Morden Engineering Case Study: Financial Appraisal and Decision Making

VerifiedAdded on 2020/06/05

|13

|3111

|35

Report

AI Summary

This report analyzes the make-or-buy decision faced by Morden Engineering, a company considering whether to continue producing a product component internally or outsource its manufacturing to Clyde Engineers. The report critically evaluates arguments from purchasing and production managers, highlighting key issues such as machinery costs, depreciation, and variable costs. It applies capital budgeting techniques, including payback period, average rate of return, net present value (NPV), and internal rate of return (IRR), to assess the financial viability of each option. The analysis considers factors like initial investment, sales, production costs, depreciation, and tax implications to arrive at a final decision. The report also addresses potential risks and alternatives, providing a comprehensive financial appraisal of the situation. The report concludes with a recommendation based on the financial analysis and offers valuable insights into the decision-making process.

International Finance & Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.......................................................................................................................................................................................1

1. Critical evaluation of arguments utilized by Purchasing and Production Managers...........................................................................1

2. Important issues in the case and factors should be considered in financial analysis...........................................................................3

3. Decision of Morden Engineering with evidence from financial appraisal..........................................................................................4

4. Possible Risk of adopting recommendation and alternatives...............................................................................................................8

CONCLUSION............................................................................................................................................................................................9

REFERENCES..........................................................................................................................................................................................10

INTRODUCTION.......................................................................................................................................................................................1

1. Critical evaluation of arguments utilized by Purchasing and Production Managers...........................................................................1

2. Important issues in the case and factors should be considered in financial analysis...........................................................................3

3. Decision of Morden Engineering with evidence from financial appraisal..........................................................................................4

4. Possible Risk of adopting recommendation and alternatives...............................................................................................................8

CONCLUSION............................................................................................................................................................................................9

REFERENCES..........................................................................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

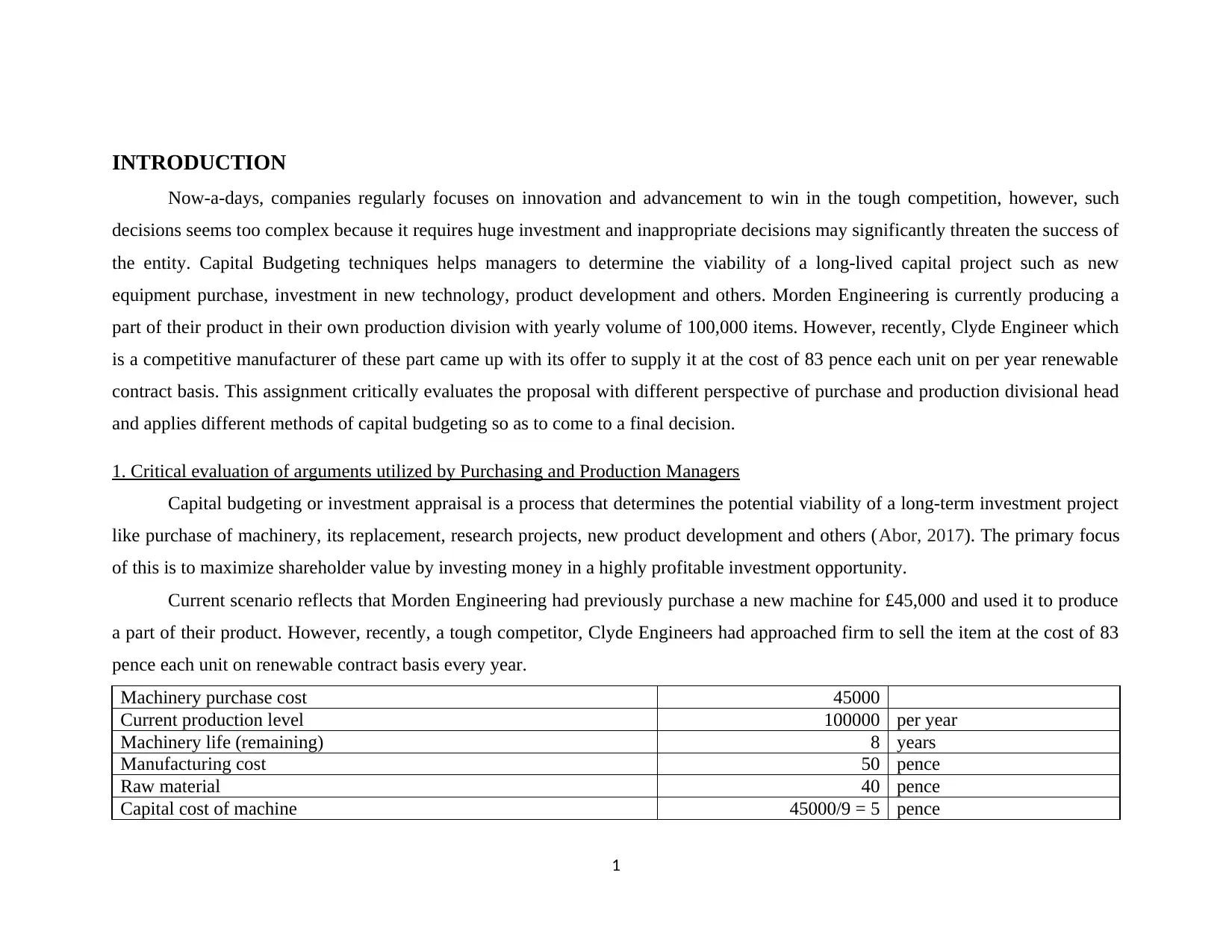

INTRODUCTION

Now-a-days, companies regularly focuses on innovation and advancement to win in the tough competition, however, such

decisions seems too complex because it requires huge investment and inappropriate decisions may significantly threaten the success of

the entity. Capital Budgeting techniques helps managers to determine the viability of a long-lived capital project such as new

equipment purchase, investment in new technology, product development and others. Morden Engineering is currently producing a

part of their product in their own production division with yearly volume of 100,000 items. However, recently, Clyde Engineer which

is a competitive manufacturer of these part came up with its offer to supply it at the cost of 83 pence each unit on per year renewable

contract basis. This assignment critically evaluates the proposal with different perspective of purchase and production divisional head

and applies different methods of capital budgeting so as to come to a final decision.

1. Critical evaluation of arguments utilized by Purchasing and Production Managers

Capital budgeting or investment appraisal is a process that determines the potential viability of a long-term investment project

like purchase of machinery, its replacement, research projects, new product development and others (Abor, 2017). The primary focus

of this is to maximize shareholder value by investing money in a highly profitable investment opportunity.

Current scenario reflects that Morden Engineering had previously purchase a new machine for £45,000 and used it to produce

a part of their product. However, recently, a tough competitor, Clyde Engineers had approached firm to sell the item at the cost of 83

pence each unit on renewable contract basis every year.

Machinery purchase cost 45000

Current production level 100000 per year

Machinery life (remaining) 8 years

Manufacturing cost 50 pence

Raw material 40 pence

Capital cost of machine 45000/9 = 5 pence

1

Now-a-days, companies regularly focuses on innovation and advancement to win in the tough competition, however, such

decisions seems too complex because it requires huge investment and inappropriate decisions may significantly threaten the success of

the entity. Capital Budgeting techniques helps managers to determine the viability of a long-lived capital project such as new

equipment purchase, investment in new technology, product development and others. Morden Engineering is currently producing a

part of their product in their own production division with yearly volume of 100,000 items. However, recently, Clyde Engineer which

is a competitive manufacturer of these part came up with its offer to supply it at the cost of 83 pence each unit on per year renewable

contract basis. This assignment critically evaluates the proposal with different perspective of purchase and production divisional head

and applies different methods of capital budgeting so as to come to a final decision.

1. Critical evaluation of arguments utilized by Purchasing and Production Managers

Capital budgeting or investment appraisal is a process that determines the potential viability of a long-term investment project

like purchase of machinery, its replacement, research projects, new product development and others (Abor, 2017). The primary focus

of this is to maximize shareholder value by investing money in a highly profitable investment opportunity.

Current scenario reflects that Morden Engineering had previously purchase a new machine for £45,000 and used it to produce

a part of their product. However, recently, a tough competitor, Clyde Engineers had approached firm to sell the item at the cost of 83

pence each unit on renewable contract basis every year.

Machinery purchase cost 45000

Current production level 100000 per year

Machinery life (remaining) 8 years

Manufacturing cost 50 pence

Raw material 40 pence

Capital cost of machine 45000/9 = 5 pence

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

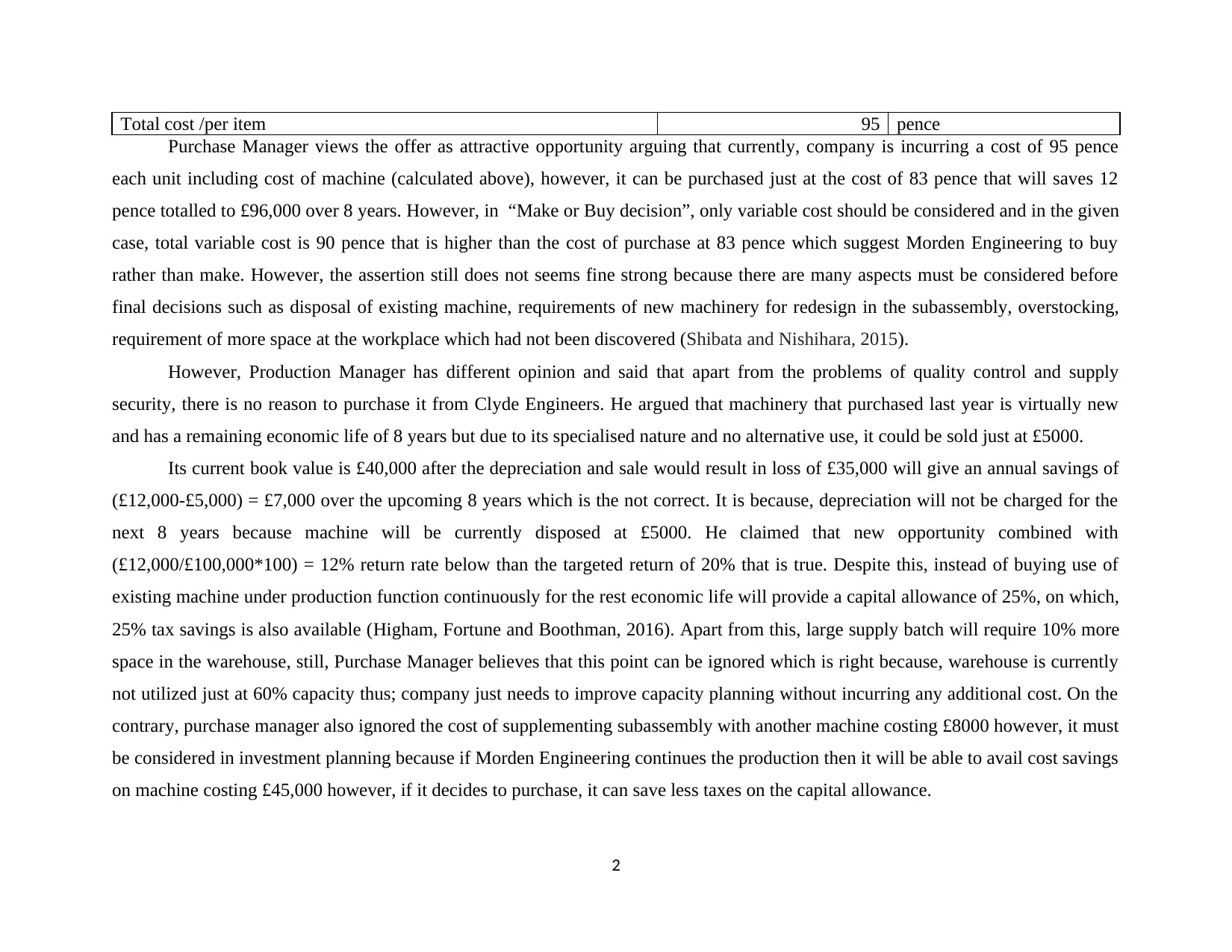

Total cost /per item 95 pence

Purchase Manager views the offer as attractive opportunity arguing that currently, company is incurring a cost of 95 pence

each unit including cost of machine (calculated above), however, it can be purchased just at the cost of 83 pence that will saves 12

pence totalled to £96,000 over 8 years. However, in “Make or Buy decision”, only variable cost should be considered and in the given

case, total variable cost is 90 pence that is higher than the cost of purchase at 83 pence which suggest Morden Engineering to buy

rather than make. However, the assertion still does not seems fine strong because there are many aspects must be considered before

final decisions such as disposal of existing machine, requirements of new machinery for redesign in the subassembly, overstocking,

requirement of more space at the workplace which had not been discovered (Shibata and Nishihara, 2015).

However, Production Manager has different opinion and said that apart from the problems of quality control and supply

security, there is no reason to purchase it from Clyde Engineers. He argued that machinery that purchased last year is virtually new

and has a remaining economic life of 8 years but due to its specialised nature and no alternative use, it could be sold just at £5000.

Its current book value is £40,000 after the depreciation and sale would result in loss of £35,000 will give an annual savings of

(£12,000-£5,000) = £7,000 over the upcoming 8 years which is the not correct. It is because, depreciation will not be charged for the

next 8 years because machine will be currently disposed at £5000. He claimed that new opportunity combined with

(£12,000/£100,000*100) = 12% return rate below than the targeted return of 20% that is true. Despite this, instead of buying use of

existing machine under production function continuously for the rest economic life will provide a capital allowance of 25%, on which,

25% tax savings is also available (Higham, Fortune and Boothman, 2016). Apart from this, large supply batch will require 10% more

space in the warehouse, still, Purchase Manager believes that this point can be ignored which is right because, warehouse is currently

not utilized just at 60% capacity thus; company just needs to improve capacity planning without incurring any additional cost. On the

contrary, purchase manager also ignored the cost of supplementing subassembly with another machine costing £8000 however, it must

be considered in investment planning because if Morden Engineering continues the production then it will be able to avail cost savings

on machine costing £45,000 however, if it decides to purchase, it can save less taxes on the capital allowance.

2

Purchase Manager views the offer as attractive opportunity arguing that currently, company is incurring a cost of 95 pence

each unit including cost of machine (calculated above), however, it can be purchased just at the cost of 83 pence that will saves 12

pence totalled to £96,000 over 8 years. However, in “Make or Buy decision”, only variable cost should be considered and in the given

case, total variable cost is 90 pence that is higher than the cost of purchase at 83 pence which suggest Morden Engineering to buy

rather than make. However, the assertion still does not seems fine strong because there are many aspects must be considered before

final decisions such as disposal of existing machine, requirements of new machinery for redesign in the subassembly, overstocking,

requirement of more space at the workplace which had not been discovered (Shibata and Nishihara, 2015).

However, Production Manager has different opinion and said that apart from the problems of quality control and supply

security, there is no reason to purchase it from Clyde Engineers. He argued that machinery that purchased last year is virtually new

and has a remaining economic life of 8 years but due to its specialised nature and no alternative use, it could be sold just at £5000.

Its current book value is £40,000 after the depreciation and sale would result in loss of £35,000 will give an annual savings of

(£12,000-£5,000) = £7,000 over the upcoming 8 years which is the not correct. It is because, depreciation will not be charged for the

next 8 years because machine will be currently disposed at £5000. He claimed that new opportunity combined with

(£12,000/£100,000*100) = 12% return rate below than the targeted return of 20% that is true. Despite this, instead of buying use of

existing machine under production function continuously for the rest economic life will provide a capital allowance of 25%, on which,

25% tax savings is also available (Higham, Fortune and Boothman, 2016). Apart from this, large supply batch will require 10% more

space in the warehouse, still, Purchase Manager believes that this point can be ignored which is right because, warehouse is currently

not utilized just at 60% capacity thus; company just needs to improve capacity planning without incurring any additional cost. On the

contrary, purchase manager also ignored the cost of supplementing subassembly with another machine costing £8000 however, it must

be considered in investment planning because if Morden Engineering continues the production then it will be able to avail cost savings

on machine costing £45,000 however, if it decides to purchase, it can save less taxes on the capital allowance.

2

2. Important issues in the case and factors should be considered in financial analysis

There are number of key issues exist in the case to decide that whether it should purchase the component or should buy it from

the outside supplier that is presented below:

One of the most important issues is that Morden Engineering had purchased new machinery just before 1 year at a cost of

£45,000 and it is in well condition now. However, if it decides to purchase the product from Clyde Engineers, then it required

to be sold, however, due to its specialised nature, it cannot be used for alternative purpose. Therefore, company will get just

£5000 on its disposal.

Another thing is Morden Engineering need to buy new machinery for the subassembly that would cost firm £8000.

As supplier charge a condition that minimum supply in every batch would be of 30,000 units with an average stockholding of

15000 parts throughout the year against the current stocking level of two weeks material supply. Thus, overstocking may be a

problem in future due to which, firm will incur high carrying cost.

Essential factors in the financial analysis of investment opportunity

Investment proposals also consider those aspects that would either results in cash inflow or outflow. As reflected in the case of

Morden Engineering, requirement of new machinery in the subassembly division will require an investment of £8000 that must be

considered. Moreover, disposal of existing machine at a very less value of £5000 only also needs to be incorporated in the financial

analysis. Apart from this, as said that Clyde Engineers manufactures the item using advanced technologies therefore, the product may

vary by 4 mm in length. It do not cause any quality concerns therefore, there is no need to consider such aspect. In addition, the

difference between the tax savings on current machine and new machine must be taken into account (Li and Trutnevyte, 2017).

Despite this, the issue of large average stocking of 15,000 parts throughout the year needs to be valued because company

would need to spend more on its holding. However, as currently warehouse just uses 60% capacity and additional stockholding would

require 10% more therefore, it would not incur any further cost and do not requires warehouse extension. It just require sound capacity

consumption plan to use warehouse at its full (100%) capacity (Gitman, Juchau and Flanagan, 2015). Thus, the warehouse extension

3

There are number of key issues exist in the case to decide that whether it should purchase the component or should buy it from

the outside supplier that is presented below:

One of the most important issues is that Morden Engineering had purchased new machinery just before 1 year at a cost of

£45,000 and it is in well condition now. However, if it decides to purchase the product from Clyde Engineers, then it required

to be sold, however, due to its specialised nature, it cannot be used for alternative purpose. Therefore, company will get just

£5000 on its disposal.

Another thing is Morden Engineering need to buy new machinery for the subassembly that would cost firm £8000.

As supplier charge a condition that minimum supply in every batch would be of 30,000 units with an average stockholding of

15000 parts throughout the year against the current stocking level of two weeks material supply. Thus, overstocking may be a

problem in future due to which, firm will incur high carrying cost.

Essential factors in the financial analysis of investment opportunity

Investment proposals also consider those aspects that would either results in cash inflow or outflow. As reflected in the case of

Morden Engineering, requirement of new machinery in the subassembly division will require an investment of £8000 that must be

considered. Moreover, disposal of existing machine at a very less value of £5000 only also needs to be incorporated in the financial

analysis. Apart from this, as said that Clyde Engineers manufactures the item using advanced technologies therefore, the product may

vary by 4 mm in length. It do not cause any quality concerns therefore, there is no need to consider such aspect. In addition, the

difference between the tax savings on current machine and new machine must be taken into account (Li and Trutnevyte, 2017).

Despite this, the issue of large average stocking of 15,000 parts throughout the year needs to be valued because company

would need to spend more on its holding. However, as currently warehouse just uses 60% capacity and additional stockholding would

require 10% more therefore, it would not incur any further cost and do not requires warehouse extension. It just require sound capacity

consumption plan to use warehouse at its full (100%) capacity (Gitman, Juchau and Flanagan, 2015). Thus, the warehouse extension

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that is planned for the next 4 years should be avoided. In addition, existing machine operator cannot be redundant for another eight

years because of the specified contractual condition. Therefore, he needs to be shift to another department at the current salary of

£8000 which is regardless to the make or buy decision because in both the situation, salary does not fluctuate.

3. Decision of Morden Engineering with evidence from financial appraisal

As in the case, different parties like purchase head and production manager has distinctive opinion whether or not to proceed

with the new proposal made by Clyde Engineers. In order to reach a final decision, investment appraisal techniques are so helpful that

assess and examines the worth of the project combining with different methods of investment appraisal. There are numbers of

techniques available to the Morden Engineering which must be applied to judge whether the project seems viable or not can be

classified into two, discounted or non-discounted techniques examined below:

Payback period: This method is used to identify the recovery period of initial investment which states that how long the

investment project will take to recoup its beginning outlay (Baum and Crosby, 2014).

Strengths:

Helps to determine recovery period

Easy to compute

Weakness:

No use of discounting means did not consider time value of money

Do not focus on the cash flows for subsequent period

It does not examine the pattern of cash flows

Average rate of return: This method is used to determine the rate of return on the investment by dividend average accounting

profit with the initial investment (Gotze, Northcott and Schuster, 2016).

ARR = Average annual profit/Initial investment

Strengths:

4

years because of the specified contractual condition. Therefore, he needs to be shift to another department at the current salary of

£8000 which is regardless to the make or buy decision because in both the situation, salary does not fluctuate.

3. Decision of Morden Engineering with evidence from financial appraisal

As in the case, different parties like purchase head and production manager has distinctive opinion whether or not to proceed

with the new proposal made by Clyde Engineers. In order to reach a final decision, investment appraisal techniques are so helpful that

assess and examines the worth of the project combining with different methods of investment appraisal. There are numbers of

techniques available to the Morden Engineering which must be applied to judge whether the project seems viable or not can be

classified into two, discounted or non-discounted techniques examined below:

Payback period: This method is used to identify the recovery period of initial investment which states that how long the

investment project will take to recoup its beginning outlay (Baum and Crosby, 2014).

Strengths:

Helps to determine recovery period

Easy to compute

Weakness:

No use of discounting means did not consider time value of money

Do not focus on the cash flows for subsequent period

It does not examine the pattern of cash flows

Average rate of return: This method is used to determine the rate of return on the investment by dividend average accounting

profit with the initial investment (Gotze, Northcott and Schuster, 2016).

ARR = Average annual profit/Initial investment

Strengths:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Helps to determine the return on investment

Useful method to meet shareholders expectations

Weaknesses:

It uses accounting return rather than net cash flow which provides artificial return because it incorporates all those transactions

which have no impact over cash.

Likewise to Payback period, the method did not value the time value of the currency which is really important.

Net present value: The method first prefers incorporating a discounting factor to determine the current/discounted value of

cash inflows and outflows (Horngren and et.al., 2013). The sum of discounted cash inflows is subtracted from the outlay which is called

NPV.

Strengths:

The most important strength of the method is time value of money is taken into account by using discounting factor to

determine the current value of anticipated inflows and outflows.

It provides insight into the future year return on the project.

Weaknesses:

It is not an easy task to identify the correct discounting factor because fluctuation in external market like inflation, interest rate

and others affects it.

Actual cash flows may be vary from the anticipated cash flows and influence the results.

Internal rate of return: This is another method which helps to know the rate at which every long-term investment project

gives zero return means NPV is null (Greenbaum, Thakor and Boot, 2015). It is also called as the yield n investment which denotes the

discounting rate equating present value of cash inflows and beginning outlay.

Strengths:

Considers time value of currency

5

Useful method to meet shareholders expectations

Weaknesses:

It uses accounting return rather than net cash flow which provides artificial return because it incorporates all those transactions

which have no impact over cash.

Likewise to Payback period, the method did not value the time value of the currency which is really important.

Net present value: The method first prefers incorporating a discounting factor to determine the current/discounted value of

cash inflows and outflows (Horngren and et.al., 2013). The sum of discounted cash inflows is subtracted from the outlay which is called

NPV.

Strengths:

The most important strength of the method is time value of money is taken into account by using discounting factor to

determine the current value of anticipated inflows and outflows.

It provides insight into the future year return on the project.

Weaknesses:

It is not an easy task to identify the correct discounting factor because fluctuation in external market like inflation, interest rate

and others affects it.

Actual cash flows may be vary from the anticipated cash flows and influence the results.

Internal rate of return: This is another method which helps to know the rate at which every long-term investment project

gives zero return means NPV is null (Greenbaum, Thakor and Boot, 2015). It is also called as the yield n investment which denotes the

discounting rate equating present value of cash inflows and beginning outlay.

Strengths:

Considers time value of currency

5

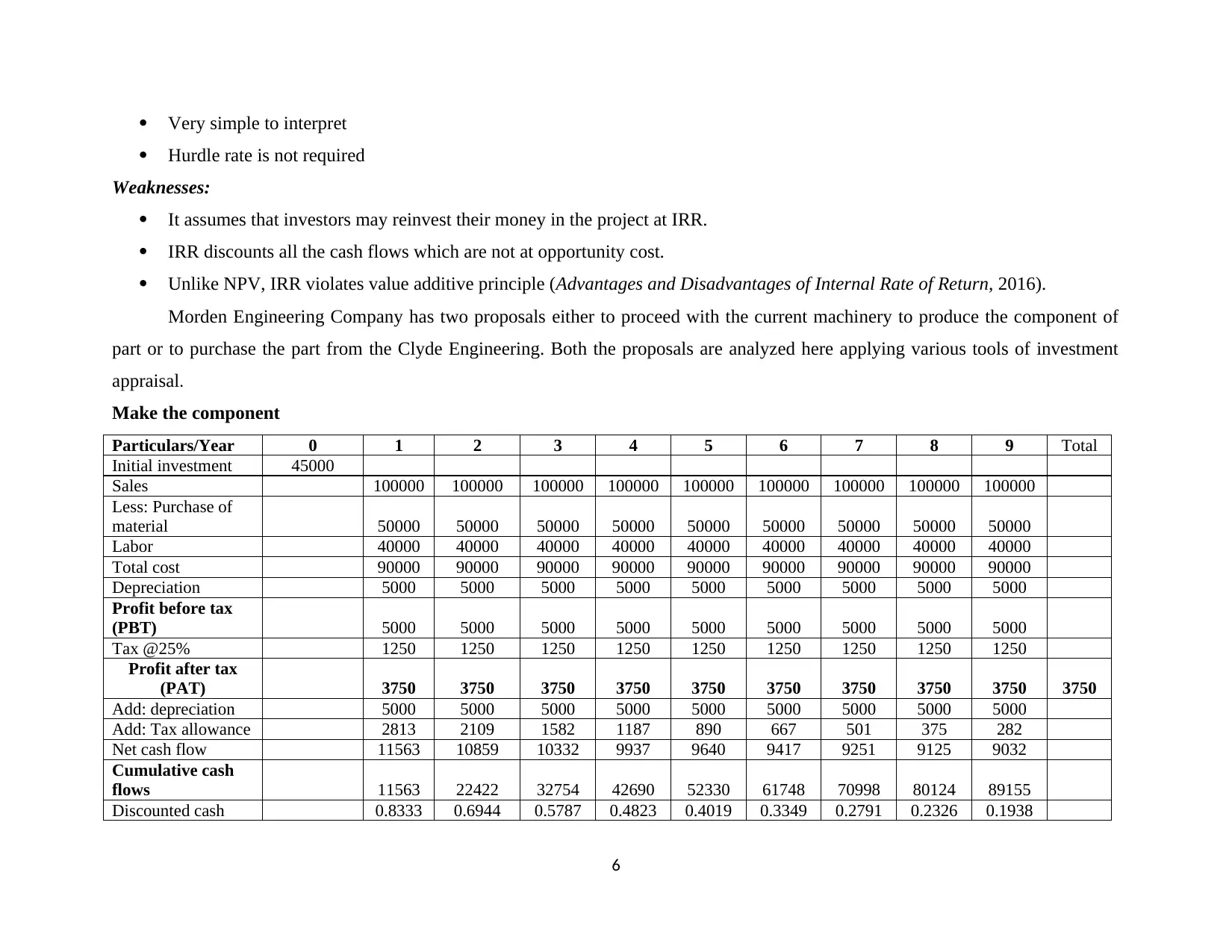

Very simple to interpret

Hurdle rate is not required

Weaknesses:

It assumes that investors may reinvest their money in the project at IRR.

IRR discounts all the cash flows which are not at opportunity cost.

Unlike NPV, IRR violates value additive principle (Advantages and Disadvantages of Internal Rate of Return, 2016).

Morden Engineering Company has two proposals either to proceed with the current machinery to produce the component of

part or to purchase the part from the Clyde Engineering. Both the proposals are analyzed here applying various tools of investment

appraisal.

Make the component

Particulars/Year 0 1 2 3 4 5 6 7 8 9 Total

Initial investment 45000

Sales 100000 100000 100000 100000 100000 100000 100000 100000 100000

Less: Purchase of

material 50000 50000 50000 50000 50000 50000 50000 50000 50000

Labor 40000 40000 40000 40000 40000 40000 40000 40000 40000

Total cost 90000 90000 90000 90000 90000 90000 90000 90000 90000

Depreciation 5000 5000 5000 5000 5000 5000 5000 5000 5000

Profit before tax

(PBT) 5000 5000 5000 5000 5000 5000 5000 5000 5000

Tax @25% 1250 1250 1250 1250 1250 1250 1250 1250 1250

Profit after tax

(PAT) 3750 3750 3750 3750 3750 3750 3750 3750 3750 3750

Add: depreciation 5000 5000 5000 5000 5000 5000 5000 5000 5000

Add: Tax allowance 2813 2109 1582 1187 890 667 501 375 282

Net cash flow 11563 10859 10332 9937 9640 9417 9251 9125 9032

Cumulative cash

flows 11563 22422 32754 42690 52330 61748 70998 80124 89155

Discounted cash 0.8333 0.6944 0.5787 0.4823 0.4019 0.3349 0.2791 0.2326 0.1938

6

Hurdle rate is not required

Weaknesses:

It assumes that investors may reinvest their money in the project at IRR.

IRR discounts all the cash flows which are not at opportunity cost.

Unlike NPV, IRR violates value additive principle (Advantages and Disadvantages of Internal Rate of Return, 2016).

Morden Engineering Company has two proposals either to proceed with the current machinery to produce the component of

part or to purchase the part from the Clyde Engineering. Both the proposals are analyzed here applying various tools of investment

appraisal.

Make the component

Particulars/Year 0 1 2 3 4 5 6 7 8 9 Total

Initial investment 45000

Sales 100000 100000 100000 100000 100000 100000 100000 100000 100000

Less: Purchase of

material 50000 50000 50000 50000 50000 50000 50000 50000 50000

Labor 40000 40000 40000 40000 40000 40000 40000 40000 40000

Total cost 90000 90000 90000 90000 90000 90000 90000 90000 90000

Depreciation 5000 5000 5000 5000 5000 5000 5000 5000 5000

Profit before tax

(PBT) 5000 5000 5000 5000 5000 5000 5000 5000 5000

Tax @25% 1250 1250 1250 1250 1250 1250 1250 1250 1250

Profit after tax

(PAT) 3750 3750 3750 3750 3750 3750 3750 3750 3750 3750

Add: depreciation 5000 5000 5000 5000 5000 5000 5000 5000 5000

Add: Tax allowance 2813 2109 1582 1187 890 667 501 375 282

Net cash flow 11563 10859 10332 9937 9640 9417 9251 9125 9032

Cumulative cash

flows 11563 22422 32754 42690 52330 61748 70998 80124 89155

Discounted cash 0.8333 0.6944 0.5787 0.4823 0.4019 0.3349 0.2791 0.2326 0.1938

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

flows @ 20%

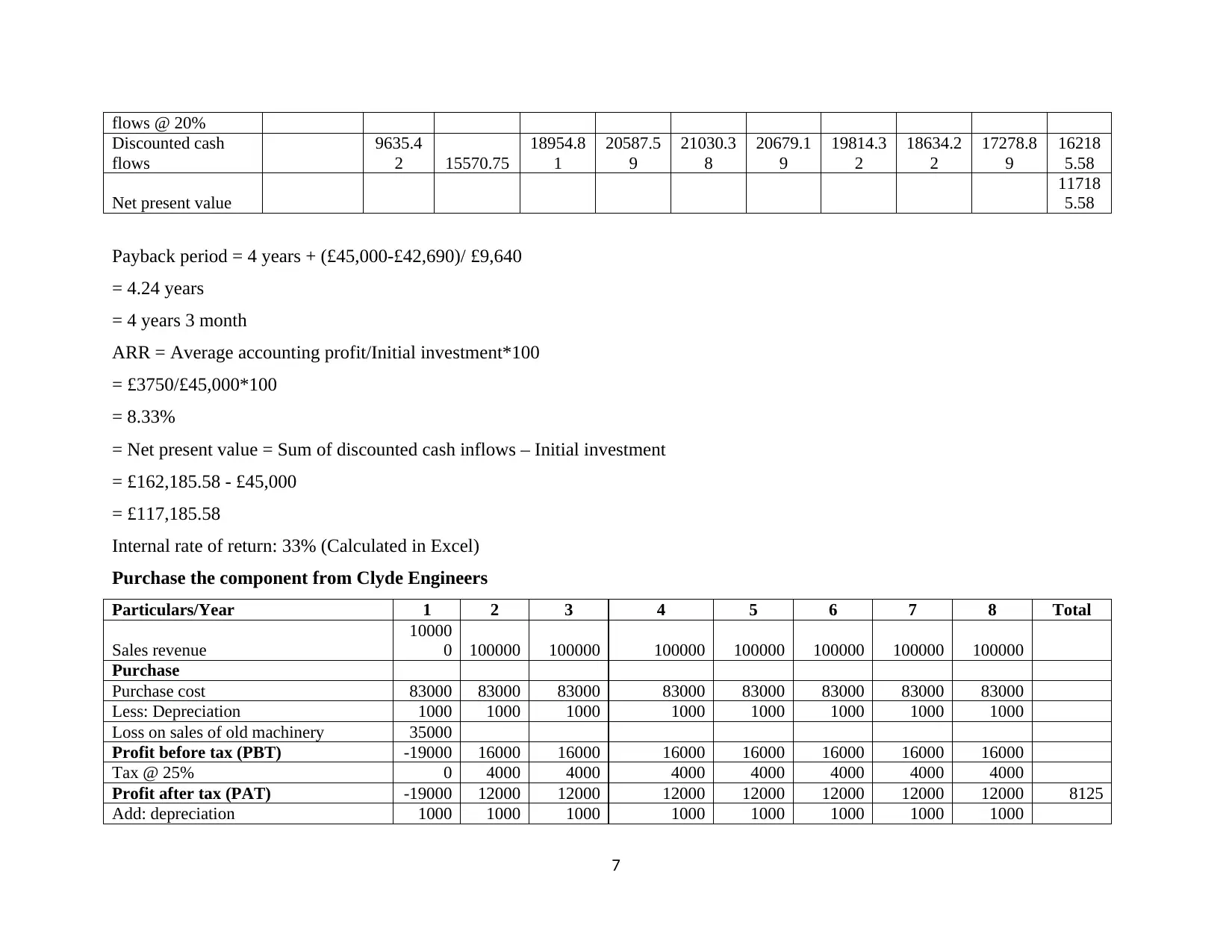

Discounted cash

flows

9635.4

2 15570.75

18954.8

1

20587.5

9

21030.3

8

20679.1

9

19814.3

2

18634.2

2

17278.8

9

16218

5.58

Net present value

11718

5.58

Payback period = 4 years + (£45,000-£42,690)/ £9,640

= 4.24 years

= 4 years 3 month

ARR = Average accounting profit/Initial investment*100

= £3750/£45,000*100

= 8.33%

= Net present value = Sum of discounted cash inflows – Initial investment

= £162,185.58 - £45,000

= £117,185.58

Internal rate of return: 33% (Calculated in Excel)

Purchase the component from Clyde Engineers

Particulars/Year 1 2 3 4 5 6 7 8 Total

Sales revenue

10000

0 100000 100000 100000 100000 100000 100000 100000

Purchase

Purchase cost 83000 83000 83000 83000 83000 83000 83000 83000

Less: Depreciation 1000 1000 1000 1000 1000 1000 1000 1000

Loss on sales of old machinery 35000

Profit before tax (PBT) -19000 16000 16000 16000 16000 16000 16000 16000

Tax @ 25% 0 4000 4000 4000 4000 4000 4000 4000

Profit after tax (PAT) -19000 12000 12000 12000 12000 12000 12000 12000 8125

Add: depreciation 1000 1000 1000 1000 1000 1000 1000 1000

7

Discounted cash

flows

9635.4

2 15570.75

18954.8

1

20587.5

9

21030.3

8

20679.1

9

19814.3

2

18634.2

2

17278.8

9

16218

5.58

Net present value

11718

5.58

Payback period = 4 years + (£45,000-£42,690)/ £9,640

= 4.24 years

= 4 years 3 month

ARR = Average accounting profit/Initial investment*100

= £3750/£45,000*100

= 8.33%

= Net present value = Sum of discounted cash inflows – Initial investment

= £162,185.58 - £45,000

= £117,185.58

Internal rate of return: 33% (Calculated in Excel)

Purchase the component from Clyde Engineers

Particulars/Year 1 2 3 4 5 6 7 8 Total

Sales revenue

10000

0 100000 100000 100000 100000 100000 100000 100000

Purchase

Purchase cost 83000 83000 83000 83000 83000 83000 83000 83000

Less: Depreciation 1000 1000 1000 1000 1000 1000 1000 1000

Loss on sales of old machinery 35000

Profit before tax (PBT) -19000 16000 16000 16000 16000 16000 16000 16000

Tax @ 25% 0 4000 4000 4000 4000 4000 4000 4000

Profit after tax (PAT) -19000 12000 12000 12000 12000 12000 12000 12000 8125

Add: depreciation 1000 1000 1000 1000 1000 1000 1000 1000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

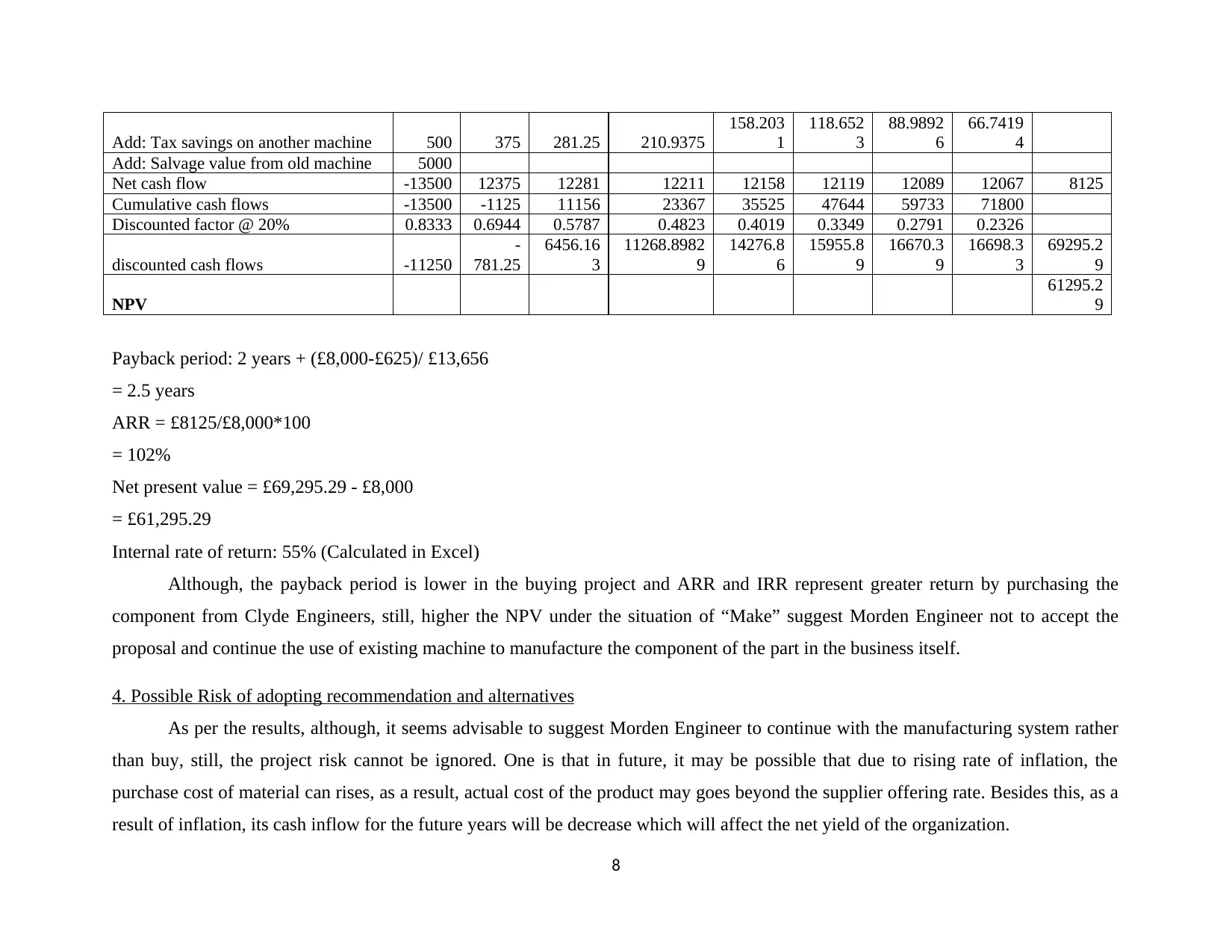

Add: Tax savings on another machine 500 375 281.25 210.9375

158.203

1

118.652

3

88.9892

6

66.7419

4

Add: Salvage value from old machine 5000

Net cash flow -13500 12375 12281 12211 12158 12119 12089 12067 8125

Cumulative cash flows -13500 -1125 11156 23367 35525 47644 59733 71800

Discounted factor @ 20% 0.8333 0.6944 0.5787 0.4823 0.4019 0.3349 0.2791 0.2326

discounted cash flows -11250

-

781.25

6456.16

3

11268.8982

9

14276.8

6

15955.8

9

16670.3

9

16698.3

3

69295.2

9

NPV

61295.2

9

Payback period: 2 years + (£8,000-£625)/ £13,656

= 2.5 years

ARR = £8125/£8,000*100

= 102%

Net present value = £69,295.29 - £8,000

= £61,295.29

Internal rate of return: 55% (Calculated in Excel)

Although, the payback period is lower in the buying project and ARR and IRR represent greater return by purchasing the

component from Clyde Engineers, still, higher the NPV under the situation of “Make” suggest Morden Engineer not to accept the

proposal and continue the use of existing machine to manufacture the component of the part in the business itself.

4. Possible Risk of adopting recommendation and alternatives

As per the results, although, it seems advisable to suggest Morden Engineer to continue with the manufacturing system rather

than buy, still, the project risk cannot be ignored. One is that in future, it may be possible that due to rising rate of inflation, the

purchase cost of material can rises, as a result, actual cost of the product may goes beyond the supplier offering rate. Besides this, as a

result of inflation, its cash inflow for the future years will be decrease which will affect the net yield of the organization.

8

158.203

1

118.652

3

88.9892

6

66.7419

4

Add: Salvage value from old machine 5000

Net cash flow -13500 12375 12281 12211 12158 12119 12089 12067 8125

Cumulative cash flows -13500 -1125 11156 23367 35525 47644 59733 71800

Discounted factor @ 20% 0.8333 0.6944 0.5787 0.4823 0.4019 0.3349 0.2791 0.2326

discounted cash flows -11250

-

781.25

6456.16

3

11268.8982

9

14276.8

6

15955.8

9

16670.3

9

16698.3

3

69295.2

9

NPV

61295.2

9

Payback period: 2 years + (£8,000-£625)/ £13,656

= 2.5 years

ARR = £8125/£8,000*100

= 102%

Net present value = £69,295.29 - £8,000

= £61,295.29

Internal rate of return: 55% (Calculated in Excel)

Although, the payback period is lower in the buying project and ARR and IRR represent greater return by purchasing the

component from Clyde Engineers, still, higher the NPV under the situation of “Make” suggest Morden Engineer not to accept the

proposal and continue the use of existing machine to manufacture the component of the part in the business itself.

4. Possible Risk of adopting recommendation and alternatives

As per the results, although, it seems advisable to suggest Morden Engineer to continue with the manufacturing system rather

than buy, still, the project risk cannot be ignored. One is that in future, it may be possible that due to rising rate of inflation, the

purchase cost of material can rises, as a result, actual cost of the product may goes beyond the supplier offering rate. Besides this, as a

result of inflation, its cash inflow for the future years will be decrease which will affect the net yield of the organization.

8

As an alternative, it is suggested to the Morden Engineering to take into account the impact of inflation also on their future

year profit so as to judge the viability of the project. Besides this, company can also create an agreement with the material supplier so

as to prevent itself against the rise in the cost. Sensitivity analysis must be inform to judge the impact of such factors before finalizing

a decision.

CONCLUSION

The results of the study concluded that although, there are number of methods for investment appraisal, still, firm must go for

discounted method that is NPV and IRR because they consider time value of money. The application of these methods for both make

and buy conditions suggested Morden Engineering to not to buy it from Clyde Engineering and continue its production. It is because,

if company uses the existing machine continuously for the remaining lifetime than it will gain more yield.

9

year profit so as to judge the viability of the project. Besides this, company can also create an agreement with the material supplier so

as to prevent itself against the rise in the cost. Sensitivity analysis must be inform to judge the impact of such factors before finalizing

a decision.

CONCLUSION

The results of the study concluded that although, there are number of methods for investment appraisal, still, firm must go for

discounted method that is NPV and IRR because they consider time value of money. The application of these methods for both make

and buy conditions suggested Morden Engineering to not to buy it from Clyde Engineering and continue its production. It is because,

if company uses the existing machine continuously for the remaining lifetime than it will gain more yield.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.