University Marketing Report: Money Mentors Market Analysis, Alberta

VerifiedAdded on 2022/11/14

|24

|4060

|232

Report

AI Summary

This report provides a comprehensive market analysis of Money Mentors, a non-profit organization based in Alberta, Canada, using the 5C approach (Customer, Context, Company, Collaborators, and Competitors). The analysis delves into the company's mission to assist Albertans facing financial crises, its history, and its operational strategies, including the Orderly Payment of Debt program. It examines the external factors affecting the company, such as political, social, technological, economic, and legal environments (PESTEL analysis). The report then explores market segmentation, primarily focusing on demographic segmentation by age, and recommends a target market of individuals aged 20 to 40. Furthermore, the report highlights the company's goals of eradicating financial hardship and suggests strategies for effective market positioning, incorporating data from government surveys and competitor analysis. The report concludes with recommendations for Money Mentors to enhance its services and reach its target audience effectively.

Running Head: Marketing management

Marketing management

Name of the student

Name of the university

Author’s note

Marketing management

Name of the student

Name of the university

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Marketing management

Executive summary

The report deals with the study of the company known as Money Mentor of Alberta,

Canada. The study introduces the reader with the market analysis of the company with the

help of 5C approach. The market segmentation of the company is also done, which works

according to the demographic segmentation. Different factors affecting the company's

performance is also demonstrated. Recommendations are also suggested to the company

about the target market. The company's goals are also shown, which is all about eradicating

the financial crisis of the people of its place.

Marketing management

Executive summary

The report deals with the study of the company known as Money Mentor of Alberta,

Canada. The study introduces the reader with the market analysis of the company with the

help of 5C approach. The market segmentation of the company is also done, which works

according to the demographic segmentation. Different factors affecting the company's

performance is also demonstrated. Recommendations are also suggested to the company

about the target market. The company's goals are also shown, which is all about eradicating

the financial crisis of the people of its place.

3

Marketing management

Table of Contents

Introduction...........................................................................................................................................4

Background............................................................................................................................................4

Market analysis.....................................................................................................................................5

Customer...........................................................................................................................................5

Context..............................................................................................................................................5

Company...........................................................................................................................................6

Collaborators.....................................................................................................................................6

Competitors.......................................................................................................................................6

Market segmentation............................................................................................................................7

Target market recommendation...........................................................................................................8

Market analysis.....................................................................................................................................8

Sizing..................................................................................................................................................8

Weighing scale...................................................................................................................................9

Segment Analysis:............................................................................................................................10

Segmenting Scale:............................................................................................................................11

Ranking:...........................................................................................................................................12

Segment Map:.................................................................................................................................13

Market segment Ranking Chart:......................................................................................................14

Conclusion...........................................................................................................................................14

References...........................................................................................................................................15

Appendix 1...........................................................................................................................................17

Appendix 2...........................................................................................................................................18

Appendix 3...........................................................................................................................................19

Appendix 4...........................................................................................................................................20

Appendix 5...........................................................................................................................................22

Appendix 6...........................................................................................................................................23

Appendix 7...........................................................................................................................................24

Marketing management

Table of Contents

Introduction...........................................................................................................................................4

Background............................................................................................................................................4

Market analysis.....................................................................................................................................5

Customer...........................................................................................................................................5

Context..............................................................................................................................................5

Company...........................................................................................................................................6

Collaborators.....................................................................................................................................6

Competitors.......................................................................................................................................6

Market segmentation............................................................................................................................7

Target market recommendation...........................................................................................................8

Market analysis.....................................................................................................................................8

Sizing..................................................................................................................................................8

Weighing scale...................................................................................................................................9

Segment Analysis:............................................................................................................................10

Segmenting Scale:............................................................................................................................11

Ranking:...........................................................................................................................................12

Segment Map:.................................................................................................................................13

Market segment Ranking Chart:......................................................................................................14

Conclusion...........................................................................................................................................14

References...........................................................................................................................................15

Appendix 1...........................................................................................................................................17

Appendix 2...........................................................................................................................................18

Appendix 3...........................................................................................................................................19

Appendix 4...........................................................................................................................................20

Appendix 5...........................................................................................................................................22

Appendix 6...........................................................................................................................................23

Appendix 7...........................................................................................................................................24

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Marketing management

Introduction

The name of the company is Money Mentors, which is a non-profit organization

which conducts counselling and administration of the Orderly Payment of Debt program on

the part of the federal government in Alberta Canada. The firm was established in the year

1997 and since been recognised as the sole counselling company. The company deals with

the issue of bankruptcy and proposals of the consumers. Its main motive is to assist the

people of Alberta in Canada from the calamity of finances. It also takes into consideration the

factors of education, counselling programmes and the coaching facilities. It provides relief by

offering debts to the people and the institutions in need. Thus, one can say that the company

offers a service which meets the needs of the consumers.

Background

Money Mentors is a company with the mission statement of educating the Albertans

through the management of money in a personal way by making use of the credit in a wise

manner. It provides alternative options to struggling families and individuals. It aims towards

building a healthy future in terms of financial issues and confirms for their financial literacy.

Thousands of Albertans have been helped since its launch of the Credit Counselling Services

by finding out suitable solutions to the financial crisis. The debts which were challenging to

manage is now managed exclusively with efficient use of the Orderly Payment of Debts

Program. The success of the company is noticed with the return of $125 million to the

respective creditors within the first fifteen years. This success has to lead them to win the

Consumer Choice Award for Business Excellence six times in a row.

The company employs efficient team members who are expert in handling the

financial issues to provide a qualified service to its consumers. The company also conducts

the OPD program for money coaching and credit counselling. The company believes in the

orderly payments of the programmes. This program is created in collaboration with the

federal government of Alberta. The entire management and the control are done under the

guidance and offerings of the Money Mentors. The strategies and the works are federally

legislated with the fixed rate of interest on the debt as considered. Online and offline

resources are also used for managing and handling the entire functioning. Practical and

realistic plans of earning and spending are dealt with the debts. The company assures its

Marketing management

Introduction

The name of the company is Money Mentors, which is a non-profit organization

which conducts counselling and administration of the Orderly Payment of Debt program on

the part of the federal government in Alberta Canada. The firm was established in the year

1997 and since been recognised as the sole counselling company. The company deals with

the issue of bankruptcy and proposals of the consumers. Its main motive is to assist the

people of Alberta in Canada from the calamity of finances. It also takes into consideration the

factors of education, counselling programmes and the coaching facilities. It provides relief by

offering debts to the people and the institutions in need. Thus, one can say that the company

offers a service which meets the needs of the consumers.

Background

Money Mentors is a company with the mission statement of educating the Albertans

through the management of money in a personal way by making use of the credit in a wise

manner. It provides alternative options to struggling families and individuals. It aims towards

building a healthy future in terms of financial issues and confirms for their financial literacy.

Thousands of Albertans have been helped since its launch of the Credit Counselling Services

by finding out suitable solutions to the financial crisis. The debts which were challenging to

manage is now managed exclusively with efficient use of the Orderly Payment of Debts

Program. The success of the company is noticed with the return of $125 million to the

respective creditors within the first fifteen years. This success has to lead them to win the

Consumer Choice Award for Business Excellence six times in a row.

The company employs efficient team members who are expert in handling the

financial issues to provide a qualified service to its consumers. The company also conducts

the OPD program for money coaching and credit counselling. The company believes in the

orderly payments of the programmes. This program is created in collaboration with the

federal government of Alberta. The entire management and the control are done under the

guidance and offerings of the Money Mentors. The strategies and the works are federally

legislated with the fixed rate of interest on the debt as considered. Online and offline

resources are also used for managing and handling the entire functioning. Practical and

realistic plans of earning and spending are dealt with the debts. The company assures its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Marketing management

customers of the services it provides by sharing the success stories of the company and

making them entrust their rules and principles.

Market analysis

The market analysis of the company Money Mentors is done with the help of 5C

approach, which determines its customers, competitors, company, collaborators and the

context.

Customer

The company is determined to fulfil the needs of the customers in terms of financial

crisis since its establishment. The people of Alberta are said to have the most significant debt

per capita on average in Canada. The company helps the people of Alberta to gain the

obligations related to the debt repayment. In this way, the clients are also protected from any

strict legal actions taken against them by the creditors. The company evaluates the varied

alternatives regarding the purchase decisions, the post-purchase choices, the search of

information, bill payments done online and the issues of underemployment among the

citizens.

Context

The analysis of the context of the company is done with the help of PESTEL analysis

which showcases the political, environmental, social, technological, economic and the legal

environment of the company (Poloz.SS. 2018)

Political factors -The population of Alberta is not less and is expected to grow in recent

years with the addition of more pressure on the company regarding financial issues. The

company, however, efficiently manages the matter on behalf of the Albertan federal

government.

Social factors -The socio-cultural environment of Alberta is such which arises the situation

of taking debts from the creditors and falling into the trap of financial crisis. The company

deals with these socio-cultural factors and provides education and counselling related to

finances and how to cover up the debts to the people of Alberta.

Technological factors -The technical elements and the resources of the company are kept up

to date to meet the urgent situations aroused due to financial scarcity. The technology plays

an essential role in keeping the records safely and accurately to be used for future reference.

Marketing management

customers of the services it provides by sharing the success stories of the company and

making them entrust their rules and principles.

Market analysis

The market analysis of the company Money Mentors is done with the help of 5C

approach, which determines its customers, competitors, company, collaborators and the

context.

Customer

The company is determined to fulfil the needs of the customers in terms of financial

crisis since its establishment. The people of Alberta are said to have the most significant debt

per capita on average in Canada. The company helps the people of Alberta to gain the

obligations related to the debt repayment. In this way, the clients are also protected from any

strict legal actions taken against them by the creditors. The company evaluates the varied

alternatives regarding the purchase decisions, the post-purchase choices, the search of

information, bill payments done online and the issues of underemployment among the

citizens.

Context

The analysis of the context of the company is done with the help of PESTEL analysis

which showcases the political, environmental, social, technological, economic and the legal

environment of the company (Poloz.SS. 2018)

Political factors -The population of Alberta is not less and is expected to grow in recent

years with the addition of more pressure on the company regarding financial issues. The

company, however, efficiently manages the matter on behalf of the Albertan federal

government.

Social factors -The socio-cultural environment of Alberta is such which arises the situation

of taking debts from the creditors and falling into the trap of financial crisis. The company

deals with these socio-cultural factors and provides education and counselling related to

finances and how to cover up the debts to the people of Alberta.

Technological factors -The technical elements and the resources of the company are kept up

to date to meet the urgent situations aroused due to financial scarcity. The technology plays

an essential role in keeping the records safely and accurately to be used for future reference.

6

Marketing management

The bankruptcy and insolvency details, the debt collection, and the written debt documents

are held securely, and records are updated with the technical assistance.

Economic factors- The company focuses on the integrity of the financial resources in the

country. It seeks for the debt management of the country along with credit counselling and

resources for financial education. The fundamental of personal finance is learnt among the

people, which enhances their confidence and leads to their economic growth. New

commercial initiatives are always undertaken by the company to increase financial

knowledge.

Legal factors -The statutory considerations of the company include preventing the struggling

individuals and the families from the strict actions which might be taken against them by the

creditors. The company thus assists them in returning their debts and enhancing productivity

in Alberta.

Company

The business model of Money Mentors has been successful in helping the people of

Alberta at the time of financial crisis. The business model considers the customer base of the

place, the services it provides and the financing details of the company. The company has

also launched various plans and online tools, which helps the Albertans to take direct

assistance from the company in case of financial struggles. People can organize their

incomes, expenses, debts and the other business assets with the help of these online tools. The

financial calculators provided by the company helps in indulging into emergency savings,

gauging the credit card debt, earning interests and focusing on investments goals. The

company implements strategies which benefit both the customers and the company and

accelerates towards eradicating the issue of finances of Alberta shortly. Credit reports are

created, and financial tips are given to the customers to deal with the debt in a healthy manner

(Equifax.C., 2018)

Collaborators

The collaborators of the Money Mentor company are the private and the public banks

of Alberta, the social services institutions and organizations owned privately and by the

government organization. The financial institutions and the counselling organizations also

collaborate with the company to help them in fulfilling their mission and achieving their goal

aimed towards society.

Marketing management

The bankruptcy and insolvency details, the debt collection, and the written debt documents

are held securely, and records are updated with the technical assistance.

Economic factors- The company focuses on the integrity of the financial resources in the

country. It seeks for the debt management of the country along with credit counselling and

resources for financial education. The fundamental of personal finance is learnt among the

people, which enhances their confidence and leads to their economic growth. New

commercial initiatives are always undertaken by the company to increase financial

knowledge.

Legal factors -The statutory considerations of the company include preventing the struggling

individuals and the families from the strict actions which might be taken against them by the

creditors. The company thus assists them in returning their debts and enhancing productivity

in Alberta.

Company

The business model of Money Mentors has been successful in helping the people of

Alberta at the time of financial crisis. The business model considers the customer base of the

place, the services it provides and the financing details of the company. The company has

also launched various plans and online tools, which helps the Albertans to take direct

assistance from the company in case of financial struggles. People can organize their

incomes, expenses, debts and the other business assets with the help of these online tools. The

financial calculators provided by the company helps in indulging into emergency savings,

gauging the credit card debt, earning interests and focusing on investments goals. The

company implements strategies which benefit both the customers and the company and

accelerates towards eradicating the issue of finances of Alberta shortly. Credit reports are

created, and financial tips are given to the customers to deal with the debt in a healthy manner

(Equifax.C., 2018)

Collaborators

The collaborators of the Money Mentor company are the private and the public banks

of Alberta, the social services institutions and organizations owned privately and by the

government organization. The financial institutions and the counselling organizations also

collaborate with the company to help them in fulfilling their mission and achieving their goal

aimed towards society.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Marketing management

Competitors

The company also has many competitors like those of the trustees of the large

organizations and the DMP's. The trustees contribute to the 90 per cent of the market share in

the sector of bankruptcy and insolvency in Alberta. The competitive edge of the company

needs to be reliable, which is maintained by operating under law and regulations.

Market segmentation

Demographic segmentation of the market is said to be the most extensive type of

market segmentation used to gain maximum analysis and benefit. Money Mentor uses the

strength of the population to achieve the significant variables of segmenting the market. The

segmentation is done more specifically to age. The industry standards of the company

demand for its demographic segmentation. The federal government considers the population

in the entire debt sector; there are major credit reporting bureaus, which are two in a number

called Equifax and TransUnion. The demographic segmentation can prove vital for the

insolvency and the bankruptcy sectors of the company.

The market is generally divided by the company into different age groups namely,

preschool children, the children of school age, adults of the age twenty to forty, adults of the

age forty to sixty-five, adults of the age sixty-five and above and the old age members. The

life cycle of the market determines various resources of segmentation the company uses.

These variables of the demographic segmentation, especially age, is associated with the needs

and wants of the customers. These variables can be easily measured with the help of a survey.

The size of the market is efficiently described, and the Money Mentor uses this variable to

determine the sections suffering from the financial crisis and then assists accordingly. The

needs and the wants of the consumer's changes with age and thus the company uses this

method of market segmentation to function efficiently (Hansen.J., 2019)

The lack of the debt to the adult will be more as compared to that of a school going

child, and thus the company can formulate and implement strategies by estimating the

number of adults and their probable needs and requirements. With the primary function of the

financial issue being the same, there may be changes in the sources leading to the scarcity.

Money Mentors also gives its support to the various training programmes to ensure that the

consumers and the participants gain the utmost benefit and enjoyable experience with

positively influencing the community. It also volunteers and contributes to the process of its

Marketing management

Competitors

The company also has many competitors like those of the trustees of the large

organizations and the DMP's. The trustees contribute to the 90 per cent of the market share in

the sector of bankruptcy and insolvency in Alberta. The competitive edge of the company

needs to be reliable, which is maintained by operating under law and regulations.

Market segmentation

Demographic segmentation of the market is said to be the most extensive type of

market segmentation used to gain maximum analysis and benefit. Money Mentor uses the

strength of the population to achieve the significant variables of segmenting the market. The

segmentation is done more specifically to age. The industry standards of the company

demand for its demographic segmentation. The federal government considers the population

in the entire debt sector; there are major credit reporting bureaus, which are two in a number

called Equifax and TransUnion. The demographic segmentation can prove vital for the

insolvency and the bankruptcy sectors of the company.

The market is generally divided by the company into different age groups namely,

preschool children, the children of school age, adults of the age twenty to forty, adults of the

age forty to sixty-five, adults of the age sixty-five and above and the old age members. The

life cycle of the market determines various resources of segmentation the company uses.

These variables of the demographic segmentation, especially age, is associated with the needs

and wants of the customers. These variables can be easily measured with the help of a survey.

The size of the market is efficiently described, and the Money Mentor uses this variable to

determine the sections suffering from the financial crisis and then assists accordingly. The

needs and the wants of the consumer's changes with age and thus the company uses this

method of market segmentation to function efficiently (Hansen.J., 2019)

The lack of the debt to the adult will be more as compared to that of a school going

child, and thus the company can formulate and implement strategies by estimating the

number of adults and their probable needs and requirements. With the primary function of the

financial issue being the same, there may be changes in the sources leading to the scarcity.

Money Mentors also gives its support to the various training programmes to ensure that the

consumers and the participants gain the utmost benefit and enjoyable experience with

positively influencing the community. It also volunteers and contributes to the process of its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Marketing management

business. The company makes the fundamental investigations and deals with the concepts of

financing the individuals and so on. The financial services marketing concepts are understood

which creates a better sense of working and functioning (Kotler, 2016)

Target market recommendation

The company implements various methodologies like data collection, mentoring

activities, the previous experiences of working and performing, and the willingness to assist

in future helps in determining the target market. The surveys are conducted by the

government of Alberta, which gives a thorough knowledge of the financial programmes and

the struggling status of the families and individuals. The target market to be recommended to

the company of Money Mentors is the group of people with the age group of twenty to forty

years. The maximum debt management is required by these people, which is eventually

fulfilled in the future run (Seskus, 2019).

The people with the significant employment status needs to be focused on regarding

the ways they handle their expenditure and the credit savings. The age of the Alberta

population demonstrates the income and the education of the community, which helps in the

mentoring of the financial issues. The company must keep the differences in mind while

implementation of the efficient strategies which reflects the requirements of the needy person

in the population. The company must interpret the needs with caution while taking the

estimates of the smaller subgroups. The company must establish itself as the formal and the

informal mentor, which helps in a distinguished level of backgrounds. The company also

investigates the target markets of the competition and the way it deals with the customers

(Craddock, 2019)

The company must make use of the information gained from the results of the survey

conducted by the federal government of Alberta, Canada. A complete list of the demographic

segmentation and its information is necessary to be relied on for work following the same.

Being specific plays an essential role in the total understanding of the system and the

financial crisis. It is also necessary for the company to keep the record of the amount of

money given to its customers so that further implementations can be done with the

affordability. The employees play a vital role in the determination of the company's success

by gaining achievement of the goal (Emter, 2010)

Marketing management

business. The company makes the fundamental investigations and deals with the concepts of

financing the individuals and so on. The financial services marketing concepts are understood

which creates a better sense of working and functioning (Kotler, 2016)

Target market recommendation

The company implements various methodologies like data collection, mentoring

activities, the previous experiences of working and performing, and the willingness to assist

in future helps in determining the target market. The surveys are conducted by the

government of Alberta, which gives a thorough knowledge of the financial programmes and

the struggling status of the families and individuals. The target market to be recommended to

the company of Money Mentors is the group of people with the age group of twenty to forty

years. The maximum debt management is required by these people, which is eventually

fulfilled in the future run (Seskus, 2019).

The people with the significant employment status needs to be focused on regarding

the ways they handle their expenditure and the credit savings. The age of the Alberta

population demonstrates the income and the education of the community, which helps in the

mentoring of the financial issues. The company must keep the differences in mind while

implementation of the efficient strategies which reflects the requirements of the needy person

in the population. The company must interpret the needs with caution while taking the

estimates of the smaller subgroups. The company must establish itself as the formal and the

informal mentor, which helps in a distinguished level of backgrounds. The company also

investigates the target markets of the competition and the way it deals with the customers

(Craddock, 2019)

The company must make use of the information gained from the results of the survey

conducted by the federal government of Alberta, Canada. A complete list of the demographic

segmentation and its information is necessary to be relied on for work following the same.

Being specific plays an essential role in the total understanding of the system and the

financial crisis. It is also necessary for the company to keep the record of the amount of

money given to its customers so that further implementations can be done with the

affordability. The employees play a vital role in the determination of the company's success

by gaining achievement of the goal (Emter, 2010)

9

Marketing management

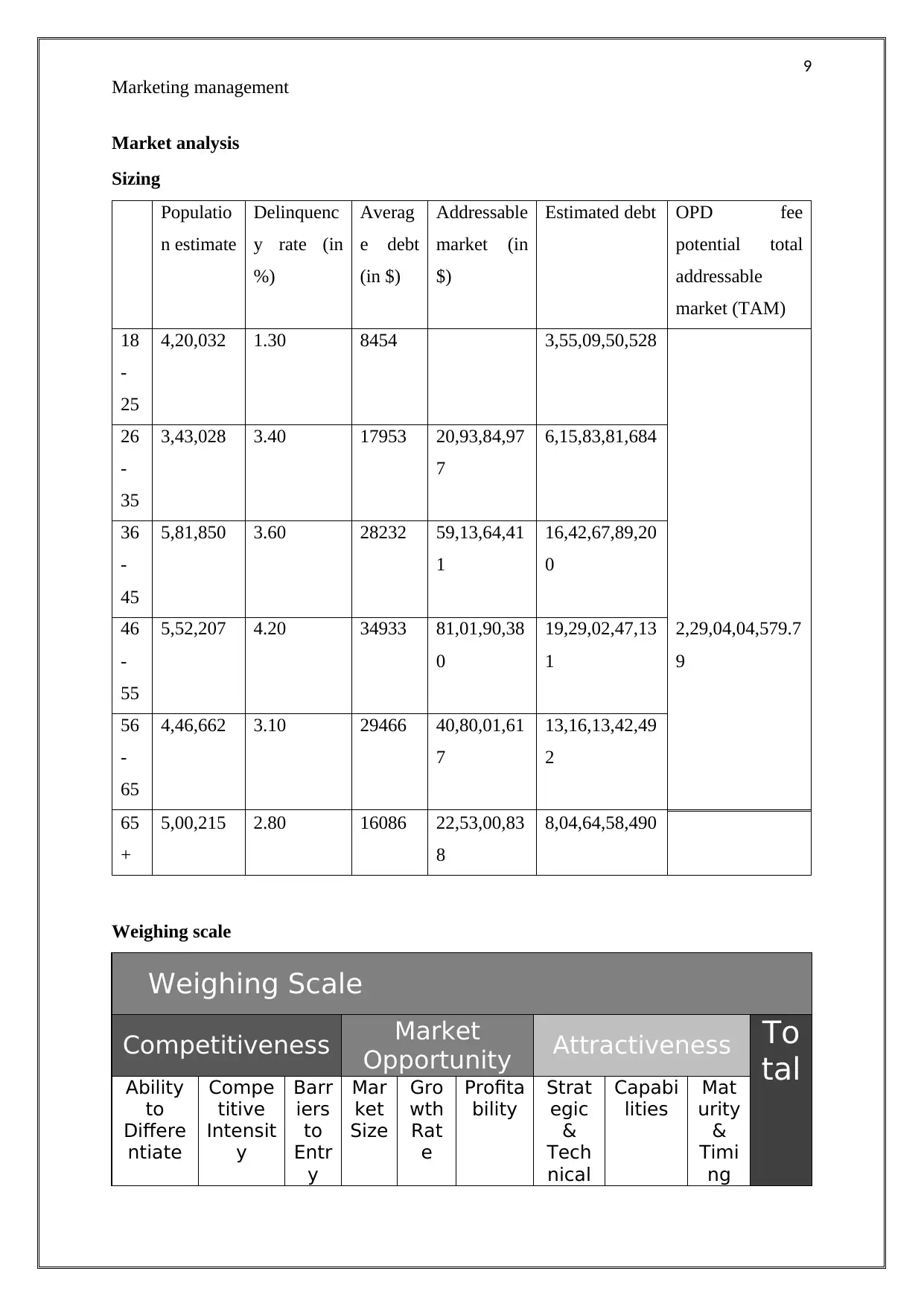

Market analysis

Sizing

Populatio

n estimate

Delinquenc

y rate (in

%)

Averag

e debt

(in $)

Addressable

market (in

$)

Estimated debt OPD fee

potential total

addressable

market (TAM)

18

-

25

4,20,032 1.30 8454 3,55,09,50,528

26

-

35

3,43,028 3.40 17953 20,93,84,97

7

6,15,83,81,684

36

-

45

5,81,850 3.60 28232 59,13,64,41

1

16,42,67,89,20

0

46

-

55

5,52,207 4.20 34933 81,01,90,38

0

19,29,02,47,13

1

2,29,04,04,579.7

9

56

-

65

4,46,662 3.10 29466 40,80,01,61

7

13,16,13,42,49

2

65

+

5,00,215 2.80 16086 22,53,00,83

8

8,04,64,58,490

Weighing scale

Weighing Scale

Competitiveness Market

Opportunity Attractiveness To

talAbility

to

Differe

ntiate

Compe

titive

Intensit

y

Barr

iers

to

Entr

y

Mar

ket

Size

Gro

wth

Rat

e

Profita

bility

Strat

egic

&

Tech

nical

Capabi

lities

Mat

urity

&

Timi

ng

Marketing management

Market analysis

Sizing

Populatio

n estimate

Delinquenc

y rate (in

%)

Averag

e debt

(in $)

Addressable

market (in

$)

Estimated debt OPD fee

potential total

addressable

market (TAM)

18

-

25

4,20,032 1.30 8454 3,55,09,50,528

26

-

35

3,43,028 3.40 17953 20,93,84,97

7

6,15,83,81,684

36

-

45

5,81,850 3.60 28232 59,13,64,41

1

16,42,67,89,20

0

46

-

55

5,52,207 4.20 34933 81,01,90,38

0

19,29,02,47,13

1

2,29,04,04,579.7

9

56

-

65

4,46,662 3.10 29466 40,80,01,61

7

13,16,13,42,49

2

65

+

5,00,215 2.80 16086 22,53,00,83

8

8,04,64,58,490

Weighing scale

Weighing Scale

Competitiveness Market

Opportunity Attractiveness To

talAbility

to

Differe

ntiate

Compe

titive

Intensit

y

Barr

iers

to

Entr

y

Mar

ket

Size

Gro

wth

Rat

e

Profita

bility

Strat

egic

&

Tech

nical

Capabi

lities

Mat

urity

&

Timi

ng

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

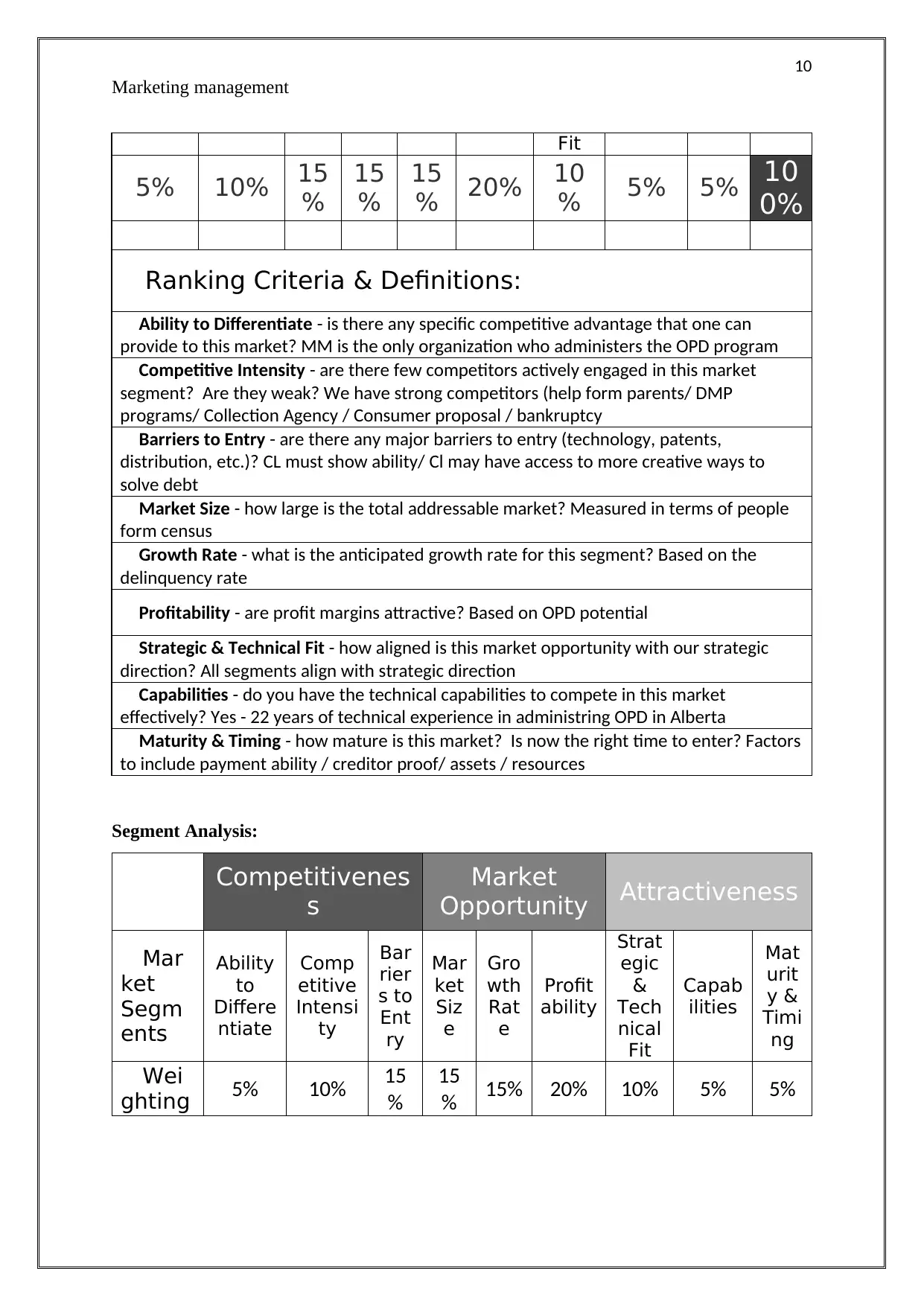

Marketing management

Fit

5% 10% 15

%

15

%

15

% 20% 10

% 5% 5% 10

0%

Ranking Criteria & Definitions:

Ability to Differentiate - is there any specific competitive advantage that one can

provide to this market? MM is the only organization who administers the OPD program

Competitive Intensity - are there few competitors actively engaged in this market

segment? Are they weak? We have strong competitors (help form parents/ DMP

programs/ Collection Agency / Consumer proposal / bankruptcy

Barriers to Entry - are there any major barriers to entry (technology, patents,

distribution, etc.)? CL must show ability/ Cl may have access to more creative ways to

solve debt

Market Size - how large is the total addressable market? Measured in terms of people

form census

Growth Rate - what is the anticipated growth rate for this segment? Based on the

delinquency rate

Profitability - are profit margins attractive? Based on OPD potential

Strategic & Technical Fit - how aligned is this market opportunity with our strategic

direction? All segments align with strategic direction

Capabilities - do you have the technical capabilities to compete in this market

effectively? Yes - 22 years of technical experience in administring OPD in Alberta

Maturity & Timing - how mature is this market? Is now the right time to enter? Factors

to include payment ability / creditor proof/ assets / resources

Segment Analysis:

Competitivenes

s

Market

Opportunity Attractiveness

Mar

ket

Segm

ents

Ability

to

Differe

ntiate

Comp

etitive

Intensi

ty

Bar

rier

s to

Ent

ry

Mar

ket

Siz

e

Gro

wth

Rat

e

Profit

ability

Strat

egic

&

Tech

nical

Fit

Capab

ilities

Mat

urit

y &

Timi

ng

Wei

ghting 5% 10% 15

%

15

% 15% 20% 10% 5% 5%

Marketing management

Fit

5% 10% 15

%

15

%

15

% 20% 10

% 5% 5% 10

0%

Ranking Criteria & Definitions:

Ability to Differentiate - is there any specific competitive advantage that one can

provide to this market? MM is the only organization who administers the OPD program

Competitive Intensity - are there few competitors actively engaged in this market

segment? Are they weak? We have strong competitors (help form parents/ DMP

programs/ Collection Agency / Consumer proposal / bankruptcy

Barriers to Entry - are there any major barriers to entry (technology, patents,

distribution, etc.)? CL must show ability/ Cl may have access to more creative ways to

solve debt

Market Size - how large is the total addressable market? Measured in terms of people

form census

Growth Rate - what is the anticipated growth rate for this segment? Based on the

delinquency rate

Profitability - are profit margins attractive? Based on OPD potential

Strategic & Technical Fit - how aligned is this market opportunity with our strategic

direction? All segments align with strategic direction

Capabilities - do you have the technical capabilities to compete in this market

effectively? Yes - 22 years of technical experience in administring OPD in Alberta

Maturity & Timing - how mature is this market? Is now the right time to enter? Factors

to include payment ability / creditor proof/ assets / resources

Segment Analysis:

Competitivenes

s

Market

Opportunity Attractiveness

Mar

ket

Segm

ents

Ability

to

Differe

ntiate

Comp

etitive

Intensi

ty

Bar

rier

s to

Ent

ry

Mar

ket

Siz

e

Gro

wth

Rat

e

Profit

ability

Strat

egic

&

Tech

nical

Fit

Capab

ilities

Mat

urit

y &

Timi

ng

Wei

ghting 5% 10% 15

%

15

% 15% 20% 10% 5% 5%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Marketing management

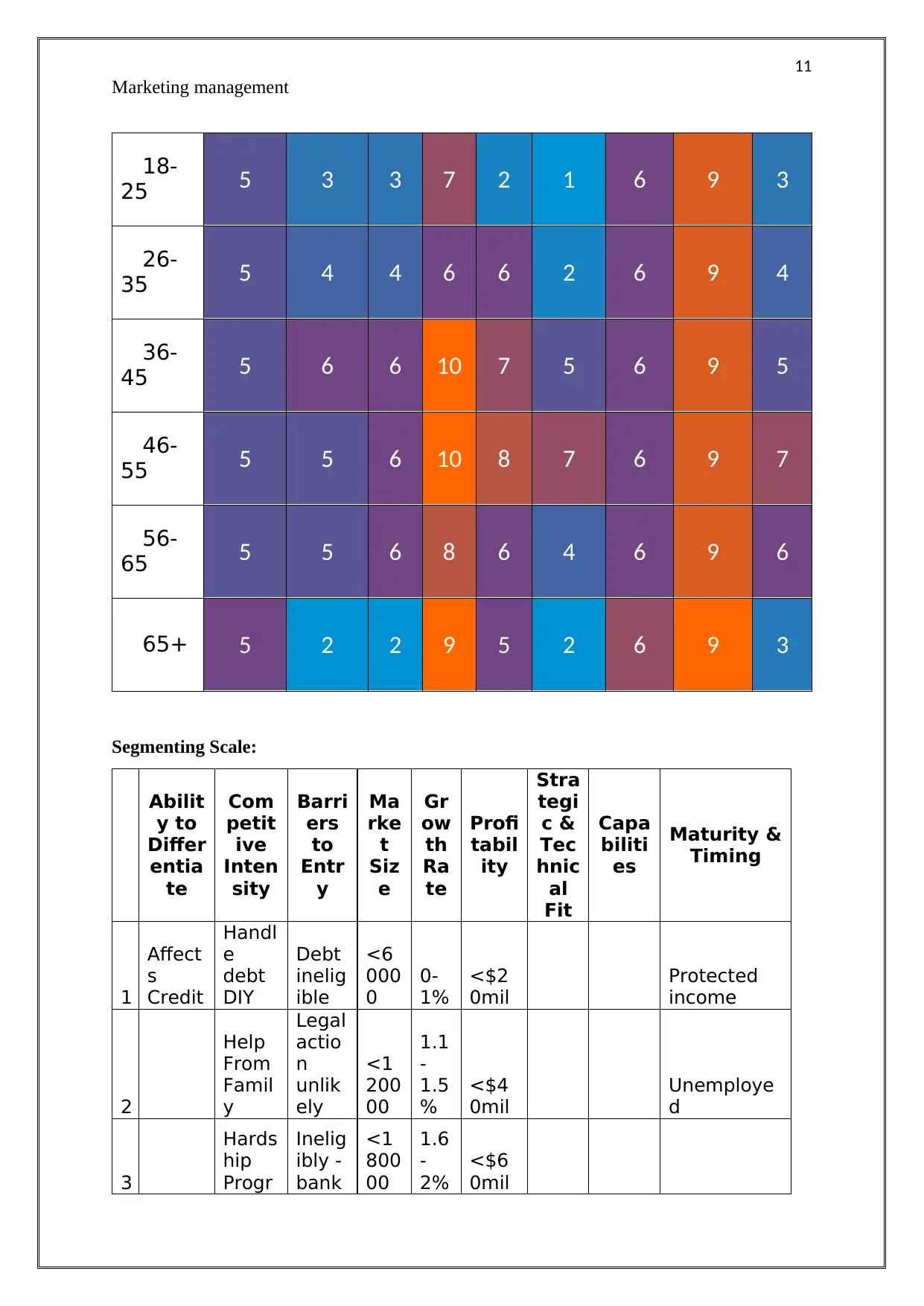

18-

25 5 3 3 7 2 1 6 9 3

26-

35 5 4 4 6 6 2 6 9 4

36-

45 5 6 6 10 7 5 6 9 5

46-

55 5 5 6 10 8 7 6 9 7

56-

65 5 5 6 8 6 4 6 9 6

65+ 5 2 2 9 5 2 6 9 3

Segmenting Scale:

Abilit

y to

Differ

entia

te

Com

petit

ive

Inten

sity

Barri

ers

to

Entr

y

Ma

rke

t

Siz

e

Gr

ow

th

Ra

te

Profi

tabil

ity

Stra

tegi

c &

Tec

hnic

al

Fit

Capa

biliti

es

Maturity &

Timing

1

Affect

s

Credit

Handl

e

debt

DIY

Debt

inelig

ible

<6

000

0

0-

1%

<$2

0mil

Protected

income

2

Help

From

Famil

y

Legal

actio

n

unlik

ely

<1

200

00

1.1

-

1.5

%

<$4

0mil

Unemploye

d

3

Hards

hip

Progr

Inelig

ibly -

bank

<1

800

00

1.6

-

2%

<$6

0mil

Marketing management

18-

25 5 3 3 7 2 1 6 9 3

26-

35 5 4 4 6 6 2 6 9 4

36-

45 5 6 6 10 7 5 6 9 5

46-

55 5 5 6 10 8 7 6 9 7

56-

65 5 5 6 8 6 4 6 9 6

65+ 5 2 2 9 5 2 6 9 3

Segmenting Scale:

Abilit

y to

Differ

entia

te

Com

petit

ive

Inten

sity

Barri

ers

to

Entr

y

Ma

rke

t

Siz

e

Gr

ow

th

Ra

te

Profi

tabil

ity

Stra

tegi

c &

Tec

hnic

al

Fit

Capa

biliti

es

Maturity &

Timing

1

Affect

s

Credit

Handl

e

debt

DIY

Debt

inelig

ible

<6

000

0

0-

1%

<$2

0mil

Protected

income

2

Help

From

Famil

y

Legal

actio

n

unlik

ely

<1

200

00

1.1

-

1.5

%

<$4

0mil

Unemploye

d

3

Hards

hip

Progr

Inelig

ibly -

bank

<1

800

00

1.6

-

2%

<$6

0mil

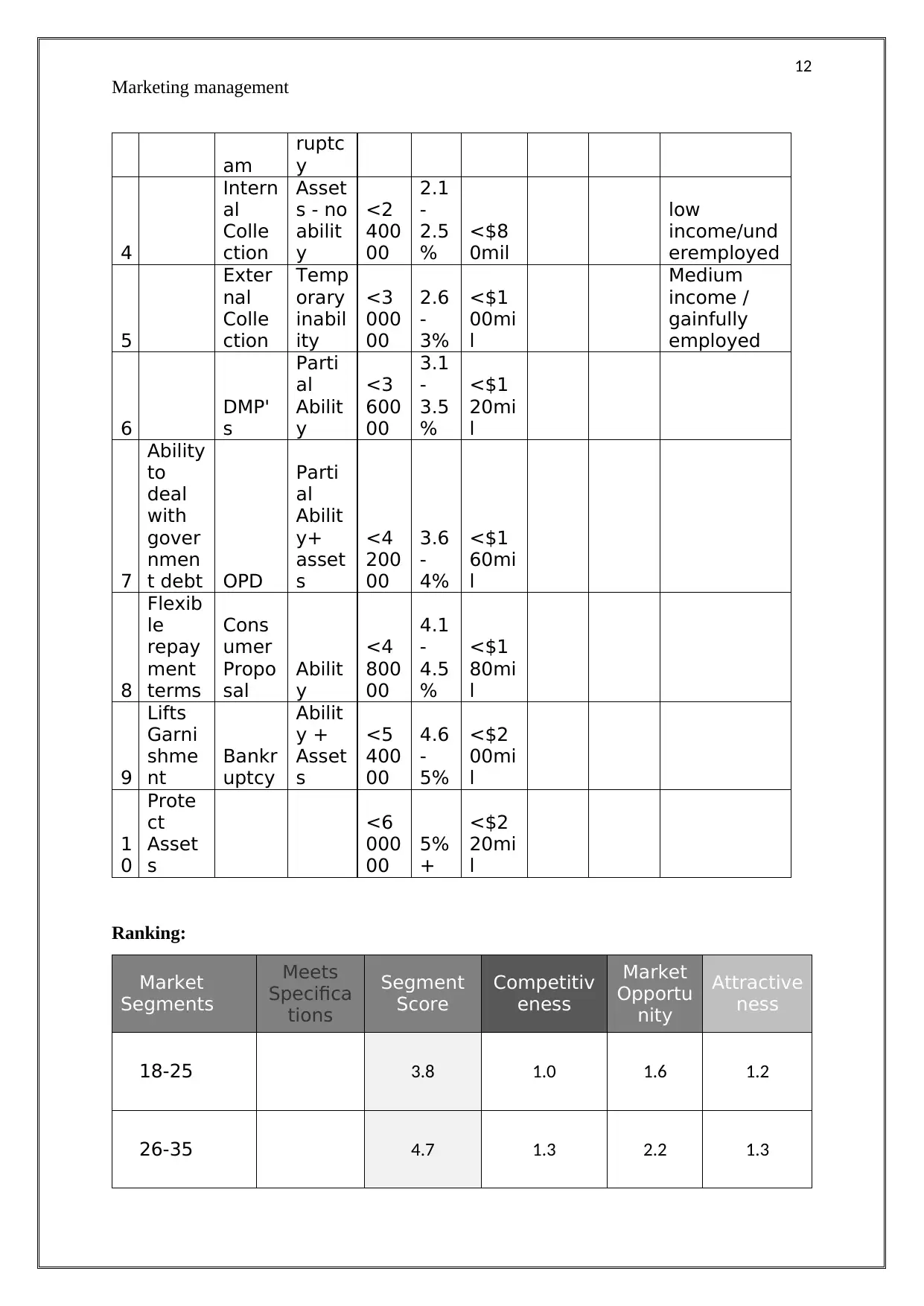

12

Marketing management

am

ruptc

y

4

Intern

al

Colle

ction

Asset

s - no

abilit

y

<2

400

00

2.1

-

2.5

%

<$8

0mil

low

income/und

eremployed

5

Exter

nal

Colle

ction

Temp

orary

inabil

ity

<3

000

00

2.6

-

3%

<$1

00mi

l

Medium

income /

gainfully

employed

6

DMP'

s

Parti

al

Abilit

y

<3

600

00

3.1

-

3.5

%

<$1

20mi

l

7

Ability

to

deal

with

gover

nmen

t debt OPD

Parti

al

Abilit

y+

asset

s

<4

200

00

3.6

-

4%

<$1

60mi

l

8

Flexib

le

repay

ment

terms

Cons

umer

Propo

sal

Abilit

y

<4

800

00

4.1

-

4.5

%

<$1

80mi

l

9

Lifts

Garni

shme

nt

Bankr

uptcy

Abilit

y +

Asset

s

<5

400

00

4.6

-

5%

<$2

00mi

l

1

0

Prote

ct

Asset

s

<6

000

00

5%

+

<$2

20mi

l

Ranking:

Market

Segments

Meets

Specifica

tions

Segment

Score

Competitiv

eness

Market

Opportu

nity

Attractive

ness

18-25 3.8 1.0 1.6 1.2

26-35 4.7 1.3 2.2 1.3

Marketing management

am

ruptc

y

4

Intern

al

Colle

ction

Asset

s - no

abilit

y

<2

400

00

2.1

-

2.5

%

<$8

0mil

low

income/und

eremployed

5

Exter

nal

Colle

ction

Temp

orary

inabil

ity

<3

000

00

2.6

-

3%

<$1

00mi

l

Medium

income /

gainfully

employed

6

DMP'

s

Parti

al

Abilit

y

<3

600

00

3.1

-

3.5

%

<$1

20mi

l

7

Ability

to

deal

with

gover

nmen

t debt OPD

Parti

al

Abilit

y+

asset

s

<4

200

00

3.6

-

4%

<$1

60mi

l

8

Flexib

le

repay

ment

terms

Cons

umer

Propo

sal

Abilit

y

<4

800

00

4.1

-

4.5

%

<$1

80mi

l

9

Lifts

Garni

shme

nt

Bankr

uptcy

Abilit

y +

Asset

s

<5

400

00

4.6

-

5%

<$2

00mi

l

1

0

Prote

ct

Asset

s

<6

000

00

5%

+

<$2

20mi

l

Ranking:

Market

Segments

Meets

Specifica

tions

Segment

Score

Competitiv

eness

Market

Opportu

nity

Attractive

ness

18-25 3.8 1.0 1.6 1.2

26-35 4.7 1.3 2.2 1.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.