Finance and Mortgage Broking Tasks: Client Relationships

VerifiedAdded on 2023/01/12

|23

|6945

|21

Homework Assignment

AI Summary

This assignment delves into the core aspects of finance and mortgage broking, encompassing a range of tasks designed to assess understanding of client relationships, credit management, and loan application processes. The initial tasks focus on establishing and nurturing professional relationships with clients, other professionals, and third-party referrers, emphasizing the importance of demonstrating competence, using appropriate language in diverse cultural contexts, and building effective business networks. Subsequent tasks explore the effective use of credit, including financing options for clients, such as personal loans and hire purchases, and the implications of credit reports. A case study is presented to evaluate and process a loan application, requiring the student to analyze financial details and recommend suitable loan products. The assignment emphasizes ethical considerations, the importance of clear communication, and the practical application of financial concepts in real-world scenarios. This assignment also covers the importance of a code of ethics and the importance of a code of ethics in the relationship between a professional and clients.

Finance and Mortgage

Broking

Broking

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Task 5:.......................................................................................................................................... 3

Task 6:.......................................................................................................................................... 6

Task 7:.......................................................................................................................................... 9

Task 8:........................................................................................................................................ 19

Task 5:.......................................................................................................................................... 3

Task 6:.......................................................................................................................................... 6

Task 7:.......................................................................................................................................... 9

Task 8:........................................................................................................................................ 19

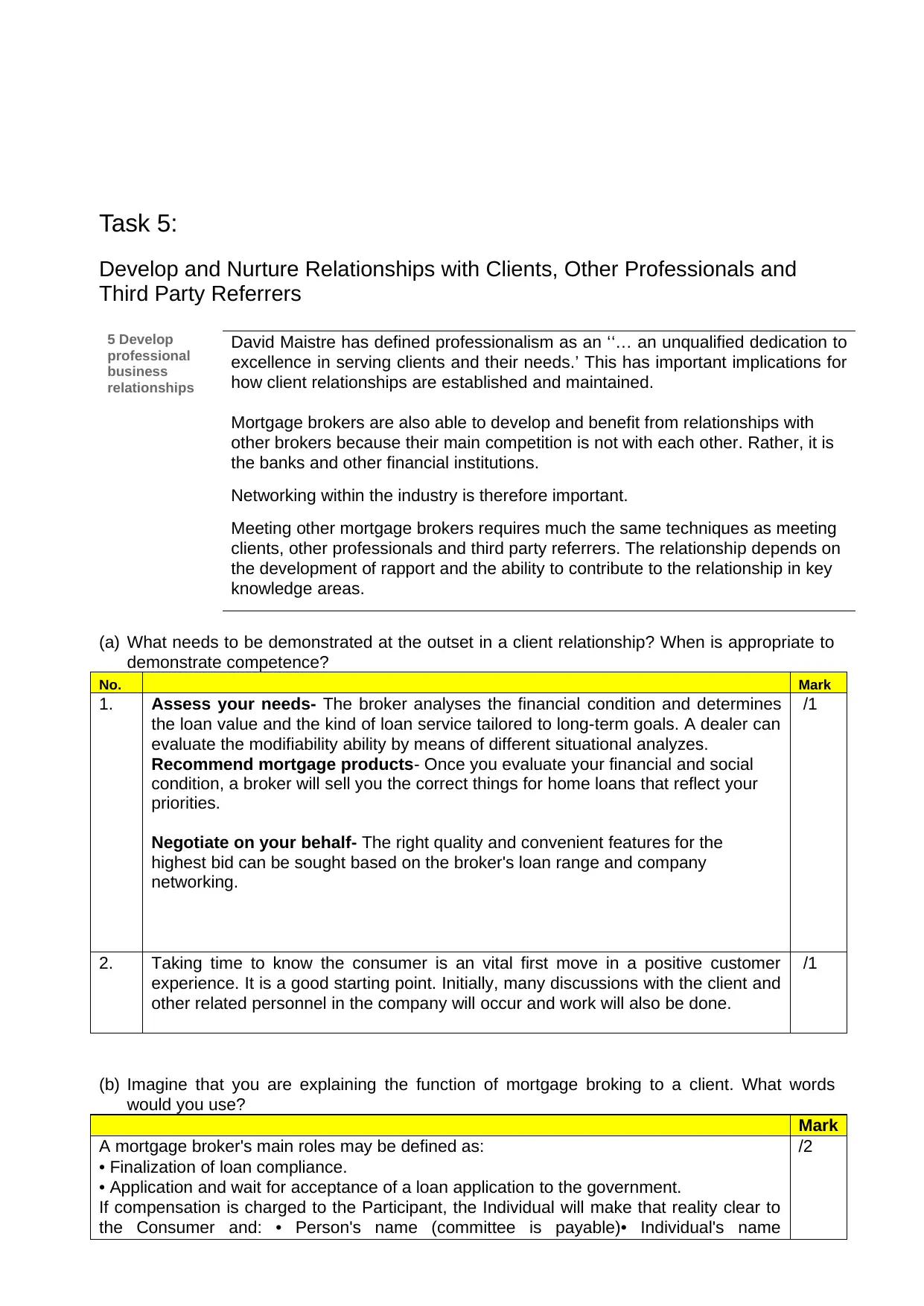

Task 5:

Develop and Nurture Relationships with Clients, Other Professionals and

Third Party Referrers

5 Develop

professional

business

relationships

David Maistre has defined professionalism as an ‘‘… an unqualified dedication to

excellence in serving clients and their needs.’ This has important implications for

how client relationships are established and maintained.

Mortgage brokers are also able to develop and benefit from relationships with

other brokers because their main competition is not with each other. Rather, it is

the banks and other financial institutions.

Networking within the industry is therefore important.

Meeting other mortgage brokers requires much the same techniques as meeting

clients, other professionals and third party referrers. The relationship depends on

the development of rapport and the ability to contribute to the relationship in key

knowledge areas.

(a) What needs to be demonstrated at the outset in a client relationship? When is appropriate to

demonstrate competence?

No. Mark

1. Assess your needs- The broker analyses the financial condition and determines

the loan value and the kind of loan service tailored to long-term goals. A dealer can

evaluate the modifiability ability by means of different situational analyzes.

Recommend mortgage products- Once you evaluate your financial and social

condition, a broker will sell you the correct things for home loans that reflect your

priorities.

Negotiate on your behalf- The right quality and convenient features for the

highest bid can be sought based on the broker's loan range and company

networking.

/1

2. Taking time to know the consumer is an vital first move in a positive customer

experience. It is a good starting point. Initially, many discussions with the client and

other related personnel in the company will occur and work will also be done.

/1

(b) Imagine that you are explaining the function of mortgage broking to a client. What words

would you use?

Mark

A mortgage broker's main roles may be defined as:

• Finalization of loan compliance.

• Application and wait for acceptance of a loan application to the government.

If compensation is charged to the Participant, the Individual will make that reality clear to

the Consumer and: • Person's name (committee is payable)• Individual's name

/2

Develop and Nurture Relationships with Clients, Other Professionals and

Third Party Referrers

5 Develop

professional

business

relationships

David Maistre has defined professionalism as an ‘‘… an unqualified dedication to

excellence in serving clients and their needs.’ This has important implications for

how client relationships are established and maintained.

Mortgage brokers are also able to develop and benefit from relationships with

other brokers because their main competition is not with each other. Rather, it is

the banks and other financial institutions.

Networking within the industry is therefore important.

Meeting other mortgage brokers requires much the same techniques as meeting

clients, other professionals and third party referrers. The relationship depends on

the development of rapport and the ability to contribute to the relationship in key

knowledge areas.

(a) What needs to be demonstrated at the outset in a client relationship? When is appropriate to

demonstrate competence?

No. Mark

1. Assess your needs- The broker analyses the financial condition and determines

the loan value and the kind of loan service tailored to long-term goals. A dealer can

evaluate the modifiability ability by means of different situational analyzes.

Recommend mortgage products- Once you evaluate your financial and social

condition, a broker will sell you the correct things for home loans that reflect your

priorities.

Negotiate on your behalf- The right quality and convenient features for the

highest bid can be sought based on the broker's loan range and company

networking.

/1

2. Taking time to know the consumer is an vital first move in a positive customer

experience. It is a good starting point. Initially, many discussions with the client and

other related personnel in the company will occur and work will also be done.

/1

(b) Imagine that you are explaining the function of mortgage broking to a client. What words

would you use?

Mark

A mortgage broker's main roles may be defined as:

• Finalization of loan compliance.

• Application and wait for acceptance of a loan application to the government.

If compensation is charged to the Participant, the Individual will make that reality clear to

the Consumer and: • Person's name (committee is payable)• Individual's name

/2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

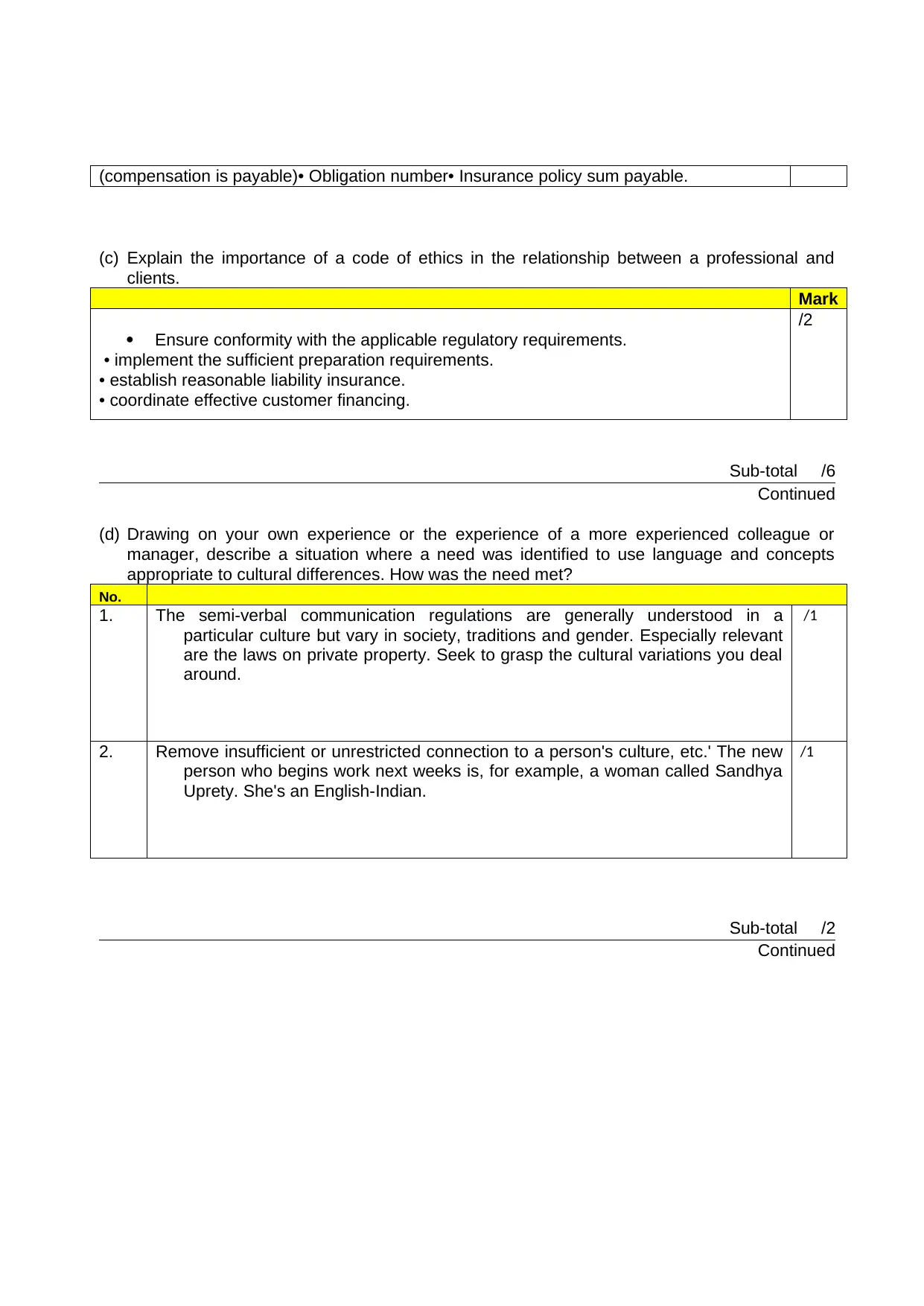

(compensation is payable)• Obligation number• Insurance policy sum payable.

(c) Explain the importance of a code of ethics in the relationship between a professional and

clients.

Mark

Ensure conformity with the applicable regulatory requirements.

• implement the sufficient preparation requirements.

• establish reasonable liability insurance.

• coordinate effective customer financing.

/2

Sub-total /6

Continued

(d) Drawing on your own experience or the experience of a more experienced colleague or

manager, describe a situation where a need was identified to use language and concepts

appropriate to cultural differences. How was the need met?

No.

1. The semi-verbal communication regulations are generally understood in a

particular culture but vary in society, traditions and gender. Especially relevant

are the laws on private property. Seek to grasp the cultural variations you deal

around.

/1

2. Remove insufficient or unrestricted connection to a person's culture, etc.' The new

person who begins work next weeks is, for example, a woman called Sandhya

Uprety. She's an English-Indian.

/1

Sub-total /2

Continued

(c) Explain the importance of a code of ethics in the relationship between a professional and

clients.

Mark

Ensure conformity with the applicable regulatory requirements.

• implement the sufficient preparation requirements.

• establish reasonable liability insurance.

• coordinate effective customer financing.

/2

Sub-total /6

Continued

(d) Drawing on your own experience or the experience of a more experienced colleague or

manager, describe a situation where a need was identified to use language and concepts

appropriate to cultural differences. How was the need met?

No.

1. The semi-verbal communication regulations are generally understood in a

particular culture but vary in society, traditions and gender. Especially relevant

are the laws on private property. Seek to grasp the cultural variations you deal

around.

/1

2. Remove insufficient or unrestricted connection to a person's culture, etc.' The new

person who begins work next weeks is, for example, a woman called Sandhya

Uprety. She's an English-Indian.

/1

Sub-total /2

Continued

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 5: Develop and Nurture Relationships with Clients, Other

Professionals and Third Party Referrers Continued

5.1 Build and

maintain

business

networks and

relationships

For a relationship with a client to continue, they need an assurance of continuing

mutual benefit. The continuing mutual benefit is also important in relationships

with other professionals, including relationships with ‘outsiders’ such as

accountants, real estate agents and other professionals.

(a) List two others type of professional your organization uses to develop client

relationships and indicate in each case how it is able to provide them with a benefit in

the relationship.

No.

1. It can also be hard to remember that we are not a justification for all knowledge

and direction. However, competent people like: • Accountants• Lawyer

/1

2. They let clients know whether they will look at a topic and offer customers

greater expertise whether needed. Capital creditors are something they should

learn to do when they are qualified. It is a matter of customer behavior, and it is

the care duty.

/1

(b) Surveys indicated that two-way dialogue, or ‘conversation’ is of overriding importance in

developing client relationships, relationships with colleagues and also other professional

relationships. List four characteristics of this process.

No. Mark

1. Through addressing consumers directly, a stronger relationship can be made. /1

2. Enables customer service to be enhanced. /1

3. Provides a market awareness system for consumers. /1

4. Let consumers know they are viewed. /1

(c) Other professionals that a mortgage broker might forms contacts with are referred to in

marketing literature as ‘Centres of Influence’ (COI). Why does David Maistre place them in

his ‘second tier’ in order of effectiveness. What activities in David Maistre’s first tier does your

organization engage in.

No. Mark

1. One thing that is interesting to remember is that clients who are very happy often

want to find a way to support social and family connections. Requests for

information do more than easily. This helps you to proceed.

/1

2. By seem to have the interest, which is important technological efficiency, when

engaging with great customers. You are most likely to establish "interaction"

/1

Professionals and Third Party Referrers Continued

5.1 Build and

maintain

business

networks and

relationships

For a relationship with a client to continue, they need an assurance of continuing

mutual benefit. The continuing mutual benefit is also important in relationships

with other professionals, including relationships with ‘outsiders’ such as

accountants, real estate agents and other professionals.

(a) List two others type of professional your organization uses to develop client

relationships and indicate in each case how it is able to provide them with a benefit in

the relationship.

No.

1. It can also be hard to remember that we are not a justification for all knowledge

and direction. However, competent people like: • Accountants• Lawyer

/1

2. They let clients know whether they will look at a topic and offer customers

greater expertise whether needed. Capital creditors are something they should

learn to do when they are qualified. It is a matter of customer behavior, and it is

the care duty.

/1

(b) Surveys indicated that two-way dialogue, or ‘conversation’ is of overriding importance in

developing client relationships, relationships with colleagues and also other professional

relationships. List four characteristics of this process.

No. Mark

1. Through addressing consumers directly, a stronger relationship can be made. /1

2. Enables customer service to be enhanced. /1

3. Provides a market awareness system for consumers. /1

4. Let consumers know they are viewed. /1

(c) Other professionals that a mortgage broker might forms contacts with are referred to in

marketing literature as ‘Centres of Influence’ (COI). Why does David Maistre place them in

his ‘second tier’ in order of effectiveness. What activities in David Maistre’s first tier does your

organization engage in.

No. Mark

1. One thing that is interesting to remember is that clients who are very happy often

want to find a way to support social and family connections. Requests for

information do more than easily. This helps you to proceed.

/1

2. By seem to have the interest, which is important technological efficiency, when

engaging with great customers. You are most likely to establish "interaction"

/1

partnerships with consumers–a lengthy-term intimate friendship. The "plot" of the

perfect buyer is therefore the foundation of a marketing campaign that targets and

retains more consumers.

Sub-total /8

Continued

(d) List four occupations and professionals that may become Centres of Influence.for your

organisation.

Mark

Solicitors

Conveyancers

Agency of credit report

Land office

/1

Sub-total / 1

Total /17

Task 6:

Promoting the Effective Use of Credit

Read the following scenario then answer the questions that follow.

Roslyn qualified as a schoolteacher some years ago, but failed to take up a teaching position

after graduating because she became a single mother. Fortunately, she has been able to live with

her widowed mother, but now that her daughter has reached school she is taking up a position as

a schoolteacher some suburbs away.

Because of the distance of her new school from her parent’s home she will need to buy a car.

After careful consideration, she has chosen a small hatchback that has an on-road cost of

$15,800.

She will be working full time with a starting salary of $50,000.

She knows little about finance and has come to you for advice. She would prefer to finance the

full cost of the car because she has little in savings.

Task 6.1.

perfect buyer is therefore the foundation of a marketing campaign that targets and

retains more consumers.

Sub-total /8

Continued

(d) List four occupations and professionals that may become Centres of Influence.for your

organisation.

Mark

Solicitors

Conveyancers

Agency of credit report

Land office

/1

Sub-total / 1

Total /17

Task 6:

Promoting the Effective Use of Credit

Read the following scenario then answer the questions that follow.

Roslyn qualified as a schoolteacher some years ago, but failed to take up a teaching position

after graduating because she became a single mother. Fortunately, she has been able to live with

her widowed mother, but now that her daughter has reached school she is taking up a position as

a schoolteacher some suburbs away.

Because of the distance of her new school from her parent’s home she will need to buy a car.

After careful consideration, she has chosen a small hatchback that has an on-road cost of

$15,800.

She will be working full time with a starting salary of $50,000.

She knows little about finance and has come to you for advice. She would prefer to finance the

full cost of the car because she has little in savings.

Task 6.1.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(i) Suggest two financing options that Roslyn might consider.

(ii) Explain the main features of each.

(iii)Choose one of these options and explain your choice. Are there any disadvantages that need

to be considered?

No. Mark

1. Personal loan and hire purchasing /1

2. Auto transactions are typically carried out with guaranteed personal loans, which

can be used to repay the debt for both vehicles. The interest rate on personal loans

is usually lower.

Commercial rent exchanges are a form of trade funding for goods like motor

vehicles that quickly depreciate. The borrower will only be in a position in the

medium and long term to obtain the product financed in the last five years of the

CHP.

/2

3. Throughout this scenario, I would encourage Roslyn to apply for a covered bank

loan. First of all, a covered bank loan may be provided with the deduction after

authorization. Moreover, reimbursed loans have lower rates in particular. If Natalie

will not settle for the property under insurance, a borrower buys the property by

obtaining a discretionary loan for cash compensation to sell the house. The debt

differential would be charged if the items are purchased for less.

/2

Sub-total /5

Continued

(ii) Explain the main features of each.

(iii)Choose one of these options and explain your choice. Are there any disadvantages that need

to be considered?

No. Mark

1. Personal loan and hire purchasing /1

2. Auto transactions are typically carried out with guaranteed personal loans, which

can be used to repay the debt for both vehicles. The interest rate on personal loans

is usually lower.

Commercial rent exchanges are a form of trade funding for goods like motor

vehicles that quickly depreciate. The borrower will only be in a position in the

medium and long term to obtain the product financed in the last five years of the

CHP.

/2

3. Throughout this scenario, I would encourage Roslyn to apply for a covered bank

loan. First of all, a covered bank loan may be provided with the deduction after

authorization. Moreover, reimbursed loans have lower rates in particular. If Natalie

will not settle for the property under insurance, a borrower buys the property by

obtaining a discretionary loan for cash compensation to sell the house. The debt

differential would be charged if the items are purchased for less.

/2

Sub-total /5

Continued

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 6: Promoting the Effective Use of Credit Continued

Task 6.2.

Write a letter to Roslyn letting her know about your preferred, explain how she will make

payments and giving your reasons for choosing it as the option more clearly meeting her needs.

You should take care to proofread your letter.

Mark

Dear Roslyn,

I said that the Westpac Car loan would be her best product. Although separate loans are

available, it's better for her. The fees are as follows:

$ 250 (Establishment fee)

$10 (Month basis)

9.9% rate of interest with 11.34% comparison rate

A equivalent rate includes interest and other expenses, as per the NCC lenders. This

rate is being used to test the goods of various banks. The local fines and costs are not

included in service fees.

Between thousands of things, one can select. Therefore, NCC requires all payment

providers to provide the official benchmark rating to help customers compare different

goods. The complex pricing structure of these goods is difficult to understand. In order to

include pricing for its lending offerings to help prospective mortgage borrowers recognize

how much they owe for their lending, it is expected to provide a comparison rate through

credit providers. The comparison figure shall follow a basic formula which shall take

account of the volume of loans, inflation, length of loans, the figure of repayment and the

expense of loan services. The mortgage interest rate may, for example, be 5.5 percent

for housing loans. The comparison rate can shift a two-price perspective. For instance,

hypothecary levels for Hypothecs A and B are 6%. Mortgage A's fees & taxation are

0.5% similar to Loan B's 0.1%. That implies that the disparity between mortgage A's

6.5% and B's 6.1% is greater. Loan B is the lowest of the two.

/4

Task 6.3.

Roslyn is concerned that the lender will apply for a credit report. Explain:

(i) The procedure and cost involved in obtaining a copy of her credit file.

(ii) The right of a lender to access credit report information.

No. Mark

1. Three big debt recovery firms currently operate on the Aussie sector. These include

Veda Benefit, Dun and Bradstreet and Tasmania's selection operation.

/2

2. The specifics of credit agencies, such as Veda Vermeil, have major implications for

creditors. A weak history of loans may result in loans being dismissed. All

consumers, particularly those with limited financial awareness, must disclose the

potential implications of paying interest on transaction agreements.

The UK government has now decided that the proposed regulatory system for

consumer loans services would have accountable borrowing obligations. It must

demand that lenders: • repay to a borrower who can make payments, without

significant problems.

/2

Task 6.4.

Task 6.2.

Write a letter to Roslyn letting her know about your preferred, explain how she will make

payments and giving your reasons for choosing it as the option more clearly meeting her needs.

You should take care to proofread your letter.

Mark

Dear Roslyn,

I said that the Westpac Car loan would be her best product. Although separate loans are

available, it's better for her. The fees are as follows:

$ 250 (Establishment fee)

$10 (Month basis)

9.9% rate of interest with 11.34% comparison rate

A equivalent rate includes interest and other expenses, as per the NCC lenders. This

rate is being used to test the goods of various banks. The local fines and costs are not

included in service fees.

Between thousands of things, one can select. Therefore, NCC requires all payment

providers to provide the official benchmark rating to help customers compare different

goods. The complex pricing structure of these goods is difficult to understand. In order to

include pricing for its lending offerings to help prospective mortgage borrowers recognize

how much they owe for their lending, it is expected to provide a comparison rate through

credit providers. The comparison figure shall follow a basic formula which shall take

account of the volume of loans, inflation, length of loans, the figure of repayment and the

expense of loan services. The mortgage interest rate may, for example, be 5.5 percent

for housing loans. The comparison rate can shift a two-price perspective. For instance,

hypothecary levels for Hypothecs A and B are 6%. Mortgage A's fees & taxation are

0.5% similar to Loan B's 0.1%. That implies that the disparity between mortgage A's

6.5% and B's 6.1% is greater. Loan B is the lowest of the two.

/4

Task 6.3.

Roslyn is concerned that the lender will apply for a credit report. Explain:

(i) The procedure and cost involved in obtaining a copy of her credit file.

(ii) The right of a lender to access credit report information.

No. Mark

1. Three big debt recovery firms currently operate on the Aussie sector. These include

Veda Benefit, Dun and Bradstreet and Tasmania's selection operation.

/2

2. The specifics of credit agencies, such as Veda Vermeil, have major implications for

creditors. A weak history of loans may result in loans being dismissed. All

consumers, particularly those with limited financial awareness, must disclose the

potential implications of paying interest on transaction agreements.

The UK government has now decided that the proposed regulatory system for

consumer loans services would have accountable borrowing obligations. It must

demand that lenders: • repay to a borrower who can make payments, without

significant problems.

/2

Task 6.4.

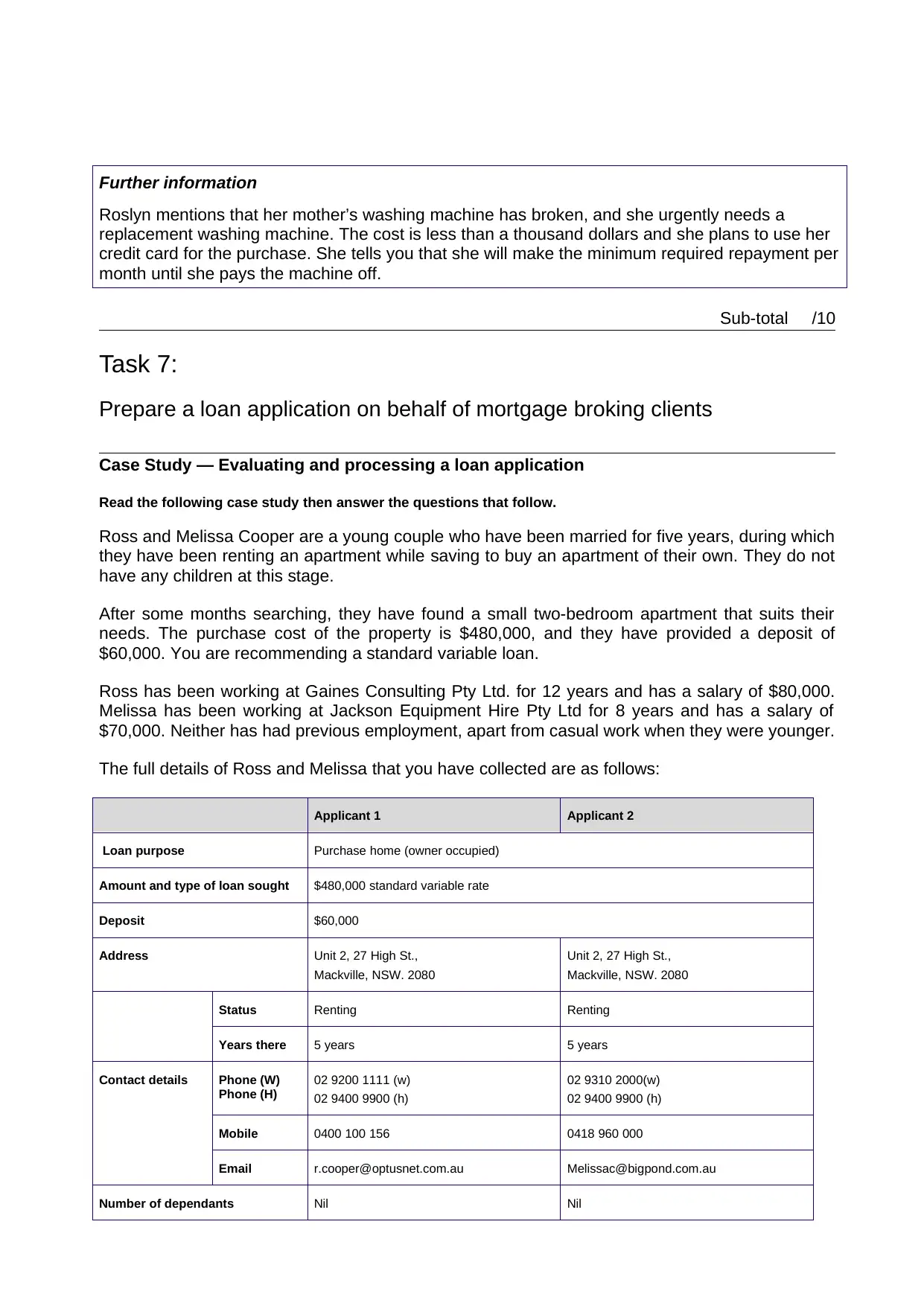

Further information

Roslyn mentions that her mother’s washing machine has broken, and she urgently needs a

replacement washing machine. The cost is less than a thousand dollars and she plans to use her

credit card for the purchase. She tells you that she will make the minimum required repayment per

month until she pays the machine off.

Sub-total /10

Task 7:

Prepare a loan application on behalf of mortgage broking clients

Case Study — Evaluating and processing a loan application

Read the following case study then answer the questions that follow.

Ross and Melissa Cooper are a young couple who have been married for five years, during which

they have been renting an apartment while saving to buy an apartment of their own. They do not

have any children at this stage.

After some months searching, they have found a small two-bedroom apartment that suits their

needs. The purchase cost of the property is $480,000, and they have provided a deposit of

$60,000. You are recommending a standard variable loan.

Ross has been working at Gaines Consulting Pty Ltd. for 12 years and has a salary of $80,000.

Melissa has been working at Jackson Equipment Hire Pty Ltd for 8 years and has a salary of

$70,000. Neither has had previous employment, apart from casual work when they were younger.

The full details of Ross and Melissa that you have collected are as follows:

Applicant 1 Applicant 2

Loan purpose Purchase home (owner occupied)

Amount and type of loan sought $480,000 standard variable rate

Deposit $60,000

Address Unit 2, 27 High St.,

Mackville, NSW. 2080

Unit 2, 27 High St.,

Mackville, NSW. 2080

Status Renting Renting

Years there 5 years 5 years

Contact details Phone (W)

Phone (H)

02 9200 1111 (w)

02 9400 9900 (h)

02 9310 2000(w)

02 9400 9900 (h)

Mobile 0400 100 156 0418 960 000

Email r.cooper@optusnet.com.au Melissac@bigpond.com.au

Number of dependants Nil Nil

Roslyn mentions that her mother’s washing machine has broken, and she urgently needs a

replacement washing machine. The cost is less than a thousand dollars and she plans to use her

credit card for the purchase. She tells you that she will make the minimum required repayment per

month until she pays the machine off.

Sub-total /10

Task 7:

Prepare a loan application on behalf of mortgage broking clients

Case Study — Evaluating and processing a loan application

Read the following case study then answer the questions that follow.

Ross and Melissa Cooper are a young couple who have been married for five years, during which

they have been renting an apartment while saving to buy an apartment of their own. They do not

have any children at this stage.

After some months searching, they have found a small two-bedroom apartment that suits their

needs. The purchase cost of the property is $480,000, and they have provided a deposit of

$60,000. You are recommending a standard variable loan.

Ross has been working at Gaines Consulting Pty Ltd. for 12 years and has a salary of $80,000.

Melissa has been working at Jackson Equipment Hire Pty Ltd for 8 years and has a salary of

$70,000. Neither has had previous employment, apart from casual work when they were younger.

The full details of Ross and Melissa that you have collected are as follows:

Applicant 1 Applicant 2

Loan purpose Purchase home (owner occupied)

Amount and type of loan sought $480,000 standard variable rate

Deposit $60,000

Address Unit 2, 27 High St.,

Mackville, NSW. 2080

Unit 2, 27 High St.,

Mackville, NSW. 2080

Status Renting Renting

Years there 5 years 5 years

Contact details Phone (W)

Phone (H)

02 9200 1111 (w)

02 9400 9900 (h)

02 9310 2000(w)

02 9400 9900 (h)

Mobile 0400 100 156 0418 960 000

Email r.cooper@optusnet.com.au Melissac@bigpond.com.au

Number of dependants Nil Nil

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

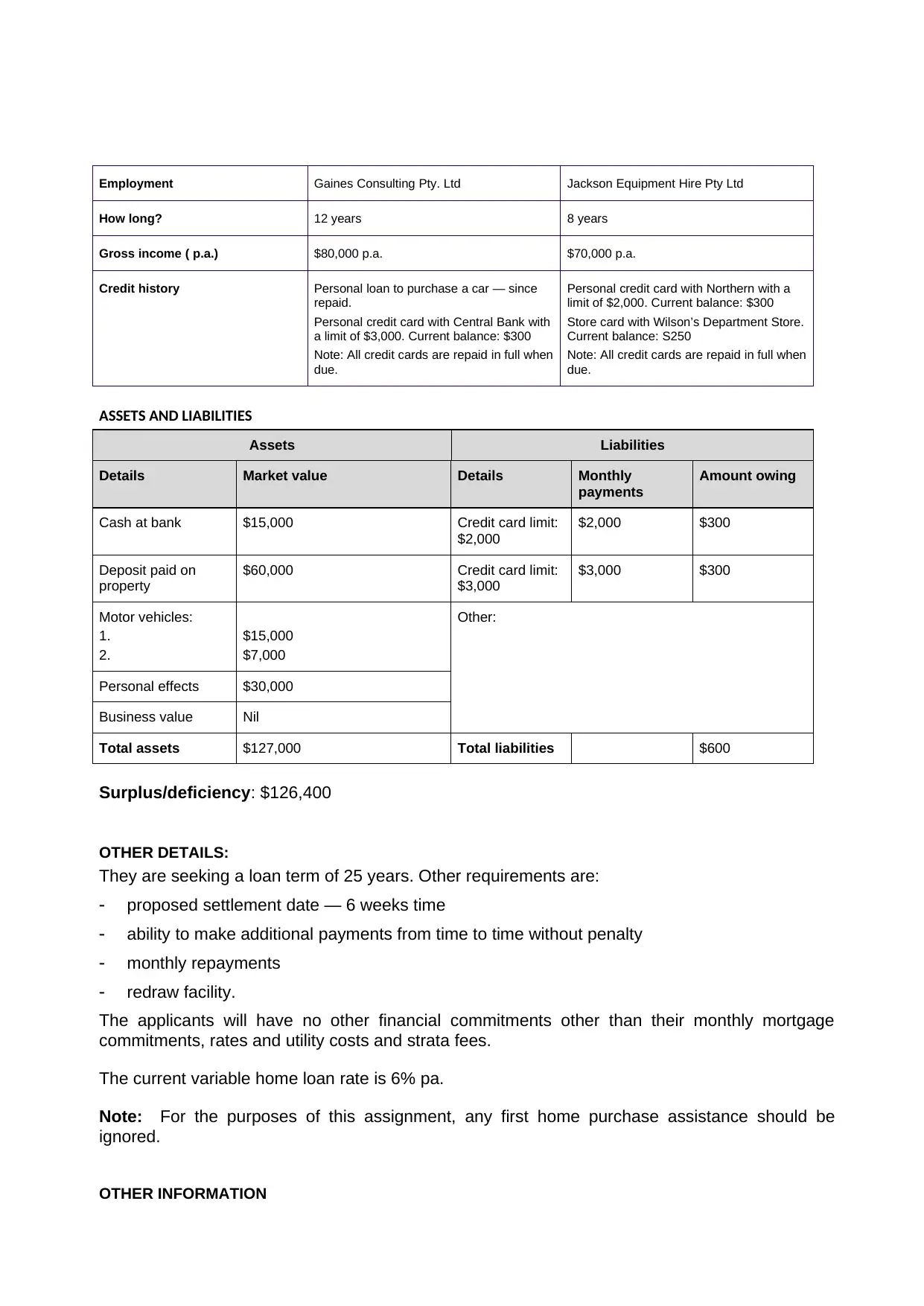

Employment Gaines Consulting Pty. Ltd Jackson Equipment Hire Pty Ltd

How long? 12 years 8 years

Gross income ( p.a.) $80,000 p.a. $70,000 p.a.

Credit history Personal loan to purchase a car — since

repaid.

Personal credit card with Central Bank with

a limit of $3,000. Current balance: $300

Note: All credit cards are repaid in full when

due.

Personal credit card with Northern with a

limit of $2,000. Current balance: $300

Store card with Wilson’s Department Store.

Current balance: S250

Note: All credit cards are repaid in full when

due.

ASSETS AND LIABILITIES

Assets Liabilities

Details Market value Details Monthly

payments

Amount owing

Cash at bank $15,000 Credit card limit:

$2,000

$2,000 $300

Deposit paid on

property

$60,000 Credit card limit:

$3,000

$3,000 $300

Motor vehicles:

1.

2.

$15,000

$7,000

Other:

Personal effects $30,000

Business value Nil

Total assets $127,000 Total liabilities $600

Surplus/deficiency: $126,400

OTHER DETAILS:

They are seeking a loan term of 25 years. Other requirements are:

proposed settlement date — 6 weeks time

ability to make additional payments from time to time without penalty

monthly repayments

redraw facility.

The applicants will have no other financial commitments other than their monthly mortgage

commitments, rates and utility costs and strata fees.

The current variable home loan rate is 6% pa.

Note: For the purposes of this assignment, any first home purchase assistance should be

ignored.

OTHER INFORMATION

How long? 12 years 8 years

Gross income ( p.a.) $80,000 p.a. $70,000 p.a.

Credit history Personal loan to purchase a car — since

repaid.

Personal credit card with Central Bank with

a limit of $3,000. Current balance: $300

Note: All credit cards are repaid in full when

due.

Personal credit card with Northern with a

limit of $2,000. Current balance: $300

Store card with Wilson’s Department Store.

Current balance: S250

Note: All credit cards are repaid in full when

due.

ASSETS AND LIABILITIES

Assets Liabilities

Details Market value Details Monthly

payments

Amount owing

Cash at bank $15,000 Credit card limit:

$2,000

$2,000 $300

Deposit paid on

property

$60,000 Credit card limit:

$3,000

$3,000 $300

Motor vehicles:

1.

2.

$15,000

$7,000

Other:

Personal effects $30,000

Business value Nil

Total assets $127,000 Total liabilities $600

Surplus/deficiency: $126,400

OTHER DETAILS:

They are seeking a loan term of 25 years. Other requirements are:

proposed settlement date — 6 weeks time

ability to make additional payments from time to time without penalty

monthly repayments

redraw facility.

The applicants will have no other financial commitments other than their monthly mortgage

commitments, rates and utility costs and strata fees.

The current variable home loan rate is 6% pa.

Note: For the purposes of this assignment, any first home purchase assistance should be

ignored.

OTHER INFORMATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

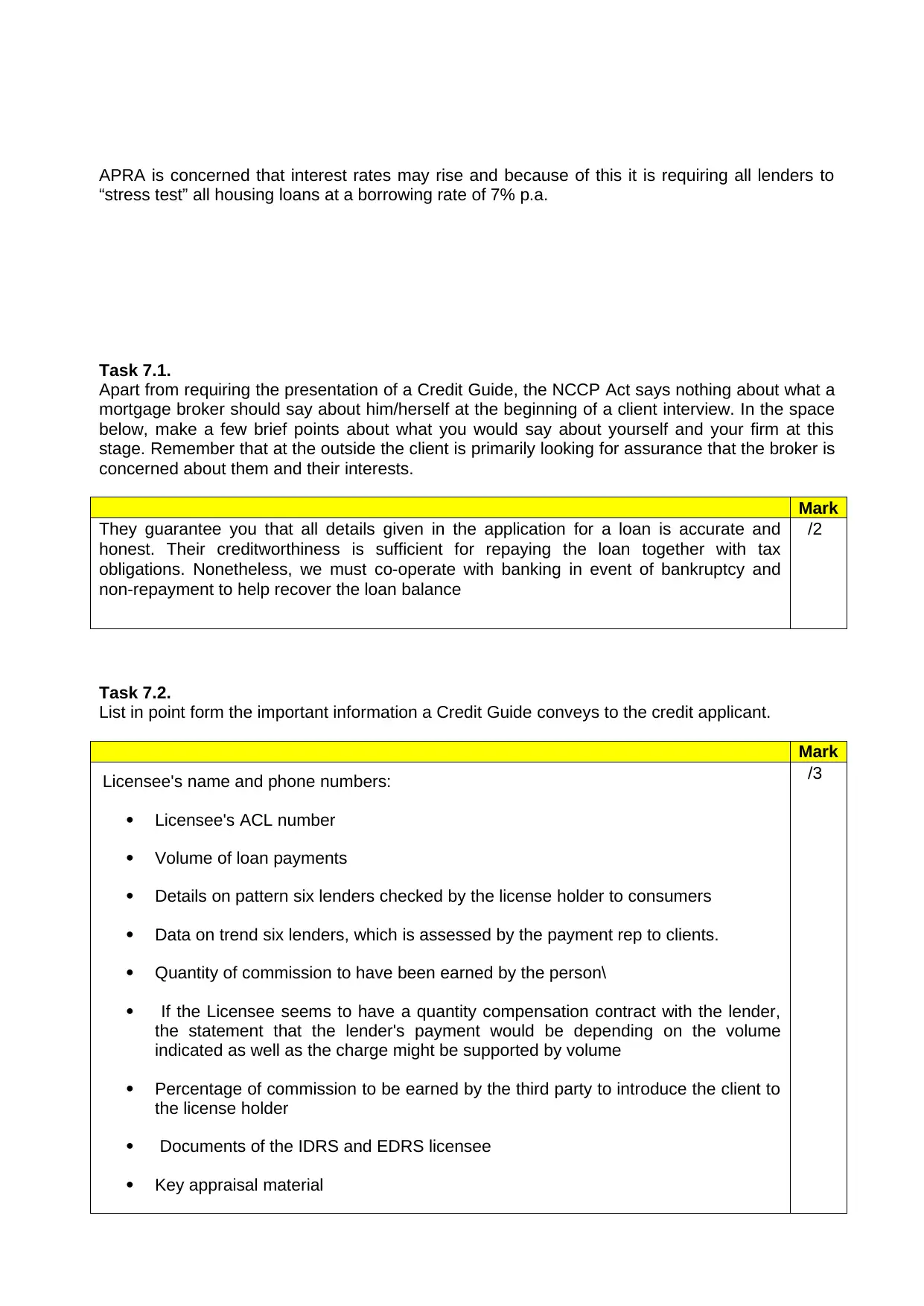

APRA is concerned that interest rates may rise and because of this it is requiring all lenders to

“stress test” all housing loans at a borrowing rate of 7% p.a.

Task 7.1.

Apart from requiring the presentation of a Credit Guide, the NCCP Act says nothing about what a

mortgage broker should say about him/herself at the beginning of a client interview. In the space

below, make a few brief points about what you would say about yourself and your firm at this

stage. Remember that at the outside the client is primarily looking for assurance that the broker is

concerned about them and their interests.

Mark

They guarantee you that all details given in the application for a loan is accurate and

honest. Their creditworthiness is sufficient for repaying the loan together with tax

obligations. Nonetheless, we must co-operate with banking in event of bankruptcy and

non-repayment to help recover the loan balance

/2

Task 7.2.

List in point form the important information a Credit Guide conveys to the credit applicant.

Mark

Licensee's name and phone numbers:

Licensee's ACL number

Volume of loan payments

Details on pattern six lenders checked by the license holder to consumers

Data on trend six lenders, which is assessed by the payment rep to clients.

Quantity of commission to have been earned by the person\

If the Licensee seems to have a quantity compensation contract with the lender,

the statement that the lender's payment would be depending on the volume

indicated as well as the charge might be supported by volume

Percentage of commission to be earned by the third party to introduce the client to

the license holder

Documents of the IDRS and EDRS licensee

Key appraisal material

/3

“stress test” all housing loans at a borrowing rate of 7% p.a.

Task 7.1.

Apart from requiring the presentation of a Credit Guide, the NCCP Act says nothing about what a

mortgage broker should say about him/herself at the beginning of a client interview. In the space

below, make a few brief points about what you would say about yourself and your firm at this

stage. Remember that at the outside the client is primarily looking for assurance that the broker is

concerned about them and their interests.

Mark

They guarantee you that all details given in the application for a loan is accurate and

honest. Their creditworthiness is sufficient for repaying the loan together with tax

obligations. Nonetheless, we must co-operate with banking in event of bankruptcy and

non-repayment to help recover the loan balance

/2

Task 7.2.

List in point form the important information a Credit Guide conveys to the credit applicant.

Mark

Licensee's name and phone numbers:

Licensee's ACL number

Volume of loan payments

Details on pattern six lenders checked by the license holder to consumers

Data on trend six lenders, which is assessed by the payment rep to clients.

Quantity of commission to have been earned by the person\

If the Licensee seems to have a quantity compensation contract with the lender,

the statement that the lender's payment would be depending on the volume

indicated as well as the charge might be supported by volume

Percentage of commission to be earned by the third party to introduce the client to

the license holder

Documents of the IDRS and EDRS licensee

Key appraisal material

/3

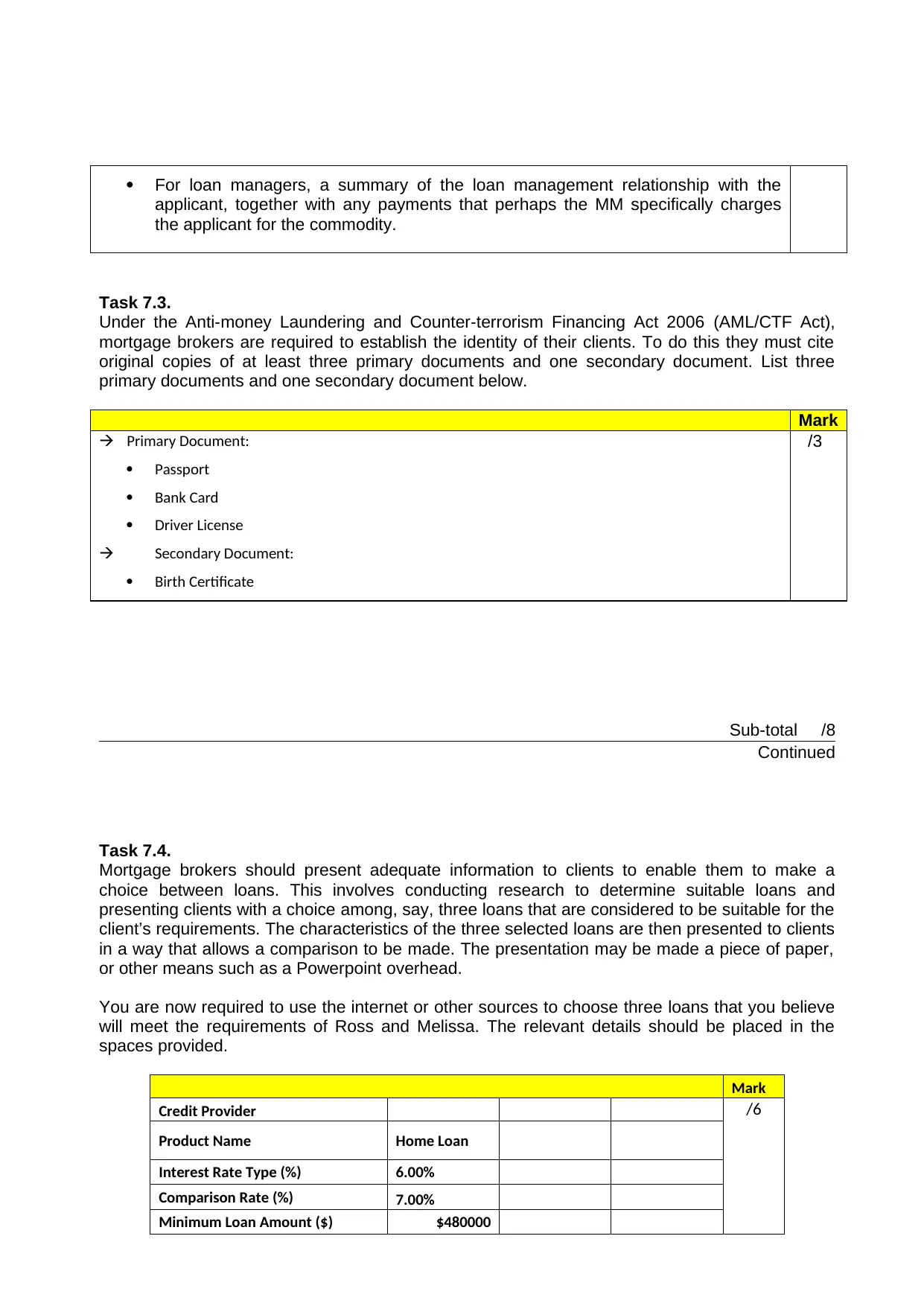

For loan managers, a summary of the loan management relationship with the

applicant, together with any payments that perhaps the MM specifically charges

the applicant for the commodity.

Task 7.3.

Under the Anti-money Laundering and Counter-terrorism Financing Act 2006 (AML/CTF Act),

mortgage brokers are required to establish the identity of their clients. To do this they must cite

original copies of at least three primary documents and one secondary document. List three

primary documents and one secondary document below.

Mark

Primary Document:

Passport

Bank Card

Driver License

Secondary Document:

Birth Certificate

/3

Sub-total /8

Continued

Task 7.4.

Mortgage brokers should present adequate information to clients to enable them to make a

choice between loans. This involves conducting research to determine suitable loans and

presenting clients with a choice among, say, three loans that are considered to be suitable for the

client’s requirements. The characteristics of the three selected loans are then presented to clients

in a way that allows a comparison to be made. The presentation may be made a piece of paper,

or other means such as a Powerpoint overhead.

You are now required to use the internet or other sources to choose three loans that you believe

will meet the requirements of Ross and Melissa. The relevant details should be placed in the

spaces provided.

Mark

Credit Provider /6

Product Name Home Loan

Interest Rate Type (%) 6.00%

Comparison Rate (%) 7.00%

Minimum Loan Amount ($) $480000

applicant, together with any payments that perhaps the MM specifically charges

the applicant for the commodity.

Task 7.3.

Under the Anti-money Laundering and Counter-terrorism Financing Act 2006 (AML/CTF Act),

mortgage brokers are required to establish the identity of their clients. To do this they must cite

original copies of at least three primary documents and one secondary document. List three

primary documents and one secondary document below.

Mark

Primary Document:

Passport

Bank Card

Driver License

Secondary Document:

Birth Certificate

/3

Sub-total /8

Continued

Task 7.4.

Mortgage brokers should present adequate information to clients to enable them to make a

choice between loans. This involves conducting research to determine suitable loans and

presenting clients with a choice among, say, three loans that are considered to be suitable for the

client’s requirements. The characteristics of the three selected loans are then presented to clients

in a way that allows a comparison to be made. The presentation may be made a piece of paper,

or other means such as a Powerpoint overhead.

You are now required to use the internet or other sources to choose three loans that you believe

will meet the requirements of Ross and Melissa. The relevant details should be placed in the

spaces provided.

Mark

Credit Provider /6

Product Name Home Loan

Interest Rate Type (%) 6.00%

Comparison Rate (%) 7.00%

Minimum Loan Amount ($) $480000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.