Diploma of Mortgage Broking and Finance: Loan Application Report

VerifiedAdded on 2021/06/17

|36

|8274

|289

Report

AI Summary

This report presents a comprehensive analysis of loan applications within the context of a Diploma of Mortgage Broking and Finance. It meticulously examines a loan submission form, detailing borrower information, including personal and financial backgrounds, and the purpose of the loan. The report assesses the details of the facility, fund positions, servicing capacity, and security offered. It further delves into risk assessment, providing recommendations for the client. The assignment also includes a case study on entrepreneurs seeking a business loan for expansion, addressing questions related to their financial situation, investment strategies, and risk tolerance. The report covers various aspects of financial planning, investment, and risk management within the mortgage broking and finance domain.

Running head: DIPLOMA OF MORTGAGE BROKING AND FINANCE

Diploma of Mortgage Broking and Finance

Name of the Student:

Name of the University:

Author’s Note:

Diploma of Mortgage Broking and Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Table of Contents

Assignment 1...................................................................................................................................2

Assignment 2...................................................................................................................................8

Part A...........................................................................................................................................8

Part B.........................................................................................................................................14

Assignment 3.................................................................................................................................18

Assignment 4.................................................................................................................................23

Assignment 5.................................................................................................................................33

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Table of Contents

Assignment 1...................................................................................................................................2

Assignment 2...................................................................................................................................8

Part A...........................................................................................................................................8

Part B.........................................................................................................................................14

Assignment 3.................................................................................................................................18

Assignment 4.................................................................................................................................23

Assignment 5.................................................................................................................................33

2

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Assignment 1

This form in relation to the loan submission gives out all the precise information that is

vital for the applicants in order to make an apply for the loan so that precise assessment can be

done after which the loan application can either be sanctioned or can be disallowed. All the

aspects in relation to the loan application for Mrs and Mrs Bisset is presented as follows:

Borrower Details

Name Andrew Mark Bisset Jane Elizabeth Bisset

Salutation Mr Bisset Mrs Bisset

Age 52 50

Marital status Married Married

Home address Currumbin Close,

Carindale QLD 4152

Currumbin Close, Carindale QLD 4152

Health Good Good

Smoker No No

Occupation Business Business Partner

Projected retirement age Not thought about it Not thought about it

The phone number of the appointed accountant for the couple who is Ainslie and Partners

is 07 3349 9999.

Background of the Client

Andrew Bisset is known to be a real estate agent and has been in this profession for over

20 years and on the other hand his wife has been working with him. They have 6 shops in

Belmont. They even have a shopping centre that is registered under Bisset Family Trust. The

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Assignment 1

This form in relation to the loan submission gives out all the precise information that is

vital for the applicants in order to make an apply for the loan so that precise assessment can be

done after which the loan application can either be sanctioned or can be disallowed. All the

aspects in relation to the loan application for Mrs and Mrs Bisset is presented as follows:

Borrower Details

Name Andrew Mark Bisset Jane Elizabeth Bisset

Salutation Mr Bisset Mrs Bisset

Age 52 50

Marital status Married Married

Home address Currumbin Close,

Carindale QLD 4152

Currumbin Close, Carindale QLD 4152

Health Good Good

Smoker No No

Occupation Business Business Partner

Projected retirement age Not thought about it Not thought about it

The phone number of the appointed accountant for the couple who is Ainslie and Partners

is 07 3349 9999.

Background of the Client

Andrew Bisset is known to be a real estate agent and has been in this profession for over

20 years and on the other hand his wife has been working with him. They have 6 shops in

Belmont. They even have a shopping centre that is registered under Bisset Family Trust. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

DIPLOMA OF MORTGAGE BROKING AND FINANCE

overall value of the property is $1,450,000 and this value has been taken 2 years ago. The couple

have a mortgage at ANZ Bank with a value of $ 625,000. The couple have rented out five shops

and the value is $96,000 and the last shop is utilised by Mr Bisset for their own business and for

the use, the company pays a rent of $42,000 annually in the family trust. The rent paid by the

company has been paying higher than the actual fair market rental value as the rent amount is

$20,000. Mr Bisset is a specialised real agent and is expertise in the field of commercial and

industrial properties. Mr Bisset draws a gross salary of $78,000 from the company and further

more withdraws $55,000 from the partnership business with Joseph Hooper.

The business was founded in the last financial year and their aim had been to acquire the

real estate market. This business was previously operated with the help of the partnership

between Mr Bisset and Joseph Hooper. Bisset Real Estate took over the business after Joseph

retired and therefore at the current time period, Andrew Bisset is the only director for the

existing business.

On the other hand, Mrs Jane Bisset had earlier been a property manager and she had been

working as a property manager since the partnership agency was taken over by Bisset Real

Estate Pty. She on the other hand withdraws a salary of $43,000.

Purpose of the loan

The couple are having the idea of applying for the loan as the couple as well as the

company has the intention of buying a property of 3000 m2 because of the fact that this land is

closer to their shopping centre and the couple have a plan holding into the land for the next 2

years and thereafter wait for the purpose of rezoning. The value of the land is $600,000 and it is

seen that is land was previously under the State Government Dental and Health Care Centre but

DIPLOMA OF MORTGAGE BROKING AND FINANCE

overall value of the property is $1,450,000 and this value has been taken 2 years ago. The couple

have a mortgage at ANZ Bank with a value of $ 625,000. The couple have rented out five shops

and the value is $96,000 and the last shop is utilised by Mr Bisset for their own business and for

the use, the company pays a rent of $42,000 annually in the family trust. The rent paid by the

company has been paying higher than the actual fair market rental value as the rent amount is

$20,000. Mr Bisset is a specialised real agent and is expertise in the field of commercial and

industrial properties. Mr Bisset draws a gross salary of $78,000 from the company and further

more withdraws $55,000 from the partnership business with Joseph Hooper.

The business was founded in the last financial year and their aim had been to acquire the

real estate market. This business was previously operated with the help of the partnership

between Mr Bisset and Joseph Hooper. Bisset Real Estate took over the business after Joseph

retired and therefore at the current time period, Andrew Bisset is the only director for the

existing business.

On the other hand, Mrs Jane Bisset had earlier been a property manager and she had been

working as a property manager since the partnership agency was taken over by Bisset Real

Estate Pty. She on the other hand withdraws a salary of $43,000.

Purpose of the loan

The couple are having the idea of applying for the loan as the couple as well as the

company has the intention of buying a property of 3000 m2 because of the fact that this land is

closer to their shopping centre and the couple have a plan holding into the land for the next 2

years and thereafter wait for the purpose of rezoning. The value of the land is $600,000 and it is

seen that is land was previously under the State Government Dental and Health Care Centre but

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

DIPLOMA OF MORTGAGE BROKING AND FINANCE

this centre became obsolete after the building was destroyed. The land has been marked under

the “Special Purpose” but it is seen that the local municipal council has declared the land to be

made use of for the purpose of future use commercially and it is due to the fact that this land has

been declared within the Town Planning Scheme. The land has an address of 43 Belmont Road

and the feature of the land is that there are two frontages and the traffic frequency has been high.

The client has made the contract of buying the property as the trustees of their trust and the

settlement amount to be due within 60 days. The client even wants to gain 100% of the property

value from the loan and an extra $25,000 in order to pay out the financing amount, stamp duty

and the conveyance expenses. A guarantee for the loan that they want to undertake comprises of

the shopping centre and the land they want to purchase. The client has the idea of paying

additional $20,000 in order to pay for the cost for the purpose of re-zoning of the land and

thereafter receiving the approval to build the shopping centre on that land. This is the real plan

for the client in order to take the loan from the desired bank.

Details of the Facility

The land in accordance to which the client is looking forward to take the loan is

discovered to be that the land was in use previously by the State Government for their Dental

Health Care services. The land has been marked for “Special Purpose” by the state government

but on the other hand the local council has declared the land for the purpose of future

commercial property use and therefore has been named as Town Planning Scheme.

Fund position

Fund is one of the significant factor by taking assistance of which the client will be

capable of buying the property which has a value of $600,000 and it is due to this fact that they

DIPLOMA OF MORTGAGE BROKING AND FINANCE

this centre became obsolete after the building was destroyed. The land has been marked under

the “Special Purpose” but it is seen that the local municipal council has declared the land to be

made use of for the purpose of future use commercially and it is due to the fact that this land has

been declared within the Town Planning Scheme. The land has an address of 43 Belmont Road

and the feature of the land is that there are two frontages and the traffic frequency has been high.

The client has made the contract of buying the property as the trustees of their trust and the

settlement amount to be due within 60 days. The client even wants to gain 100% of the property

value from the loan and an extra $25,000 in order to pay out the financing amount, stamp duty

and the conveyance expenses. A guarantee for the loan that they want to undertake comprises of

the shopping centre and the land they want to purchase. The client has the idea of paying

additional $20,000 in order to pay for the cost for the purpose of re-zoning of the land and

thereafter receiving the approval to build the shopping centre on that land. This is the real plan

for the client in order to take the loan from the desired bank.

Details of the Facility

The land in accordance to which the client is looking forward to take the loan is

discovered to be that the land was in use previously by the State Government for their Dental

Health Care services. The land has been marked for “Special Purpose” by the state government

but on the other hand the local council has declared the land for the purpose of future

commercial property use and therefore has been named as Town Planning Scheme.

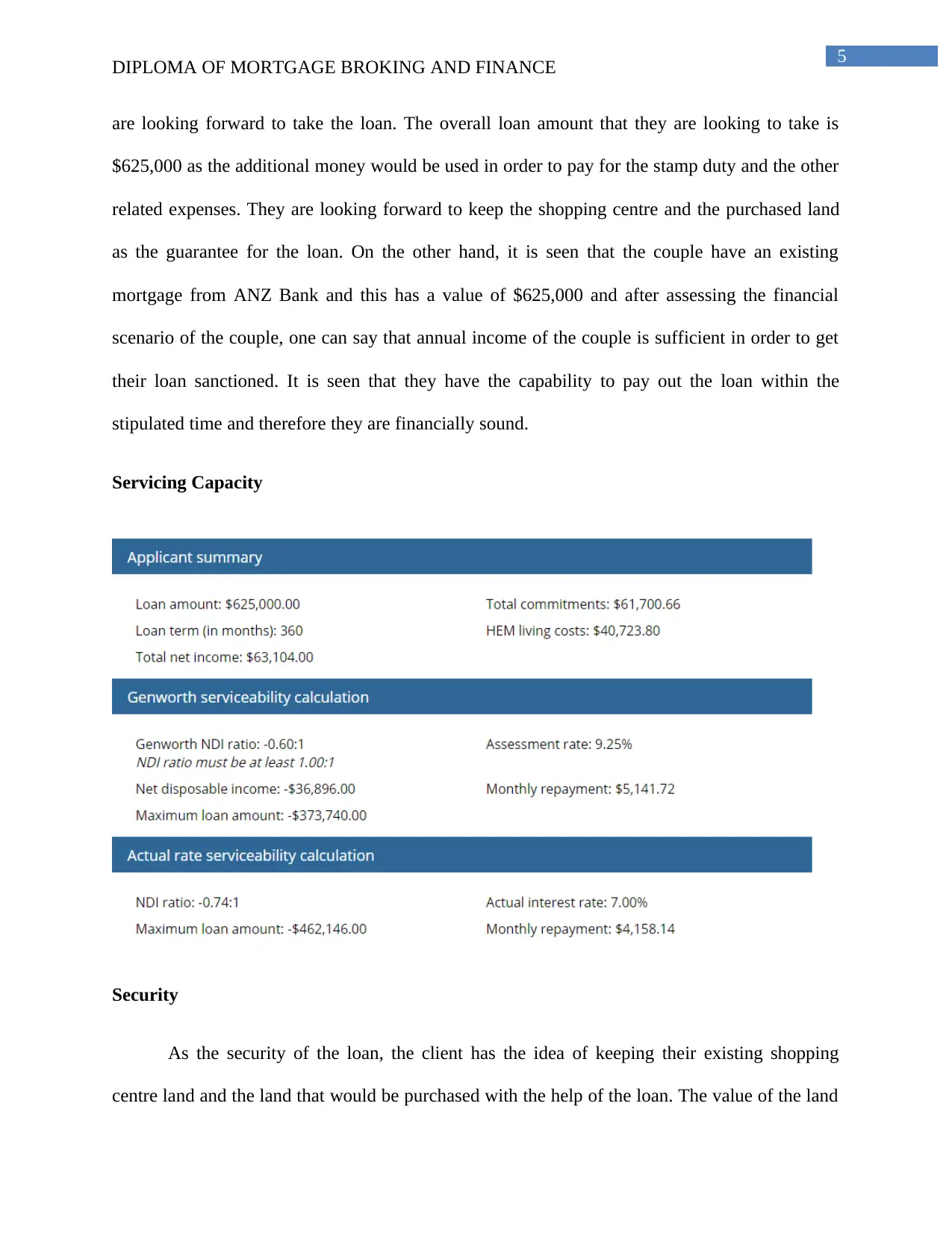

Fund position

Fund is one of the significant factor by taking assistance of which the client will be

capable of buying the property which has a value of $600,000 and it is due to this fact that they

5

DIPLOMA OF MORTGAGE BROKING AND FINANCE

are looking forward to take the loan. The overall loan amount that they are looking to take is

$625,000 as the additional money would be used in order to pay for the stamp duty and the other

related expenses. They are looking forward to keep the shopping centre and the purchased land

as the guarantee for the loan. On the other hand, it is seen that the couple have an existing

mortgage from ANZ Bank and this has a value of $625,000 and after assessing the financial

scenario of the couple, one can say that annual income of the couple is sufficient in order to get

their loan sanctioned. It is seen that they have the capability to pay out the loan within the

stipulated time and therefore they are financially sound.

Servicing Capacity

Security

As the security of the loan, the client has the idea of keeping their existing shopping

centre land and the land that would be purchased with the help of the loan. The value of the land

DIPLOMA OF MORTGAGE BROKING AND FINANCE

are looking forward to take the loan. The overall loan amount that they are looking to take is

$625,000 as the additional money would be used in order to pay for the stamp duty and the other

related expenses. They are looking forward to keep the shopping centre and the purchased land

as the guarantee for the loan. On the other hand, it is seen that the couple have an existing

mortgage from ANZ Bank and this has a value of $625,000 and after assessing the financial

scenario of the couple, one can say that annual income of the couple is sufficient in order to get

their loan sanctioned. It is seen that they have the capability to pay out the loan within the

stipulated time and therefore they are financially sound.

Servicing Capacity

Security

As the security of the loan, the client has the idea of keeping their existing shopping

centre land and the land that would be purchased with the help of the loan. The value of the land

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

DIPLOMA OF MORTGAGE BROKING AND FINANCE

where the shopping centre is situated has been $1,450,000 two years earlier and hence, this will

be adequate as collateral in order to pay for the loan in case the couple is unable to pay for the

same.

Risk Assessment

The extent of risk for the client has been low mainly because of the fact that they have

their own business and being a business that is acquired from a well established business it is

seen that the level of profit earned and the income received is high. The risk related to them has

been the health factor for the couple as they are middle aged now and anything in their health can

have an impact on their business and their activities as well. The changes in the tax regulations or

unprecedented economic events can have an impact their business. Therefore, the recognition of

these risks would be helpful in the reduction of risks and thereby have a peaceful future life

ahead. This would be helpful in the pay out for the loan and the mortgage that are existent to

them and even maintain their level of income.

Recommendations

The client need to purchase an insurance for their business and individually so that this

insurance would compensate for the any kind of unexpected events. All the documents related to

the client need to be presented in an orderly manner and all financial documents of the collateral

provided needs to be submitted beforehand. The couple need to increase their profit level and

income and should even assess their financial condition from time to time in order to maintain

balance in their portfolio.

Attachment

DIPLOMA OF MORTGAGE BROKING AND FINANCE

where the shopping centre is situated has been $1,450,000 two years earlier and hence, this will

be adequate as collateral in order to pay for the loan in case the couple is unable to pay for the

same.

Risk Assessment

The extent of risk for the client has been low mainly because of the fact that they have

their own business and being a business that is acquired from a well established business it is

seen that the level of profit earned and the income received is high. The risk related to them has

been the health factor for the couple as they are middle aged now and anything in their health can

have an impact on their business and their activities as well. The changes in the tax regulations or

unprecedented economic events can have an impact their business. Therefore, the recognition of

these risks would be helpful in the reduction of risks and thereby have a peaceful future life

ahead. This would be helpful in the pay out for the loan and the mortgage that are existent to

them and even maintain their level of income.

Recommendations

The client need to purchase an insurance for their business and individually so that this

insurance would compensate for the any kind of unexpected events. All the documents related to

the client need to be presented in an orderly manner and all financial documents of the collateral

provided needs to be submitted beforehand. The couple need to increase their profit level and

income and should even assess their financial condition from time to time in order to maintain

balance in their portfolio.

Attachment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Address Proof of the client

Financial and income statement of the applicant

Documents of the collateral

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Address Proof of the client

Financial and income statement of the applicant

Documents of the collateral

8

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Assignment 2

Part A

List of Questions

Question 1: What are the annual income and the present age of Ray and Steve?

Question 2: What are the key income sources of two of you?

Question 3: Why are you interested in growing your business?

Question 4: What sort of income do you expect to create from the business?

Question 5: What is the present budget you need to start the business?

Question 6: What are yearly expenses?

Question 7: Please cite the aims and objectives for developing your business

Question 8: Please explain the need of the investments you are looking forward to

Question 9: What is your present bank balance?

Question 10: What is the basic capital required to assist the expansion?

Question 11: What is the role you want us to perform?

Question 12: Have you followed the investment rules that are disclosed by the Australian government?

Question 13: What would be your actions if the investment amount reduces in next 40 years?

Question 14: Explain the current demands of going into new investment for the business

Question 15: What is the actual source of the income for your business?

Question 16: What do you desire; short-term gains or long-term returns?

Question 17: Does any sort of short-term risk have an impact on the development of the business portfolio?

Question 18: Specify the actions taken during the investment loss

Question 19: Explain your investment strategy, which is being that is currently being undertaken during the

procedure of making decisions in order to mitigate risk

Question 20: How much effectively do you have knowledge about the demands in the investment market?

Question 21: Kindly specify the past decisions associated to investment and its effect on profit

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Assignment 2

Part A

List of Questions

Question 1: What are the annual income and the present age of Ray and Steve?

Question 2: What are the key income sources of two of you?

Question 3: Why are you interested in growing your business?

Question 4: What sort of income do you expect to create from the business?

Question 5: What is the present budget you need to start the business?

Question 6: What are yearly expenses?

Question 7: Please cite the aims and objectives for developing your business

Question 8: Please explain the need of the investments you are looking forward to

Question 9: What is your present bank balance?

Question 10: What is the basic capital required to assist the expansion?

Question 11: What is the role you want us to perform?

Question 12: Have you followed the investment rules that are disclosed by the Australian government?

Question 13: What would be your actions if the investment amount reduces in next 40 years?

Question 14: Explain the current demands of going into new investment for the business

Question 15: What is the actual source of the income for your business?

Question 16: What do you desire; short-term gains or long-term returns?

Question 17: Does any sort of short-term risk have an impact on the development of the business portfolio?

Question 18: Specify the actions taken during the investment loss

Question 19: Explain your investment strategy, which is being that is currently being undertaken during the

procedure of making decisions in order to mitigate risk

Question 20: How much effectively do you have knowledge about the demands in the investment market?

Question 21: Kindly specify the past decisions associated to investment and its effect on profit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Question 22: Please identify the conciliation priority level of you have

Question 24: Kindly explain the criteria you desire to gain success

Question 25: Highlight the procedure of borrowing undertaken from your side for growing the business

Question 26: Explain investment method of your business

Question 27: Identify the present financial scenario of the business

Question 28: What are the other investments that you may undertake in future?

Question 29: What qualities and qualifications are demanded by you from the consultants?

Question 30: Are there any geographical limitations of your business?

Question 31: What are the geographical advantages of your business?

Question 32: Do you have the ability to maintain the extent of income till the time of loan?

Question 33: What is your risk tolerance?

Question 34: Address your current disposable income

Report

This document is given to the customer to gain knowledge of their actual position, the

demand for taking the loan in order to develop their business and thereby raise their extent of

profit.

The case study is related to approval of the loan for Steve and Ray who are entrepreneurs

for a transport company and have been having a good business in the Australian economy. They

are in the intention of growing their business and therefore has been looking to start a new

business where trailers would be given out as rent and other tools would even be provided to the

current firm of Steve and Ray, which would be helpful in the development of the business

performance for both the companies and thereby there would be a rise in the extent of income as

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Question 22: Please identify the conciliation priority level of you have

Question 24: Kindly explain the criteria you desire to gain success

Question 25: Highlight the procedure of borrowing undertaken from your side for growing the business

Question 26: Explain investment method of your business

Question 27: Identify the present financial scenario of the business

Question 28: What are the other investments that you may undertake in future?

Question 29: What qualities and qualifications are demanded by you from the consultants?

Question 30: Are there any geographical limitations of your business?

Question 31: What are the geographical advantages of your business?

Question 32: Do you have the ability to maintain the extent of income till the time of loan?

Question 33: What is your risk tolerance?

Question 34: Address your current disposable income

Report

This document is given to the customer to gain knowledge of their actual position, the

demand for taking the loan in order to develop their business and thereby raise their extent of

profit.

The case study is related to approval of the loan for Steve and Ray who are entrepreneurs

for a transport company and have been having a good business in the Australian economy. They

are in the intention of growing their business and therefore has been looking to start a new

business where trailers would be given out as rent and other tools would even be provided to the

current firm of Steve and Ray, which would be helpful in the development of the business

performance for both the companies and thereby there would be a rise in the extent of income as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

DIPLOMA OF MORTGAGE BROKING AND FINANCE

the money would remain within the two businesses. This is even helpful for the existing

company to reduce their reliance on the external suppliers. The issue that is to be taken into

consideration that there are numerous lending companies from where they can take the loan but

the selection of the company would be based on the objectives of the customers.

Security

The transport company has been operational for over 34 months and therefore gains

significant amount of returns. The financial statement of the company has been appreciable and

the profit attained is ideal for them to get their loan sanctioned. The security that would be given

out by the clients will be their entire transpiration business and even the property over which the

company is established. The overall income and the value of property will be sufficient to be the

collateral for the loan.

Facility

The customers have the aim of growing their business and in order to develop their

existing business and in order to do the same is looking to start a trailer renting business and the

rent will be given to the existing company of the customer. This in a way will be helpful in the

rise in the extent of profit for the business as it is seen that the external suppliers will not be

dependent on by the current business. In order to start the business they are looking to take a land

on lease and the rent will be $6000 per month.

Lender Details

The details for the precise lender are given as follows:

DIPLOMA OF MORTGAGE BROKING AND FINANCE

the money would remain within the two businesses. This is even helpful for the existing

company to reduce their reliance on the external suppliers. The issue that is to be taken into

consideration that there are numerous lending companies from where they can take the loan but

the selection of the company would be based on the objectives of the customers.

Security

The transport company has been operational for over 34 months and therefore gains

significant amount of returns. The financial statement of the company has been appreciable and

the profit attained is ideal for them to get their loan sanctioned. The security that would be given

out by the clients will be their entire transpiration business and even the property over which the

company is established. The overall income and the value of property will be sufficient to be the

collateral for the loan.

Facility

The customers have the aim of growing their business and in order to develop their

existing business and in order to do the same is looking to start a trailer renting business and the

rent will be given to the existing company of the customer. This in a way will be helpful in the

rise in the extent of profit for the business as it is seen that the external suppliers will not be

dependent on by the current business. In order to start the business they are looking to take a land

on lease and the rent will be $6000 per month.

Lender Details

The details for the precise lender are given as follows:

11

DIPLOMA OF MORTGAGE BROKING AND FINANCE

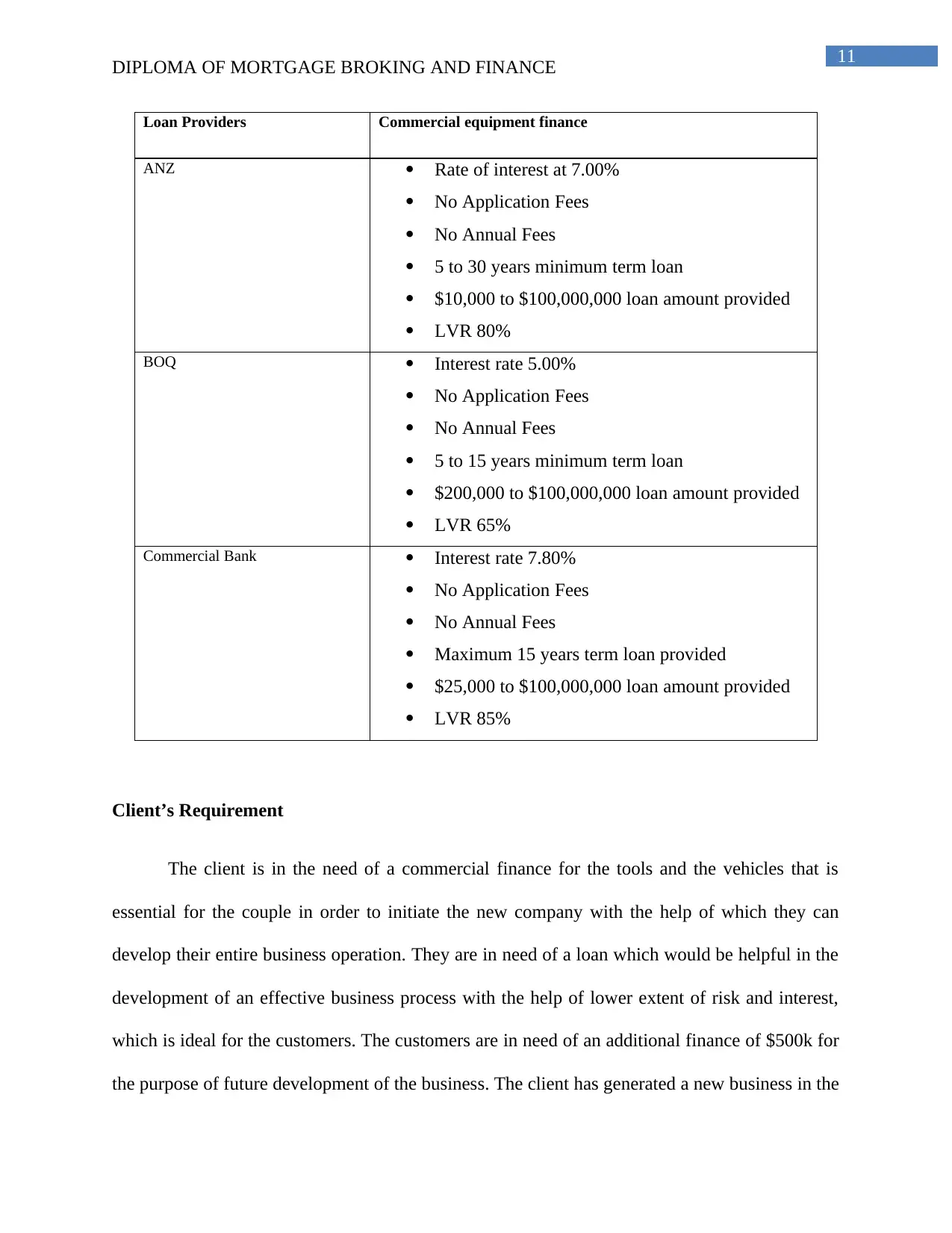

Loan Providers Commercial equipment finance

ANZ Rate of interest at 7.00%

No Application Fees

No Annual Fees

5 to 30 years minimum term loan

$10,000 to $100,000,000 loan amount provided

LVR 80%

BOQ Interest rate 5.00%

No Application Fees

No Annual Fees

5 to 15 years minimum term loan

$200,000 to $100,000,000 loan amount provided

LVR 65%

Commercial Bank Interest rate 7.80%

No Application Fees

No Annual Fees

Maximum 15 years term loan provided

$25,000 to $100,000,000 loan amount provided

LVR 85%

Client’s Requirement

The client is in the need of a commercial finance for the tools and the vehicles that is

essential for the couple in order to initiate the new company with the help of which they can

develop their entire business operation. They are in need of a loan which would be helpful in the

development of an effective business process with the help of lower extent of risk and interest,

which is ideal for the customers. The customers are in need of an additional finance of $500k for

the purpose of future development of the business. The client has generated a new business in the

DIPLOMA OF MORTGAGE BROKING AND FINANCE

Loan Providers Commercial equipment finance

ANZ Rate of interest at 7.00%

No Application Fees

No Annual Fees

5 to 30 years minimum term loan

$10,000 to $100,000,000 loan amount provided

LVR 80%

BOQ Interest rate 5.00%

No Application Fees

No Annual Fees

5 to 15 years minimum term loan

$200,000 to $100,000,000 loan amount provided

LVR 65%

Commercial Bank Interest rate 7.80%

No Application Fees

No Annual Fees

Maximum 15 years term loan provided

$25,000 to $100,000,000 loan amount provided

LVR 85%

Client’s Requirement

The client is in the need of a commercial finance for the tools and the vehicles that is

essential for the couple in order to initiate the new company with the help of which they can

develop their entire business operation. They are in need of a loan which would be helpful in the

development of an effective business process with the help of lower extent of risk and interest,

which is ideal for the customers. The customers are in need of an additional finance of $500k for

the purpose of future development of the business. The client has generated a new business in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 36

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.