Inventory, Costing & Financial Statement Impact: Motorcycle Holdings

VerifiedAdded on 2023/04/24

|8

|1383

|147

Essay

AI Summary

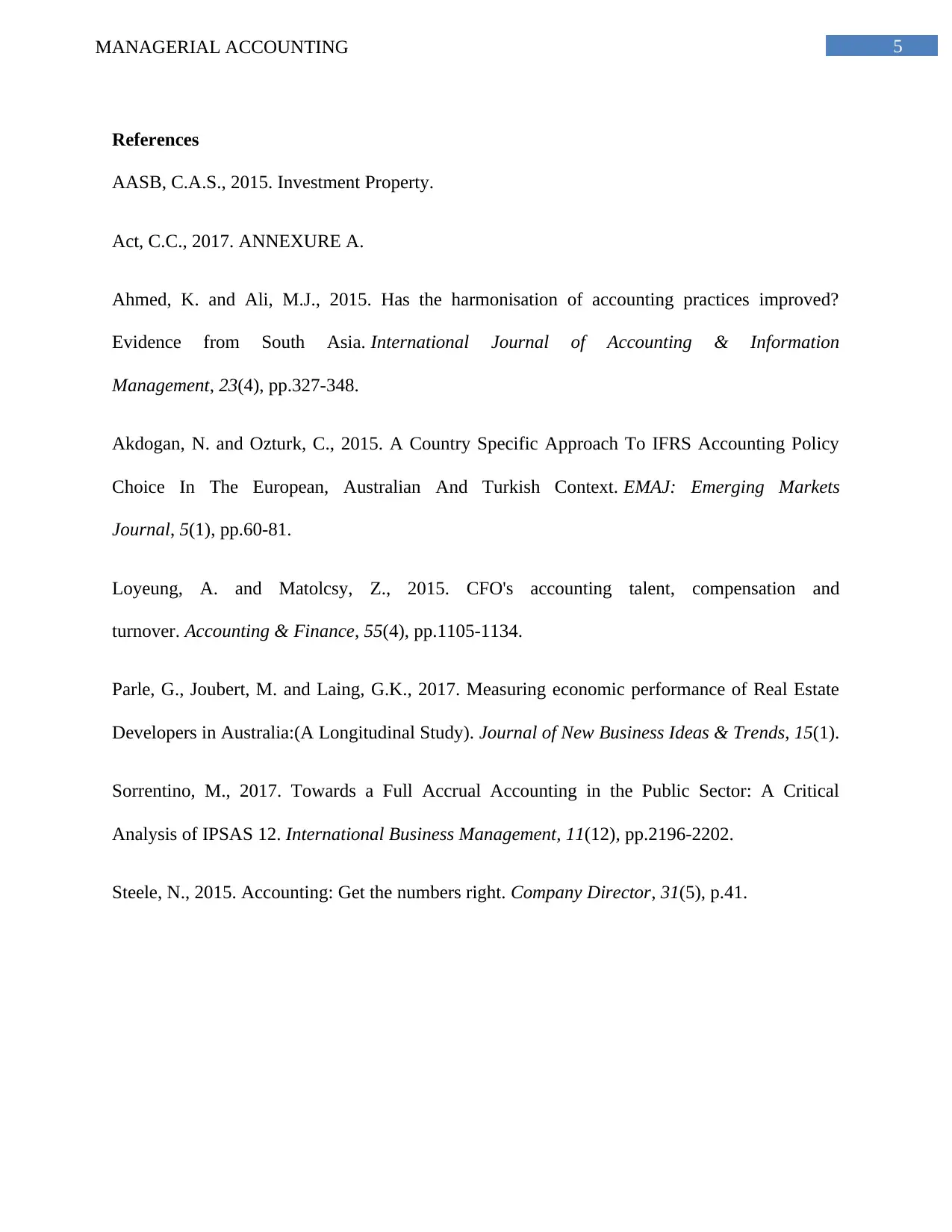

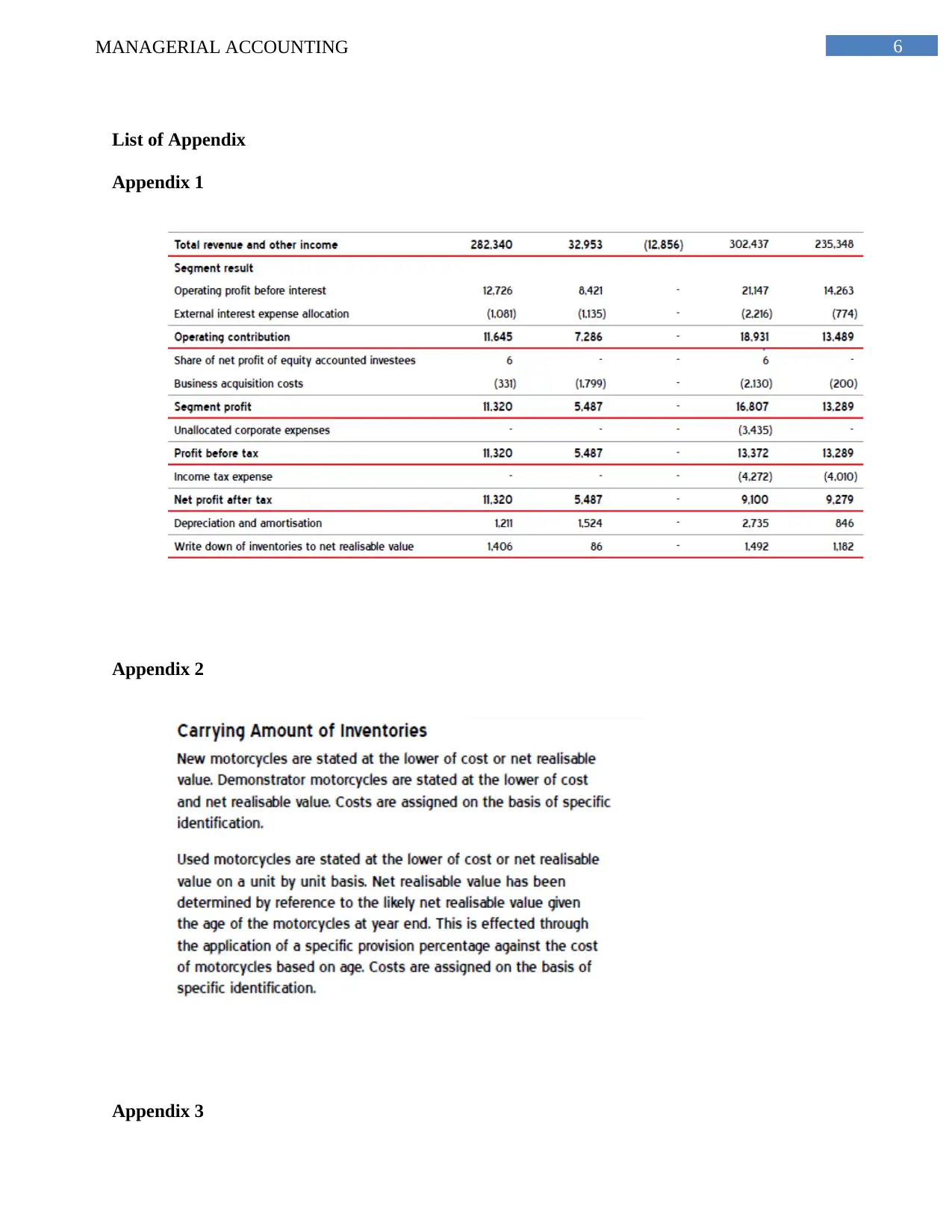

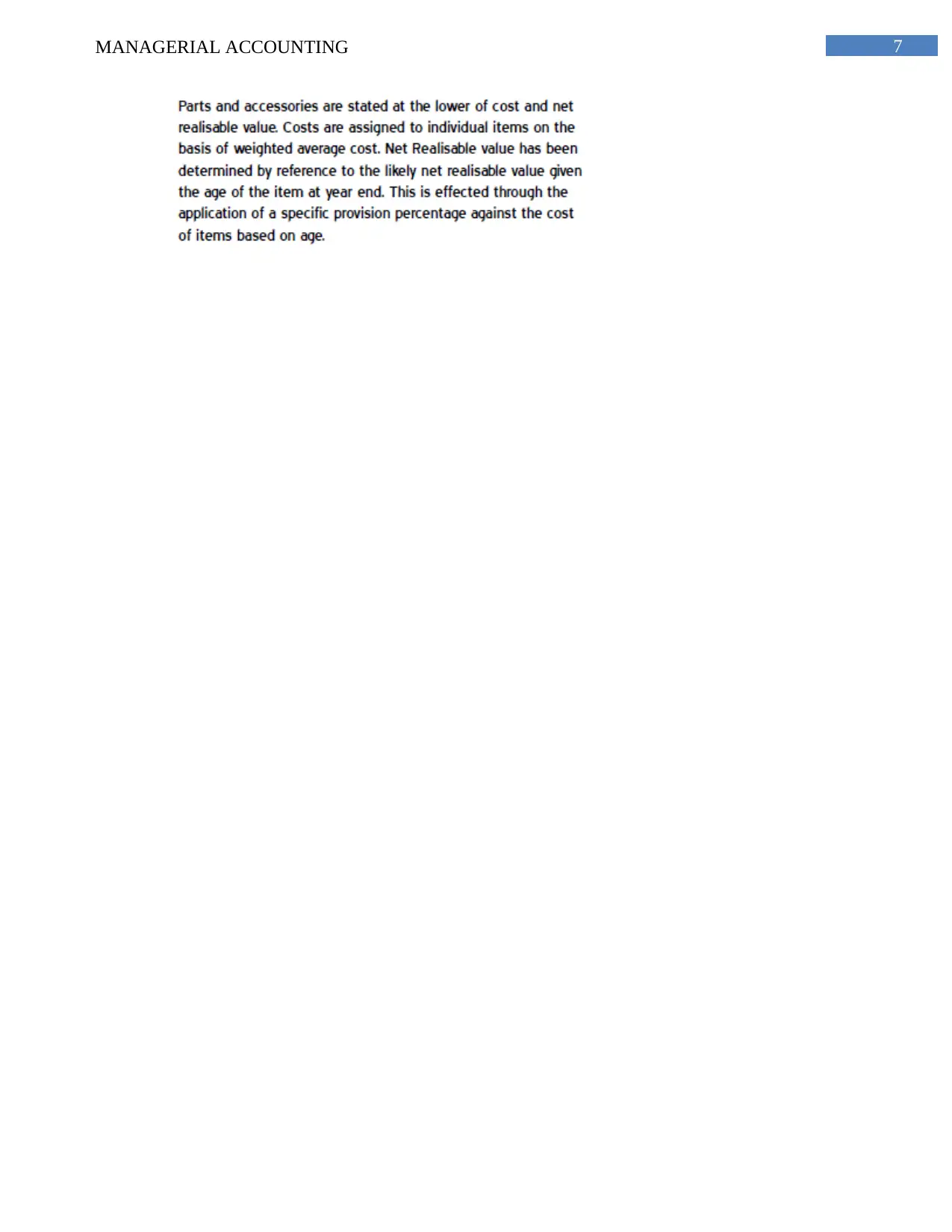

This essay provides a comprehensive analysis of Motorcycle Holdings Limited's inventory management and costing methods, aligning with Australian Accounting Standards, particularly AASB 102. It evaluates the company's inventory measurement practices, highlighting the use of 'writing down the inventory to net realisable value' and the weighted average method. The study identifies the company's costing method as a traditional approach, classifying costs into direct material, direct labor, and overhead, which influences the company's EBIT. The essay further discusses the potential impact of different costing methods on the company's financial statements, noting inaccuracies that may arise from the traditional method's treatment of overhead costs. It concludes by advocating for the implementation of an Activity-Based Costing (ABC) system to address the limitations of the traditional approach and improve the accuracy of cost allocation.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.