Mortgage Broking Report: Risks, Process, and Client Considerations

VerifiedAdded on 2019/11/12

|5

|1766

|151

Report

AI Summary

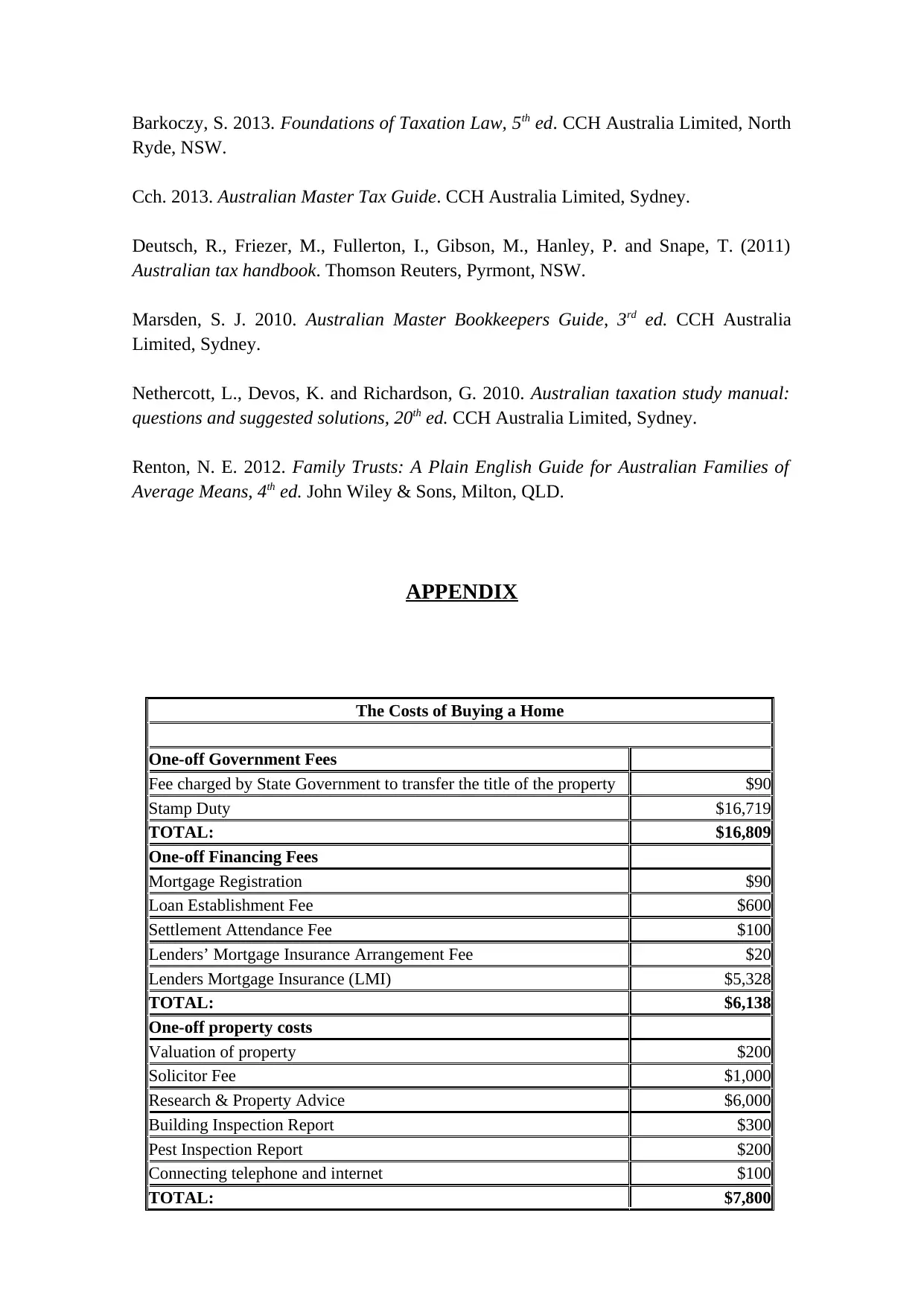

This report provides a comprehensive analysis of mortgage broking, addressing key aspects such as lending risks, the loan application process, and client considerations. Task A focuses on identifying and assessing systemic risks like rising interest rates, income variations, and fluctuating house prices, providing insights into their potential impact on clients. The report also explores risk mitigation strategies involving partnerships between the state, market, and borrowers, as well as the role of insurance companies. Task B delves into the mortgage process, covering pre-qualification, mortgage programs, loan applications, loan estimates, processing, required documents, credit reports, and closing disclosures. The report also includes an LVR calculation and an appendix with a detailed breakdown of fees and costs associated with purchasing a home, offering valuable information for both borrowers and industry professionals. The report emphasizes the importance of understanding the mortgage process and the associated costs to make informed financial decisions.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.