Decision Modelling for Business Analytics: Mortgage Loan (MIS775)

VerifiedAdded on 2023/06/14

|17

|1474

|255

Report

AI Summary

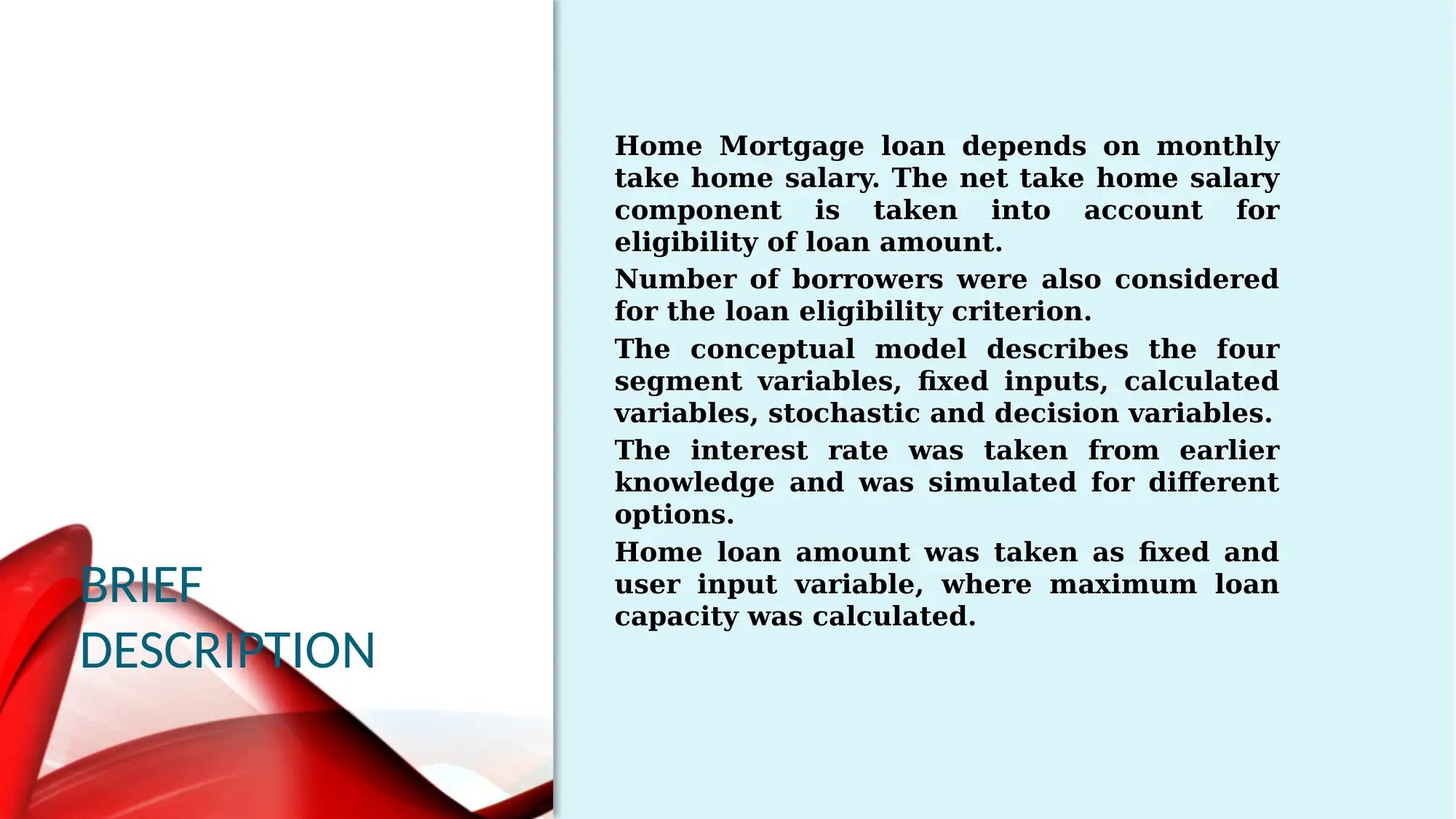

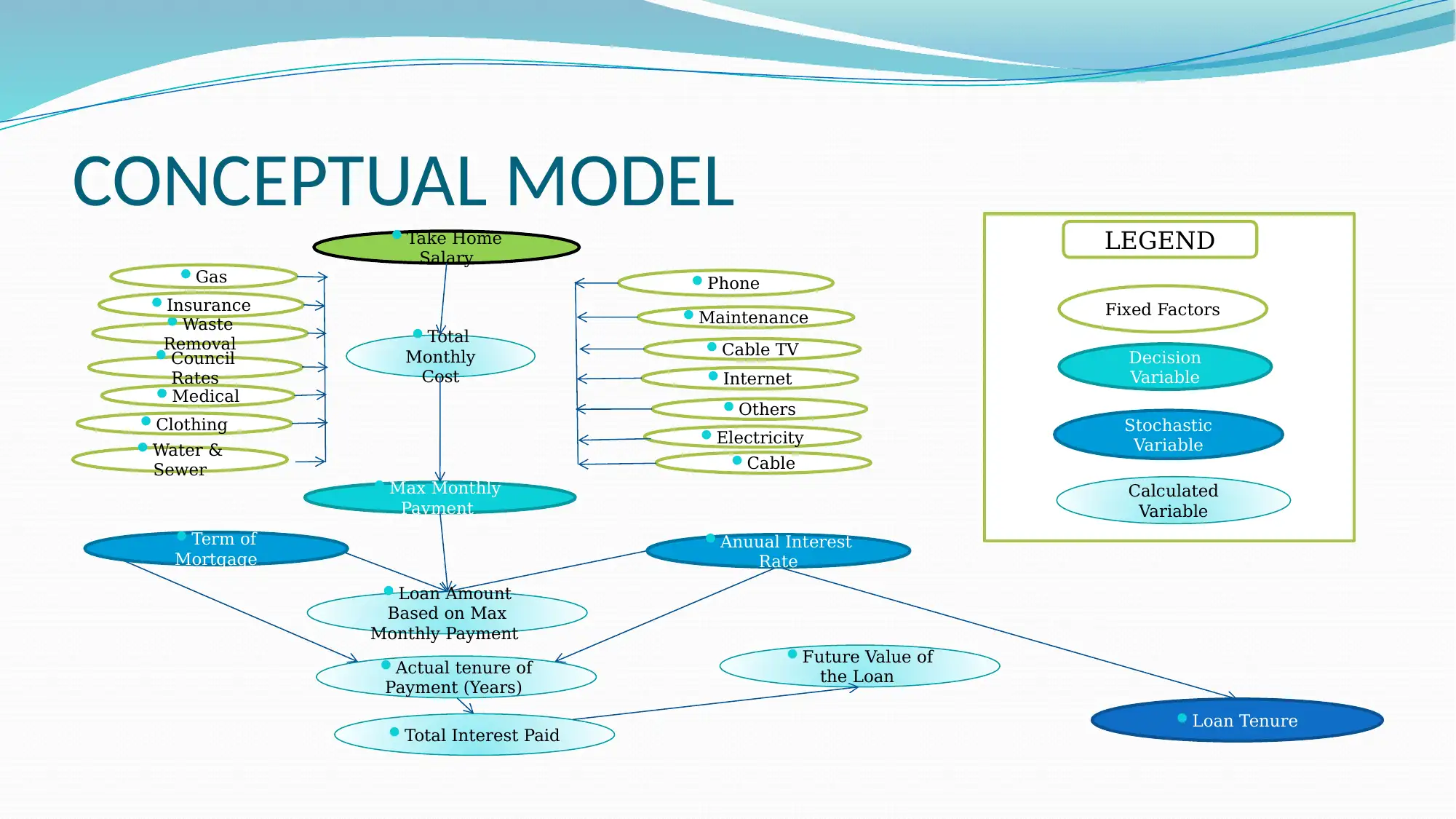

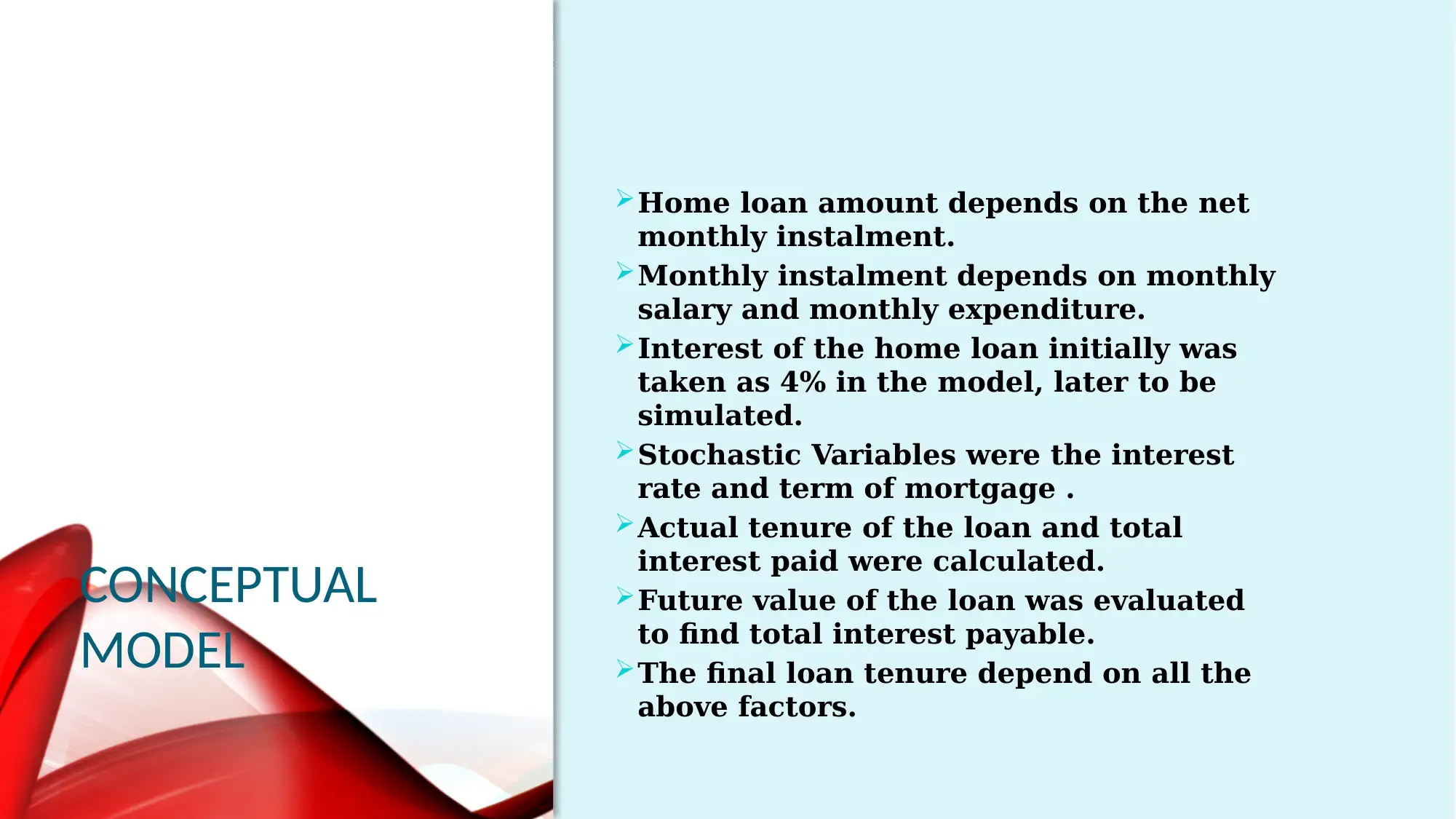

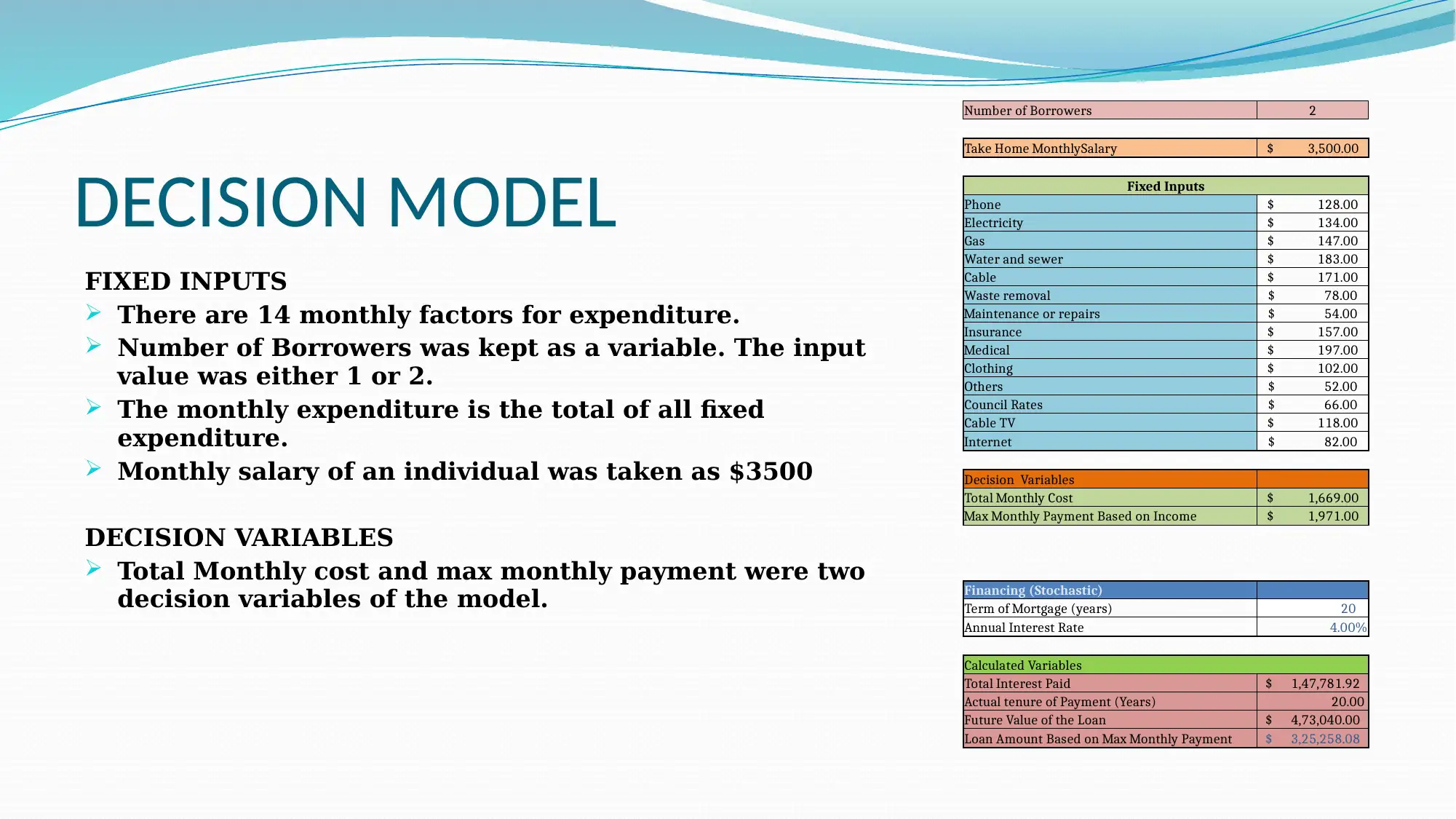

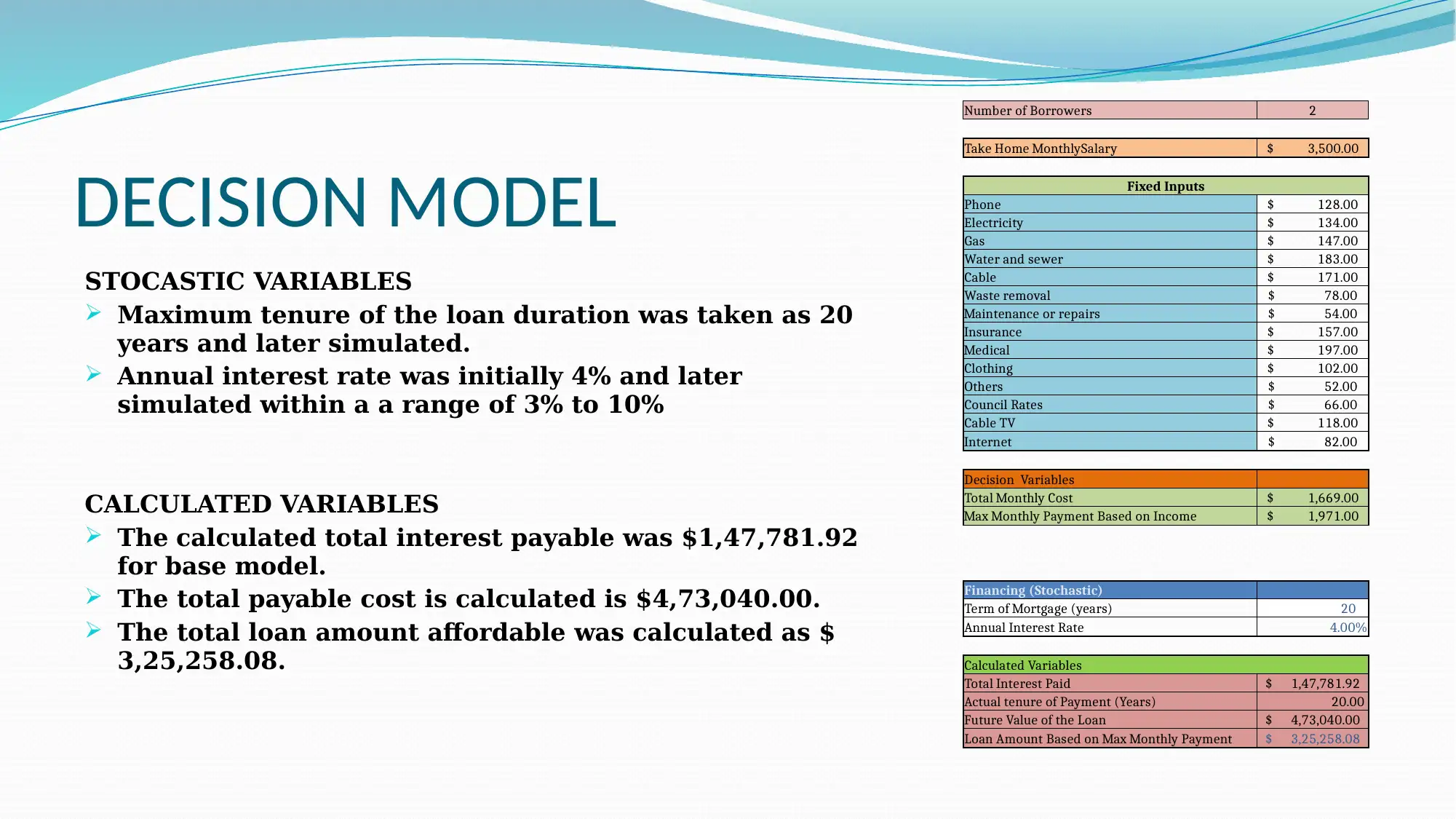

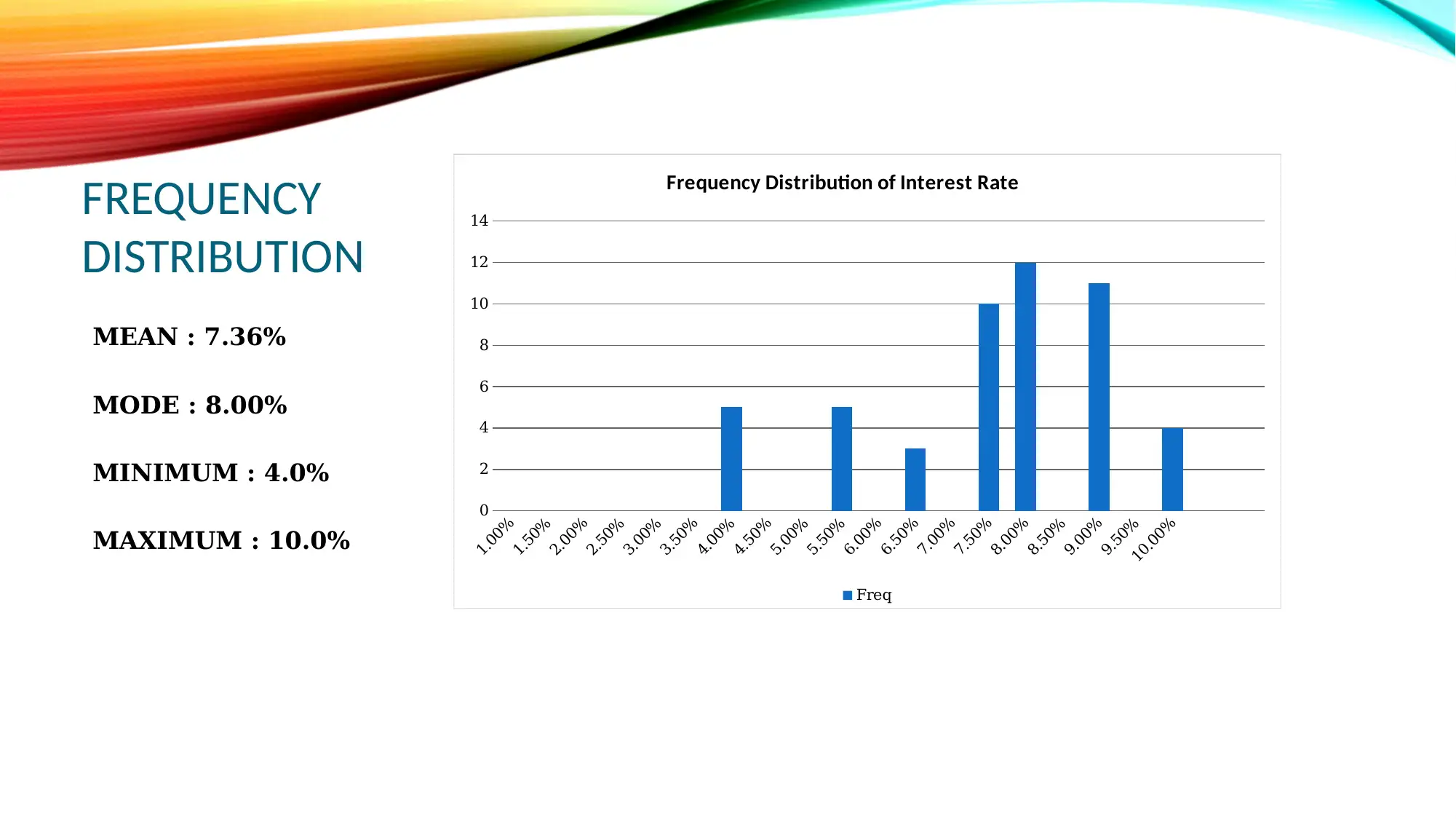

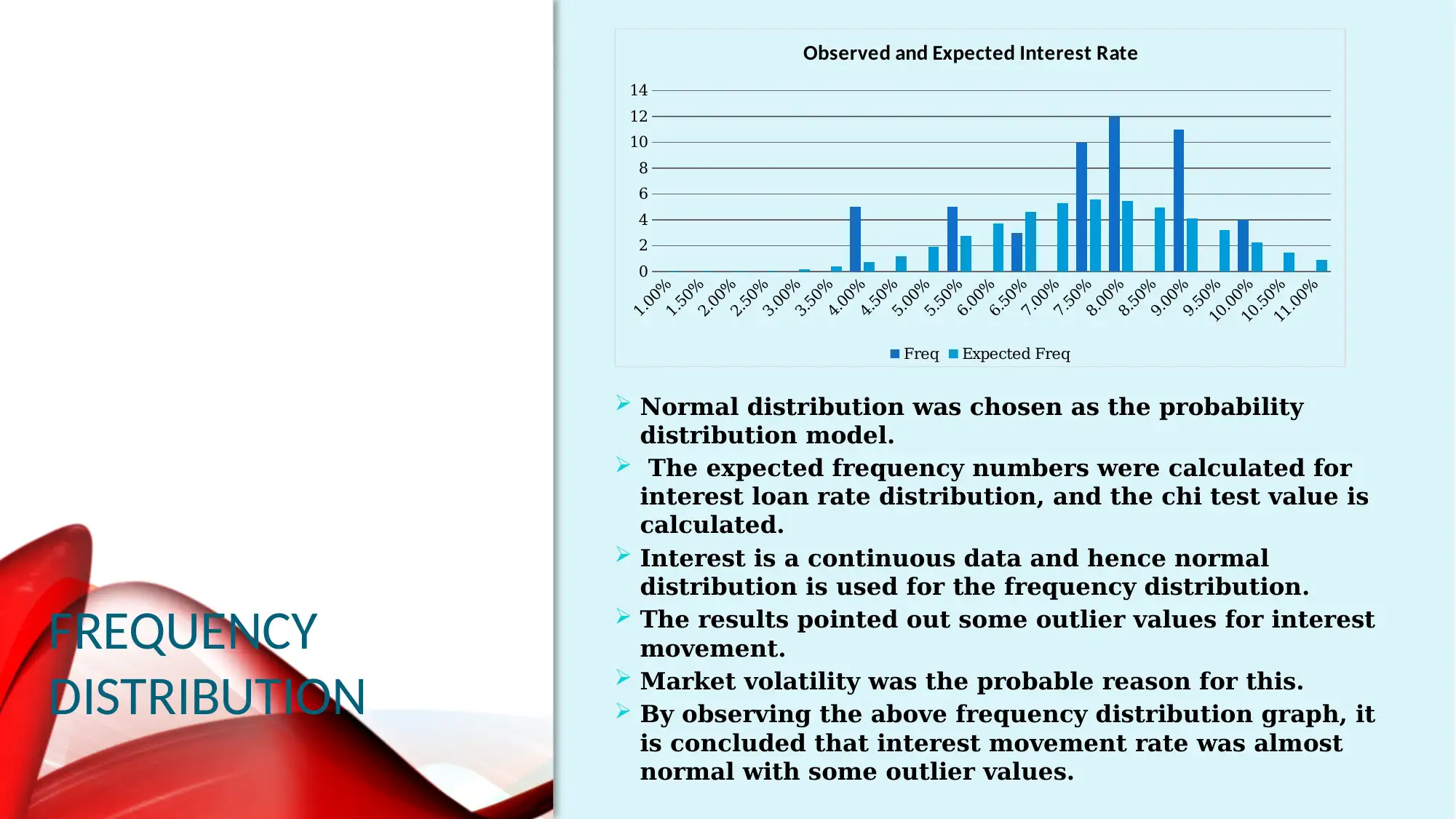

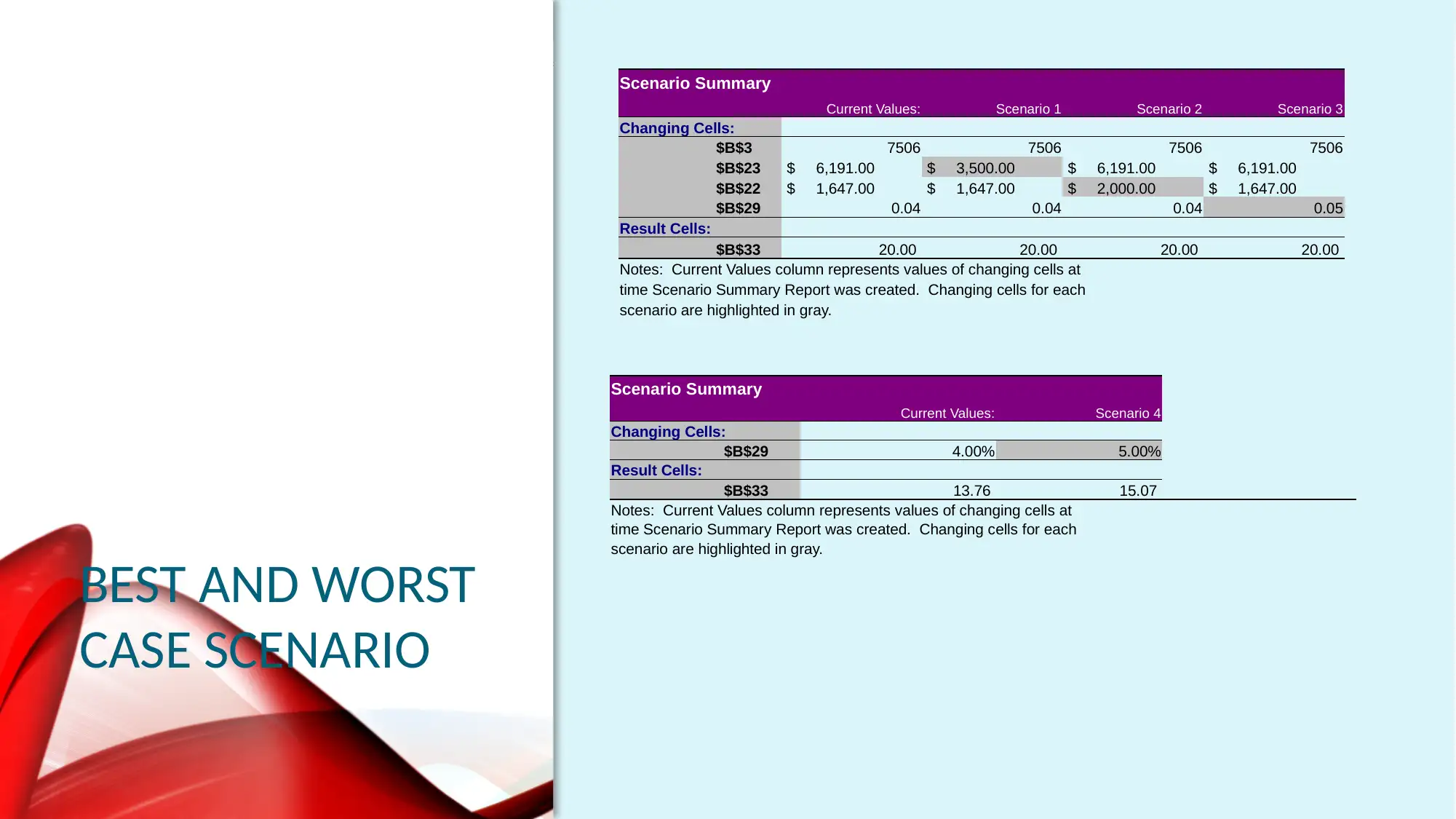

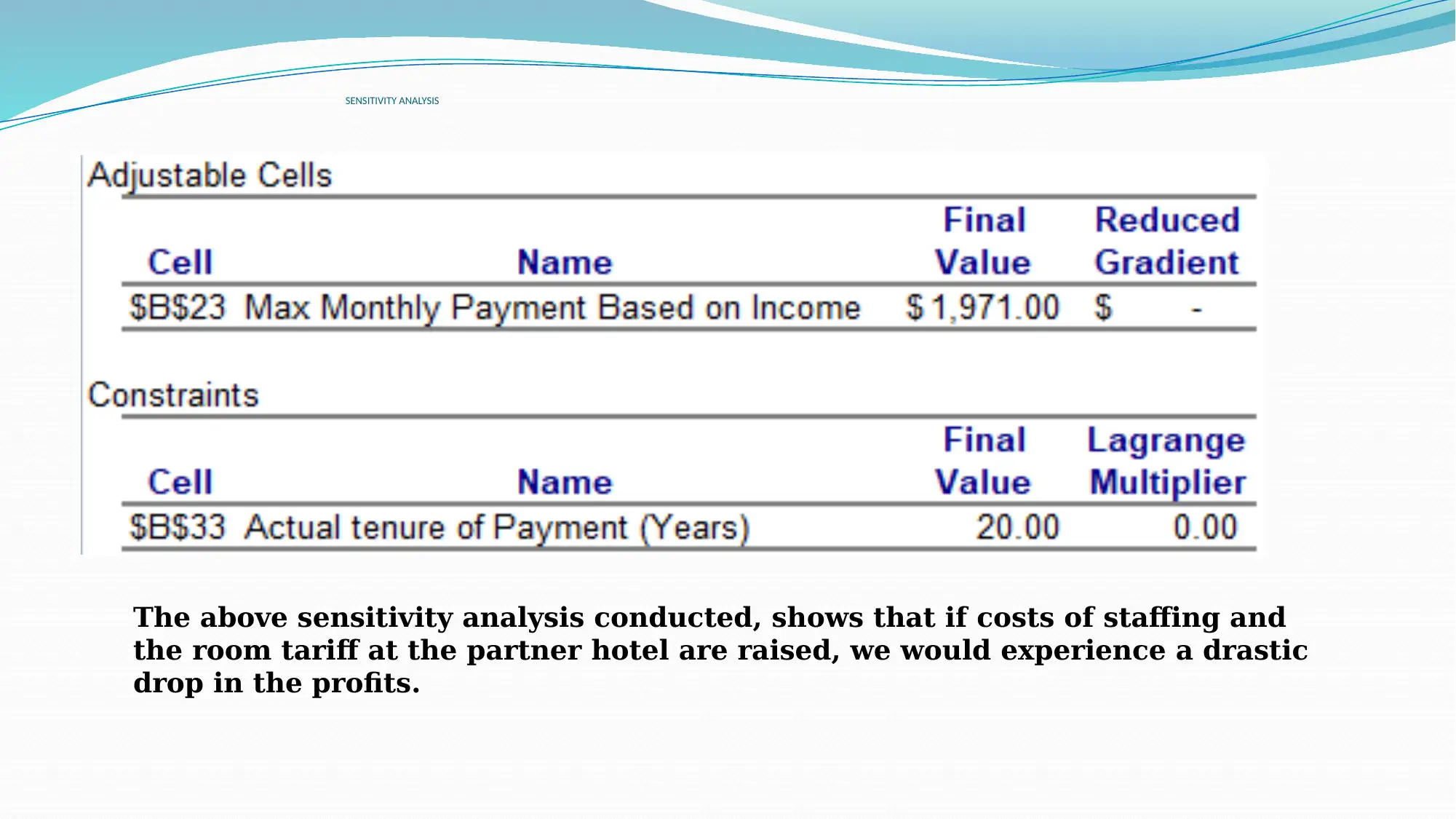

This report presents a decision model for analyzing mortgage loan decisions within a business analytics context. The model incorporates fixed inputs like monthly expenses, stochastic variables such as interest rates and loan terms, and decision variables including total monthly cost and maximum monthly payment. Scenario analysis explores the impact of changes in salary, monthly costs, and interest rates on loan affordability and tenure. Sensitivity analysis identifies key risk factors, primarily monthly costs and interest rates, affecting loan eligibility and monthly payments. The report concludes with recommendations such as increasing the number of borrowers, reducing monthly costs, and taking advantage of lower interest rates to improve loan terms. This assignment is available on Desklib, a platform offering study tools for students.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.