaysia's financial institutions. It begins with an overview of Malaysia and its banking industry, highlighting the sector's growth and importance while acknowledging the underlying issues of corporate fraud, money laundering, and corruption. The report delves into the concept and history of money laundering, tracing its origins and evolution. It discusses the role of forensic accounting skills in detecting and preventing money laundering, particularly from the perspective of AML experts. The report also examines the regulatory framework, including the AMLATFPUA 2001 and its amendments, which are crucial for combating money laundering and terrorism financing. It addresses the challenges faced by banks in detecting and preventing money laundering, emphasizing the need for robust risk assessment mechanisms, IT infrastructure, and compliance departments. The report concludes by underscoring the ongoing risks of money laundering in the Malaysian banking sector and the continuous efforts required to combat these threats.

Running head: MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

Money Laundering in Malaysia’s Financial Institutions

Name of the Student:

Name of the University:

Author’s Note:

Money Laundering in Malaysia’s Financial Institutions

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

Chapter 2:

Literature Review

2.1 Introduction

This segment of the paper brings forth an overview of the results found in the

previous researches that is in accordance to the research topic. In order to give out a larger

picture on the associated researches on forensic accounting and money laundering, this

section of the paper provides researches from the international and domestic aspect. By

depending on the assessed literature, the research framework and hypothesis are framed and

constructed. Distinctively, this section of the paper initiates with the background of Malaysia

and the history of the banking industry in the country. In the later sub-sections of the this

chapter an overview of forensic accounting and money laundering is addressed. The

implications of the skills of forensic accounting in the AML detection especially a focus from

the perspective of the AML experts and then followed by a research model is provided in this

chapter. This section even constructs the research hypothesis and lastly the chapter ends with

the conclusion of the literature review.

2.2 Malaysia and its Banking Industry

Malaysia is generally considered as a proper instance of a flourishing reasonable

Islamic nation (Hall and Page, 2016), a standard setter and global leader of the Islamic

finance (International Monetary Fund, 2017). It has developed in a tremendous manner and

has established to become a developed nation during the years after their independence more

than 50 years ago. The country was ranked to be the 24th successful nation and within the top

four among the Asian countries after nations like Singapore, Hong Kong and Taiwan in the

international ranking with regards to the easiness to do business in a country (The World

Bank, 2017).

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

Chapter 2:

Literature Review

2.1 Introduction

This segment of the paper brings forth an overview of the results found in the

previous researches that is in accordance to the research topic. In order to give out a larger

picture on the associated researches on forensic accounting and money laundering, this

section of the paper provides researches from the international and domestic aspect. By

depending on the assessed literature, the research framework and hypothesis are framed and

constructed. Distinctively, this section of the paper initiates with the background of Malaysia

and the history of the banking industry in the country. In the later sub-sections of the this

chapter an overview of forensic accounting and money laundering is addressed. The

implications of the skills of forensic accounting in the AML detection especially a focus from

the perspective of the AML experts and then followed by a research model is provided in this

chapter. This section even constructs the research hypothesis and lastly the chapter ends with

the conclusion of the literature review.

2.2 Malaysia and its Banking Industry

Malaysia is generally considered as a proper instance of a flourishing reasonable

Islamic nation (Hall and Page, 2016), a standard setter and global leader of the Islamic

finance (International Monetary Fund, 2017). It has developed in a tremendous manner and

has established to become a developed nation during the years after their independence more

than 50 years ago. The country was ranked to be the 24th successful nation and within the top

four among the Asian countries after nations like Singapore, Hong Kong and Taiwan in the

international ranking with regards to the easiness to do business in a country (The World

Bank, 2017).

2

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

The disclosure of the sustainable development, “Brand Finance” looked upon as the

top “500 Banking Brands” in the year 2017 disclosed that all the banks of Malaysia have

enhanced their international ranking out of which CIMB and Maybank retained their crown

of being the Top 10 ASEAN banks and furthermore, top two Malaysian banks in the

international brand ranking (Rao, 2017). In accordance to the other developing nations, the

banking process has a key role to play with regards to the financial intermediary in the

economy of Malaysia as it has an impact on the economic development of the nation (Levine,

1998). The banking system administers most of the financial transactions and flows and plays

a part in more than 70% of the total assets of the financial system. Hence, it is understandable

to admit that an effective and profitable banking sector may be helpful in making sure that an

effective financial process which can lead to sustainable economic development and growth.

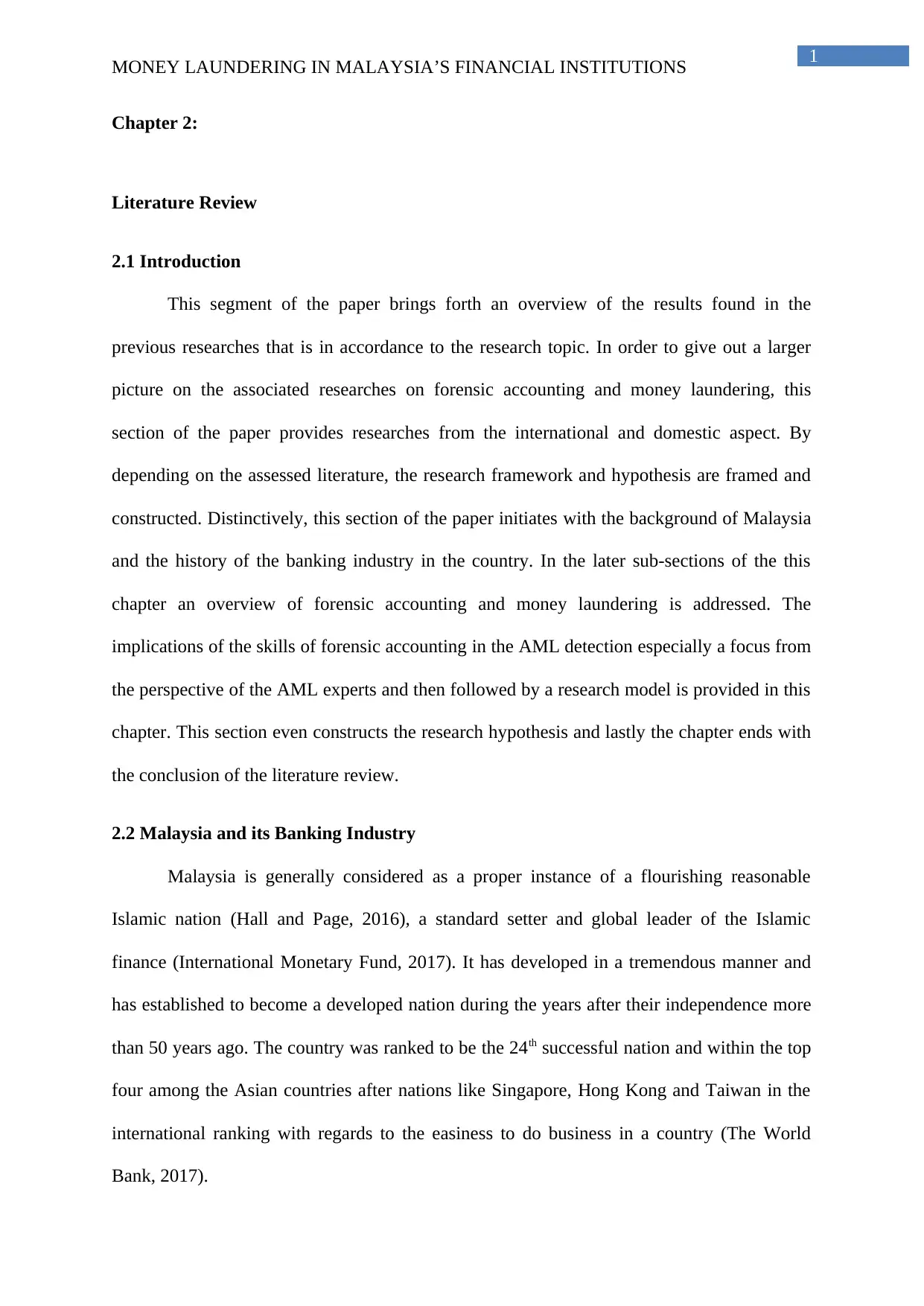

The changes in the financial sector of Malaysia over the current decade give out a key

platform that has assistance for the future development and growth of the financial sector. It

has enhanced their role as an essential contributor to the development in the economy of

Malaysia where the financial sector has recorded a better growth of more than 6.2% in the

year 2017 in their third quarter (Bank Negara Malaysia, 2018).

In spite of their successful attainments, there are several underlying issues over the

development and perseverance of corporate falsifications especially laundering of money,

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

The disclosure of the sustainable development, “Brand Finance” looked upon as the

top “500 Banking Brands” in the year 2017 disclosed that all the banks of Malaysia have

enhanced their international ranking out of which CIMB and Maybank retained their crown

of being the Top 10 ASEAN banks and furthermore, top two Malaysian banks in the

international brand ranking (Rao, 2017). In accordance to the other developing nations, the

banking process has a key role to play with regards to the financial intermediary in the

economy of Malaysia as it has an impact on the economic development of the nation (Levine,

1998). The banking system administers most of the financial transactions and flows and plays

a part in more than 70% of the total assets of the financial system. Hence, it is understandable

to admit that an effective and profitable banking sector may be helpful in making sure that an

effective financial process which can lead to sustainable economic development and growth.

The changes in the financial sector of Malaysia over the current decade give out a key

platform that has assistance for the future development and growth of the financial sector. It

has enhanced their role as an essential contributor to the development in the economy of

Malaysia where the financial sector has recorded a better growth of more than 6.2% in the

year 2017 in their third quarter (Bank Negara Malaysia, 2018).

In spite of their successful attainments, there are several underlying issues over the

development and perseverance of corporate falsifications especially laundering of money,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

corporate cheatings and corruption that are increasingly disclosed to the banking industry;

ASG and FATF, 2015 with the help of their “Malaysian National Risk Assessments in the

year 2012 and 2013” as explained by Said et al, (2013) furthermore assists these issues. In

their “Global Anti-Money Laundering Survey” in the year 2014, KPMG even accepts that

money laundering still is a vital aspect and associates with a greater amount of risk towards

the financial institutions (KPMG, 2014). This information makes it obvious that laundering of

money is a key aspect and a practical issue to the financial industries and that their threats

cannot be undervalued. Provided any bank would be facing a huge amount of risk due to the

intrinsic nature of the banking activities as they provide various services and products that

unconsciously and consciously by taking assistance of the banking organizations, a launderer

transact illegal money by account transfer and fund remittance and the resource of the money

that is retained illegally will remain hidden (Wit, 2007). Reuter and Truman (2004) add

tonally explains that bank transfer with the help of check and wire are most the general

mediums for unlawful transfer of money. Even after saying this, it is commonly accepted that

the banking companies are most commonly utilised tools for the money launderers (Mat et al,

2015). From the point of view of the money launderers, the market of the banking sector

provides benefits like the relatively lower expenses related to laundering in accordance to the

other processes. This phrase was assisted by Sharma (2001) who discovered the evidence in

their research and explains that laundering has a cost that is approximately 6.9% by making

use of the financial markets in opposition to the conventional 20-25% that is given to the

expert money launderers by the terrorist organizations. In accordance to the British National

Crime Intelligence Service as explained by Kumar (2015), costs may be within the range of

6-8% while in certain extraordinary cases it can be 10-50% and the terrorists are satisfied and

happy if they eventually legalise and purify their money with the extent of 30-40%. In the

current regime of AML they have induced the banking organizations to take their

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

corporate cheatings and corruption that are increasingly disclosed to the banking industry;

ASG and FATF, 2015 with the help of their “Malaysian National Risk Assessments in the

year 2012 and 2013” as explained by Said et al, (2013) furthermore assists these issues. In

their “Global Anti-Money Laundering Survey” in the year 2014, KPMG even accepts that

money laundering still is a vital aspect and associates with a greater amount of risk towards

the financial institutions (KPMG, 2014). This information makes it obvious that laundering of

money is a key aspect and a practical issue to the financial industries and that their threats

cannot be undervalued. Provided any bank would be facing a huge amount of risk due to the

intrinsic nature of the banking activities as they provide various services and products that

unconsciously and consciously by taking assistance of the banking organizations, a launderer

transact illegal money by account transfer and fund remittance and the resource of the money

that is retained illegally will remain hidden (Wit, 2007). Reuter and Truman (2004) add

tonally explains that bank transfer with the help of check and wire are most the general

mediums for unlawful transfer of money. Even after saying this, it is commonly accepted that

the banking companies are most commonly utilised tools for the money launderers (Mat et al,

2015). From the point of view of the money launderers, the market of the banking sector

provides benefits like the relatively lower expenses related to laundering in accordance to the

other processes. This phrase was assisted by Sharma (2001) who discovered the evidence in

their research and explains that laundering has a cost that is approximately 6.9% by making

use of the financial markets in opposition to the conventional 20-25% that is given to the

expert money launderers by the terrorist organizations. In accordance to the British National

Crime Intelligence Service as explained by Kumar (2015), costs may be within the range of

6-8% while in certain extraordinary cases it can be 10-50% and the terrorists are satisfied and

happy if they eventually legalise and purify their money with the extent of 30-40%. In the

current regime of AML they have induced the banking organizations to take their

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

responsibilities to restrict direct contact with the unlawful money with the incorporation of

the reporting process and enhanced management techniques that make them less susceptible

for the operations of money laundering.

Therefore, in several nations, banking sector has been looked upon as the key source

of key information for the identification of money laundering. Nonetheless, with the

international process that has developed provided the tangible restrictions to utilise the banks

and its mainstream services and products for the operations of money laundering to occur and

effectiveness of the AML regime is very difficult to evaluate. In accordance to safeguarding

the integrity of the central financial process, the regime of AML created in the key

jurisdiction all over the globe transformed and how the banking industries function in their

business. However, from the prospective of the banks, the key reason for their presence is to

generate profit as much as possible.

Conversely, their commercial and cultural interests are entirely specific from that of

as they now think of money laundering mechanisms with respect to the supply and demands

of the unlawful services within an extrinsic and intrinsic price (Reuter and Truman, 2004).

This has put forth a vital pressure on the banking sector especially over the participation of

the smaller markets. Geiger and Wuensch (2004) and Hubli and Geiger (2004) as explained

by Buehrer, Hubli and Marti (2005), assists this point of view that the pressure for the smaller

banks is double higher than the bigger banks and distinctively this was supported by Hubli

and Geiger (2004) survey where the laundering of money restriction measures take 455 of the

overall regulatory pressure and 2% of the overall costs in the private banking of Switzerland.

Without any doubt, banking organizations has become the most susceptible organization

being the frontier of laundering of money ring in the current decade. In this aspect, the

banking sector in Malaysia have mechanised themselves with sufficient infrastructure to

assess the money laundering risks like the laundering of money risk evaluation mechanism,

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

responsibilities to restrict direct contact with the unlawful money with the incorporation of

the reporting process and enhanced management techniques that make them less susceptible

for the operations of money laundering.

Therefore, in several nations, banking sector has been looked upon as the key source

of key information for the identification of money laundering. Nonetheless, with the

international process that has developed provided the tangible restrictions to utilise the banks

and its mainstream services and products for the operations of money laundering to occur and

effectiveness of the AML regime is very difficult to evaluate. In accordance to safeguarding

the integrity of the central financial process, the regime of AML created in the key

jurisdiction all over the globe transformed and how the banking industries function in their

business. However, from the prospective of the banks, the key reason for their presence is to

generate profit as much as possible.

Conversely, their commercial and cultural interests are entirely specific from that of

as they now think of money laundering mechanisms with respect to the supply and demands

of the unlawful services within an extrinsic and intrinsic price (Reuter and Truman, 2004).

This has put forth a vital pressure on the banking sector especially over the participation of

the smaller markets. Geiger and Wuensch (2004) and Hubli and Geiger (2004) as explained

by Buehrer, Hubli and Marti (2005), assists this point of view that the pressure for the smaller

banks is double higher than the bigger banks and distinctively this was supported by Hubli

and Geiger (2004) survey where the laundering of money restriction measures take 455 of the

overall regulatory pressure and 2% of the overall costs in the private banking of Switzerland.

Without any doubt, banking organizations has become the most susceptible organization

being the frontier of laundering of money ring in the current decade. In this aspect, the

banking sector in Malaysia have mechanised themselves with sufficient infrastructure to

assess the money laundering risks like the laundering of money risk evaluation mechanism,

5

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

mechanised administering solutions, IT framework which is inclusive of the information

process within the company that acts as an assistance tool for the purpose of risk evaluation,

generation of compliance department and regulatory need (Isa et al, 2015; Reuter and

Truman, 2004). .

In this aspect, Malaysia has even joined with the other nations putting in critical

exertions to fight operations of money laundering through the performance of “AMLATFA

2001” under the surveillance of numerous organisations and headed by “Central Bank of

Malaysia”, which was constructed to stay in traditional values with the international

agreements in accordance to money laundering specifically the FATF40 suggestions on

“Money Laundering” and the “Ninth Special Recommendations” on criminal funding

(Shanmugam, 2004; Rahman, 2013). “AMLATFA 2001” is the initial act with the

enforcement of several agencies in Malaysia. In the year 2014, on 8th August, the “Anti-

Money Laundering and Anti-Terrorism Financing Amendment Act 2014” was authorised to

reform the “Anti-Money Laundering and Anti-Terrorism Financing Act 2001” and currently

is known as the “Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of

Unlawful Activities Act 2001” (AMLATFPUA) where the treaty was extended in order to

add in anti-terrorism investments where AMLATFPUA gives out for the wrongdoing of

laundering of money and offences that are anti-terrorism in nature and the actions that can be

undertaken for the restriction of money laundering, power of investigation and the penalty of

the involved property or attained from money laundering and offences related to terrorism

financing along with the proceeds of the terrorist property from the illegal operations and the

instrumentalities of a fault (Bank Negara Malaysia, 2018b; Malaymail Online, 2016). As the

banks developed their control of detecting, restricting, regulating and reporting anti-money

laundering initiatives and still laundering of money is still regarded to be one of the

significant restrictions to an efficient financial process in Malaysia and even globally. This is

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

mechanised administering solutions, IT framework which is inclusive of the information

process within the company that acts as an assistance tool for the purpose of risk evaluation,

generation of compliance department and regulatory need (Isa et al, 2015; Reuter and

Truman, 2004). .

In this aspect, Malaysia has even joined with the other nations putting in critical

exertions to fight operations of money laundering through the performance of “AMLATFA

2001” under the surveillance of numerous organisations and headed by “Central Bank of

Malaysia”, which was constructed to stay in traditional values with the international

agreements in accordance to money laundering specifically the FATF40 suggestions on

“Money Laundering” and the “Ninth Special Recommendations” on criminal funding

(Shanmugam, 2004; Rahman, 2013). “AMLATFA 2001” is the initial act with the

enforcement of several agencies in Malaysia. In the year 2014, on 8th August, the “Anti-

Money Laundering and Anti-Terrorism Financing Amendment Act 2014” was authorised to

reform the “Anti-Money Laundering and Anti-Terrorism Financing Act 2001” and currently

is known as the “Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of

Unlawful Activities Act 2001” (AMLATFPUA) where the treaty was extended in order to

add in anti-terrorism investments where AMLATFPUA gives out for the wrongdoing of

laundering of money and offences that are anti-terrorism in nature and the actions that can be

undertaken for the restriction of money laundering, power of investigation and the penalty of

the involved property or attained from money laundering and offences related to terrorism

financing along with the proceeds of the terrorist property from the illegal operations and the

instrumentalities of a fault (Bank Negara Malaysia, 2018b; Malaymail Online, 2016). As the

banks developed their control of detecting, restricting, regulating and reporting anti-money

laundering initiatives and still laundering of money is still regarded to be one of the

significant restrictions to an efficient financial process in Malaysia and even globally. This is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

due to the fact that the launderers and the terrorists have learned to spread their activities and

extend into their financial organizations or the channel for the financial operations (FATF,

2006). The sequences of the financial businesses in several financial organizations among

many several dominions makes it complex to make a trace (Mohamed and Ahmad, 2012).

However, electronic banking which has made life simple in making transactions with the

banking organizations has even hugely facilitates with the movement of billion dollars in the

illegal funds. Significantly, it not only generates a key dilemma for the banks as it

manufactures a change in the process in which the banks communicate with their customers

but even has the probability to badly impact the activities of the banks (Rahman, 2013). It

cannot be denied that the banks of Malaysia have given desirable amount of money on the

programs associated to ant-money laundering. From these elements it seems relevant to

remember that laundering of money is one of the major risks in the banking sector.

2.3 Money Laundering

2.3.1 Concept and History

There is certain disagreement in the literature in accordance to where the meaning of

money laundering generated from as there is no proof that recommends when the word

“money laundering” was created. Chaikin and Sharman (2009); Steel (1997); and Hardani

(2017) cites that money laundering is a metaphorical word that looks to have generated from

the United States of America during the 1920s in which the Al-Capone’s story of using the

strategy of the launderers and their small businesses in order to costume their profit from the

illegal alcohol during the time of prohibition. This ownership of the mafia of the

Laundromats in USA creates a bigger amount of cash from the illegal proceeds from a

number of profitable offences like the trading of the unlawful drugs, prostitutions, extortions

and murders in order to mingle with the true and fair income from the business of laundry to

confuse the enforcement of the law examinations by revealing a true and authentic source for

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

due to the fact that the launderers and the terrorists have learned to spread their activities and

extend into their financial organizations or the channel for the financial operations (FATF,

2006). The sequences of the financial businesses in several financial organizations among

many several dominions makes it complex to make a trace (Mohamed and Ahmad, 2012).

However, electronic banking which has made life simple in making transactions with the

banking organizations has even hugely facilitates with the movement of billion dollars in the

illegal funds. Significantly, it not only generates a key dilemma for the banks as it

manufactures a change in the process in which the banks communicate with their customers

but even has the probability to badly impact the activities of the banks (Rahman, 2013). It

cannot be denied that the banks of Malaysia have given desirable amount of money on the

programs associated to ant-money laundering. From these elements it seems relevant to

remember that laundering of money is one of the major risks in the banking sector.

2.3 Money Laundering

2.3.1 Concept and History

There is certain disagreement in the literature in accordance to where the meaning of

money laundering generated from as there is no proof that recommends when the word

“money laundering” was created. Chaikin and Sharman (2009); Steel (1997); and Hardani

(2017) cites that money laundering is a metaphorical word that looks to have generated from

the United States of America during the 1920s in which the Al-Capone’s story of using the

strategy of the launderers and their small businesses in order to costume their profit from the

illegal alcohol during the time of prohibition. This ownership of the mafia of the

Laundromats in USA creates a bigger amount of cash from the illegal proceeds from a

number of profitable offences like the trading of the unlawful drugs, prostitutions, extortions

and murders in order to mingle with the true and fair income from the business of laundry to

confuse the enforcement of the law examinations by revealing a true and authentic source for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

the money (Malinoski, 2007). The Laundromats were selected by the criminals as they were

the cash businesses and this was a certain benefit to decriminalize their profits. With the

assistance of the legalised businesses, the money that was illegitimate in nature was

diversified with the legitimate earnings and the overall value was reported as the overall

earnings of the legal businesses. By utilising this process, the unlawful income was

eliminated as the money took the image of the business that is legal. After this mechanism,

the money could therefore be utilised independently without giving any hint to the law

enforcement people. On the other hand, Al-Capone was questioned and convicted in the year

1931 for evading tax which triggered the business of money laundering getting off the ground

(Steel, 1997).

On the other hand, Shehu (2000) discovered a different result and in his paper, he

discovered that the word money laundering came into existence in the year 1932 in the

scenario of Mayer Lansky in USA. In this scenario, Mayer carried out an account that is

offshore in a bank in Switzerland which was exploited to cover the illegal incomes of the

“Governor” named “Huey Long” of Louisiana. Mayer on a later period created a slot device

in New Orleans and the banks that is in Switzerland provided money in the manner of loans

to the company named Lansky & Co. With the help of this process, it permitted the unlawful

money to come back to United States. From that time onwards the activities of money

laundering have developed by making use of innovations that is seen in the development of

new and improved technologies.

On the other hand, looking at the historical sense and in the light of the features of the

term money laundering, the process of concealing the money from the government has huge

history, even though the idea of laundering money may have been unknowing in China. Li

(2009) supports that there are several forms and principles of laundering money that have

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

the money (Malinoski, 2007). The Laundromats were selected by the criminals as they were

the cash businesses and this was a certain benefit to decriminalize their profits. With the

assistance of the legalised businesses, the money that was illegitimate in nature was

diversified with the legitimate earnings and the overall value was reported as the overall

earnings of the legal businesses. By utilising this process, the unlawful income was

eliminated as the money took the image of the business that is legal. After this mechanism,

the money could therefore be utilised independently without giving any hint to the law

enforcement people. On the other hand, Al-Capone was questioned and convicted in the year

1931 for evading tax which triggered the business of money laundering getting off the ground

(Steel, 1997).

On the other hand, Shehu (2000) discovered a different result and in his paper, he

discovered that the word money laundering came into existence in the year 1932 in the

scenario of Mayer Lansky in USA. In this scenario, Mayer carried out an account that is

offshore in a bank in Switzerland which was exploited to cover the illegal incomes of the

“Governor” named “Huey Long” of Louisiana. Mayer on a later period created a slot device

in New Orleans and the banks that is in Switzerland provided money in the manner of loans

to the company named Lansky & Co. With the help of this process, it permitted the unlawful

money to come back to United States. From that time onwards the activities of money

laundering have developed by making use of innovations that is seen in the development of

new and improved technologies.

On the other hand, looking at the historical sense and in the light of the features of the

term money laundering, the process of concealing the money from the government has huge

history, even though the idea of laundering money may have been unknowing in China. Li

(2009) supports that there are several forms and principles of laundering money that have

8

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

been observable and related in the history of China even though the term laundering has

currently has been given to these adverse results.

A similar observation was seen in the book named “Lord of the Rim” by Sterling

Seagrave, who was an American historian. He wrote that “more than 2000 years ago the

Chinese merchants laundered with their profits as the local governments banned various

forms of commercial trades” (Seagrave, 1995). He wrote that the government considered the

activities of the merchants with a huge amount of doubt as they were looked upon as greedy,

ruthless and they followed a rule that was different. Along with this, a huge amount of the

merchant’s income evolved from black marketing, bribe and extortions. The merchants who

remained hidden were successful in keeping their income and wealth safeguarded from the

sustainable extortions by the diplomats. Therefore, they used the mechanisms like changing

their money into assets that are movable easily and taking the cash out of the area, trading at

a higher price in order to make the money invested in the businesses and tax exile funds. This

process is even used in the current time period by the professional money launderers

PHPWind (2008), He (2002) and China Culture (2006) as explained in Li (2009) addtionally

are in line with this idea.

For instance, during the Hans Dynasty (206BC-AD220) reported that theere were

exterme fines to punish a tomb theft who used to lauder their illegal income by working on

behalf of the pawnshops and the antique dealers. The tomb theives had their individual

legalrecognitions and therefore had to conceal their criminal actions from the authority and

public and it is seen till the poresent time the authorities of the tomb raiders is ongoing. The

msot recent evidence is the arrest of the leader of a group and his gang members in the

Northern China authenticates the presence of this group since 206 BC to the current time

period and most of them have been working as archaelogists in certain Chinese national

projects (Yan, 2016). By assessing the extensive degree of the sources that have been

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

been observable and related in the history of China even though the term laundering has

currently has been given to these adverse results.

A similar observation was seen in the book named “Lord of the Rim” by Sterling

Seagrave, who was an American historian. He wrote that “more than 2000 years ago the

Chinese merchants laundered with their profits as the local governments banned various

forms of commercial trades” (Seagrave, 1995). He wrote that the government considered the

activities of the merchants with a huge amount of doubt as they were looked upon as greedy,

ruthless and they followed a rule that was different. Along with this, a huge amount of the

merchant’s income evolved from black marketing, bribe and extortions. The merchants who

remained hidden were successful in keeping their income and wealth safeguarded from the

sustainable extortions by the diplomats. Therefore, they used the mechanisms like changing

their money into assets that are movable easily and taking the cash out of the area, trading at

a higher price in order to make the money invested in the businesses and tax exile funds. This

process is even used in the current time period by the professional money launderers

PHPWind (2008), He (2002) and China Culture (2006) as explained in Li (2009) addtionally

are in line with this idea.

For instance, during the Hans Dynasty (206BC-AD220) reported that theere were

exterme fines to punish a tomb theft who used to lauder their illegal income by working on

behalf of the pawnshops and the antique dealers. The tomb theives had their individual

legalrecognitions and therefore had to conceal their criminal actions from the authority and

public and it is seen till the poresent time the authorities of the tomb raiders is ongoing. The

msot recent evidence is the arrest of the leader of a group and his gang members in the

Northern China authenticates the presence of this group since 206 BC to the current time

period and most of them have been working as archaelogists in certain Chinese national

projects (Yan, 2016). By assessing the extensive degree of the sources that have been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

mentioned earlier, it is looked upon as the fact that the justification behind these trail of

money is that the illegal proceeds are sold generally in cash and therefore has to be

transferred into financiual resources that can be utilised that have an appearance of a legal

origin.

Li (2009) in his reserach cited that the effect of money laudnering on Chine did not

give out any attnetion of their laws and the policy makers like in case of the western parties.

According to OECD (2005), China has been looked as a magnet for the purpose of activities

like money laundering which comprises of approximately up to USD 24 Billion of the assets

that have been illegally obtained for the purpose of laundering each year and the values are

secretly taken out of the country has been increasing. It is justifiable to recommend that the

adversity of money laundering was not observed to be a posting threat to the country as a

whole. A less amount of work was done distinctively in accordance to the efforts of anti-

money laundering and the anti-money launderers within the nation was not as motivated as in

USA in fighting with the crimes as no publishing in the law or the regulation in the year

1980s was generated to address clearly the money laundering term.

However, the word money laundering as an idea was already into existence in USA in

the early periods of 1970s when the country passed the Bank Secrecy Act that looked to

provide enforcement personnel with the weapon that is essential to fight with money

laundering (Madinger, 2012). This Act is in need of the financial organizations in order to

keep a record of the file and requirement of reporting for the Suspicious Activity Report, a

Currency Transaction Report, a report on the accounts in the foreign banks and the reports on

the movements of the currency that is taking place through cross-border movements and

administering of the mechanism. The justification for this reporting reliant process is to

generate a paper trail that would assist the law enforcement personnel in examining money

laundering scenarios. Furthermore, the efficient incorporation and enforcement of BSA of

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

mentioned earlier, it is looked upon as the fact that the justification behind these trail of

money is that the illegal proceeds are sold generally in cash and therefore has to be

transferred into financiual resources that can be utilised that have an appearance of a legal

origin.

Li (2009) in his reserach cited that the effect of money laudnering on Chine did not

give out any attnetion of their laws and the policy makers like in case of the western parties.

According to OECD (2005), China has been looked as a magnet for the purpose of activities

like money laundering which comprises of approximately up to USD 24 Billion of the assets

that have been illegally obtained for the purpose of laundering each year and the values are

secretly taken out of the country has been increasing. It is justifiable to recommend that the

adversity of money laundering was not observed to be a posting threat to the country as a

whole. A less amount of work was done distinctively in accordance to the efforts of anti-

money laundering and the anti-money launderers within the nation was not as motivated as in

USA in fighting with the crimes as no publishing in the law or the regulation in the year

1980s was generated to address clearly the money laundering term.

However, the word money laundering as an idea was already into existence in USA in

the early periods of 1970s when the country passed the Bank Secrecy Act that looked to

provide enforcement personnel with the weapon that is essential to fight with money

laundering (Madinger, 2012). This Act is in need of the financial organizations in order to

keep a record of the file and requirement of reporting for the Suspicious Activity Report, a

Currency Transaction Report, a report on the accounts in the foreign banks and the reports on

the movements of the currency that is taking place through cross-border movements and

administering of the mechanism. The justification for this reporting reliant process is to

generate a paper trail that would assist the law enforcement personnel in examining money

laundering scenarios. Furthermore, the efficient incorporation and enforcement of BSA of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

1970, Congress acted the Money Laundering Control Act (MLCA) of 1986 that was followed

by the incorporation of the “United Nations Conventions” that is in contradiction of unlawful

“Traffic in Narcotic Drugs and Psychotropic Substances” that made money laundering into

the global stage and thereby played a key role in the initiation of the idea of money

laundering internationally (Amrani, 2012). Thereafter, “Financial Action Task Force”

(FATF) established in the “G-7 Summit” in Paris in the year 1989 on July was generated as a

free inter-governmental agency looking to further promote and enhance the policies and

safeguard the international financial system against things like money laundering and

criminal financing (FATF, 2018). During the time of the early 1990s, the efforts from the

international AML experienced a quick and huge development as the key global

organizations diffused and endorsed the rules of the AML. The actual FATF 40 suggestions

were constructed in the year 190 as an initiation to fight the mishandling of the financial

process by the individuals who are laundering the drug money. In the year 1996, the

suggestions had to be changed for the first time and thereafter revises continuously till the

year 2013 in order to reflect the developing money laundering which extensively created new

threats of anti-money laundering, anti-criminal activities, rise in the level of financing and

incorporation of the risk evaluation rule of the nation’s criminal financing and terrorism of

money laundering (FATF, 2018; Mei, Ye and Gao,2014). The measures of the FATF are

looked upon as the leading international standards of international money laundering that

provides an improved, consistent and complete structure for fighting laundering of money

and criminal financing that functions as a global benchmark for the national agencies and the

governments to incorporate within their national boundaries, for the identification, restriction

and suppression of laundering of money and financing of the criminals. It is the most

effective body in constructing the standards of AL from their establishment to the current day

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

1970, Congress acted the Money Laundering Control Act (MLCA) of 1986 that was followed

by the incorporation of the “United Nations Conventions” that is in contradiction of unlawful

“Traffic in Narcotic Drugs and Psychotropic Substances” that made money laundering into

the global stage and thereby played a key role in the initiation of the idea of money

laundering internationally (Amrani, 2012). Thereafter, “Financial Action Task Force”

(FATF) established in the “G-7 Summit” in Paris in the year 1989 on July was generated as a

free inter-governmental agency looking to further promote and enhance the policies and

safeguard the international financial system against things like money laundering and

criminal financing (FATF, 2018). During the time of the early 1990s, the efforts from the

international AML experienced a quick and huge development as the key global

organizations diffused and endorsed the rules of the AML. The actual FATF 40 suggestions

were constructed in the year 190 as an initiation to fight the mishandling of the financial

process by the individuals who are laundering the drug money. In the year 1996, the

suggestions had to be changed for the first time and thereafter revises continuously till the

year 2013 in order to reflect the developing money laundering which extensively created new

threats of anti-money laundering, anti-criminal activities, rise in the level of financing and

incorporation of the risk evaluation rule of the nation’s criminal financing and terrorism of

money laundering (FATF, 2018; Mei, Ye and Gao,2014). The measures of the FATF are

looked upon as the leading international standards of international money laundering that

provides an improved, consistent and complete structure for fighting laundering of money

and criminal financing that functions as a global benchmark for the national agencies and the

governments to incorporate within their national boundaries, for the identification, restriction

and suppression of laundering of money and financing of the criminals. It is the most

effective body in constructing the standards of AL from their establishment to the current day

11

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

as it is not an official treaty company but is more dependent on the frequent decisions to

renovate their existence by the states where the meetings are held three times within a year.

2.3.2 Definition

The significance of the crimes of money laundering has led to the academic research on

this aspect from all sections of the world encompassing the practical and the legal issues

which cover the research on the offences, restrictive actions, cases, regulations and

discovering the patterns of money laundering operations in which it is covering the crime.

Therefore, there are several and numerous explanations of money laundering in the articles

that have been published which may be different among the companies and the jurisdictions

(Adewale, 2008). The UN explained the process of money laundering as an action that is

associated with the transfer or the conversion of a property or the hiding of the true character

of the property as a knowledge is there that this property is attained from drug and other

trafficking. The FATF (2012) explained money laundering to be the mechanism of the

earnings of the criminals to costume their unlawful source, in order to legalise the unlawful

revenue from the crime which is gained through the unlawful operations like the sale of the

illicit drugs, wildlife sales and sales of arms and ammunitions, forgery of tax, insider trading,

embezzlement, fraud in the securities, bribery and corruption (Johnson, 2001). AMLAFTA

2001 explains that money laundering is the performance of a person who:

(a) Directly, indirectly engages in a financial dealings that is associated with the proceeds

of any illegal operations:

(b) Possesses, gains, receives, converts, carries, transfers, utilises, exchanges and

eliminates from or brings forth into the proceeds in Malaysia of any illegal operations:

or

(c) Covers, hides or obstructs the creation of location, origin, true, disposition,

movements and the title of proceeds, rights and ownership of any illicit operations.

MONEY LAUNDERING IN MALAYSIA’S FINANCIAL INSTITUTIONS

as it is not an official treaty company but is more dependent on the frequent decisions to

renovate their existence by the states where the meetings are held three times within a year.

2.3.2 Definition

The significance of the crimes of money laundering has led to the academic research on

this aspect from all sections of the world encompassing the practical and the legal issues

which cover the research on the offences, restrictive actions, cases, regulations and

discovering the patterns of money laundering operations in which it is covering the crime.

Therefore, there are several and numerous explanations of money laundering in the articles

that have been published which may be different among the companies and the jurisdictions

(Adewale, 2008). The UN explained the process of money laundering as an action that is

associated with the transfer or the conversion of a property or the hiding of the true character

of the property as a knowledge is there that this property is attained from drug and other

trafficking. The FATF (2012) explained money laundering to be the mechanism of the

earnings of the criminals to costume their unlawful source, in order to legalise the unlawful

revenue from the crime which is gained through the unlawful operations like the sale of the

illicit drugs, wildlife sales and sales of arms and ammunitions, forgery of tax, insider trading,

embezzlement, fraud in the securities, bribery and corruption (Johnson, 2001). AMLAFTA

2001 explains that money laundering is the performance of a person who:

(a) Directly, indirectly engages in a financial dealings that is associated with the proceeds

of any illegal operations:

(b) Possesses, gains, receives, converts, carries, transfers, utilises, exchanges and

eliminates from or brings forth into the proceeds in Malaysia of any illegal operations:

or

(c) Covers, hides or obstructs the creation of location, origin, true, disposition,

movements and the title of proceeds, rights and ownership of any illicit operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.